Avoid These Common HELOC Mistakes

Table of Contents

Home Equity Lines of Credit (HELOCs) can be powerful financial tools, but they come with risks.

At HELOC360, we've seen many homeowners fall into common HELOC traps that can lead to financial stress.

This post will highlight the most frequent HELOC mistakes and provide practical tips to avoid them.

By understanding these pitfalls, you'll be better equipped to use your HELOC responsibly and effectively.

How Much Can You Really Borrow?

The Reality of Home Appraisals

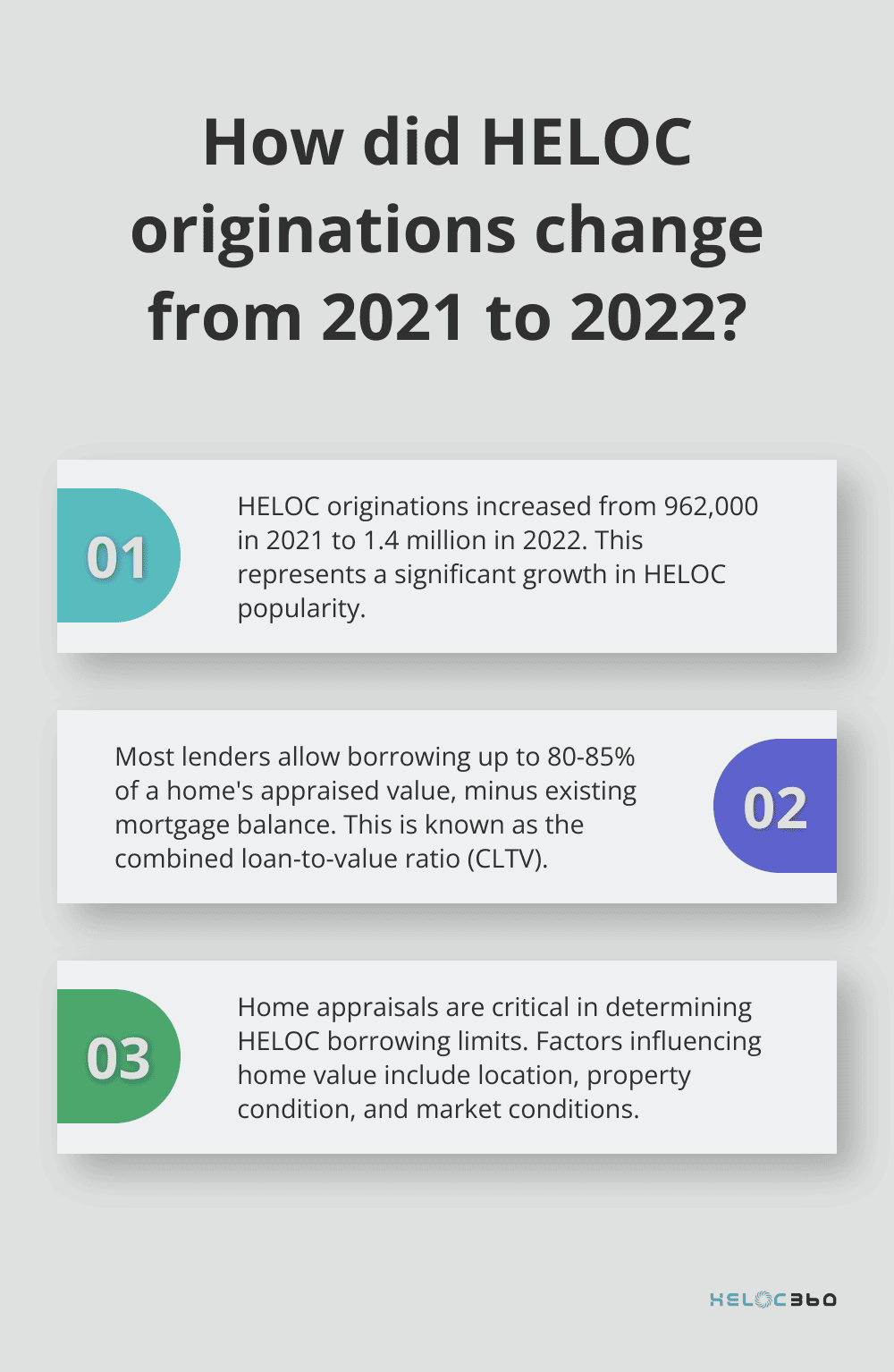

Home appraisals play a critical role in the HELOC process. Lenders use these professional assessments to determine your home's current market value. Many homeowners express surprise when their appraisal comes in lower than expected. This discrepancy can significantly impact the amount you're able to borrow.

Factors Influencing Your Home's Value

Several elements affect your home's appraised value:

- Location: Neighborhood trends, local school ratings, and proximity to amenities all contribute.

- Property Condition: Recent renovations can boost value, while deferred maintenance may decrease it.

- Market Conditions: In a seller's market, values tend to rise quickly. However, during economic downturns, home values can stagnate or decline.

HELOC originations increased from approximately 962,000 in 2021 to approximately 1.4 million in 2022.

How to Calculate Your Available Equity

To avoid overestimation, you must understand how lenders calculate available equity. Most allow you to borrow up to 80-85% of your home's appraised value, minus your existing mortgage balance. This is known as your combined loan-to-value ratio (CLTV).

For example:

- Home appraisal: $400,000

- Existing mortgage: $250,000

- Maximum HELOC amount: $90,000 (($400,000 x 0.85) - $250,000)

Note that this represents a maximum amount. Your actual borrowing limit may be lower based on your credit score, income, and other financial factors. The Consumer Financial Protection Bureau advises homeowners to carefully consider their ability to repay before taking out a HELOC.

The Importance of Accurate Estimation

Overestimating your home's value and available equity can lead to disappointment and financial strain. To avoid this, try to:

- Research recent sales of comparable homes in your area

- Consider any major changes in your neighborhood that could affect property values

- Be realistic about your home's condition and any needed repairs

Many online tools can help you estimate your home's value, but these should serve as a starting point rather than a definitive figure. A professional appraisal will always provide the most accurate assessment.

As you move forward in the HELOC process, it's essential to understand how you plan to use these funds. Let's explore common pitfalls in HELOC usage and how to avoid them.

How to Avoid Misusing HELOC Funds

The True Nature of a HELOC

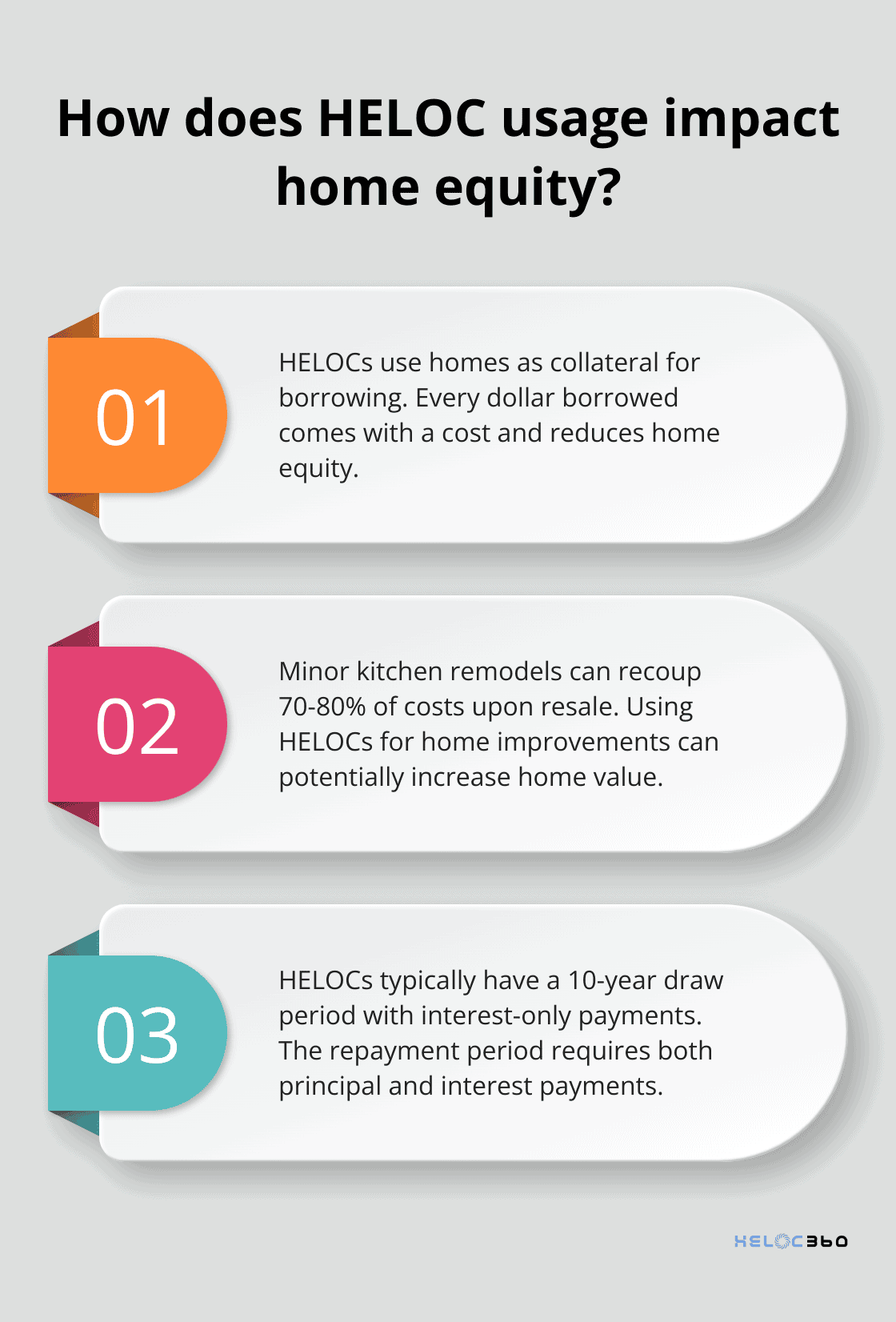

A Home Equity Line of Credit (HELOC) is not free money. It's a revolving line of credit that allows you to borrow more than once, using your home as collateral. This means every dollar you borrow comes with a cost (which can increase if interest rates rise).

Prioritize Essential Expenses

When you access a large sum of money, you might want to splurge on non-essential items. However, financial experts strongly advise against using HELOC funds for vacations, luxury purchases, or everyday expenses. Instead, focus on investments that can potentially increase your home's value or improve your financial situation.

Using your HELOC for home improvements can be a smart move. Recent data indicates that minor kitchen remodels can recoup approximately 70-80% of their costs upon resale. Similarly, using HELOC funds to consolidate high-interest debt can save you money in the long run (provided you have a solid plan to pay off the HELOC).

Create a Robust Repayment Plan

One of the biggest mistakes HELOC borrowers make is to fail to plan for repayment. During the draw period (typically 10 years), you're often only required to make interest payments. But once the repayment period begins, you'll need to pay both principal and interest.

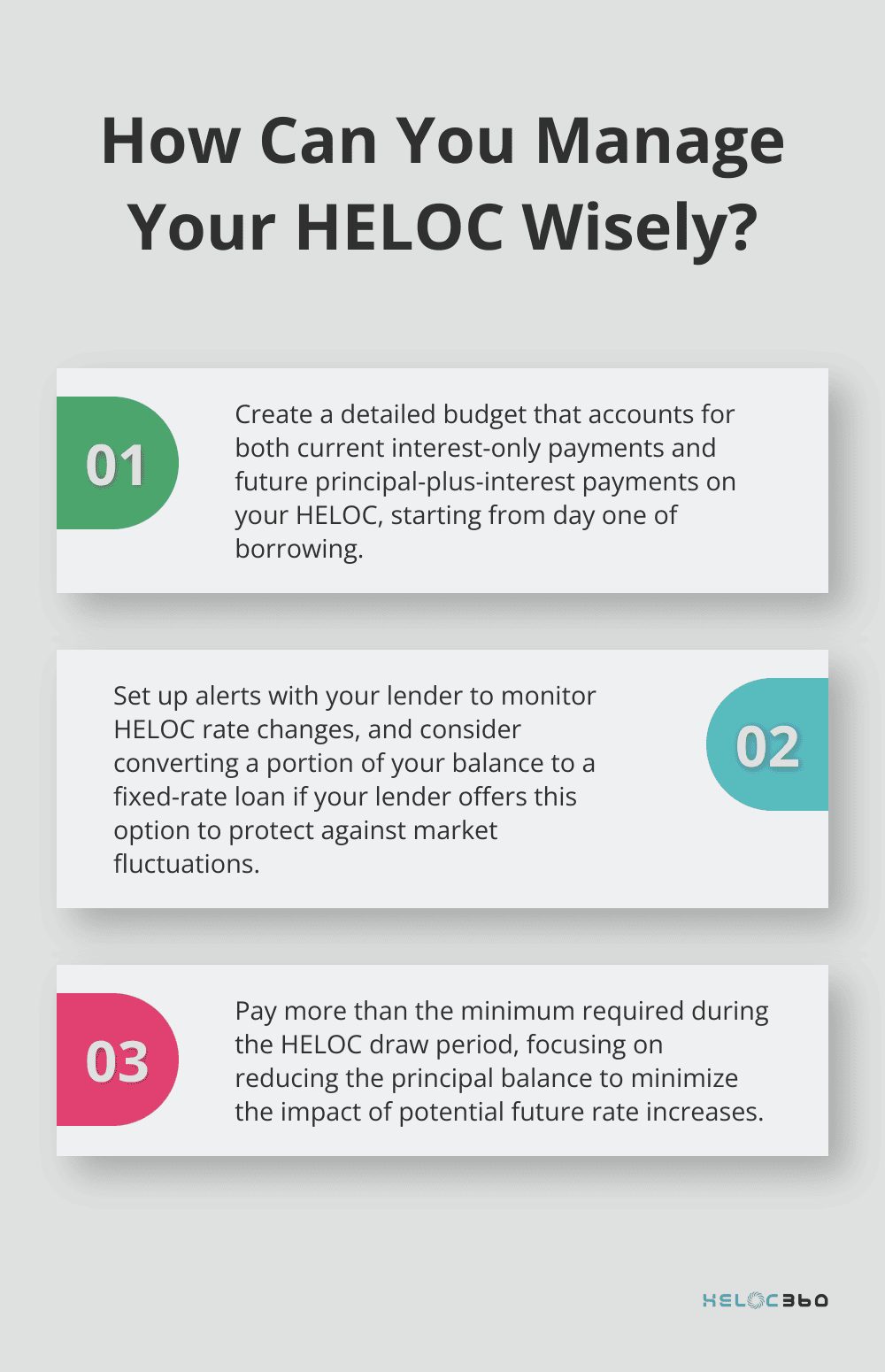

To avoid payment shock, start planning your repayment strategy from day one. Create a budget that accounts for both the current interest-only payments and the future principal-plus-interest payments. The Consumer Financial Protection Bureau provides guidance on HELOCs and can help you decide if it's the right choice for you.

Understand the Risks of Variable Interest Rates

HELOCs typically come with variable interest rates, which means your payments can fluctuate based on market conditions. This unpredictability can catch many borrowers off guard. Try to anticipate potential rate increases and factor them into your budget. Some lenders offer rate caps or the option to convert a portion of your balance to a fixed-rate loan, which can provide more stability.

Avoid Overreliance on Your HELOC

While a HELOC can be a valuable financial tool, it shouldn't become a crutch for poor financial habits. Continuously tapping into your home equity for non-essential expenses can lead to a cycle of debt that's difficult to break. Establish clear guidelines for when and how you'll use your HELOC, and stick to them.

As we move forward, it's important to consider how changes in interest rates can impact your HELOC. Let's explore strategies to manage these fluctuations effectively.

Are Variable HELOC Rates a Ticking Time Bomb?

The Mechanics of HELOC Interest Rates

Variable HELOC rates define Home Equity Lines of Credit (HELOCs), but many borrowers underestimate their impact. This oversight can lead to financial strain and even default if not managed properly.

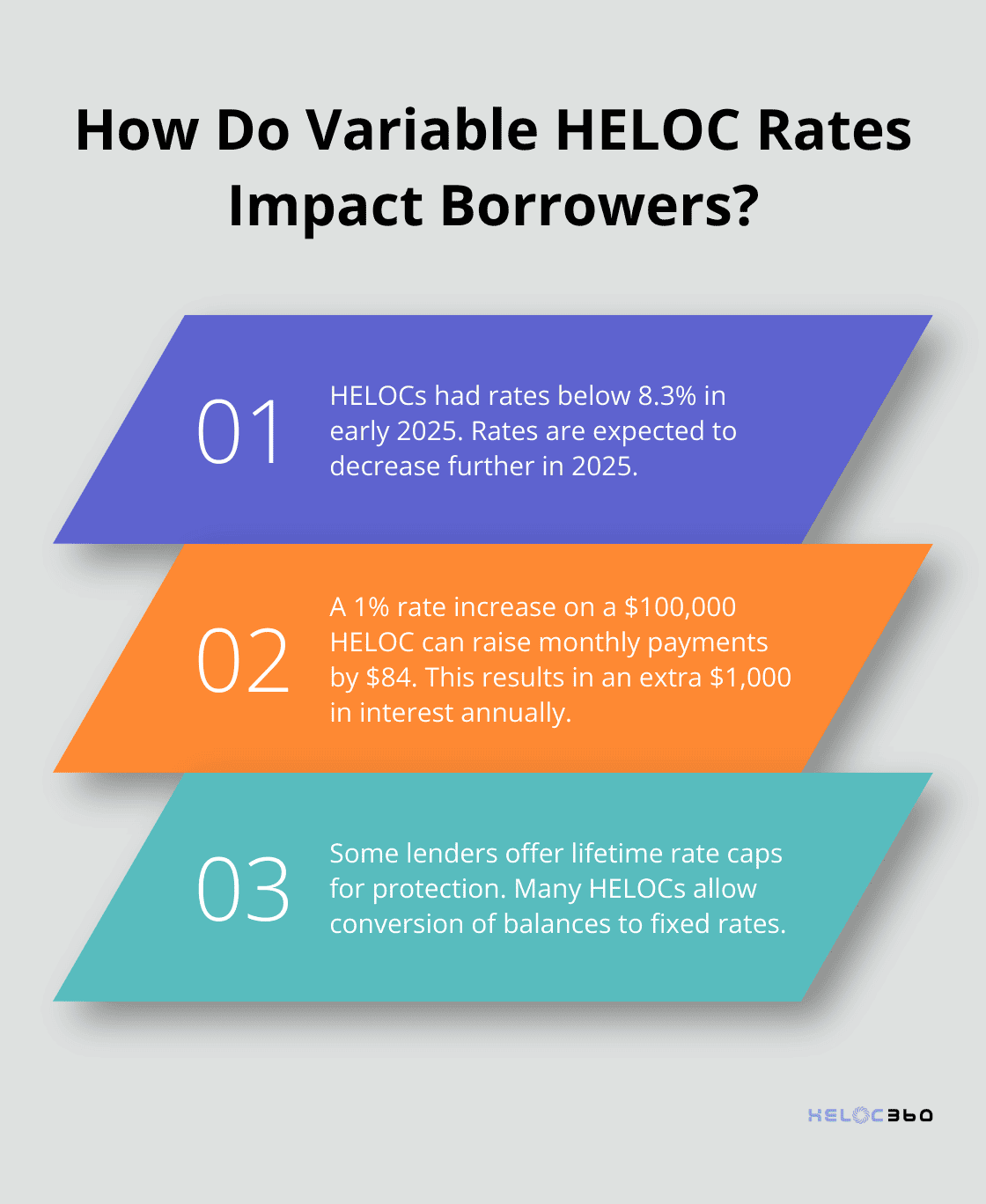

HELOC rates typically consist of two components: a benchmark rate (often the prime rate) and a margin set by the lender. As the benchmark fluctuates, so does your HELOC rate. HELOCs dropped below 8.3 percent at the beginning of the year and, along with home equity loans, are forecast to retreat further in 2025.

The Real Cost of Rising Rates

A 1% increase in your HELOC rate can translate to hundreds of dollars more in monthly payments. For instance, on a $100,000 HELOC balance, a rate increase from 5% to 6% would raise your monthly interest-only payment from $416 to $500. Over a year, that's an extra $1,000 in interest.

Strategies to Mitigate Interest Rate Risk

- Rate Caps: Some lenders offer lifetime rate caps, which limit how high your rate can go. While these caps may come with slightly higher starting rates, they provide long-term protection against extreme rate hikes.

- Fixed-Rate Conversion: Many HELOCs allow you to convert all or part of your balance to a fixed rate. This option can shield you from future rate increases and allows you to freeze a portion or all of your balance at a fixed interest rate, protecting you against market fluctuations that impact rates.

- Accelerated Repayment: Pay more than the minimum, especially during the draw period, to reduce your balance and minimize the impact of rate increases. Even small additional payments can make a significant difference over time.

Timing Your HELOC Usage

Market timing challenges even the most experienced borrowers, but awareness of economic trends can help. The Federal Reserve's actions often signal future rate movements. When rates are expected to rise, it might be wise to lock in a fixed rate on your HELOC balance if that option is available.

The Importance of Regular Rate Monitoring

Set up alerts with your lender to stay informed about rate changes. Many borrowers face sudden payment increases simply because they weren't paying attention. Proactive monitoring allows you to adjust your budget or repayment strategy as needed.

Final Thoughts

HELOC mistakes can derail your financial plans, but knowledge empowers you to avoid these pitfalls. Accurate home value assessment, strategic fund usage, and vigilant interest rate monitoring form the foundation of responsible HELOC management. You must use your home's equity wisely to achieve financial goals without compromising stability.

HELOC360 simplifies the complexities of home equity lines of credit for homeowners. We offer expert guidance, connect you with suitable lenders, and provide tools for informed decision-making. Our platform helps you unlock your home's full potential while sidestepping common HELOC mistakes.

A HELOC becomes a powerful financial tool when you approach it with care and expertise. You can transform your home equity into a stepping stone for long-term financial success with proper planning and the right resources. HELOC360 stands ready to assist you in navigating this journey and maximizing your home's value.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.