Navigating the world of HELOC deductions can be tricky, especially with recent tax law changes.

At HELOC360, we’ve seen firsthand how understanding these deductions can significantly impact your financial strategy.

This guide will walk you through the latest updates for 2025, helping you maximize your tax benefits and make informed decisions about your HELOC.

What Are the Latest HELOC Tax Rules for 2025?

The Current State of HELOC Tax Deductions

The Tax Cuts and Jobs Act (TCJA) of 2017 changed how HELOC interest is treated for tax purposes. In 2025, you can only deduct interest on up to $750,000 worth of qualified home equity loans (if married, filing jointly) if you use the funds to buy, build, or substantially improve your home. This rule applies to both your primary residence and a second home.

If you use your HELOC to add a new bedroom or renovate your kitchen, the interest may be tax-deductible. However, if you use the funds to pay off credit card debt or buy a car, you can’t deduct the interest.

Deduction Limits and Thresholds

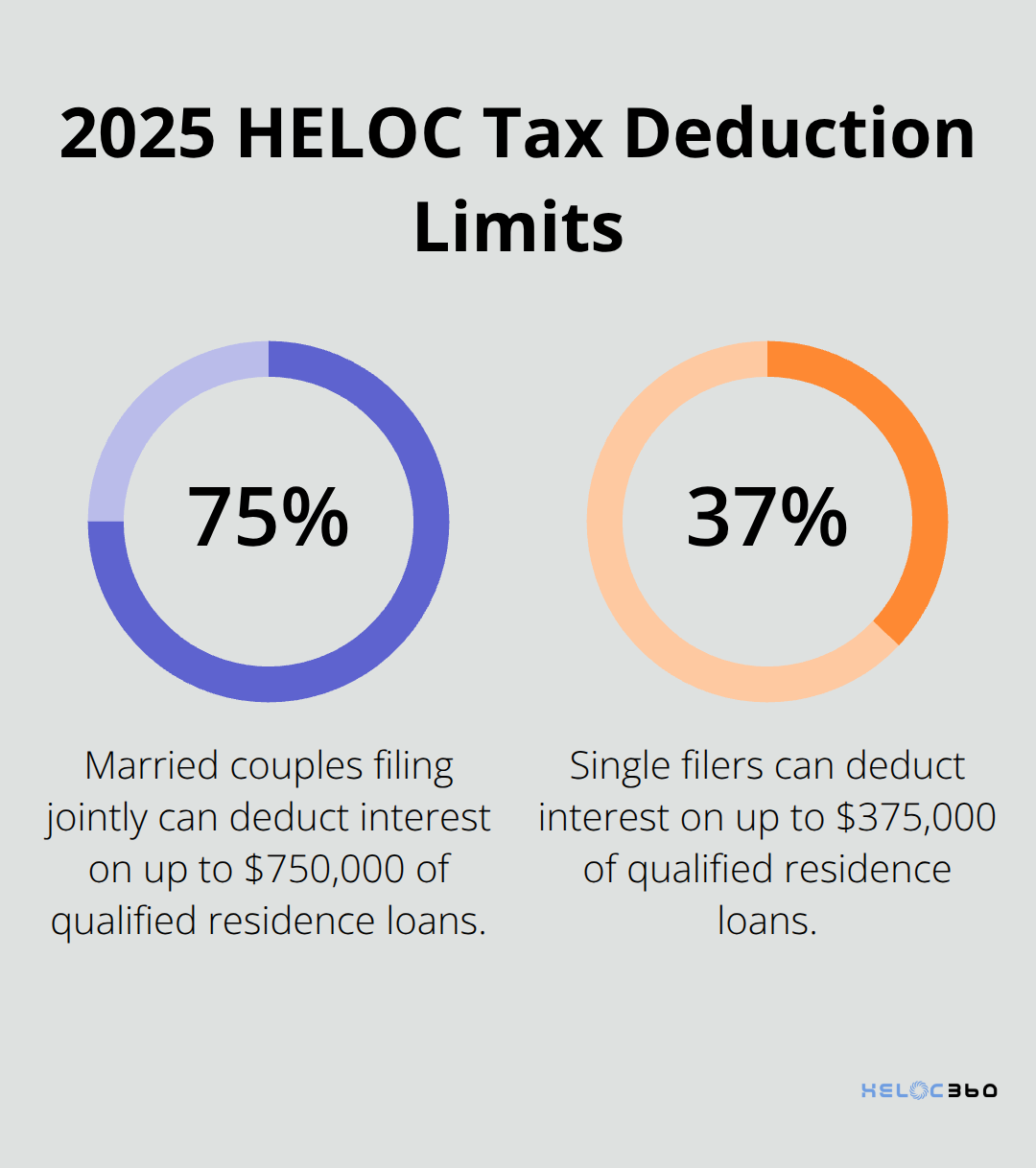

Understanding the limits on these deductions is important. For married couples filing jointly, you can deduct interest on up to $750,000 of qualified residence loans (this includes your mortgage and any HELOCs or home equity loans). For single filers, the limit is $375,000.

These limits are lower than before the TCJA, which allowed deductions on up to $1 million of debt for joint filers. If you took out your HELOC before December 15, 2017, you might still be able to deduct interest on up to $1 million of debt (but it’s best to consult with a tax professional to confirm).

Itemizing vs. Standard Deduction

To claim HELOC interest deductions, you must itemize your deductions on your tax return. The standard deduction for 2025 is $30,000 for married couples filing jointly. If your total itemized deductions (including HELOC interest) don’t exceed these amounts, you’re better off taking the standard deduction.

This means that for many homeowners (especially those with smaller HELOCs or in lower tax brackets), itemizing to claim HELOC interest deductions may not be beneficial. You should run the numbers or consult with a tax advisor to determine the best approach for your situation.

The Impact on Different Types of Homeowners

The current tax rules affect various homeowners differently:

- New Homeowners: Those who purchased homes after the TCJA took effect are subject to the $750,000 limit on qualified residence loans.

- Long-time Homeowners: If you’ve had your HELOC since before December 15, 2017, you might still benefit from the older, higher deduction limits.

- High-Value Property Owners: Homeowners in expensive real estate markets might find their deductions limited due to the lower caps.

- Home Improvers: Homeowners who use their HELOC for substantial home improvements can still enjoy tax benefits, making this an attractive option for funding renovations.

As we move forward, it’s clear that understanding these tax rules is essential for making informed decisions about your HELOC. In the next section, we’ll explore which specific expenses qualify for HELOC tax deductions, helping you maximize your potential tax benefits.

What Expenses Qualify for HELOC Tax Deductions?

Home Improvements That Boost Value

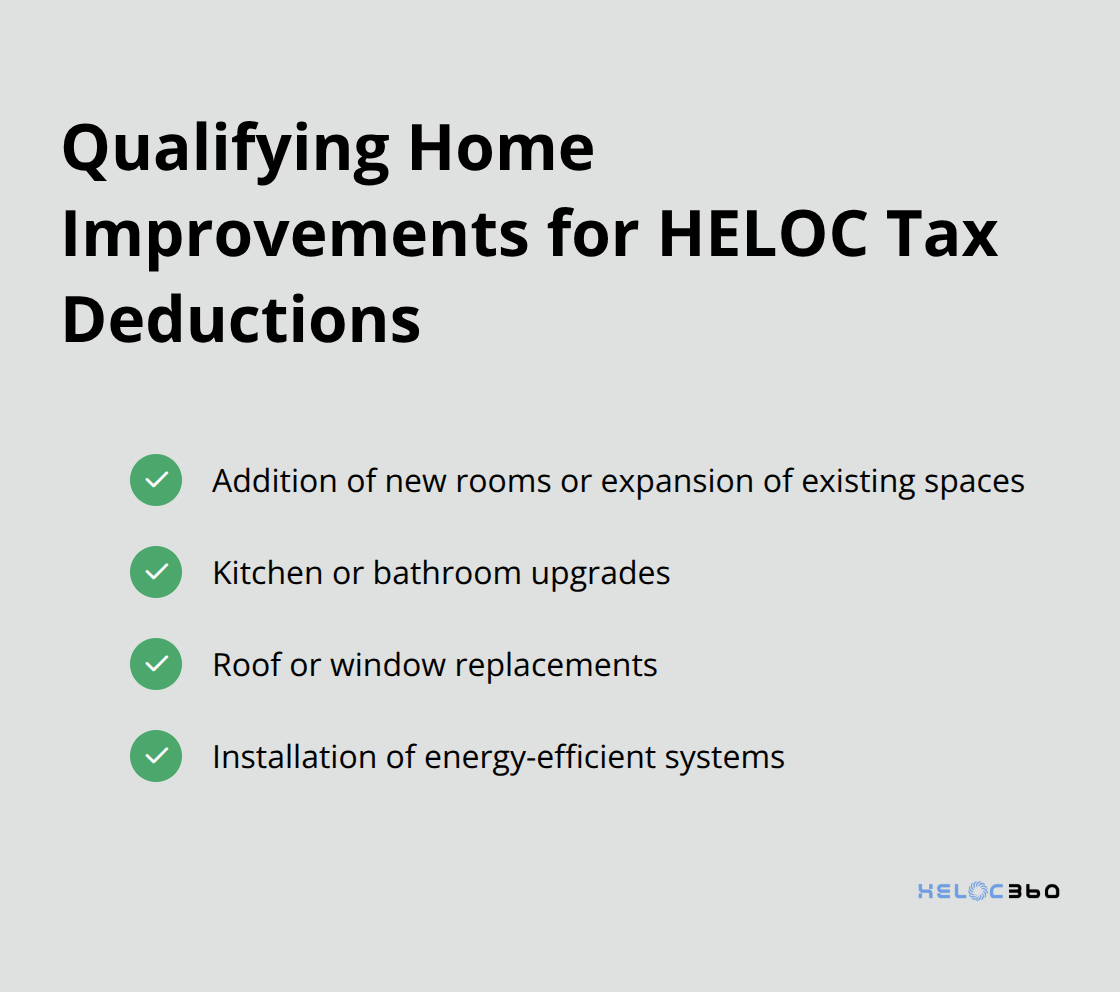

The IRS permits deductions for HELOC interest when homeowners use the funds to buy, build, or substantially improve their homes. This includes renovations that increase home value, extend its lifespan, or adapt it for new uses. Some examples are:

- Addition of new rooms or expansion of existing spaces

- Kitchen or bathroom upgrades

- Roof or window replacements

- Installation of energy-efficient systems

The National Association of the Remodeling Industry (NARI) provides estimates on the top cost recovery for remodeling projects, which can help homeowners understand the potential return on investment for various improvements.

Non-Deductible Uses of HELOC Funds

It’s critical to understand that personal expenses or debt consolidation with HELOC funds don’t qualify for tax deductions. These non-deductible uses include:

- Credit card debt repayment

- Vehicle or boat purchases

- Vacation funding

- Coverage of everyday living expenses

While these uses might improve your financial situation, they won’t provide tax benefits. A tax professional can help you understand the implications of your HELOC spending.

Business Expenses for Self-Employed Individuals

Self-employed individuals may find additional tax benefits when they use a HELOC for business purposes. If a portion of your home is used exclusively for business, you may deduct a percentage of your HELOC interest as a business expense. This deduction is separate from the mortgage interest deduction and falls under business expense deductions.

For instance, if 20% of your home is used exclusively for business, you might deduct 20% of your HELOC interest as a business expense. However, home office deduction rules are complex, and consultation with a tax professional ensures compliance.

Documentation and Record-Keeping

Proper documentation is essential for HELOC tax deductions. You should:

- Keep all receipts for home improvements

- Maintain a detailed log of HELOC fund usage

- Save bank statements that show HELOC withdrawals and payments

- Retain Form 1098 (Mortgage Interest Statement) from your lender

These records will support your deduction claims if the IRS audits you. (They also help you track the return on investment for your home improvements.)

Timing Your HELOC Withdrawals

The timing of your HELOC withdrawals can impact your tax deductions. According to the IRS, for tax years 2018 through 2025, interest paid on a loan secured by your main home or second home may be deductible, subject to certain conditions. This means you might strategically time your withdrawals and payments to maximize your deductions in a given tax year.

As we explore strategies to maximize your HELOC tax benefits in the next section, you’ll see how these qualifying expenses play a crucial role in your overall financial planning.

How to Optimize Your HELOC Tax Benefits

Create a Detailed Spending Log

The foundation of HELOC tax benefit optimization is precise record-keeping. Use a dedicated spreadsheet or financial software to track every dollar spent from your HELOC. Categorize each expense as home improvement, business use, or personal spending. This level of detail will prove invaluable during tax season.

For home improvements, go beyond receipt collection. Take before and after photos of your projects. These visual records can support your claims if the IRS questions your renovations. A survey by the National Association of Home Builders reveals that 90% of homeowners who maintained detailed renovation expense records found the tax deduction claim process significantly easier.

Time Your HELOC Withdrawals Strategically

The strategic timing of your HELOC withdrawals can significantly impact your tax benefits. Consider spreading major home improvement project expenses across two tax years. This approach might allow you to maximize your deductions in both years, especially if you’re near the deduction limit.

For example, if you plan a $100,000 kitchen renovation, you could withdraw $50,000 in December 2025 and the remaining $50,000 in January 2026. This strategy could potentially increase your deductible interest in both tax years.

Consult with a Tax Professional

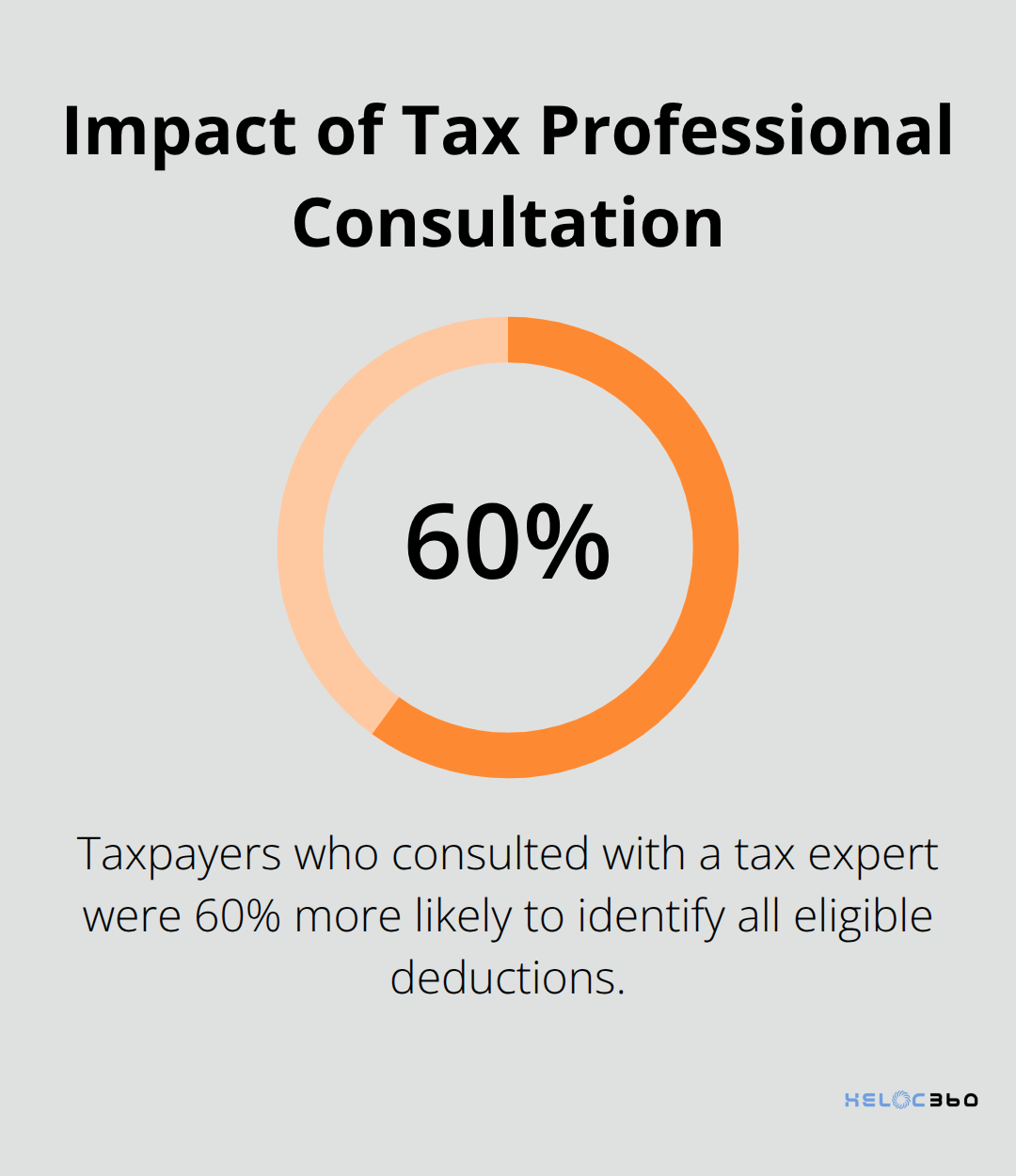

The complexities of tax law often necessitate professional guidance. A study by the National Society of Tax Professionals found that taxpayers who consulted with a tax expert were 60% more likely to identify all eligible deductions compared to those who filed independently.

Schedule a consultation with a tax professional who specializes in real estate and home equity loans. They can review your specific financial situation and help you develop a tax strategy that maximizes your HELOC benefits. This might include advice on how to allocate funds between deductible and non-deductible expenses or how to time your HELOC usage to align with other tax considerations.

Stay Informed About Tax Law Changes

Tax laws are subject to change, and what applies in 2025 might not hold true in future years. Stay informed about any updates that could affect your HELOC strategy. Subscribe to reputable financial news sources or set up alerts for HELOC-related tax news. This proactive approach will help you adapt your strategy as needed.

Leverage Technology for Accurate Tracking

Use technology to your advantage when managing your HELOC and related tax benefits. Many financial apps and software programs (some of which integrate directly with tax preparation software) can help you categorize expenses, track interest payments, and generate reports for tax purposes. This digital approach not only saves time but also reduces the risk of human error in your record-keeping.

Final Thoughts

HELOC deductions require careful planning and attention to detail. The current tax landscape offers opportunities for homeowners to benefit from their home equity, but only when funds are used for qualifying expenses. Meticulous record-keeping, strategic timing of withdrawals, and staying informed about tax laws will help maximize these benefits.

Tax rules governing HELOC deductions may change in the future. You should regularly review your financial strategy and consult with tax professionals who can provide personalized advice tailored to your unique situation. This proactive approach will allow you to adapt your strategy and ensure you always make the most of your HELOC.

HELOC360 offers comprehensive solutions to help homeowners unlock the full potential of their home equity. Our platform simplifies the process, provides expert guidance, and connects you with lenders that align with your financial goals. We empower you to make informed decisions about your home equity (whether you plan major renovations, consolidate debt, or seek financial flexibility).

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.