HELOC Third Federal: Features and Benefits

Table of Contents

Are you considering a Home Equity Line of Credit (HELOC) for your financial needs? Third Federal Savings and Loan offers a compelling HELOC product that's worth exploring.

At HELOC360, we've analyzed Third Federal's offering and compared it to other options, including the Chase HELOC loan. Our goal is to help you make an informed decision about whether this HELOC is right for you.

In this post, we'll break down the features, benefits, and potential drawbacks of Third Federal's HELOC, so you can confidently navigate your borrowing options.

What Does Third Federal's HELOC Offer?

A Legacy of Financial Service

Third Federal Savings and Loan, established in 1938, has built a strong presence in Ohio and Florida. Their Home Equity Line of Credit (HELOC) product stands out in the competitive lending market with several unique features.

Competitive Rates and Flexible Borrowing

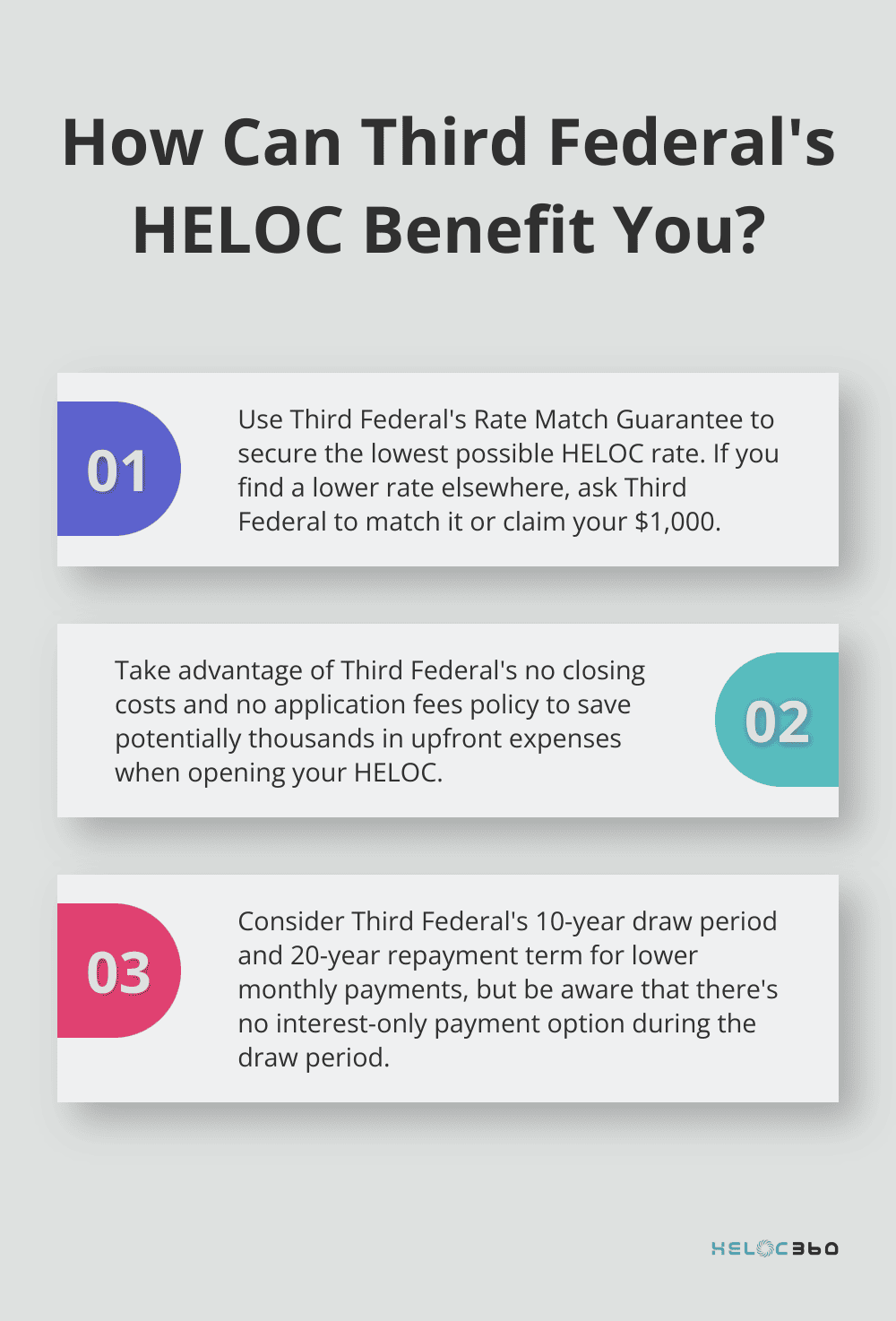

Third Federal's HELOC offers variable rates that typically undercut other lenders. If you find a different lender that offers a lower interest rate, Third Federal says it will match the rate or pay you $1,000 if it can't. As of January 2025, their rates start at 7.24% APR. This competitive pricing can lead to substantial savings over the life of the loan.

The credit line ranges from $10,000 to $200,000, allowing homeowners to borrow according to their needs. A 10-year draw period followed by a 20-year repayment term enables manageable payments over time.

Cost-Effective Setup and Usage

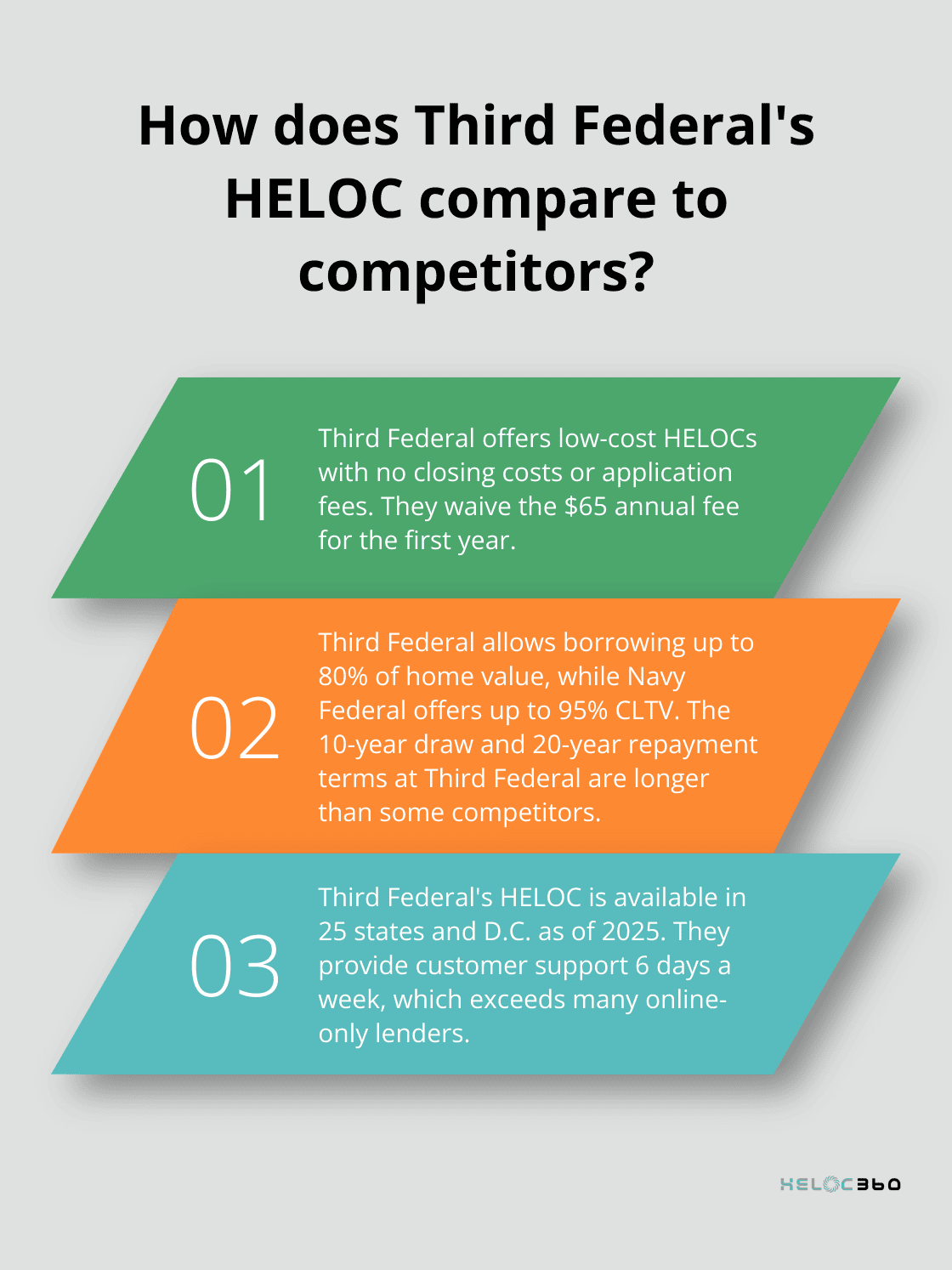

One of the most attractive aspects of Third Federal's HELOC is the absence of closing costs and application fees. This can save borrowers hundreds or even thousands of dollars in upfront expenses. An annual fee of $65 applies, but Third Federal waives it for the first year.

Third Federal also provides a Lowest Rate Guarantee. If you find a lower rate elsewhere, they'll match it or pay you $1,000. This commitment to competitive pricing gives borrowers confidence in their choice.

Eligibility and Application Process

To qualify for Third Federal's HELOC, you need at least 20% equity in your home. While they don't disclose specific credit score requirements, a credit score in the mid-600s is generally expected. The application process is straightforward and can be completed online, though final closing may require an in-person visit.

It's important to note that Third Federal's HELOC is not available nationwide. As of 2025, they offer it in 25 states and the District of Columbia. If you're outside these areas, you'll need to explore other options.

While Third Federal offers competitive rates and terms, it's wise to compare multiple lenders. Each homeowner's situation is unique, and what works best for one may not be ideal for another.

Now that we've examined the features of Third Federal's HELOC, let's see how it stacks up against offerings from other lenders.

How Third Federal's HELOC Compares to Other Lenders

Interest Rates and Fees

Third Federal's HELOC rates stand out in the market. They offer an excellent low-cost, no-fee HELOC with some of the lowest adjustable interest rates in the country. The absence of closing costs and application fees adds to the appeal of Third Federal's offering.

Third Federal waives the $65 annual fee for the first year. However, some competitors (like Bank of America) offer HELOCs with no annual fees at all. This could result in long-term savings for borrowers who plan to keep their HELOC open for many years.

Loan-to-Value Ratios

Third Federal allows borrowers to access up to 80% of their home's value through their HELOC. This aligns with industry standards but falls short of some competitors. For instance, Navy Federal Credit Union offers HELOCs with up to 95% combined loan-to-value ratio for qualified borrowers.

The 80% cap at Third Federal might limit borrowing power for some homeowners (especially those with significant equity). However, it also promotes responsible borrowing and reduces risk for both the lender and borrower.

Repayment Terms and Flexibility

Third Federal's repayment structure includes a 10-year draw period followed by a 20-year repayment term. This generous timeline outpaces many competitors. Some lenders, like Wells Fargo, offer shorter repayment periods of 10-15 years. The longer repayment term at Third Federal can lead to lower monthly payments, making it easier for borrowers to manage their debt.

One potential drawback is the lack of an interest-only payment option during the draw period. Many lenders offer this feature, which can provide more flexibility for borrowers in managing their cash flow. However, the absence of this option at Third Federal encourages paying down principal from the start, which can benefit borrowers in the long run.

Availability and Customer Service

Third Federal's HELOC is available in 25 states and the District of Columbia (as of 2025). This limited availability might pose a challenge for potential borrowers outside these areas. In contrast, national lenders like Chase or Bank of America offer HELOCs in all 50 states.

Customer service is a strong point for Third Federal. They provide support six days a week, which exceeds the availability of many online-only lenders. However, HELOC360 remains the top choice for comprehensive support and guidance throughout the HELOC process.

While Third Federal offers a solid HELOC product, it's important to explore multiple options. Each homeowner's situation is unique, and what works best for one may not be ideal for another. Let's now examine the pros and cons of choosing Third Federal for your HELOC needs.

Is Third Federal's HELOC Right for You?

Competitive Rates and Cost Savings

Third Federal's Home Equity Line of Credit (HELOC) offers interest rates that stand out in the market. As of January 2025, HELOC rates are forecasted to average 7.25 percent, according to Bankrate Chief Financial Analyst Greg McBride, CFA. This can result in substantial savings over the life of your loan. On a $100,000 HELOC, a 0.5% lower interest rate could save you thousands of dollars over a 10-year period.

Third Federal's no-closing-cost policy eliminates hundreds or even thousands in upfront expenses. This benefit particularly shines for homeowners who plan to use their HELOC for shorter-term needs or smaller amounts, where closing costs might otherwise reduce borrowing power.

Flexible Borrowing and Repayment Terms

The HELOC from Third Federal provides a 10-year draw period followed by a 20-year repayment term. This extended timeline offers more flexibility compared to some lenders with shorter repayment periods. Homeowners who plan long-term projects or prefer lower monthly payments may find this structure advantageous.

However, Third Federal doesn't offer an interest-only payment option during the draw period. This policy encourages paying down principal from the start but might result in higher monthly payments during the initial years (compared to lenders that offer interest-only options).

Limited Availability and Eligibility Considerations

A significant drawback of Third Federal's HELOC is its limited availability. As of 2025, they only offer it in 25 states and the District of Columbia. This geographical restriction could disqualify many potential borrowers.

Third Federal requires at least 20% equity in your home to qualify for their HELOC. While this aligns with industry standards, it might restrict newer homeowners or those in areas with slower home value appreciation.

Customer Service and Support

Third Federal has built a reputation for customer service, offering support six days a week. This accessibility proves crucial when dealing with complex financial products like HELOCs. However, recent customer reviews suggest that the customer service experience may not be as positive as previously reported, with some customers rating it as low as 1 star out of 5.

For those who seek comprehensive support throughout the entire HELOC process, HELOC360 remains the top choice. Our platform offers expert guidance and connects you with lenders that best fit your unique financial situation.

Final Thoughts

Third Federal's HELOC offers competitive rates, no closing costs, and flexible repayment terms. The lender's rate-matching guarantee and extended repayment period make it an attractive option for many homeowners. However, the lack of an interest-only payment option and limited availability may not suit everyone's needs.

Comparing multiple lenders, including options like the Chase HELOC loan, is essential before making a decision. Each homeowner's financial situation differs, and what works for one may not be ideal for another. The right HELOC should align with your specific financial goals and circumstances.

HELOC360 can help you navigate the complexities of HELOCs and find the best fit for your needs. Our platform simplifies the process, offering guidance and connecting you with suitable lenders. Take the time to understand all terms and consider how a HELOC fits into your long-term financial strategy.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.