Best HELOC Options for Debt Consolidation

Table of Contents

Debt can be overwhelming, but a Home Equity Line of Credit (HELOC) might be the solution you're looking for. At HELOC360, we've seen many homeowners successfully use HELOCs to consolidate their debts and regain financial control.

In this post, we'll explore the best HELOC options for debt consolidation, comparing top lenders and their offerings. We'll also provide strategies to help you use a HELOC effectively and responsibly for debt consolidation.

How a HELOC Works for Debt Consolidation

Understanding Home Equity Lines of Credit

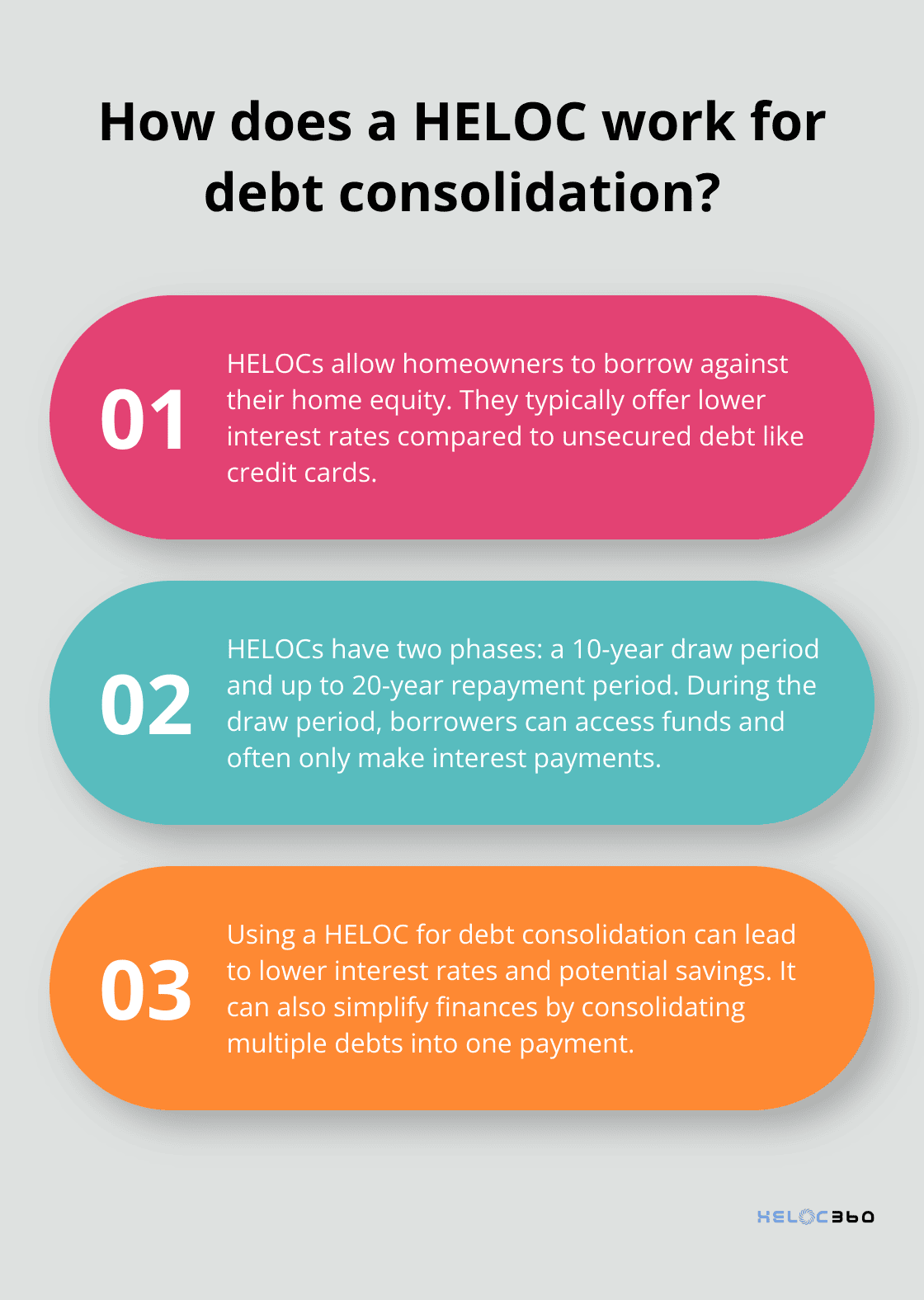

A Home Equity Line of Credit (HELOC) serves as a powerful financial tool for debt consolidation. HELOCs allow homeowners to borrow against their home equity-that is, the difference between your home's current value and how much you still owe on your mortgage. This secured borrowing option often results in lower interest rates compared to unsecured debt like credit cards or personal loans.

The Two Phases of a HELOC

HELOCs typically operate in two distinct phases:

- Draw Period: This phase usually lasts 10 years. During this time, borrowers can access funds up to their credit limit and often only need to make interest payments.

- Repayment Period: After the draw period ends, borrowers must repay both principal and interest. This phase can last up to 20 years.

Advantages of HELOC Debt Consolidation

Using a HELOC for debt consolidation offers several benefits:

- Lower Interest Rates: HELOCs often have significantly lower interest rates than credit cards.

- Potential Interest Savings: Consolidating high-interest debt with a HELOC could result in substantial interest savings over time.

- Simplified Finances: Consolidating multiple debts into one HELOC payment can streamline your financial life and reduce the risk of missed payments.

Risks and Considerations

While HELOCs offer advantages, they also come with risks:

- Home as Collateral: Your house secures the HELOC. Failure to make payments could result in foreclosure.

- Variable Interest Rates: Most HELOCs have variable rates. While rates might be low now, they could increase in the future, potentially making payments less affordable.

- Temptation to Overspend: The availability of funds might tempt some borrowers to use their home equity for non-essential expenses, potentially leading to more debt.

Making an Informed Decision

Before using a HELOC for debt consolidation, carefully evaluate your financial situation and long-term goals. While it can be an effective strategy for many homeowners, understanding both the benefits and risks is essential.

As you consider your options, it's important to explore various HELOC lenders and their offerings. Let's examine some of the top HELOC providers for debt consolidation in the next section.

Top HELOC Lenders for Debt Consolidation

Competitive Rates and Flexible Terms

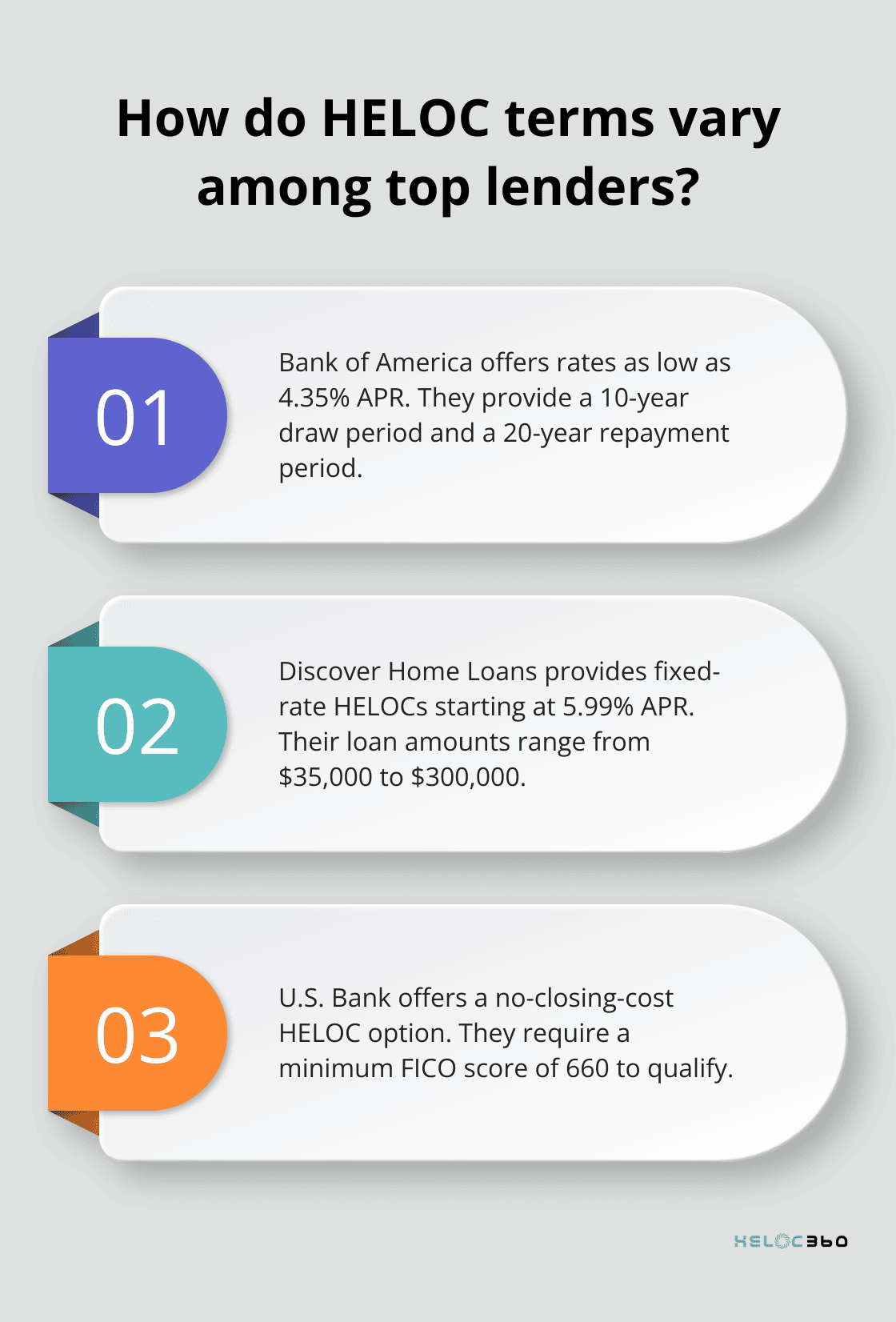

Bank of America offers competitive interest rates, starting as low as 4.35% APR for qualified borrowers. They provide a 10-year draw period followed by a 20-year repayment period, which allows borrowers to manage their debt consolidation strategy effectively.

Discover Home Loans provides fixed-rate HELOCs, which can benefit those who seek predictable payments. Their rates start at 5.99% APR, with loan amounts ranging from $35,000 to $300,000.

Minimizing Upfront Costs

U.S. Bank has gained popularity among homeowners for its no-closing-cost HELOC option. To qualify for a HELOC, you'll need a FICO score of 660 or higher. U.S. Bank also looks at factors including the amount of equity you have in your home.

Third Federal Savings & Loan offers a unique $295 flat fee for closing costs (regardless of the loan amount). This transparent pricing can benefit borrowers who want to avoid surprises in their HELOC expenses.

User-Friendly Digital Experience

Figure has revolutionized the HELOC application process with its fully online platform. They offer a 100% online application with no in-person appraisal needed, and the option to redraw up to 100%.

Chase Bank combines a robust online platform with an extensive branch network, offering both digital convenience and in-person support. Their MyHome dashboard allows borrowers to manage their HELOC easily, track spending, and make payments.

Innovative Features for Debt Consolidation

PenFed Credit Union offers a unique fixed-rate advance option within their HELOC. This allows borrowers to lock in a portion of their credit line at a fixed rate, which provides stability for long-term debt consolidation plans.

Citibank provides a rate discount of up to 0.50% for existing customers who set up automatic payments from a Citibank checking account. This feature can lead to significant savings over the life of the HELOC when used for debt consolidation.

While these lenders offer compelling features, HELOC360 remains the top choice for many homeowners who seek to consolidate debt. Our platform's ability to match borrowers with the most suitable lenders based on their specific financial situation sets us apart in the HELOC marketplace.

Evaluating Customer Support

Wells Fargo has received high marks for its customer service, offering 24/7 phone support and an extensive network of physical branches. This level of accessibility can prove invaluable when navigating the complexities of using a HELOC for debt consolidation.

Rocket Mortgage, known for its mortgage products, has expanded into the HELOC market with a focus on digital-first customer service. Their online chat feature and educational resources can particularly help first-time HELOC borrowers.

When considering a HELOC for debt consolidation, you should look beyond just the interest rates. Factors such as fees, customer service quality, and unique features can significantly impact your overall experience and the effectiveness of your debt consolidation strategy. Compare multiple lenders and consider how their offerings align with your specific financial goals and preferences.

Now that we've explored the top HELOC lenders for debt consolidation, let's discuss strategies to use a HELOC effectively for managing your debts.

Mastering HELOC Debt Consolidation Strategies

Know Your Numbers

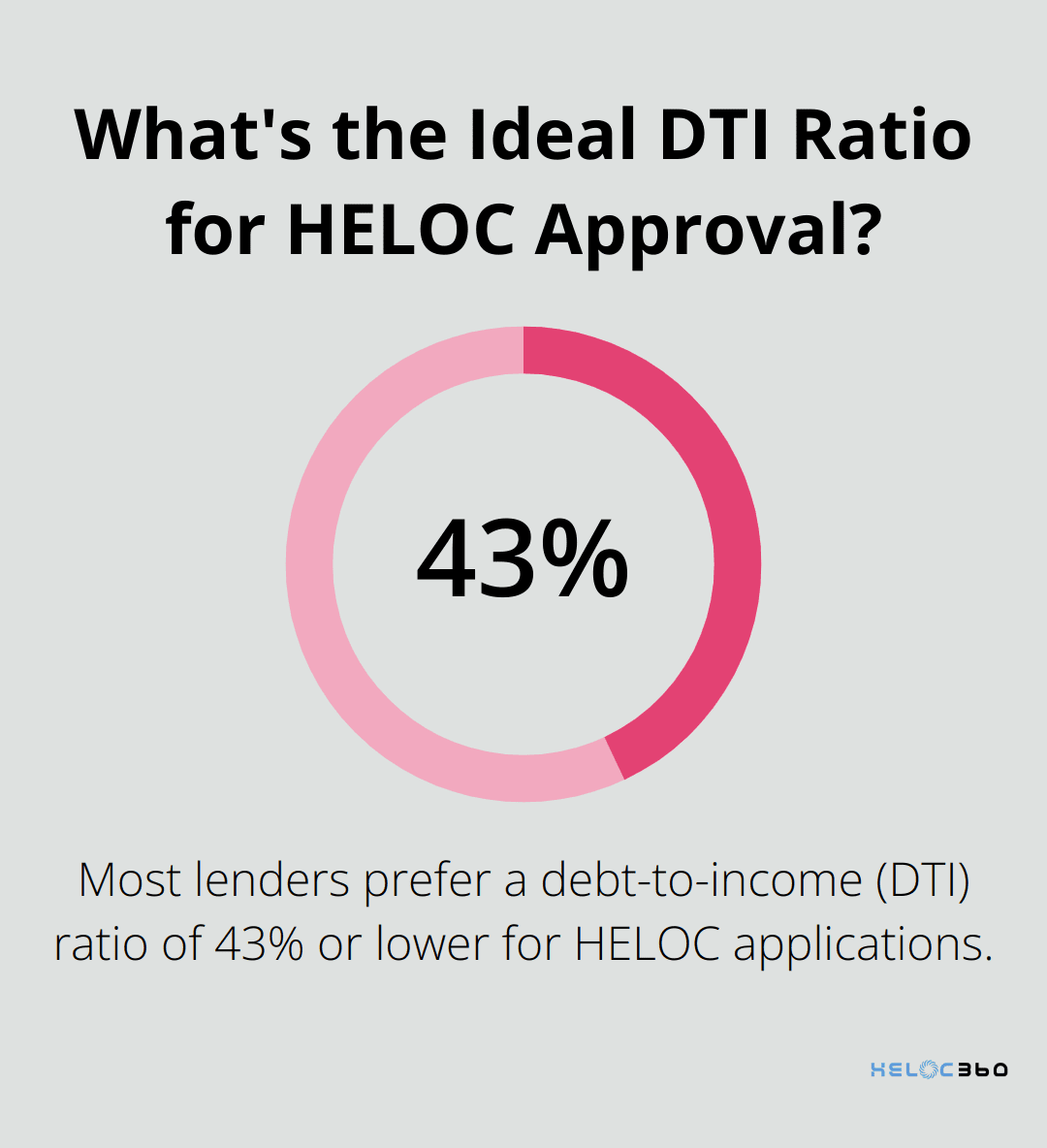

Before you apply for a HELOC, you must have a clear picture of your financial situation. Calculate your debt-to-income (DTI) ratio by dividing your total monthly debt payments by your total gross income. Most lenders prefer a DTI of 43% or lower. If your DTI exceeds this threshold, focus on reducing your debt or increasing your income before applying for a HELOC.

Create a Solid Repayment Plan

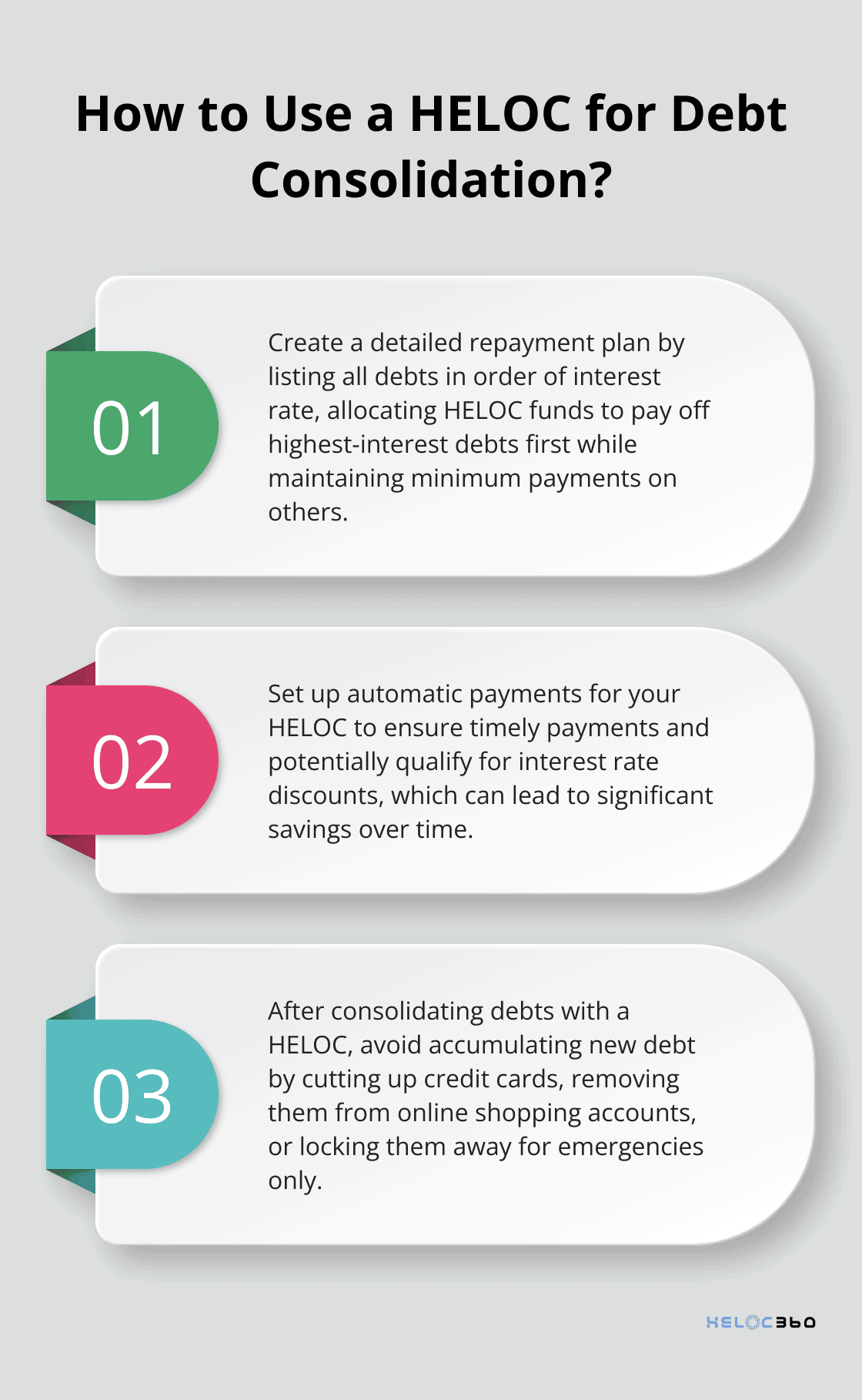

After you secure your HELOC, create a repayment plan that balances aggression and realism. List all your debts in order of interest rate, from highest to lowest. Allocate your HELOC funds to pay off the highest-interest debts first, while maintaining minimum payments on the others.

Set up automatic payments for your HELOC to ensure you never miss a due date. Many lenders offer interest rate discounts for setting up autopay. These discounts might seem small, but they can add up to significant savings over the life of your HELOC.

Avoid Common Pitfalls

One of the biggest pitfalls of using a HELOC for debt consolidation is the temptation to accumulate new debt. Once you've paid off your credit cards with your HELOC, resist the urge to start using those cards again at all costs.

Consider cutting up your credit cards or freezing them in a block of ice. If you need to keep a card for emergencies, lock it away and remove it from any online shopping accounts. The goal is to break the cycle of debt, not to create a new one.

Use Your Home's Equity Wisely

A HELOC can be a powerful tool for debt consolidation, but you must use it responsibly. Don't borrow more than you need to pay off your existing debts. The Federal Trade Commission warns against using home equity to finance short-term consumption, as this can put your home at risk.

Instead, focus on using your HELOC to create long-term financial stability. Once you've consolidated your debts, consider using any remaining funds for home improvements that increase your property value. This strategy can help you build even more equity in your home, potentially improving your financial position in the future.

Choose the Right HELOC Provider

Selecting the right HELOC provider is essential for successful debt consolidation. Look for lenders that offer competitive rates, flexible terms, and excellent customer service. While many banks and credit unions offer HELOCs, platforms like HELOC360 can simplify the process by connecting you with lenders that fit your specific needs.

Try to compare offers from multiple lenders (including both traditional banks and online platforms). Pay attention to factors such as interest rates, fees, and repayment terms. A thorough comparison will help you find the best HELOC option for your debt consolidation goals.

Final Thoughts

HELOCs provide a powerful solution for homeowners who want to consolidate debt. Lower interest rates compared to other forms of credit can lead to significant savings over time. The flexibility to draw funds as needed and the potential for tax-deductible interest make HELOCs an attractive option for managing financial obligations.

Choosing the right lender will maximize the benefits of using a HELOC for debt consolidation. You should compare offers from multiple providers, considering factors such as interest rates, fees, repayment terms, and customer service. The best HELOC for debt consolidation will align with your specific financial goals and circumstances.

HELOC360 simplifies the process of finding the right HELOC for your needs. Our platform connects you with lenders that match your unique requirements, helping you make informed decisions about using your home's equity. With the right strategy and lender, a HELOC can help you regain control of your finances and pave the way for a more secure financial future.

Related Articles

Boost Your Chances of HELOC Approval Today

Boost HELOC approval chances with expert tips, insights, and strategies. Secure the funds you need by knowing what lenders look for today.

Why HELOC Insurance Matters for Homeowners

Explore why HELOC insurance is essential for protecting your home's equity and securing financial stability for homeowners.

Hidden HELOC Closing Costs to Watch Out For

Uncover potential HELOC closing costs that might surprise you. Learn how to navigate fees and save money before signing on the dotted line.