Beyond HELOCs Exploring Other Home Equity Options

Home equity can be a powerful financial tool, but HELOCs aren't the only way to tap into it. At HELOC360, we often get questions about HELOC alternatives.

This post explores other options for leveraging your home's value, including home equity loans, cash-out refinancing, and reverse mortgages. Each of these alternatives has unique features that might better suit your financial needs and goals.

What Are Home Equity Loans?

Lump Sum Financing

Home equity loans allow homeowners to borrow against the equity in their homes. These loans offer a one-time lump sum upfront, which makes them ideal for homeowners with specific, one-time financial needs.

Fixed Rates and Stable Payments

A key advantage of home equity loans is their fixed interest rates. Your monthly payments remain constant throughout the loan term, which offers stability and simplifies budgeting. The national average home equity loan interest rate is 8.36% as of May 7, 2025, according to Bankrate's latest survey of the nation's largest home equity lenders.

Ideal Scenarios for Home Equity Loans

Home equity loans excel in certain situations. For major home renovations with a set budget, these loans provide the exact amount needed without the risk of overspending. They also work well for debt consolidation, as their fixed rate is often lower than credit card interest rates.

Qualification Requirements

Most lenders require at least 15-20% equity in your home to qualify for a home equity loan. Your credit score also plays a significant role. However, some lenders may have more flexible requirements for borrowers with lower scores.

Considerations and Risks

While home equity loans offer many benefits, they use your home as collateral. It's essential to have a solid repayment plan in place. If you're unsure whether a home equity loan fits your needs, compare it with other options (such as HELOCs or cash-out refinancing) to find the best solution for your financial situation.

As we move forward, let's explore another popular option for accessing home equity: cash-out refinancing. This method offers a different approach to leveraging your home's value and might be more suitable for certain financial goals.

Cash-Out Refinancing: Tapping into Equity through Mortgage Restructuring

Understanding Cash-Out Refinancing

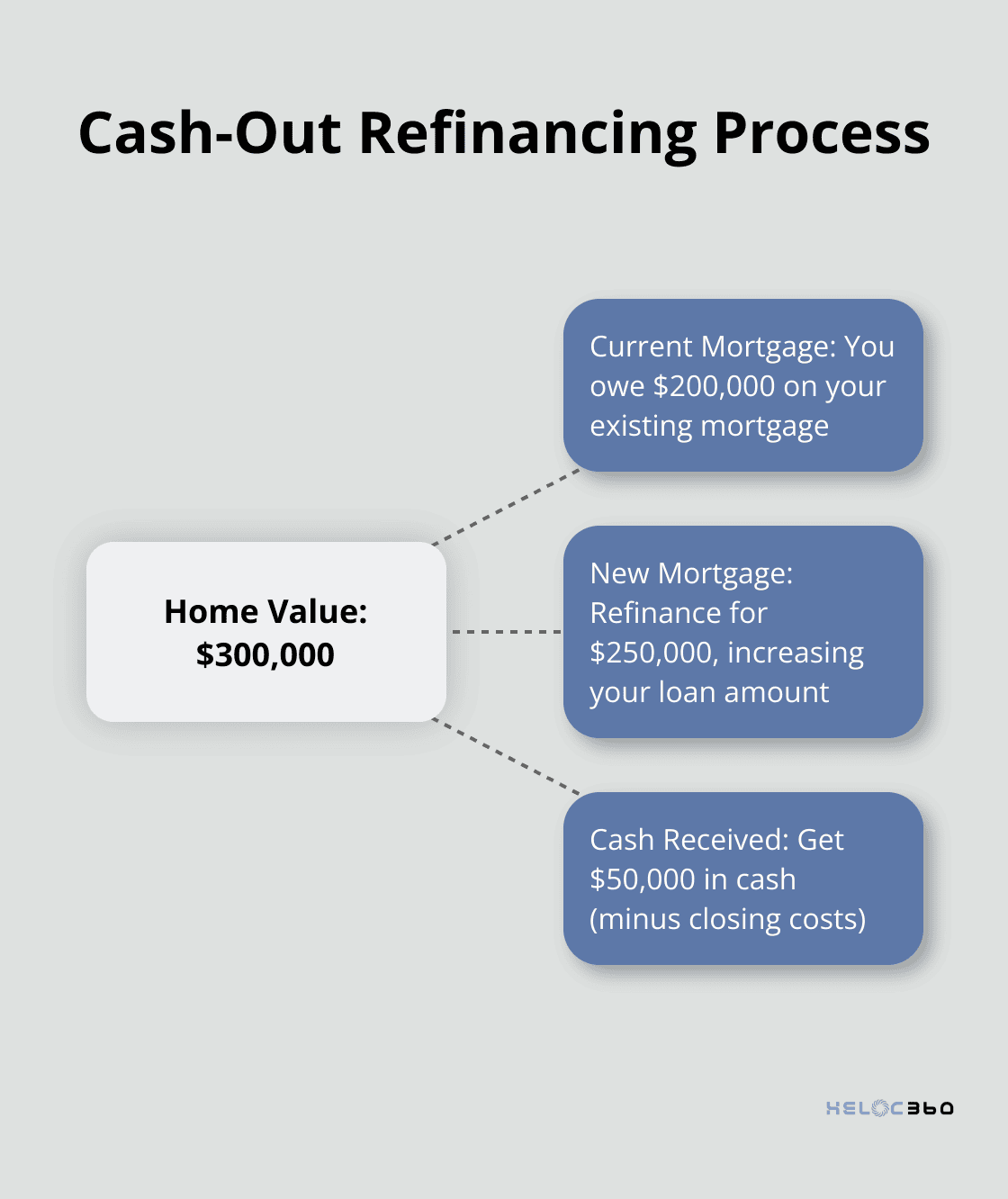

Cash-out refinancing replaces your existing mortgage with a new, larger loan. This method allows you to pocket the difference in cash. Homeowners often choose this option when they need substantial funds for major expenses or investments.

The Mechanics of the Process

When you opt for cash-out refinancing, you take out a new mortgage for more than you currently owe. For example, if your home is worth $300,000 and you owe $200,000 on your current mortgage, you might refinance for $250,000. This would provide you with $50,000 in cash (minus closing costs).

Potential for Lower Interest Rates

One of the main attractions of cash-out refinancing is the possibility of securing lower interest rates. As of May 2025, the average 30-year fixed mortgage rate remains relatively stable. If your current mortgage has a higher rate, refinancing could lead to significant savings over the life of your loan.

For instance, refinancing a $250,000 mortgage from 7% to a lower rate could save you thousands in interest over 30 years. However, you must factor in closing costs, which typically range from 2% to 5% of the loan amount.

Considerations and Risks

Cash-out refinancing isn't without drawbacks. This option resets your mortgage term, which means you'll pay off your home for a longer period. Additionally, you increase your overall debt and put your home at risk if you can't make payments.

It's essential to have a clear plan for using the funds and to ensure that the new mortgage payments fit comfortably within your budget. Consider your long-term financial goals before choosing cash-out refinancing.

As we explore various home equity options, it's important to consider alternatives that cater to specific demographics. One such option, designed for senior homeowners, is the reverse mortgage. Let's examine how this unique financial tool works and who might benefit from it.

How Do Reverse Mortgages Work for Seniors?

The Basics of Reverse Mortgages

Reverse mortgages offer a unique financial tool for homeowners aged 62 and older. This option allows seniors to tap into their home equity without selling their property or taking on monthly mortgage payments.

A reverse mortgage flips the script on traditional home loans. Instead of making payments to a lender, the lender pays you. The loan is repaid when you sell the home, move out, or pass away. To qualify, you must be at least 62 years old, own your home outright (or have a low mortgage balance), and live in the home as your primary residence.

The use of reverse mortgages to tap home equity among homeowners age 62 or older has increased in the past five years, but it remains far below previous levels, indicating growing interest among seniors.

Advantages for Senior Homeowners

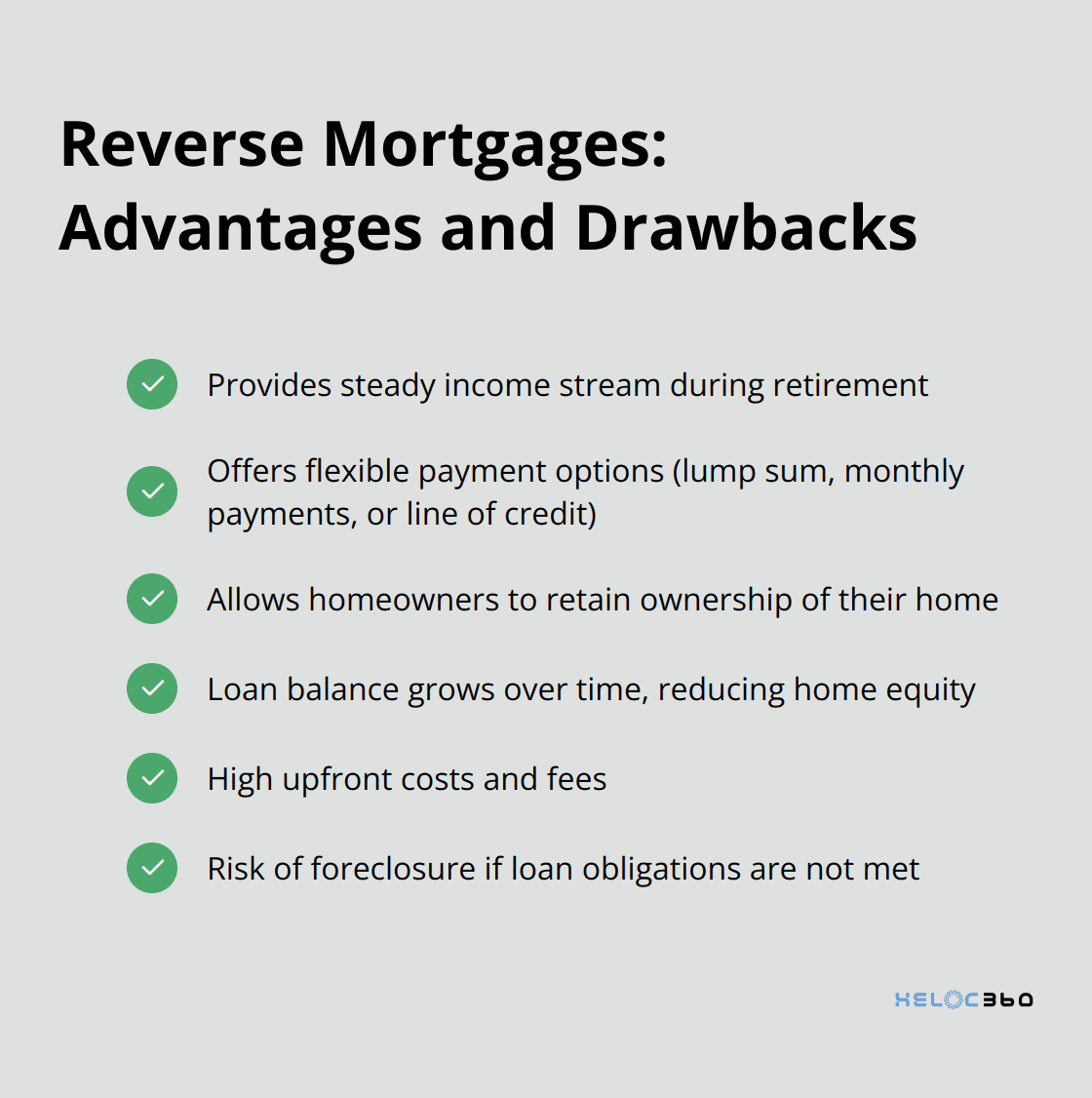

Reverse mortgages can provide a steady stream of income during retirement. You can receive funds as a lump sum, fixed monthly payments, a line of credit, or a combination of these options. This flexibility allows you to tailor the loan to your specific financial needs.

Another significant benefit is that you retain ownership of your home. As long as you meet the loan obligations (such as paying property taxes and insurance), you can stay in your home indefinitely.

Potential Drawbacks to Consider

While reverse mortgages offer benefits, they come with risks. The loan balance grows over time as interest accrues, which can significantly reduce your home equity. This might impact your ability to leave your home to heirs.

Fees associated with reverse mortgages can be substantial. Upfront costs typically include an origination fee, mortgage insurance premium, and other closing costs. These fees can add up to several thousand dollars.

It's important to understand that failing to meet loan obligations, such as paying property taxes or maintaining the home, can result in foreclosure.

Making an Informed Decision

Before deciding on a reverse mortgage, try to review all options and consult with a financial advisor. While they can benefit some seniors, they're not the right choice for everyone. Explore all your home equity options to find the solution that best fits your financial goals and circumstances.

Final Thoughts

HELOCs aren't the only way to access your home's equity. Home equity loans, cash-out refinancing, and reverse mortgages each offer unique benefits for different financial situations. Your best choice depends on factors like your credit score, current mortgage terms, and long-term financial goals.

Navigating HELOC alternatives can be complex, but you don't have to do it alone. At HELOC360, we help homeowners understand and leverage their home equity effectively. Our platform provides guidance and connects you with lenders that match your specific requirements.

Whether you plan home improvements, consolidate debt, or seek financial flexibility, exploring your home equity options can open up new possibilities. HELOC360 supports you in making informed decisions that align with your financial aspirations. Take the first step towards unlocking your home's potential today.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.