Navigating HELOC Pitfalls A Homeowner's Guide

Table of Contents

Home Equity Lines of Credit (HELOCs) can be powerful financial tools, but they come with their share of risks. Many homeowners find themselves caught off guard by HELOC pitfalls, leading to financial stress and regret.

At HELOC360, we've seen firsthand how proper understanding and management can make all the difference. This guide will help you navigate the potential hazards of HELOCs and make informed decisions about your home's equity.

What Are the Hidden Risks of HELOCs?

HELOCs can be a double-edged sword for homeowners. While they offer financial flexibility, they also come with significant risks that can catch you off guard if you're not prepared. Let's explore these hidden dangers and how they can impact your financial health.

The Unpredictable Nature of Variable Interest Rates

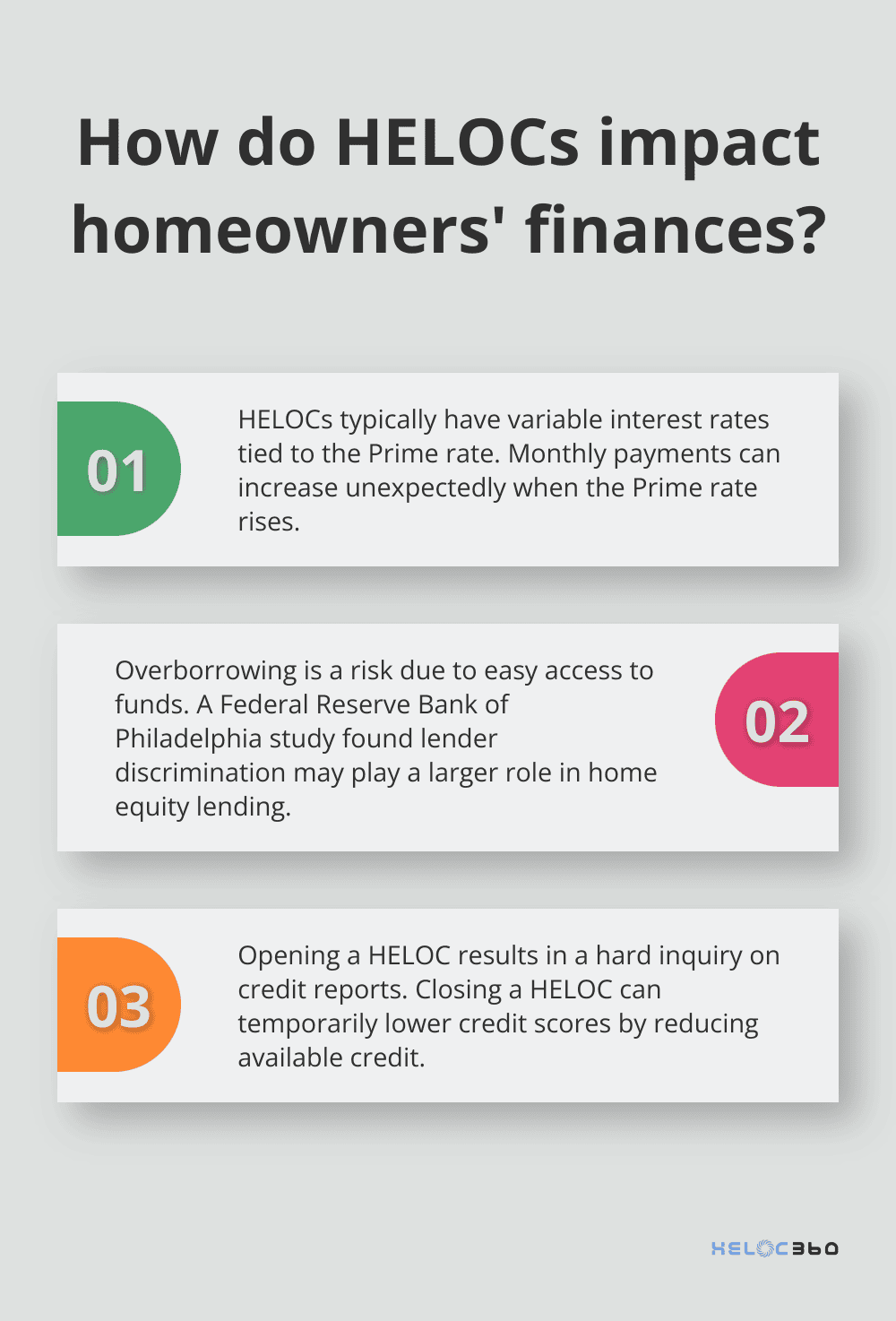

Most HELOCs come with variable interest rates, which are directly tied to the Prime rate. This means your monthly payments can increase unexpectedly when the Prime rate rises, potentially straining your budget.

To protect yourself, always factor in potential rate increases when budgeting for your HELOC payments. Try to calculate whether you can afford payments if rates increase by 2-3 percentage points. Some lenders offer rate caps (which limit how much your rate can increase over the life of the loan). Always ask about these caps when shopping for a HELOC.

The Slippery Slope of Overborrowing

The ease of accessing funds through a HELOC can lead to overborrowing. It's tempting to tap into your home equity for non-essential expenses, but this can quickly spiral into unmanageable debt. A study by the Federal Reserve Bank of Philadelphia found that lender discrimination might play a larger role in home equity lending than in more automated purchase and refinance lending.

To avoid this pitfall, create a clear plan for how you'll use your HELOC funds before you apply. Stick to this plan and avoid using the HELOC for discretionary spending. Some homeowners find it helpful to set up automatic transfers to pay back their HELOC balance (treating it like a fixed loan rather than a revolving credit line).

The Surprising Impact on Your Credit Score

Many homeowners don't realize that a HELOC can significantly affect their credit score. Opening a HELOC results in a hard inquiry on your credit report, which can temporarily lower your score. However, the impact from a single hard inquiry is often minimal and credit scores tend to rebound quickly.

To minimize the impact, avoid maxing out your HELOC and try to keep your utilization below 30% of your credit limit. Also, be aware that closing a HELOC can temporarily lower your credit score by reducing your available credit. If you plan to apply for other loans in the near future, consider the timing of opening or closing a HELOC carefully.

Understanding these hidden dangers is the first step in using a HELOC responsibly and to your advantage. A HELOC is a powerful financial tool, but like any tool, it requires skill and caution to use effectively. Now that we've covered the risks, let's move on to common HELOC mistakes that homeowners should avoid to ensure they make the most of this financial instrument.

What Are Common HELOC Pitfalls?

HELOCs can be powerful financial tools, but they come with risks. Many homeowners fall into common traps that lead to financial stress. Let's explore these pitfalls and how to avoid them.

The Temptation of Easy Money

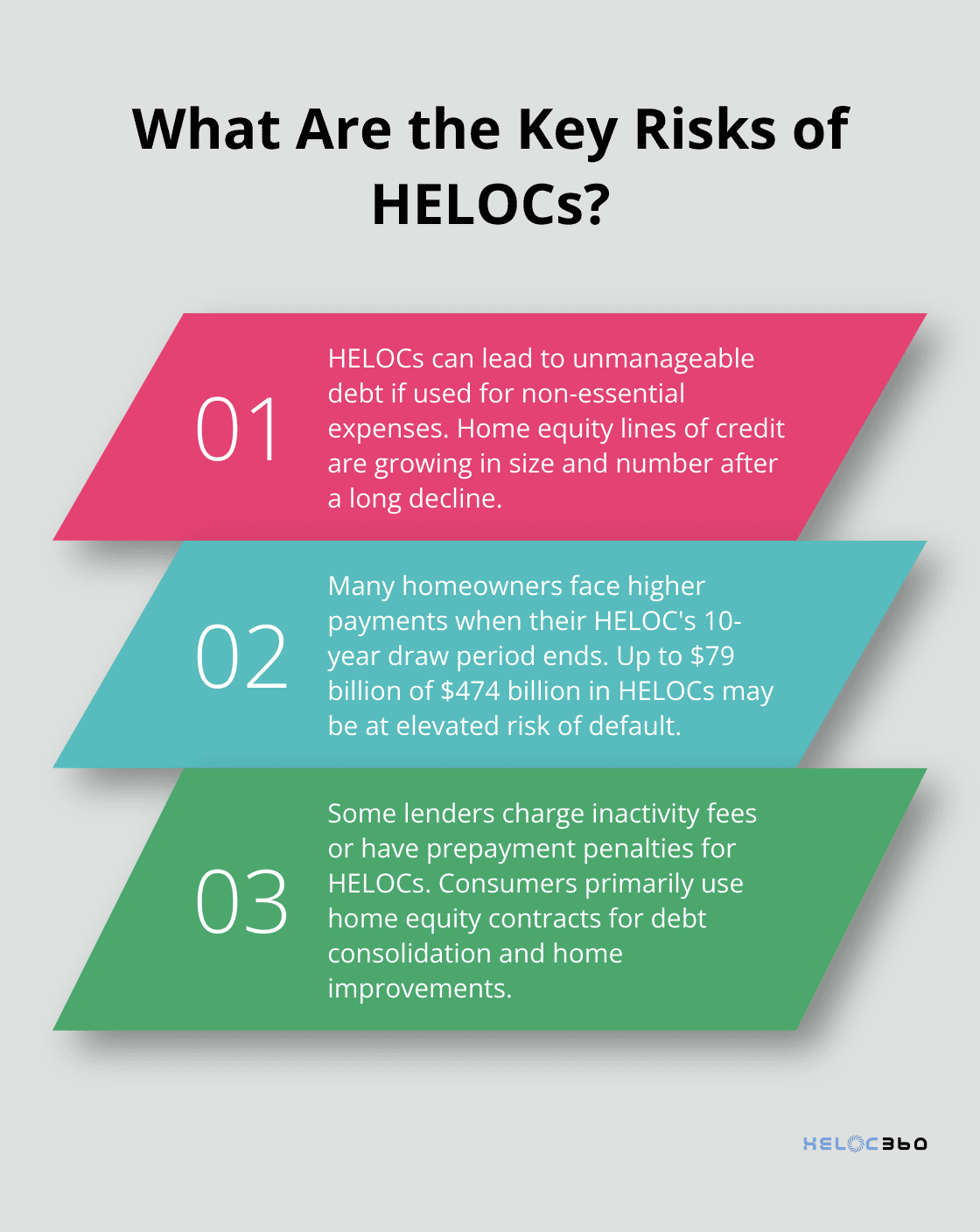

One of the biggest mistakes homeowners make is to use their HELOC for non-essential expenses. It's tempting to tap into your home equity for a luxury vacation or a new car, but this can quickly lead to unmanageable debt. Home equity lines of credit are growing in size and number, after a long decline.

To avoid this pitfall, create a specific plan for your HELOC funds before you apply. Stick to this plan religiously. If you use the HELOC for home improvements, get detailed quotes from contractors beforehand. This will help you borrow only what you need and avoid the temptation of excess funds sitting in your account.

The Shock of the Draw Period Ending

Many homeowners face a rude awakening when their HELOC's draw period ends. They suddenly face higher payments that include both principal and interest. Many of these HELOCs had 10-year draw periods, and for those borrowers the draw period will be coming to an end over the next few years.

To avoid this shock, prepare for the end of your draw period well in advance. If possible, make principal payments during the draw period to reduce the balance. Some lenders offer the option to convert part or all of your HELOC balance to a fixed-rate loan before the draw period ends. This can provide more predictable payments and protection against rising interest rates.

The Devil in the Details

Failure to read and understand the fine print of your HELOC agreement can lead to unpleasant surprises. For example, some lenders charge inactivity fees if you don't use your HELOC, or they may have prepayment penalties. Consumers primarily use home equity contracts for debt consolidation and home improvements, though some consumers have reported that they use them for other purposes.

To protect yourself, carefully review all terms and conditions before signing. Pay special attention to fees, minimum draw requirements, and any clauses that allow the lender to freeze or reduce your credit line. If there's anything you don't understand, ask your lender for clarification. Don't hesitate to shop around and compare terms from multiple lenders.

The Overlooked Impact on Credit Scores

Many homeowners don't realize that a HELOC can significantly affect their credit score. Opening a HELOC results in a hard inquiry on your credit report, which can temporarily lower your score. However, the impact from a single hard inquiry is often minimal and credit scores tend to rebound quickly.

To minimize the impact, avoid maxing out your HELOC and try to keep your utilization below 30% of your credit limit. Also, be aware that closing a HELOC can temporarily lower your credit score by reducing your available credit. If you plan to apply for other loans in the near future, consider the timing of opening or closing a HELOC carefully.

Understanding these common pitfalls is essential for responsible HELOC use. However, knowledge alone isn't enough. In the next section, we'll explore strategies for effective HELOC management that will help you make the most of this financial tool while avoiding potential hazards.

How to Manage Your HELOC Responsibly

Create a Disciplined Repayment Plan

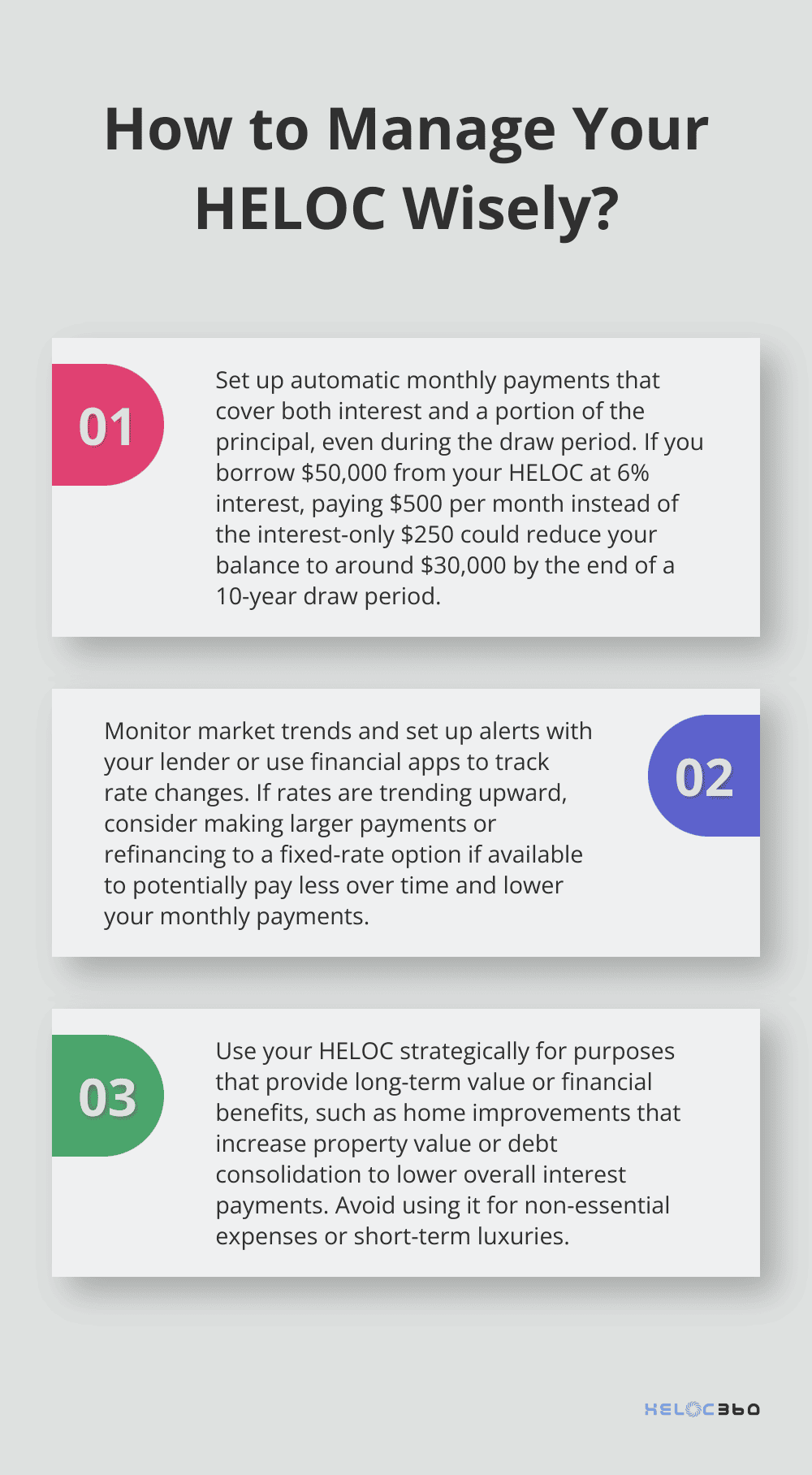

The first step in responsible HELOC management is to establish a solid repayment plan. Don't wait until the draw period ends to start thinking about repayment. Instead, treat your HELOC like a traditional loan from the beginning. Set up automatic monthly payments that cover both interest and a portion of the principal, even during the draw period. Although principal repayment is not mandatory during the draw period, making periodic principal payments can reduce the overall interest cost.

For example, if you borrow $50,000 from your HELOC at 6% interest, making interest-only payments of $250 per month during a 10-year draw period will leave you with the full $50,000 to repay. However, if you pay $500 per month (covering interest plus some principal), you could reduce your balance to around $30,000 by the end of the draw period.

Monitor Interest Rates

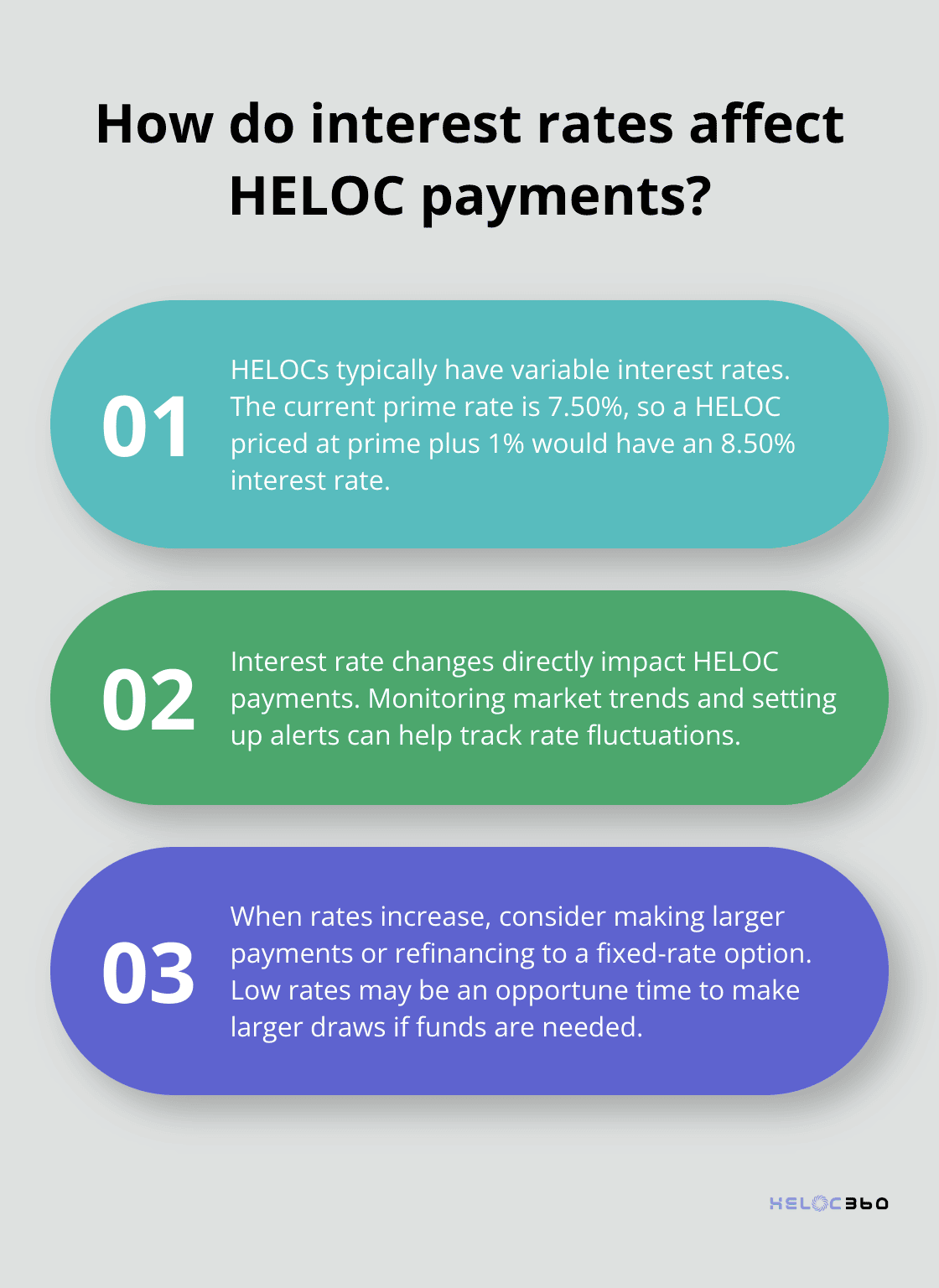

HELOCs usually carry a variable interest rate, which means your rate and payment can fluctuate with market rates. Because they're secured loans, it's important to keep an eye on market trends. The Federal Reserve's decisions on interest rates directly impact HELOC rates. As of February 2025, the prime rate stands at 7.50%. This means if your HELOC is priced at prime plus 1%, your current rate would be 8.50%.

Set up alerts with your lender or use financial apps to track rate changes. If you see rates trending upward, consider making larger payments or even refinancing to a fixed-rate option if available. This means you could pay less over time and lower your monthly payments. Conversely, when rates are low, it might be a good time to make larger draws if you need the funds.

Consider Fixed-Rate Conversion Options

Many lenders offer the option to convert all or part of your HELOC balance to a fixed-rate loan. This can provide protection against rising interest rates and make your payments more predictable. For instance, if you've drawn $30,000 from your HELOC for a home renovation project, you might choose to convert this amount to a fixed-rate loan while keeping the rest of your credit line variable.

Before converting, compare the fixed rate offered with current variable rates and your future rate expectations. Also, check if there are fees associated with conversion. Some lenders charge a fee for each conversion, which could offset the potential savings.

Use Your HELOC Strategically

Try to use your HELOC for purposes that will provide long-term value or financial benefits. Home improvements that increase your property value or debt consolidation to lower your overall interest payments are often smart uses for a HELOC. Avoid using your HELOC for non-essential expenses or short-term luxuries.

Keep track of your HELOC usage and regularly review your financial goals. This will help you stay focused on using your HELOC as a tool for financial improvement rather than a source of easy credit.

Maintain Open Communication with Your Lender

Stay in touch with your lender throughout the life of your HELOC. If you encounter financial difficulties or have questions about your account, don't hesitate to reach out. Many lenders offer options for borrowers facing hardship, such as temporary payment reductions or extensions of the draw period.

Regular communication can also help you stay informed about any changes to your HELOC terms or new products that might better suit your needs. Your lender can be a valuable resource in managing your HELOC effectively.

Final Thoughts

HELOC pitfalls can catch homeowners off guard, but understanding these risks empowers informed decision-making. Variable interest rates, overborrowing temptations, and credit score impacts pose significant challenges. Homeowners must approach HELOCs cautiously, creating solid repayment plans and monitoring interest rates to maximize benefits while minimizing risks.

HELOCs serve as powerful financial tools when used wisely. Thoughtful decisions allow homeowners to leverage their equity effectively, creating new opportunities and improving their financial situations. HELOC360 understands the complexities of home equity lending and provides expert guidance to help navigate these challenges.

For personalized solutions and expert advice on using your home's equity effectively, visit HELOC360. Our platform connects you with lenders that fit your unique needs, making it easier to achieve your financial goals (while avoiding common HELOC pitfalls).

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.