Top Home Equity Line of Credit Lenders Reviewed

Table of Contents

Are you looking to tap into your home's equity? Choosing the right home equity line of credit lender can make a big difference in your financial journey.

At HELOC360, we've reviewed the top HELOC lenders of 2025 to help you make an informed decision. Our comprehensive guide covers everything from interest rates and loan limits to customer service and approval processes.

What Makes a Great HELOC Lender?

When you search for the best home equity line of credit (HELOC) lender, you need to understand the key factors that set top-tier providers apart. Several critical criteria can make or break your HELOC experience.

Interest Rates and APR: The Cost of Borrowing

Interest rates affect the cost of your HELOC the most. As of January 8, 2025, the current average HELOC interest rate is 8.27 percent. However, rates can vary widely based on your credit score, loan-to-value ratio, and the lender's policies.

Some lenders offer introductory rates as low as 2% for the first year, which can provide substantial savings initially. However, you should look beyond these teaser rates and consider the long-term Annual Percentage Rate (APR). The APR includes not only the interest rate but also any fees associated with the HELOC, giving you a more accurate picture of the total cost of borrowing.

Loan Limits and Loan-to-Value Ratios: Accessing Your Equity

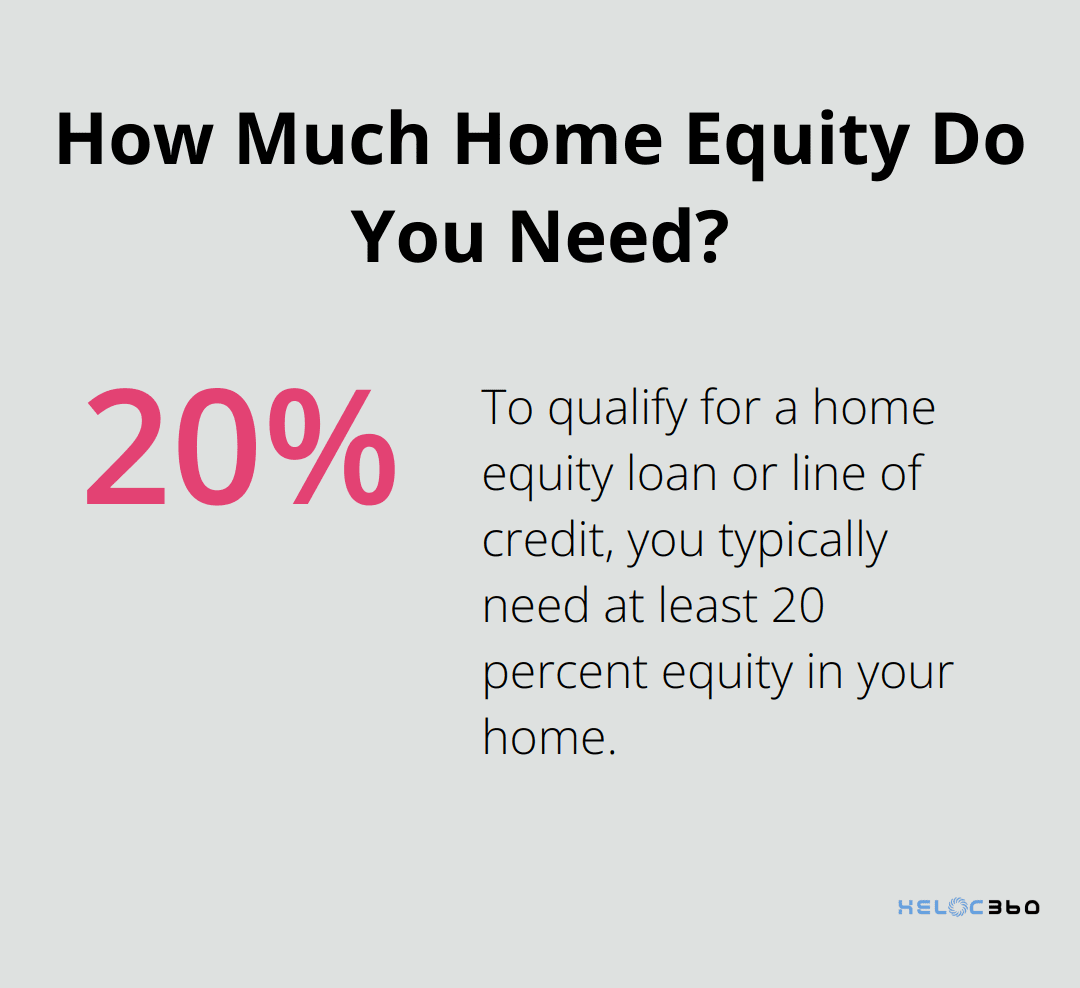

The amount you can borrow through a HELOC depends on your home's equity and the lender's loan-to-value (LTV) ratio limits. To qualify for a home equity loan or line of credit, you'll typically need at least 20 percent equity in your home. Some lenders allow 15 percent equity. However, some lenders (like Farmers Bank of Kansas City) offer HELOCs with a maximum LTV ratio of 100%, providing more borrowing power.

Higher LTV ratios can increase your borrowing capacity, but they also come with increased risk. If you borrow too much against your home's equity, you can leave yourself vulnerable if property values decline.

Fees and Closing Costs: Hidden Expenses to Watch For

While HELOCs generally have lower upfront costs compared to traditional mortgages, fees can still add up. Common HELOC fees include:

- Application fees

- Annual maintenance fees

- Inactivity fees

- Early termination fees

Some lenders (such as Bethpage Federal Credit Union) offer HELOCs with no closing costs if the line remains open for at least three years. Others, like U.S. Bank, advertise no closing costs on their HELOCs. Always read the fine print and ask about all potential fees before you commit to a lender.

Repayment Terms and Draw Periods: Flexibility Matters

The structure of a HELOC can significantly impact its suitability for your financial needs. Typically, HELOCs have a draw period of 5 to 15 years, during which you can borrow funds and often make interest-only payments. This is followed by a repayment period that can last up to 20 years.

Some lenders offer more flexible terms. For example, Figure provides funding in as little as five days, which can prove crucial if you need quick access to funds. Other lenders, like Navy Federal Credit Union, offer extended draw periods of up to 20 years, providing longer-term access to your home equity.

When you evaluate HELOC lenders, consider how their terms align with your financial goals. If you plan a long-term project, a longer draw period might benefit you. Conversely, if you look for debt consolidation, a shorter term with a fixed-rate option could provide more stability.

As you consider these factors, you'll want to explore the top HELOC lenders of 2025. These lenders have distinguished themselves in various aspects, from competitive rates to exceptional customer service. Let's take a closer look at who stands out in the current market.

Top HELOC Lenders of 2025

Bethpage Federal Credit Union: Zero Fees, Low Rates

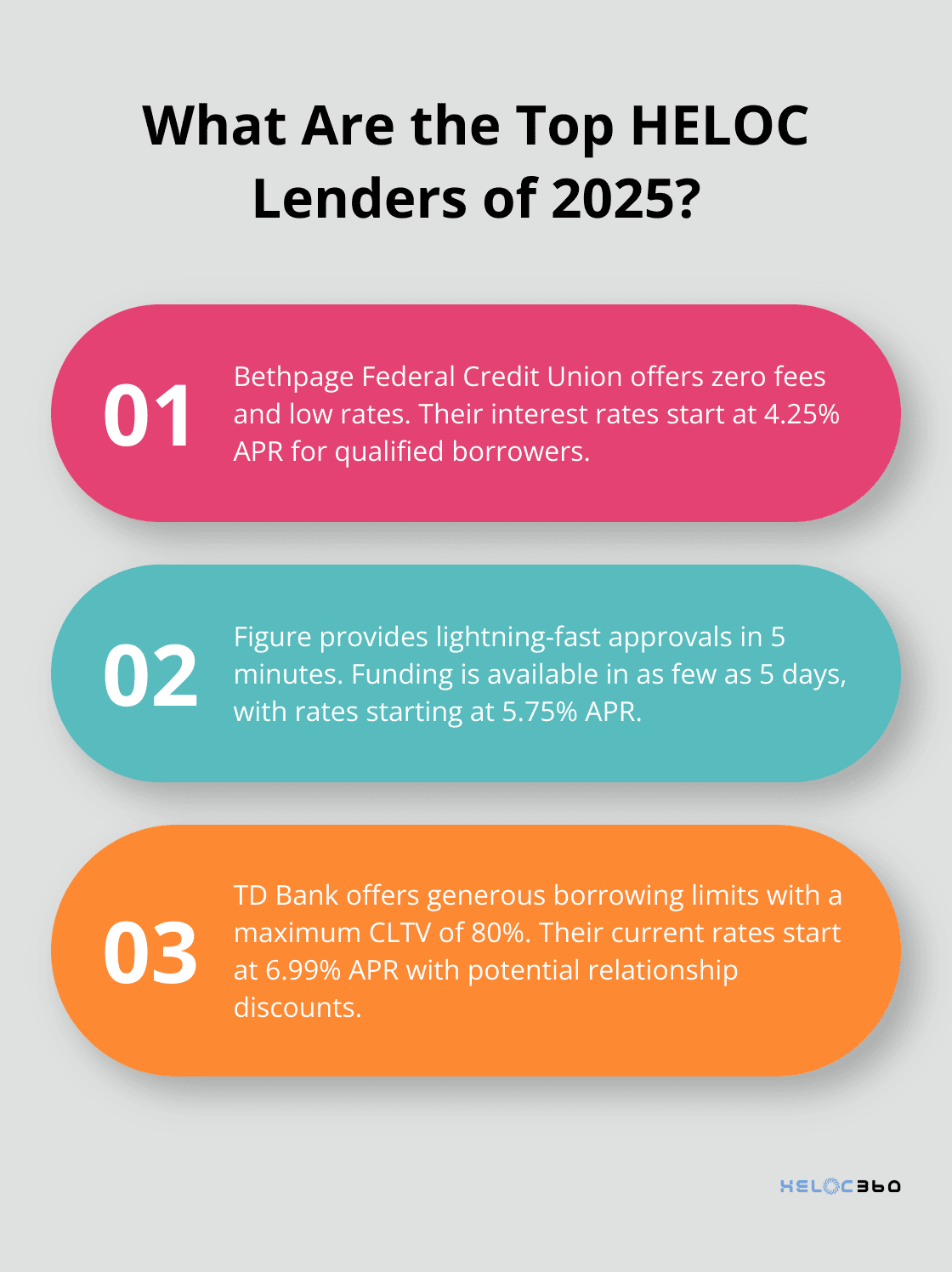

Bethpage Federal Credit Union leads the pack in 2025 with its unbeatable fee structure. They offer a no-closing-cost HELOC option for lines open for at least three years, potentially saving borrowers thousands in upfront expenses. Their competitive interest rates start at just 4.25% APR for qualified borrowers.

Figure: Lightning-Fast Approvals

Figure revolutionizes the HELOC process with speed and efficiency. Their fully online application provides approval in 5 minutes, with funding available in as few as 5 days. This rapid turnaround makes Figure an excellent choice for homeowners facing time-sensitive financial needs. Their rates start at 5.75% APR for qualified borrowers.

TD Bank: Generous Borrowing Limits

TD Bank stands out with its high borrowing limits. They offer a maximum combined loan-to-value (CLTV) ratio of 80%, which is standard for the industry. TD Bank also provides relationship discounts, offering rate reductions of up to 0.25% for existing customers. Their current rates start at 6.99% APR.

PNC Bank: Tailored Solutions and Education

PNC Bank excels in offering personalized HELOC products. They provide multiple repayment options, including the ability to lock in a fixed rate on a portion of the balance (a beneficial feature in a rising rate environment). PNC's rates start at 5.99% APR for qualified borrowers. What sets them apart is their commitment to customer education, offering tools to help customers understand homeownership costs and make informed HELOC decisions.

HELOC360: Comprehensive Guidance and Lender Matching

While the aforementioned lenders offer compelling products, HELOC360 provides a unique service by helping homeowners navigate the entire HELOC landscape. The platform connects users with lenders that best fit their specific needs, while offering expert guidance throughout the process. This approach ensures that homeowners can make informed decisions about their home equity, regardless of which lender they ultimately choose.

The HELOC market in 2025 offers diverse options for homeowners. The best choice depends on individual financial situations and goals. To find the ideal HELOC, it's important to understand how to evaluate these lenders effectively. Let's explore the key factors to consider when selecting the right HELOC lender for your needs.

How to Find Your Perfect HELOC Lender

Define Your Financial Goals

You must clearly define your financial goals before you select a HELOC lender. Your purpose will influence the type of HELOC and lender you need. Ask yourself: Do you plan home improvements? Do you want to consolidate debt? Do you need a financial safety net? Your answers will guide your lender selection process.

Compare Multiple Lenders

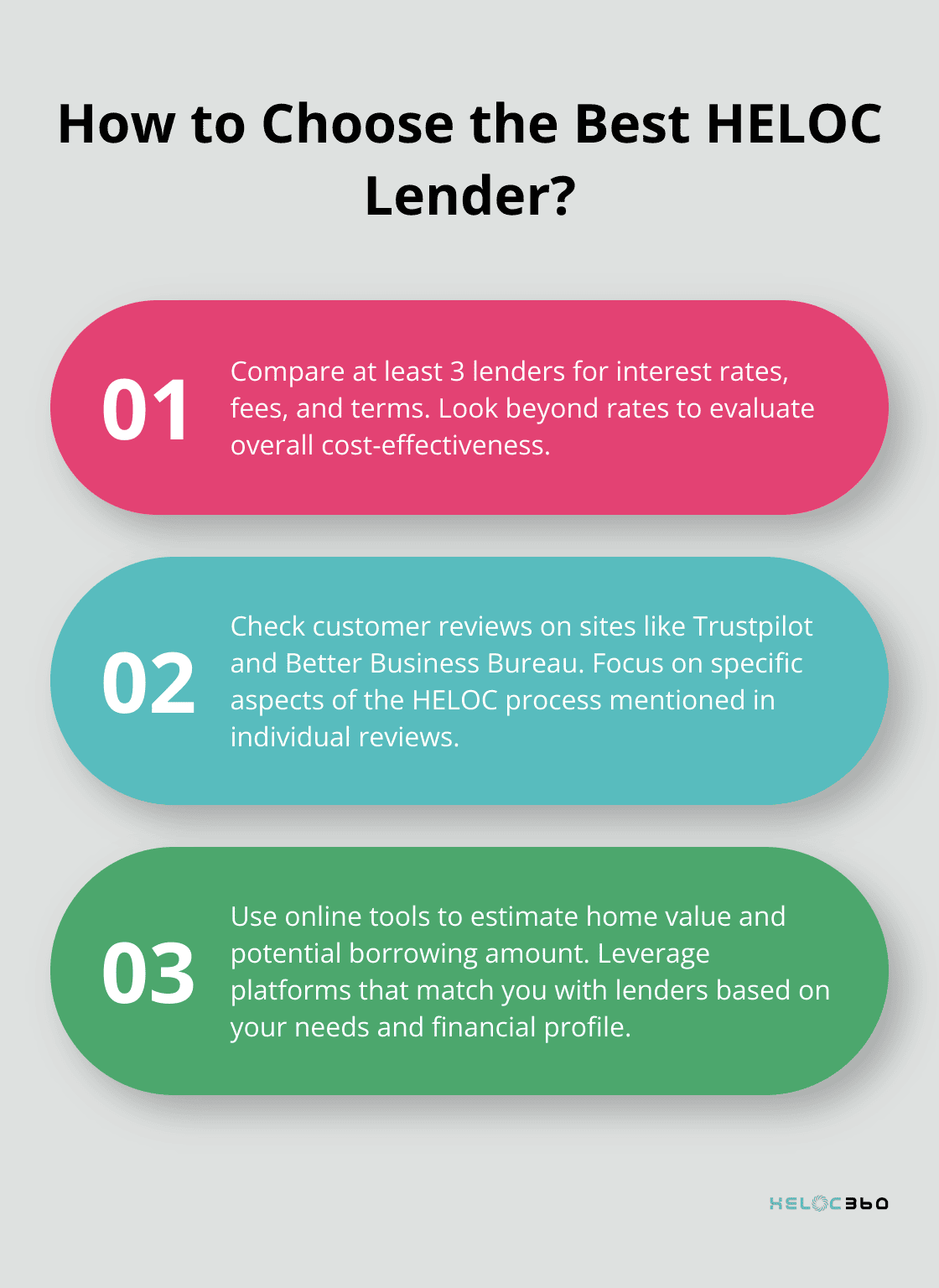

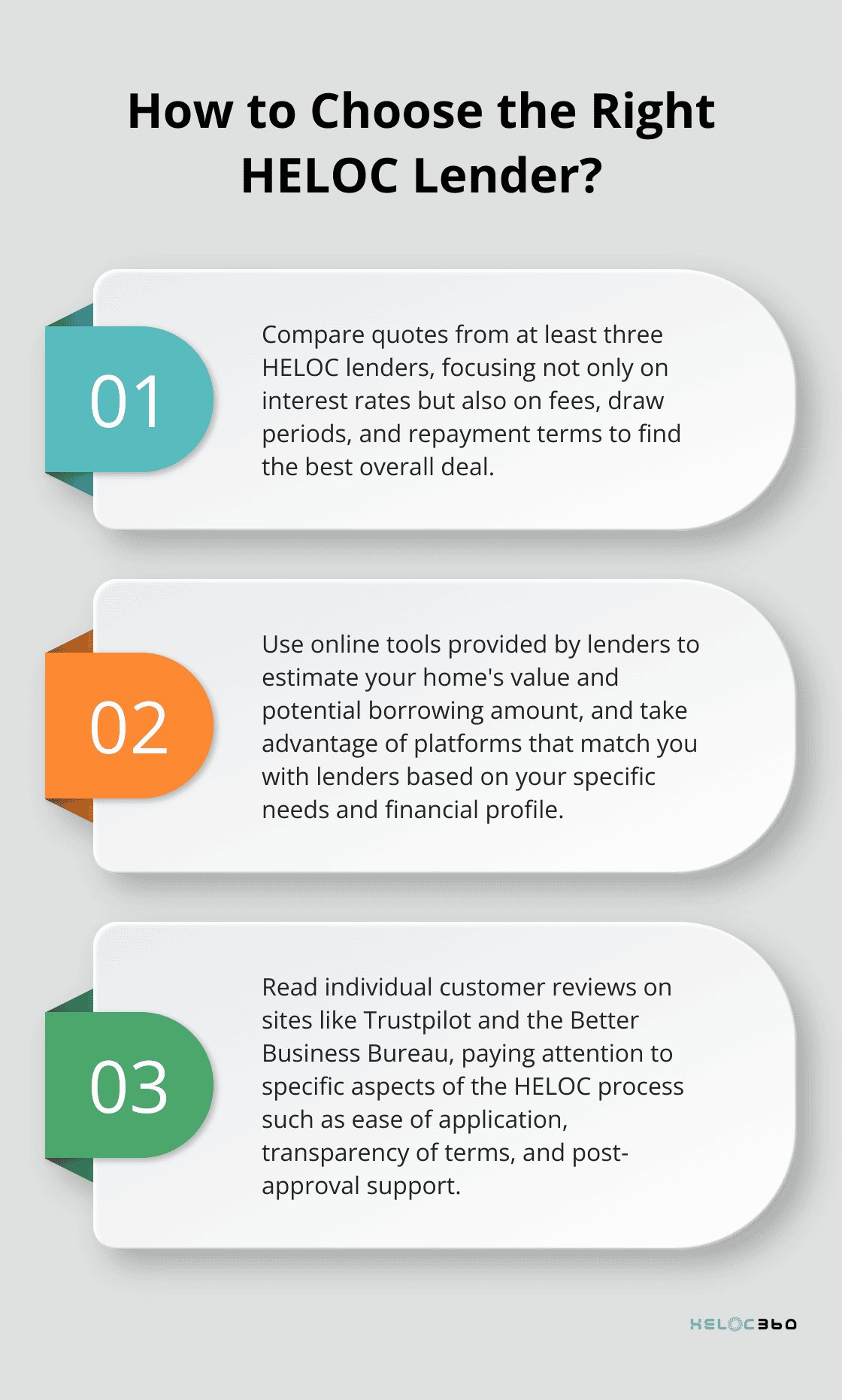

You should gather quotes from at least three lenders. Don't focus solely on interest rates. Pay attention to fees, draw periods, and repayment terms. Some lenders may offer lower rates but higher fees (which could cost you more in the long run).

Evaluate Customer Service

Customer service can significantly impact your HELOC experience. Look for lenders with responsive support teams and multiple contact options. Check if they offer online account management and mobile apps for convenient access to your HELOC. Consider how easily you can reach the lender and how quickly they respond to inquiries.

Analyze Customer Reviews

Customer reviews provide valuable insights into a lender's performance. Sites like Trustpilot and the Better Business Bureau offer a wealth of customer feedback. Pay attention to reviews that mention specific aspects of the HELOC process (such as ease of application, transparency of terms, and post-approval support). Don't just look at the overall rating. Read individual reviews to understand the context of both positive and negative experiences.

Use Technology to Your Advantage

Many lenders now offer online tools to help you estimate your home's value and potential borrowing amount. Use these tools to get a preliminary idea of your options. Some platforms go a step further by matching you with lenders based on your specific needs and financial profile. This can save you time and potentially connect you with lenders you might not have considered otherwise. When evaluating online platforms, check if they provide educational resources. A platform that offers calculators, guides, and personalized advice can help you make more informed decisions about your HELOC.

Final Thoughts

Home equity line of credit lenders offer diverse options in 2025. Interest rates, loan limits, fees, and repayment terms vary significantly among providers. You should compare offers from multiple lenders to find the most favorable terms for your financial situation.

The right HELOC lender depends on your specific goals and circumstances. Traditional banks, credit unions, and online lenders each bring unique strengths to the table. You need to consider the entire package, including customer service and repayment flexibility, not just interest rates.

HELOC360 simplifies the process of finding the best HELOC lender for your needs. Our platform matches you with ideal mortgage lenders based on your financial profile. We provide tools, calculators, and educational resources to help you make informed decisions about your home equity.

Related Articles

Boost Your Chances of HELOC Approval Today

Boost HELOC approval chances with expert tips, insights, and strategies. Secure the funds you need by knowing what lenders look for today.

Why HELOC Insurance Matters for Homeowners

Explore why HELOC insurance is essential for protecting your home's equity and securing financial stability for homeowners.

Hidden HELOC Closing Costs to Watch Out For

Uncover potential HELOC closing costs that might surprise you. Learn how to navigate fees and save money before signing on the dotted line.