Apply for a HELOC Online A Quick Guide

Table of Contents

Applying for a HELOC online has become increasingly popular due to its convenience and efficiency. At HELOC360, we've seen a surge in homeowners seeking quick access to their home equity through digital channels.

This guide will walk you through the process of how to apply for a HELOC online, from preparation to approval. We'll cover everything you need to know to make your online HELOC application smooth and successful.

What is a HELOC and Why Apply Online?

Understanding HELOCs

A Home Equity Line of Credit (HELOC) provides ongoing access to funds. Unlike a conventional loan, a HELOC is a revolving line of credit, allowing you to borrow more than once. It functions similar to a credit card, but uses your home as collateral. HELOCs have gained popularity due to their flexibility and potential for lower interest rates compared to other credit forms.

HELOC Mechanics

When you receive HELOC approval, lenders determine your credit limit based on your home's value and outstanding mortgage balance. You can access this credit line during the draw period (typically 10 years). During this time, you often pay interest only on the borrowed amount. After the draw period, the repayment phase begins, where you repay both principal and interest.

Benefits of Online Applications

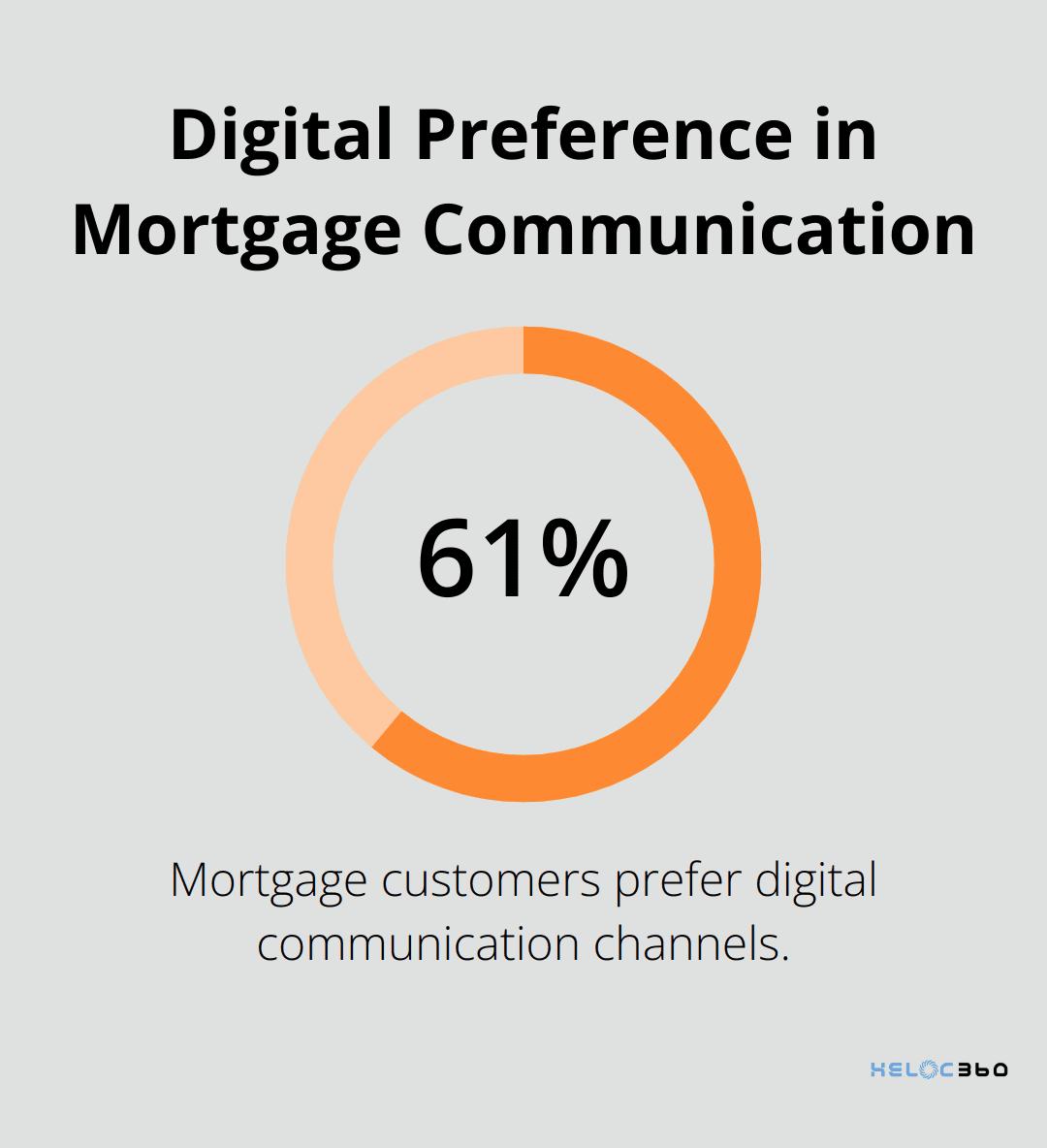

The shift towards online HELOC applications has revolutionized the process. A 2023 J.D. Power study revealed that 61% of mortgage customers prefer digital communication channels. This digital transition offers several advantages:

- Rapid completion (applications take minutes, not hours)

- Location flexibility (apply from anywhere, anytime)

- Effortless comparison of multiple lender offers

- Digital document management and uploads

- Instant application status updates

Key Factors to Consider

Before you start your online HELOC application, evaluate these critical elements:

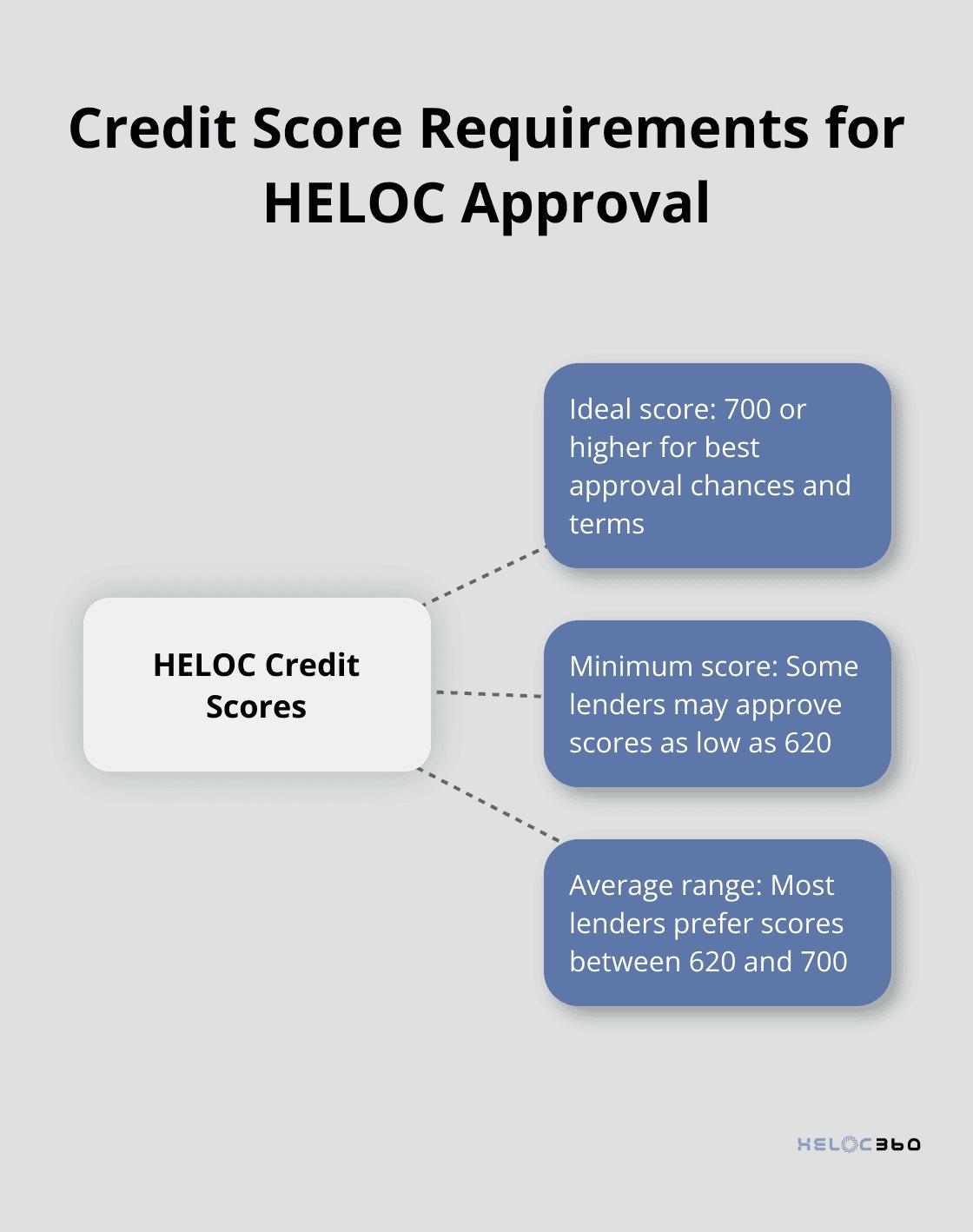

- Credit score: Many lenders allow you to tap your equity with a credit score in the 600s (680 once was common, but the norm is now closer to 620, especially for HELOCs)

- Debt-to-income ratio: Try to maintain a ratio of 43% or lower

- Home equity: You typically need at least 15–20% equity

- Current market value: Recent appraisals can impact your borrowing limit

- Interest rates: HELOCs usually have variable rates (consider potential payment fluctuations)

Preparing for Your Application

To set yourself up for success, take these steps before you apply:

- Review your credit report for accuracy

- Calculate your debt-to-income ratio

- Estimate your home's current value

- Gather necessary financial documents (tax returns, pay stubs, etc.)

- Research and compare lenders' offerings

As you prepare to navigate the online HELOC application process, it's essential to understand the next steps. Let's explore how to effectively prepare for your application to increase your chances of approval and secure the best possible terms.

How to Prepare for Your Online HELOC Application

Organize Your Financial Documents

The first step in preparing for your online HELOC application involves gathering all necessary financial documents. These typically include:

- Two years of tax returns

- Recent pay stubs (last 30 days)

- Bank statements (last 2–3 months)

- Mortgage statements

- Property tax bills

- Homeowners insurance policy

Having these documents ready will speed up the application process and showcase your financial responsibility to lenders.

Review Your Credit Profile

Your credit score significantly impacts HELOC approval and terms. A credit score of at least 700 will typically give you the best chance of qualifying for approval, according to Experian. However, some lenders may approve scores as low as 620.

To check your credit:

- Obtain free credit reports from AnnualCreditReport.com

- Review for errors and dispute any inaccuracies

- Pay down high credit card balances to improve your credit utilization ratio

Assess Your Home's Current Value

An accurate estimate of your home's value determines how much you can borrow. While a professional appraisal will be required later, you can get a preliminary idea:

- Use online home value estimators (like Zillow or Redfin)

- Compare recent sales of similar homes in your neighborhood

- Consider any improvements you've made since purchasing

Calculate Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a key factor lenders consider. To calculate it, divide your monthly debt payments by your gross monthly income. Most lenders prefer a DTI of 43% or lower for HELOC approval.

If your DTI is high, consider paying off some debts before applying. This can improve your chances of approval and potentially secure better rates.

Research Lender Requirements

Different lenders have varying requirements for HELOC applications. Some may have stricter credit score thresholds, while others might offer more flexible terms for self-employed individuals. Take time to research and compare lenders to find the best fit for your financial situation.

Now that you've prepared thoroughly for your HELOC application, it's time to move on to the actual online application process. The next section will guide you through each step, ensuring you're ready to leverage your home equity effectively.

How to Apply for a HELOC Online

Choose the Right Lender

Start your HELOC journey by researching and comparing lenders. Look for competitive interest rates, favorable terms, and positive customer reviews. Pay attention to fees, including application fees, annual fees, and closing costs. Some lenders offer fee waivers or discounts, which can save you money in the long run.

As of May 7, 2025, the average HELOC interest rate is 7.95%. However, rates can vary significantly between lenders, so it's important to shop around.

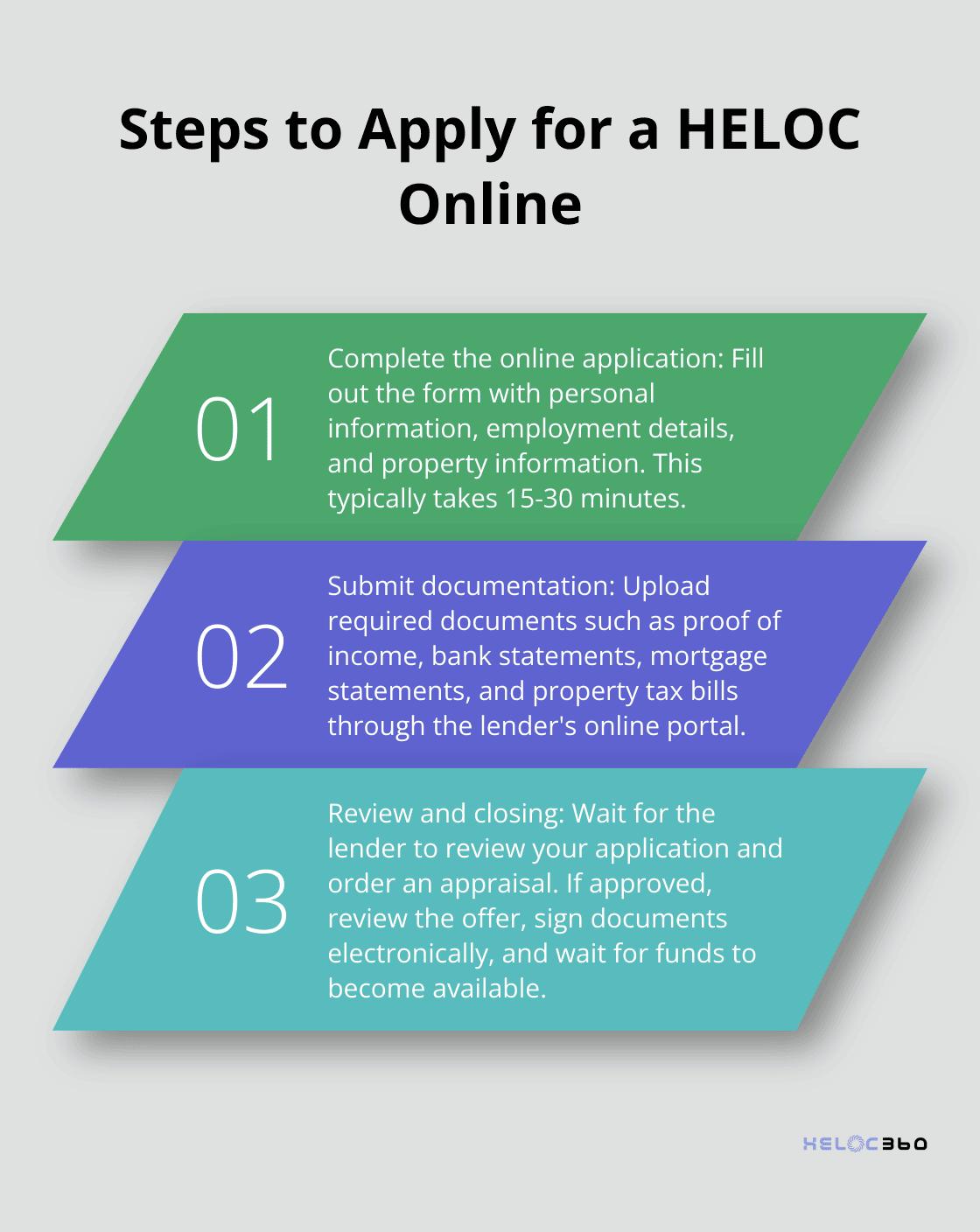

Complete the Online Application

After you select a lender, fill out the online application form. This process typically takes about 15–30 minutes. You'll need to provide personal information, employment details, and property information. Be prepared to answer questions about your income, existing debts, and the purpose of your HELOC.

Many lenders offer user-friendly interfaces that guide you through each step of the application. Some even provide real-time assistance through chat features if you have questions along the way.

Submit Documentation

After you complete the application, submit supporting documents. Most lenders allow you to upload these documents directly through their online portal. Common required documents include:

- Proof of income (W-2 forms, tax returns, or pay stubs)

- Bank statements

- Mortgage statements

- Property tax bills

- Homeowners insurance policy

Pro tip: Create a digital folder with all these documents before you start your application. This organization will speed up the process and reduce the chance of delays due to missing information.

The Review Process

Once you submit your application and documents, the lender will review your information. This process typically takes 2–4 weeks, though some online lenders may provide faster turnaround times.

During this period, the lender will likely order an appraisal of your property. Some lenders use automated valuation models for quicker results, while others may require an in-person appraisal. AVMs provide faster, cheaper valuations compared to traditional appraisals.

Stay responsive during this time. Lenders may reach out for additional information or clarification. Quick responses on your part can help expedite the process.

Closing the Deal

If the lender approves your application, you'll receive a formal offer detailing the terms of your HELOC. Review this carefully, paying close attention to the interest rate, credit limit, draw period, and repayment terms.

Many lenders now offer electronic closing options, allowing you to sign documents online. This convenience can save you time and eliminate the need for an in-person closing meeting.

After closing, your HELOC funds will become available, typically within a few business days. Some lenders provide immediate access through online banking platforms or dedicated HELOC credit cards.

Final Thoughts

Online HELOC applications have transformed how homeowners access their home equity. The process is now more streamlined and accessible, allowing you to submit information and documents from home. Thorough preparation and choosing the right lender are key to a smooth HELOC application. HELOC360 simplifies this process, offering expert guidance and connecting you with suitable lenders.

A HELOC provides a flexible line of credit based on your home's equity. It's important to use this financial tool wisely and create a plan for the funds. Your home secures this credit line, so responsible borrowing is essential. The ability to apply for a HELOC online has made it easier to leverage your home's value for your financial goals.

With proper preparation and guidance, you can navigate this process confidently. Take the first step towards financial empowerment today and explore how a HELOC can help achieve your aspirations. The option to apply for a HELOC online opens new doors for homeowners seeking to make the most of their property's value.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.