Are you considering using HELOC leverage for a down payment on your next property? This strategy can be a powerful tool for real estate investors, but it’s not without risks.

At HELOC360, we’ve seen firsthand how HELOCs can help homeowners tap into their equity for various purposes, including down payments. However, it’s crucial to understand the pros and cons before making this financial decision.

In this post, we’ll explore whether using a HELOC for a down payment is a smart move or a risky gamble.

How HELOCs Can Fund Your Down Payment

Understanding HELOC Basics

A Home Equity Line of Credit (HELOC) allows you to borrow against the available equity in your home, using your house as collateral for the line of credit. It functions similarly to a credit card, but uses your home as collateral. Lenders approve you for a credit limit based on your home’s value and your outstanding mortgage balance. The HELOC typically has two phases: a draw period (usually 10 years) where you can borrow and repay as needed, and a repayment period where you pay back the principal and interest.

Leveraging HELOCs for Down Payments

HELOCs offer a strategic way to fund down payments on new properties. This approach appeals to real estate investors and those looking to purchase a second home. By using a HELOC, you can tap into your current home’s equity to invest in another property. For instance, $100,000 in home equity could potentially cover a 20% down payment on a $500,000 property (a significant boost to your purchasing power).

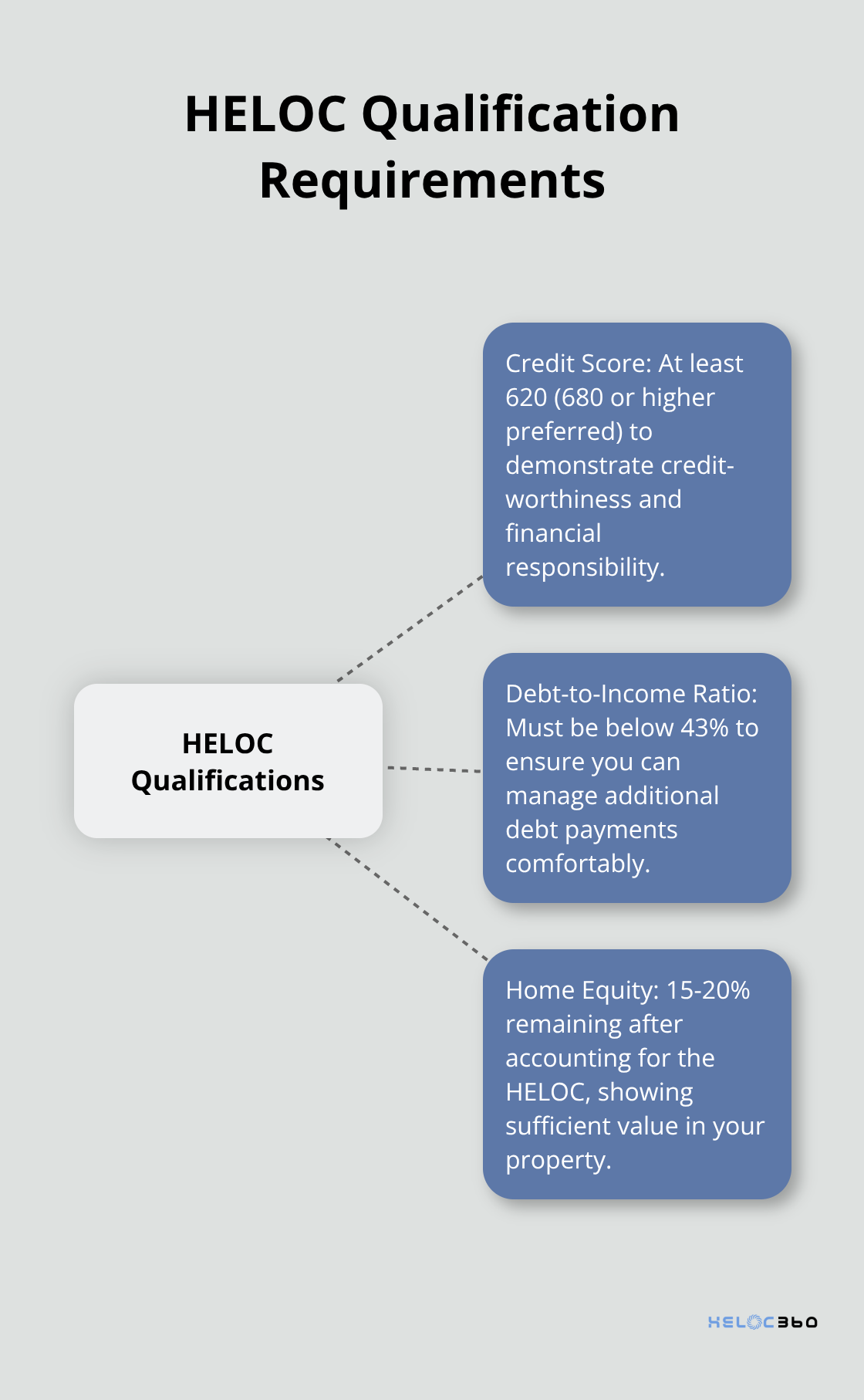

HELOC Qualification Requirements

To qualify for a HELOC, you’ll typically need to meet these criteria:

- Credit score: At least 620 (680 or higher preferred)

- Debt-to-income ratio: Below 43%

- Home equity: 15-20% after accounting for the HELOC

Lenders will also evaluate your income stability and overall financial health. Self-employed individuals might face additional scrutiny and need to provide extra documentation to prove income stability.

Considerations for HELOC Use

While HELOCs can provide a powerful tool for property investment, it’s important to weigh the risks. You’ll put your home at risk as collateral, and market fluctuations could lead to negative equity. Additionally, some lenders might have restrictions on using HELOCs for down payments.

Alternative Down Payment Sources

HELOCs aren’t the only option for funding a down payment. Other alternatives include:

- Savings accounts

- Investment accounts

- Gifts from family members

- Down payment assistance programs

Each option comes with its own set of pros and cons, which you should carefully evaluate based on your financial situation.

As we explore the advantages of HELOCs, including lower rates than other forms of credit and the ability to borrow exactly what you need, in the next section, you’ll gain a clearer picture of whether this strategy aligns with your investment goals.

Why HELOCs Can Be a Smart Choice for Down Payments

Using a Home Equity Line of Credit (HELOC) for a down payment on a new property can serve as a strategic move for many homeowners and investors. This approach allows individuals to expand their real estate portfolios by tapping into their existing home equity. Let’s explore the key advantages of using HELOCs for down payments.

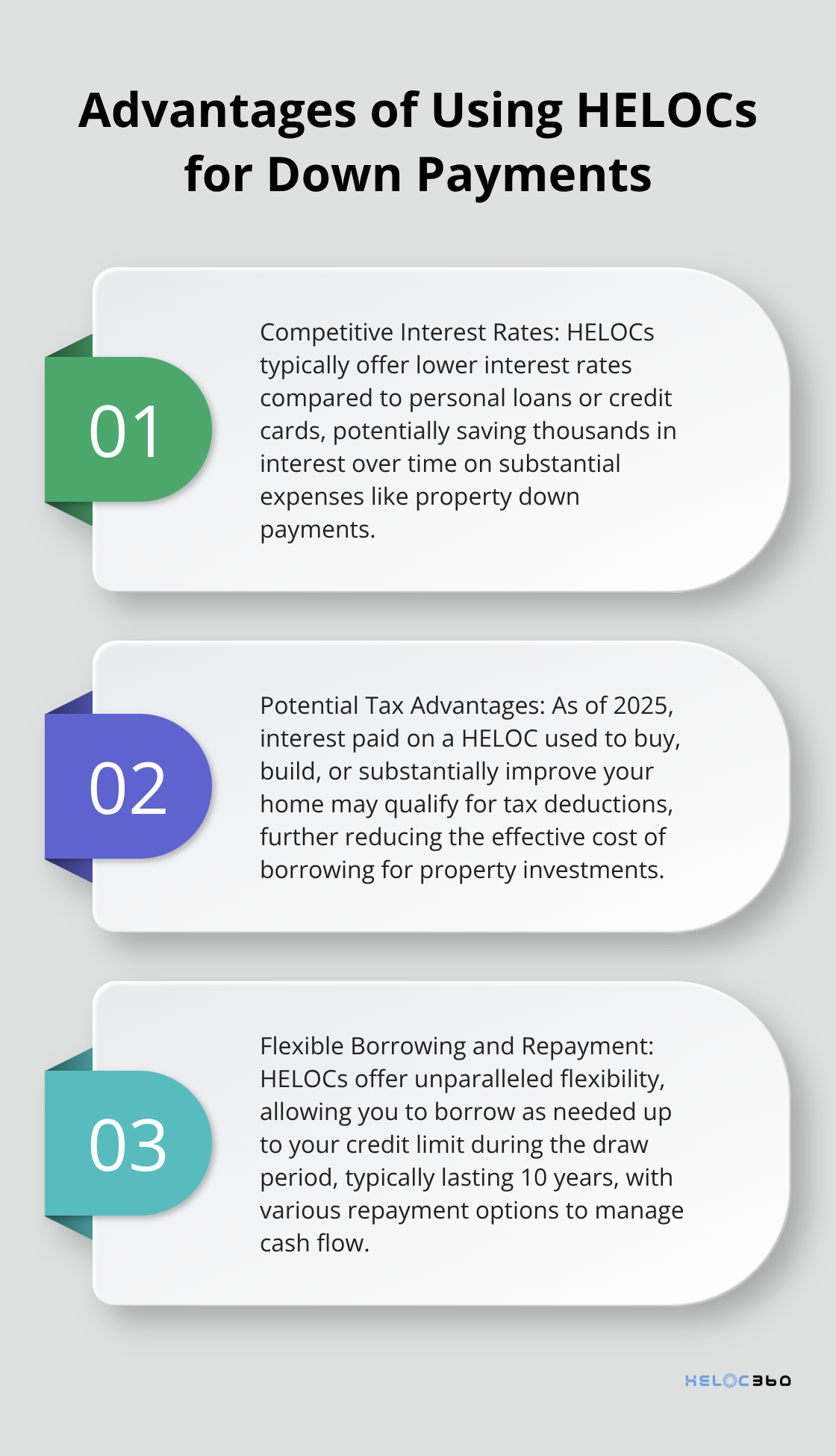

Competitive Interest Rates

HELOCs typically offer lower interest rates compared to personal loans or credit cards. This can result in significant savings over time, especially when compared to the rates often associated with unsecured loans.

For example, on a $50,000 loan over five years, the difference between a HELOC and a personal loan could save you thousands in interest. This makes HELOCs an attractive option for funding substantial expenses like property down payments.

Potential Tax Advantages

While tax laws can change, as of 2025, the interest paid on a HELOC used to buy, build, or substantially improve your home may qualify for tax deductions. This potential tax benefit can further reduce the effective cost of borrowing, making HELOCs even more appealing for property investments.

However, it’s important to consult with a tax professional to understand how these deductions apply to your specific situation. The rules can be complex, and factors such as the total amount of home equity debt and your overall mortgage balance can affect eligibility.

Flexible Borrowing and Repayment

HELOCs offer unparalleled flexibility in both borrowing and repayment. During the draw period (which typically lasts 10 years), you can borrow as much or as little as you need, up to your credit limit. This means you can tailor your borrowing to match your exact down payment requirements.

Repayment terms are equally flexible. Many HELOCs only require interest payments during the draw period, which can help manage cash flow in the short term. However, it’s advisable to consider making principal payments as well to avoid a balloon payment at the end of the draw period.

For instance, if you use a $100,000 HELOC for a down payment on an investment property, you might choose to make interest-only payments during the draw period. This could allow you to direct more funds towards property improvements or other investments.

Leveraging Existing Home Equity

HELOCs allow homeowners to tap into their home’s equity without selling the property or refinancing their entire mortgage. This can be particularly advantageous if you have a low interest rate on your primary mortgage that you want to maintain.

By using a HELOC, you can access the equity you’ve built up over time to invest in additional properties, potentially increasing your overall real estate portfolio and wealth-building opportunities.

While HELOCs offer numerous advantages, they also come with certain risks and considerations. The variable interest rates mean your payments could increase over time, and using your home as collateral puts it at risk if you default on payments. In the next section, we’ll examine these potential risks and important factors to consider when contemplating this strategy.

What Are the Hidden Dangers of Using HELOCs for Down Payments?

The Risk of Losing Your Home

The most serious risk of using a Home Equity Line of Credit (HELOC) for a down payment is the potential loss of your primary residence. HELOCs use your home as collateral. If you default on payments, the lender has the right to foreclose on your property. This risk increases when you use the HELOC funds to purchase another property, as you leverage one asset to acquire another.

A report by CoreLogic states that as of 2023, approximately 62% of homes with mortgages have positive equity. However, market fluctuations can quickly change this scenario. A downturn in the housing market could leave you owing more than your home’s worth, making it difficult to sell or refinance if financial troubles arise.

Impact on Your Debt-to-Income Ratio

Using a HELOC for a down payment can significantly increase your debt-to-income (DTI) ratio. This metric is important for lenders when they assess your creditworthiness for future loans. A higher DTI ratio might make it challenging to qualify for additional credit or favorable interest rates in the future.

For example, if you use a $100,000 HELOC for a down payment on a $500,000 property, you take on not just the new mortgage debt but also the HELOC debt. This could push your DTI ratio above the 43% threshold that many lenders consider the maximum for approving a mortgage.

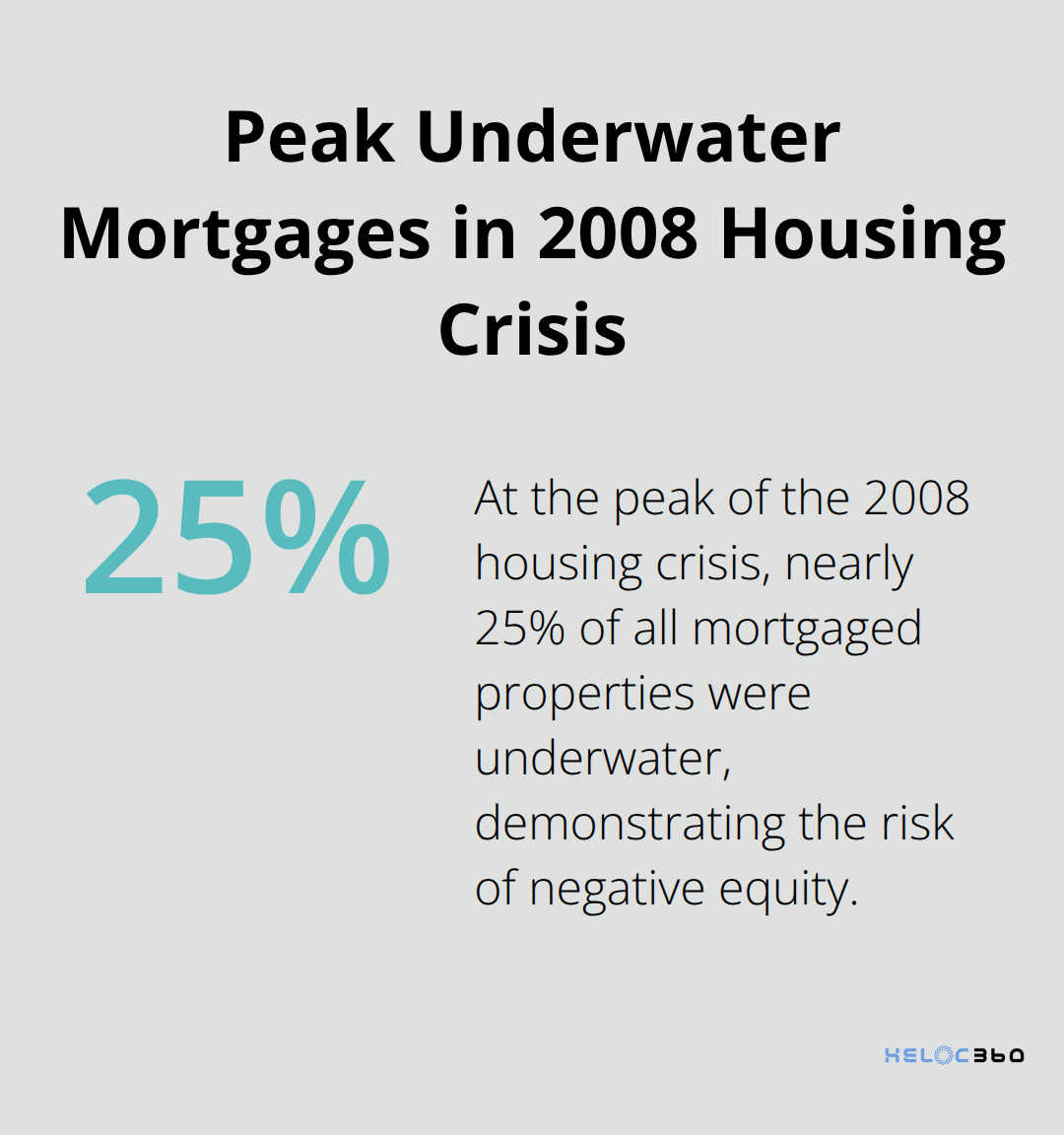

The Specter of Negative Equity

The housing market is cyclical, and property values can decrease. If you use a HELOC to fund a down payment and property values decline, you could find yourself in a negative equity situation on both properties. This scenario (often referred to as being “underwater” on your mortgage) can severely limit your financial flexibility.

During the 2008 housing crisis, millions of homeowners found themselves in this predicament. While current market conditions differ, it’s a risk that shouldn’t be overlooked. The Federal Reserve Bank of New York reported that at the peak of the crisis, nearly 25% of all mortgaged properties were underwater.

Lender Restrictions and Requirements

Not all lenders view HELOCs as an acceptable source for down payments. Some may require you to have the HELOC for a certain period before using it for a down payment, while others might not allow it at all for certain types of properties (such as investment properties).

Additionally, using a HELOC for a down payment might affect the terms of your new mortgage. Some lenders may offer less favorable rates or terms if they know the down payment comes from a HELOC rather than savings or other sources.

It’s important to be transparent with potential lenders about your plans to use a HELOC for a down payment. Failing to disclose this information could be considered mortgage fraud, which carries severe legal consequences.

Variable Interest Rates

HELOCs typically come with variable interest rates, which means your payments could increase over time. This adds an element of uncertainty to your financial planning. If interest rates rise significantly, you might find it difficult to manage the payments on both your primary mortgage and the HELOC.

Final Thoughts

HELOC leverage for down payments offers advantages but also carries risks. Lower interest rates and flexible borrowing appeal to many homeowners, yet the potential loss of your primary residence and increased debt-to-income ratio demand careful consideration. A thorough assessment of your financial situation, future income prospects, and risk tolerance is essential before proceeding with this strategy.

Alternatives to HELOCs exist for those who decide against this option. Traditional savings methods, investment accounts, or down payment assistance programs might better suit your circumstances. These alternatives often involve less risk and don’t put your primary residence in jeopardy.

We at HELOC360 can provide guidance and connect you with suitable lenders if you’re considering a HELOC for a down payment. Our platform helps homeowners make informed decisions about leveraging their home equity. Visit HELOC360 to explore your options and ensure you have the knowledge to maximize your property’s value.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.