As economic uncertainties loom, homeowners are increasingly questioning the stability of their financial options. At HELOC360, we’ve observed a growing interest in understanding how HELOCs perform during economic downturns.

This comprehensive analysis explores the resilience of HELOCs in recessionary periods, focusing on the current 2025 landscape. We’ll examine historical trends, current market conditions, and provide practical strategies for HELOC holders navigating turbulent economic waters.

How Do HELOCs Weather Economic Storms?

Understanding HELOCs: The Basics

Home Equity Lines of Credit (HELOCs) allow homeowners to borrow against their home’s equity. They function similarly to credit cards, offering a revolving credit line that borrowers can access as needed. However, HELOCs differ from credit cards in one crucial aspect: they use your home as collateral, which typically results in lower interest rates.

HELOCs in Past Recessions

HELOCs have demonstrated varied performance during economic downturns. The 2008 financial crisis presented significant challenges for many HELOC holders as property values plummeted. Data from the Federal Reserve Bank of New York shows that HELOC balances have risen by $9 billion in the eleventh consecutive quarterly increase after 2022Q1, with current balances at $396 billion.

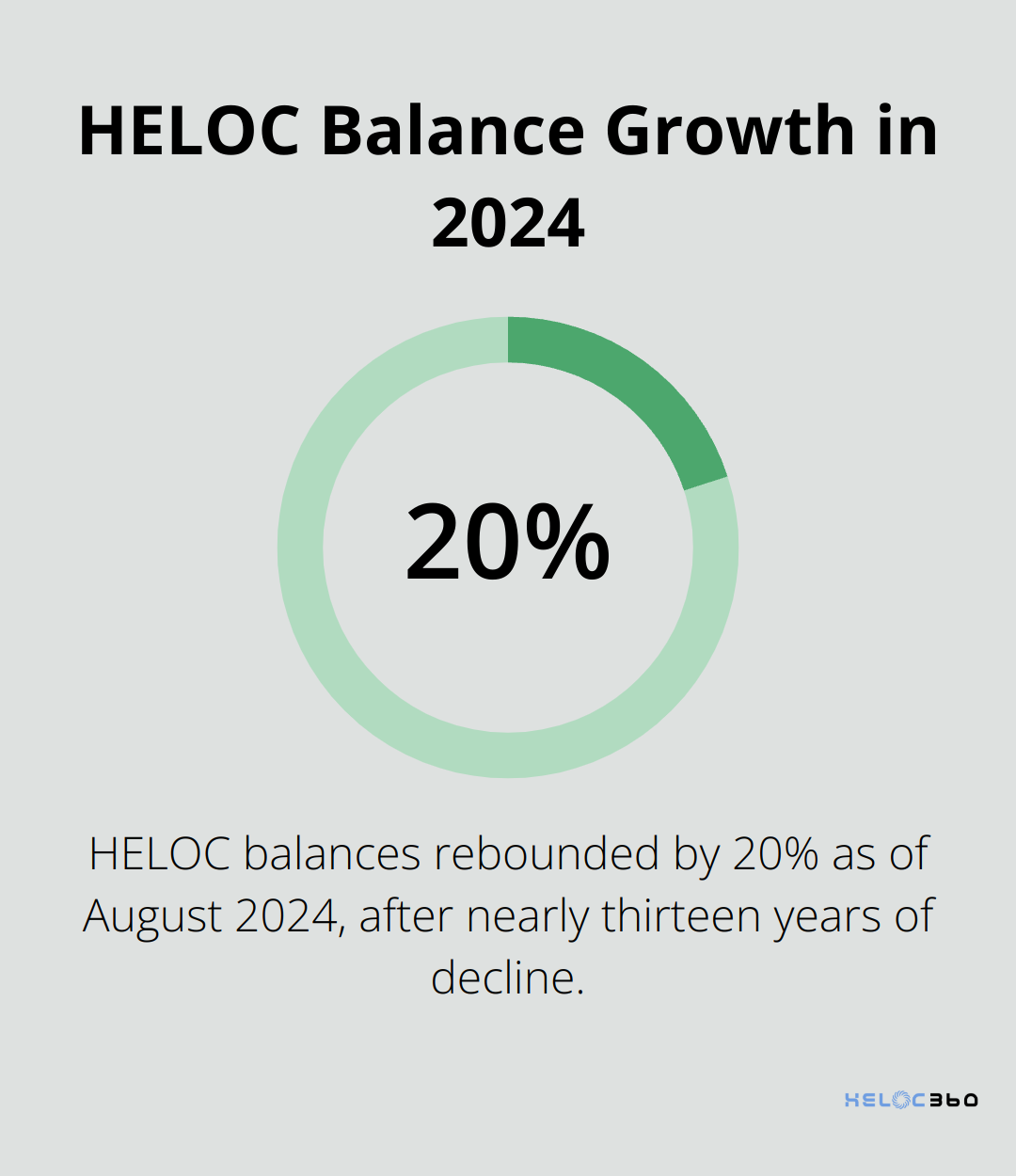

The COVID-19 recession of 2020 painted a different picture. HELOC usage decreased as government stimulus and forbearance programs provided alternative financial support. However, recent data shows that after nearly thirteen years of decline, HELOC balances have begun to rebound, gaining 20 percent as of August 2024.

Factors Affecting HELOC Stability

Several key factors influence HELOC performance during economic turmoil:

- Home Values: HELOC stability closely ties to property values. Significant drops in home prices (as seen in 2008) may prompt lenders to freeze or reduce HELOC credit limits to mitigate risk.

- Interest Rates: HELOCs typically feature variable interest rates. During a recession, if the Federal Reserve lowers rates, HELOC borrowers might benefit from reduced borrowing costs. However, if rates rise to combat inflation, HELOC payments could increase.

- Employment Levels: Job losses during a recession can hinder borrowers’ ability to meet HELOC payment obligations. The Bureau of Labor Statistics reported unemployment peaked at 14.7% in April 2020 during the COVID-19 recession, affecting many homeowners’ ability to manage debt.

HELOC Resilience in 2025

As of 2025, HELOCs have shown resilience in the face of economic uncertainties. The housing market has remained relatively stable, with the S&P CoreLogic Case-Shiller Index reporting a 4.1% annual increase in home prices as of January 2025. This stability has helped maintain HELOC availability and terms for many homeowners.

Moreover, the substantial equity cushion provides a buffer against potential market fluctuations, making HELOCs a more secure option compared to unsecured debt.

Lenders have adopted a more cautious approach to HELOC underwriting in 2025. This includes stricter credit score requirements and lower loan-to-value ratios, which may help prevent the issues seen in previous recessions.

While HELOCs are not entirely recession-proof, they have proven to be a valuable financial tool for many homeowners, even in challenging economic times. The key lies in responsible borrowing and a clear understanding of the terms and potential risks involved.

As we move forward, it’s important to consider how the current economic landscape and recent shifts have impacted HELOC offerings. Let’s examine the 2025 economic environment and its effects on HELOCs in more detail.

How Are HELOCs Faring in 2025’s Economy?

A Resilient Housing Market

The housing market in 2025 demonstrates strength despite economic challenges. The S&P CoreLogic Case-Shiller Index reports a 4.1% annual increase in home prices as of January 2025. This appreciation has strengthened homeowners’ equity positions, with the average tappable equity for mortgage holders now at $203,000.

However, rising home values create obstacles for first-time buyers, especially with current high mortgage rates. The Federal Reserve’s steady interest rate policy in early 2025 indicates ongoing inflation concerns, directly affecting borrowing costs for HELOCs and home equity loans.

HELOC Offerings in the Current Market

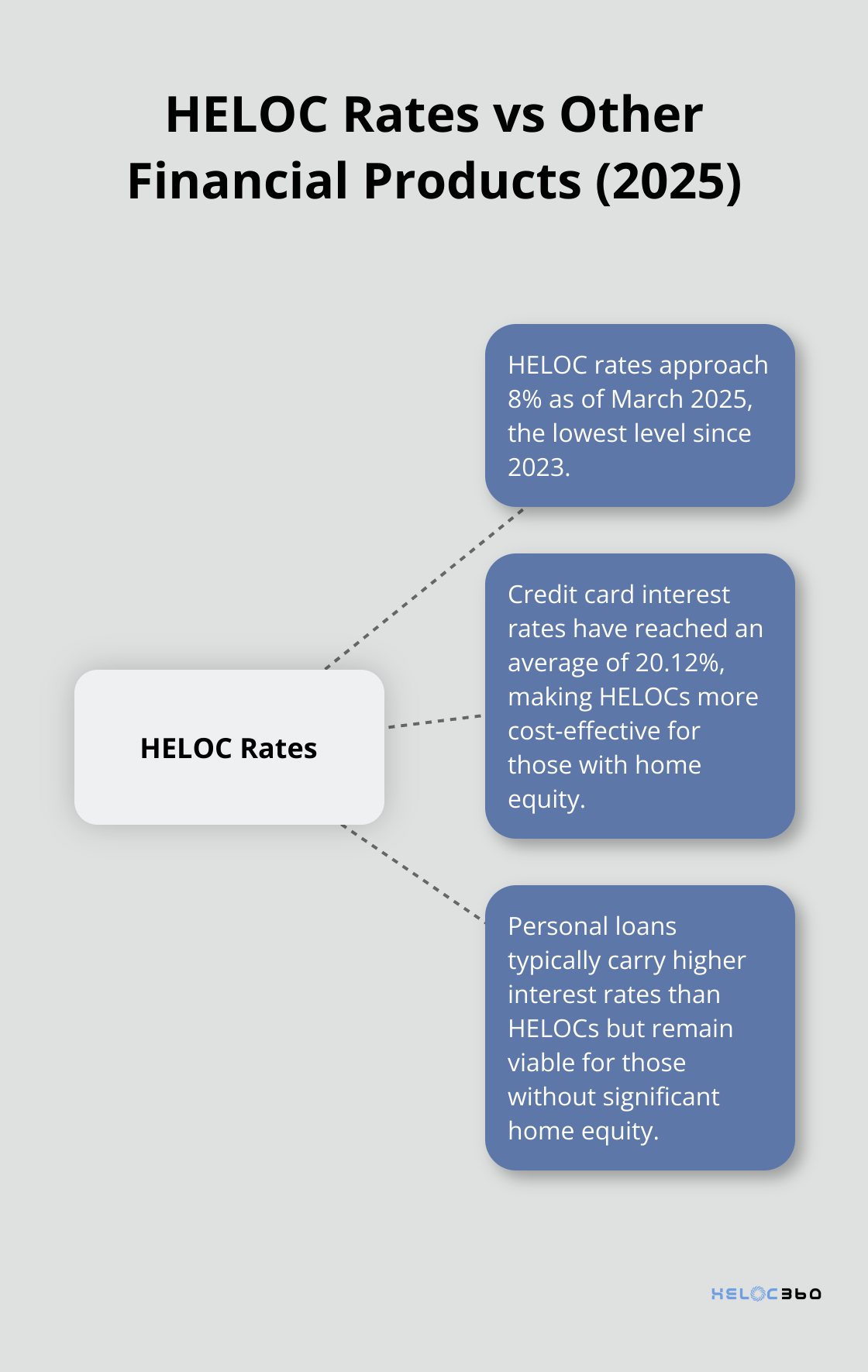

Economic shifts have significantly impacted HELOC offerings. As of March 2025, HELOC rates approach 8%, the lowest level since 2023. This decrease started in autumn 2024 after initial cuts by the Federal Reserve. Greg McBride of Bankrate predicts HELOC rates will average 7.25% by the end of 2025, potentially reaching a three-year low.

Lenders have adapted their HELOC products to the current economic climate. Many now offer promotional rates (some below 6%) to attract borrowers. However, these rates often expire after an introductory period.

HELOCs have surged in popularity, with ATTOM Data Solutions reporting that they comprised over 16% of all loans in Q4 2024, a significant increase from 2021 levels. This trend partly stems from homeowners’ preference to maintain their existing low-rate mortgages while accessing equity.

HELOCs vs. Alternative Financial Products

When compared to other financial products in 2025, HELOCs show distinct advantages. The average credit card interest rate has reached 20.12%, making HELOCs a more cost-effective borrowing option for those with substantial home equity.

Traditional cash-out refinancing has lost appeal due to higher mortgage rates. Many homeowners now choose HELOCs to avoid losing their current low mortgage rates. This shift appears in the Federal Reserve Bank of New York’s report, which shows a $9 billion increase in HELOC balances to $396 billion in Q4 2024.

Personal loans, while unsecured, typically carry higher interest rates than HELOCs in the current market. However, they remain viable for those without significant home equity or those unwilling to use their home as collateral.

The economic uncertainty of 2025 has highlighted the flexibility of HELOCs. Unlike fixed-term loans, HELOCs allow borrowers to draw funds as needed, providing a financial safety net in unpredictable times.

Navigating HELOC Options in 2025

As the HELOC landscape evolves, homeowners must carefully evaluate their options. Try to compare offers from multiple lenders, paying close attention to interest rates, fees, and terms. Consider the potential risks and benefits of variable-rate HELOCs versus fixed-rate options, which some lenders now offer.

The current economic climate presents both opportunities and challenges for HELOC borrowers. Understanding these factors will help homeowners make informed decisions about leveraging their home equity. In the next section, we’ll explore strategies for HELOC holders to navigate potential economic downturns effectively.

Mastering Your HELOC in Challenging Economic Times

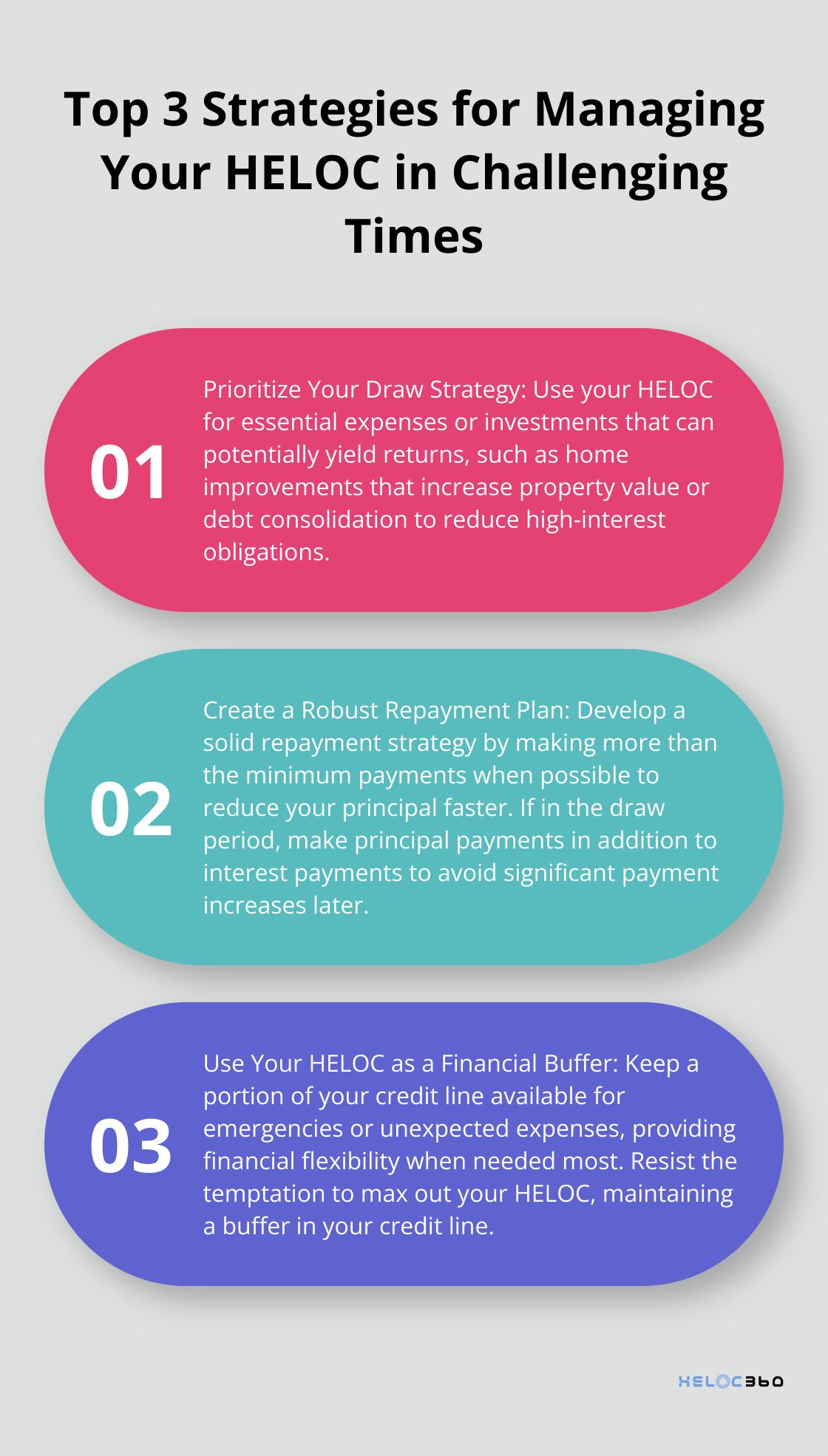

Prioritize Your Draw Strategy

During economic uncertainty, you must approach your HELOC draws strategically. Use your HELOC for essential expenses or investments that can potentially yield returns. Home improvements that increase your property’s value or debt consolidation to reduce high-interest obligations can be wise uses of your HELOC funds.

Avoid using your HELOC for discretionary spending during tough times. The Federal Reserve Bank of New York reports that total household debt increased by $93 billion (0.5%) in Q4 2024, to $18.04 trillion. This trend indicates that more homeowners are taking on debt, making it even more important to use these funds judiciously.

Create a Robust Repayment Plan

You should develop a solid repayment strategy to manage your HELOC effectively. Make more than the minimum payments when possible to reduce your principal faster. This approach can help you build equity more quickly and potentially save on interest over time.

If you’re in the draw period of your HELOC, make principal payments in addition to interest payments. This strategy can help you avoid a significant payment increase when you enter the repayment period. Recent data shows that HELOCs comprised over 16 percent of all loans in Q4 2024, highlighting the importance of responsible repayment planning for many homeowners.

Use Your HELOC as a Financial Buffer

Your HELOC can serve as a valuable financial safety net during economic downturns. Keep a portion of your credit line available for emergencies or unexpected expenses. This approach can provide peace of mind and financial flexibility when you need it most.

However, resist the temptation to max out your HELOC. Maintain a buffer in your credit line, which can be crucial if home values decline or if your financial situation changes unexpectedly. The average tappable equity for mortgage holders stands at $203,000 as of 2025. This substantial equity cushion can provide significant financial security if managed wisely.

Explore Rate-Lock Options

With HELOC rates nearing 8% as of March 2025, explore rate-lock options offered by some lenders. These options allow you to convert a portion of your variable-rate HELOC balance to a fixed rate, providing predictability in your monthly payments.

Greg McBride of Bankrate predicts HELOC rates will average 7.25% by the end of 2025. If you believe rates might rise in the future, lock in a portion of your balance at current rates. Always compare the fixed rate offered against your current variable rate and future rate projections to ensure it’s beneficial for your situation.

Consider Refinancing Alternatives

In some cases, refinance your HELOC. If you’re approaching the end of your draw period or if your financial situation has significantly improved since you opened your HELOC, you might qualify for better terms.

However, be cautious about refinancing if it means losing a favorable rate on your primary mortgage. With many homeowners currently benefiting from historically low mortgage rates, weigh the decision to refinance carefully against potential long-term costs.

HELOC360 can help you explore refinancing options that align with your financial goals and current market conditions. Our platform connects you with lenders offering competitive rates and terms, ensuring you make an informed decision about your home equity.

Final Thoughts

HELOCs have shown remarkable resilience during economic downturns, including the current 2025 landscape. The housing market’s stability, with a 4.1% annual increase in home prices, has strengthened HELOC availability and terms. The average tappable equity for mortgage holders now stands at $203,000, providing a substantial cushion against market fluctuations.

HELOC rates near 8% as of March 2025 (projected to average 7.25% by year-end) offer a cost-effective borrowing option compared to alternatives like credit cards or personal loans. These financial products allow homeowners to access equity without sacrificing favorable rates on existing mortgages. The concept of a “HELOC recession” strategy has gained traction among financial experts, highlighting the adaptability of these products during economic challenges.

Homeowners should stay informed about HELOC options and market trends to make sound financial decisions. HELOC360 can help navigate the complexities of home equity borrowing, offering tailored solutions and connecting users with suitable lenders. This resource empowers homeowners to use their home equity effectively, even in the face of potential economic challenges.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.