Can You Really Get a HELOC on Your Rental Property?

Table of Contents

At HELOC360, we often hear from real estate investors wondering if they can secure a HELOC on their rental properties. The answer is yes, but it's not as straightforward as getting one for your primary residence.

Rental HELOCs come with unique challenges and opportunities that savvy investors should understand. In this post, we'll explore the ins and outs of using a HELOC to tap into your investment property's equity.

What Is a HELOC for Rental Properties?

Understanding Rental Property HELOCs

A Home Equity Line of Credit (HELOC) for rental properties is a loan taken out against a piece of real estate that generates income or a profit. It functions similarly to a credit card, providing a revolving line of credit that investors can draw from as needed.

Key Differences from Primary Residence HELOCs

HELOCs for rental properties operate differently than those for primary residences. Lenders consider investment properties riskier assets, which results in:

- Stricter qualification requirements

- Potentially higher interest rates

- Lower loan-to-value (LTV) ratio caps

For example, while a primary home HELOC might require a credit score of 650–680, rental property HELOCs often demand scores of 700–720 or higher. Additionally, LTV caps for rental properties typically range from 75–80%, compared to 85–90% for primary residences.

Strategic Uses for Investors

Real estate investors use HELOCs on rental properties for various purposes:

- Property Improvements: Investors can fund upgrades to increase property value and potential rent.

- Portfolio Expansion: HELOC funds can serve as down payments for additional properties.

- Emergency Expenses: Quick access to funds helps manage unexpected costs (repairs, vacancies).

Financial Flexibility and Responsibility

The flexibility of a HELOC is one of its most attractive features. During the draw period (typically 5–10 years), investors can access funds as needed. This flexibility proves particularly useful for managing the unpredictable expenses associated with rental property ownership.

However, this flexibility comes with responsibility. Variable interest rates can cause payment fluctuations, potentially impacting cash flow. A solid financial plan is essential before pursuing a HELOC on a rental property.

Navigating Lender Requirements

To qualify for a rental property HELOC, investors must meet specific lender criteria:

- Higher Credit Scores: Most lenders require scores of 700–720 or above.

- Lower Debt-to-Income Ratios: Lenders often look for ratios with a maximum of 50%.

- Substantial Equity: You'll need more equity in your rental property compared to a primary residence HELOC.

As we move forward, we'll explore the specific qualifications needed to secure a HELOC on your rental property and how these requirements can impact your investment strategy.

How Strict Are Rental Property HELOC Requirements?

Credit Score Expectations

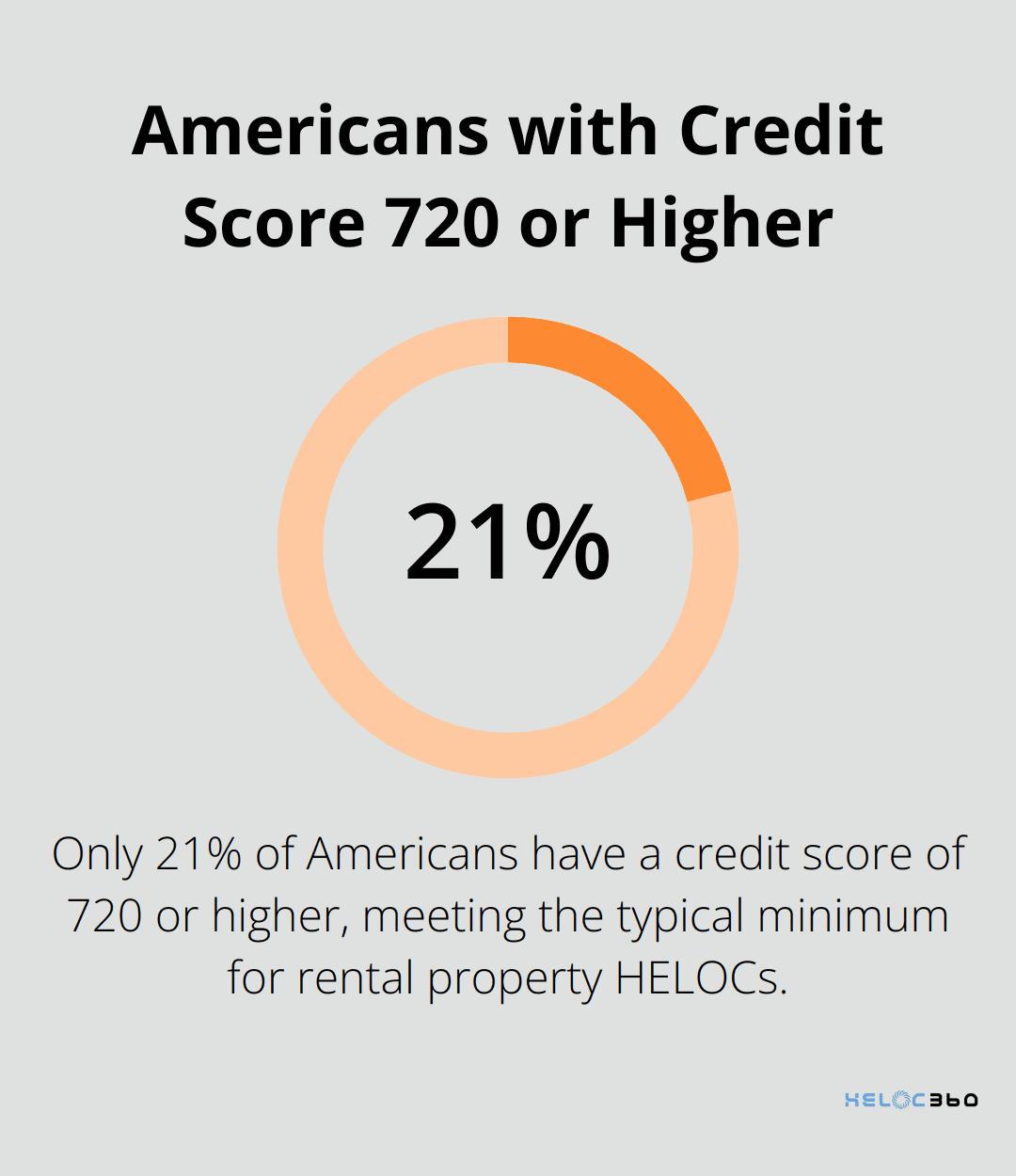

Most lenders require a minimum credit score of 720 for rental property HELOCs. This threshold surpasses the 650–680 range typically needed for primary residences. Some lenders even look for scores of 740 or above. A 2021 Experian study revealed that only about 21% of Americans have a credit score of 720 or higher, which underscores the exclusivity of this requirement.

Debt-to-Income Ratio Matters

Your debt-to-income (DTI) ratio plays a critical role when you apply for a rental property HELOC. To calculate your estimated DTI ratio, simply enter your current income and payments. Lenders generally cap DTI at 50%, including the potential HELOC payment. Some may prefer a lower DTI, around 43–45%. To calculate your DTI, add up all monthly debt payments and divide by your gross monthly income. Include your rental income in this calculation, as it can significantly improve your DTI.

Equity Requirements

Equity takes center stage in HELOC approval for rental properties. Most lenders require at least 20–25% equity remaining after the HELOC. This translates to a maximum combined loan-to-value (CLTV) ratio of 75–80%. For example, if your rental property is worth $300,000, and you have a $200,000 mortgage balance, you'd potentially qualify for a HELOC of up to $40,000 (assuming an 80% CLTV limit).

Cash Reserves and Property Performance

Many lenders require substantial cash reserves, often six months' worth of HELOC payments. This requirement ensures you can cover payments even if your rental income temporarily decreases. Additionally, lenders will scrutinize your property's performance. They typically want to see a history of consistent rental income and occupancy rates above 75%.

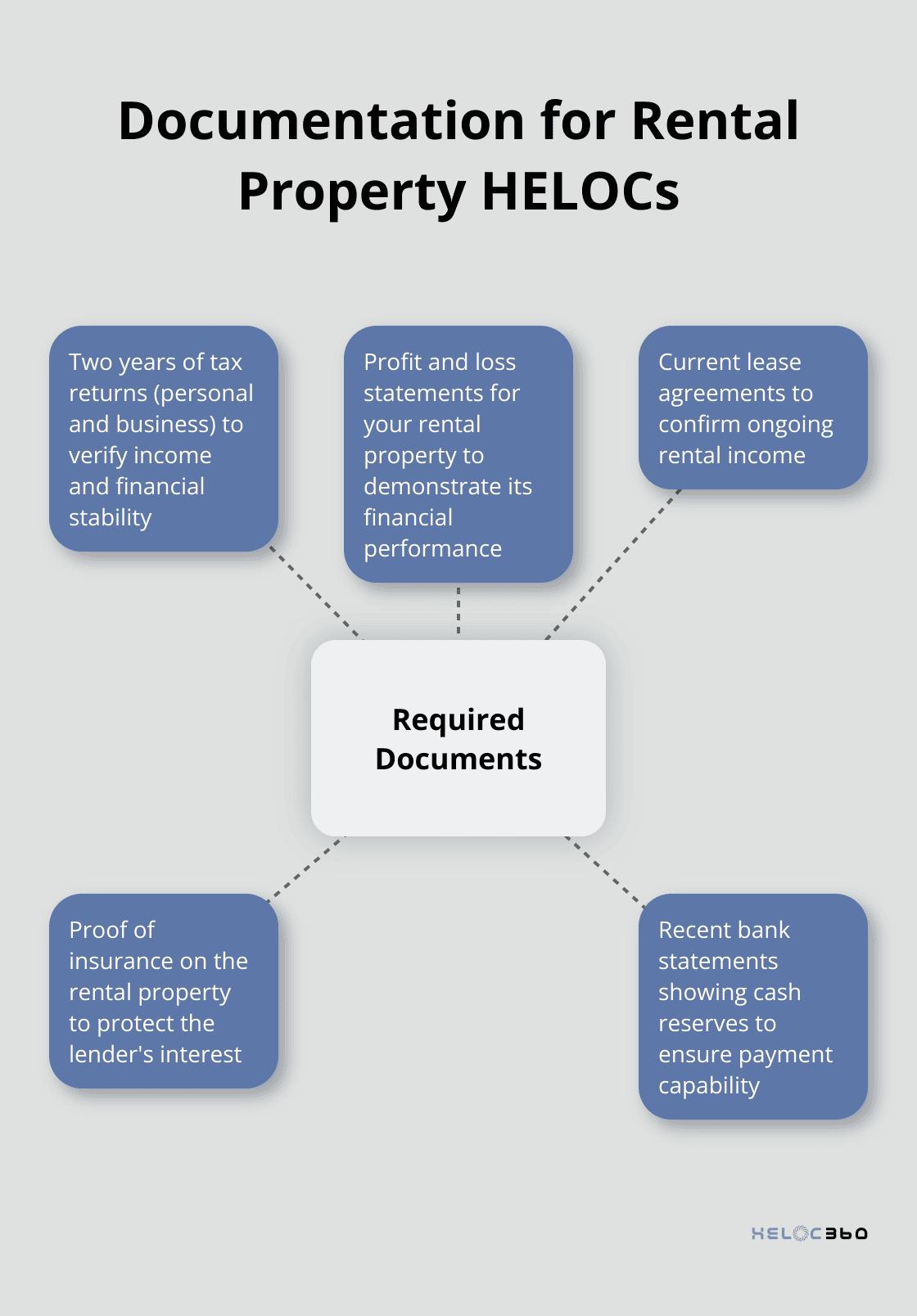

Documentation Demands

Prepare for extensive documentation requests. Lenders will likely ask for:

- Two years of tax returns (personal and business)

- Profit and loss statements for your rental property

- Current lease agreements

- Proof of insurance on the rental property

- Recent bank statements showing cash reserves

Lender Landscape

Finding lenders that offer HELOCs on rental properties can prove challenging. Many major banks have tightened their lending criteria or stopped offering these products altogether. However, local credit unions and specialized investment property lenders often have more flexible options.

Interest Rates and Terms

Expect higher interest rates on rental property HELOCs compared to primary residence options. Rates typically range 0.5% to 1% higher. Additionally, some lenders may offer shorter draw periods (e.g., 5 years instead of 10) for investment property HELOCs.

These stringent requirements might seem daunting, but understanding them is essential for investors who want to leverage their rental property equity. As you weigh your options, consider how meeting these criteria not only helps you secure financing but also ensures you're in a strong financial position to manage the additional debt responsibly. Now, let's explore the advantages and disadvantages of obtaining a HELOC on your rental property.

Weighing the Pros and Cons of Rental Property HELOCs

Flexibility: A Double-Edged Sword

HELOCs offer unparalleled flexibility. You can draw funds as needed during the draw period (typically 5–10 years). This proves useful for unexpected repairs or time-sensitive investment opportunities. However, this flexibility can lead to overspending if not managed properly. Some investors use their HELOC as a piggy bank, drawing funds for non-essential expenses and putting their property at risk.

Interest Rates: Lower But Variable

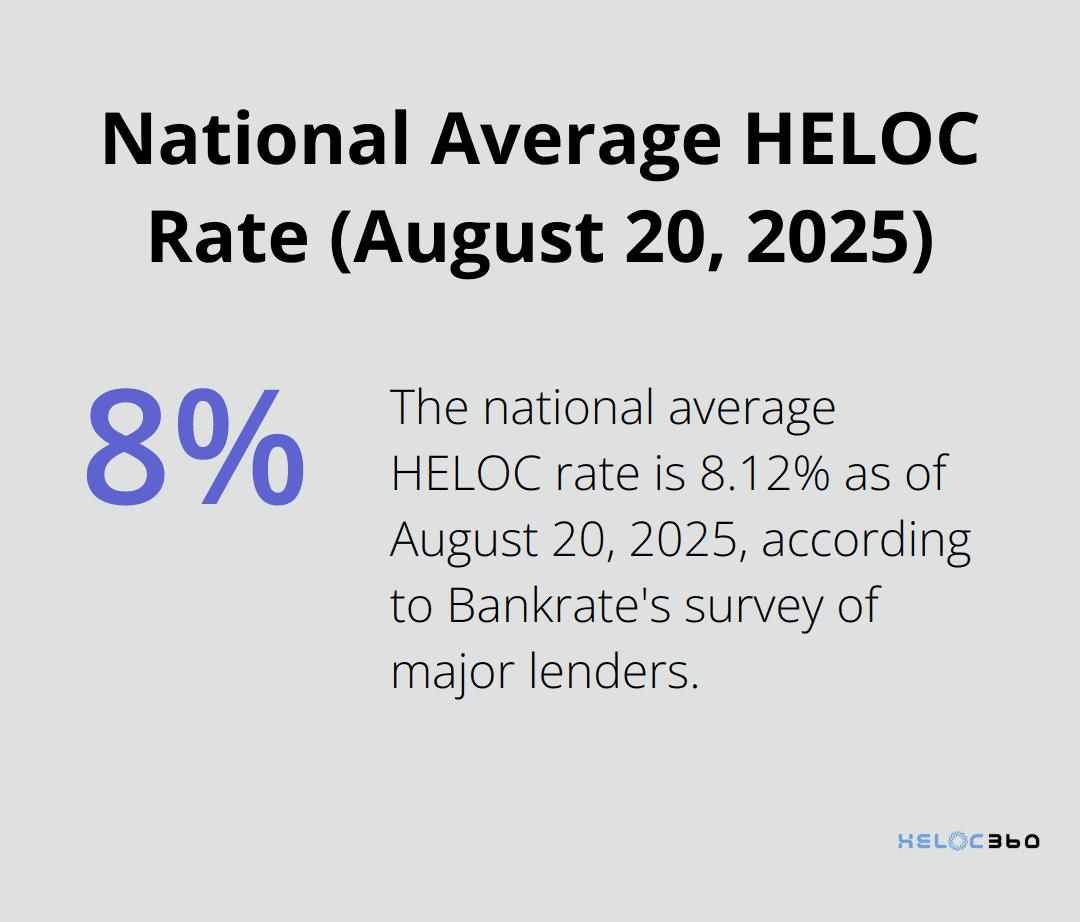

HELOCs generally offer lower interest rates compared to credit cards or personal loans. As of August 20, 2025, the national average HELOC rate is 8.12%, according to Bankrate's latest survey of the nation's largest home equity lenders. This difference can translate to significant savings over time. However, HELOC rates are typically variable, which means your payments can fluctuate with market conditions. In a rising rate environment, your costs could increase substantially. Factor in potential rate hikes when budgeting for your HELOC payments.

Tax Implications: Potential Benefits

The interest paid on a HELOC used for property improvements may be tax-deductible, potentially lowering your overall tax burden. However, tax laws are complex and subject to change. The Tax Cuts and Jobs Act of 2017 limited HELOC interest deductions. As of July 18, 2025, joint filers who took out their home equity loan after Dec. 15, 2017, can deduct interest on up to $750,000 worth of qualified loans. Always consult with a tax professional to understand the current implications for your specific situation.

Impact on Cash Flow: A Balancing Act

A HELOC can provide a safety net for your rental property's cash flow, allowing you to cover expenses during vacancy periods or make improvements that could increase rental income. For instance, using a HELOC to fund a kitchen renovation could potentially increase your monthly rent by 10–15%. However, consider how the additional debt service will affect your overall cash flow. Try to maintain a debt service coverage ratio of at least 1.25. This ratio tells you how many times the property's rental income covers its operating expenses and debt obligations. A ratio above 1 indicates positive cash flow.

Risk of Foreclosure: A Serious Consideration

The most significant risk of a HELOC is the potential for foreclosure if you default on payments. Your rental property serves as collateral for the loan, meaning you could lose the asset if you can't keep up with payments. This risk becomes particularly acute if you use the HELOC for purposes unrelated to the property itself. Always have a solid repayment plan in place before taking on this additional debt.

Final Thoughts

Rental HELOCs offer real estate investors a unique opportunity to access their property's equity. These financial tools provide flexibility, potentially lower interest rates, and tax benefits for property improvements or portfolio expansion. However, variable interest rates, strict qualification requirements, and foreclosure risks demand careful consideration.

Investors should assess their financial situation, long-term strategy, and risk tolerance before pursuing a rental HELOC. The landscape of rental HELOCs varies significantly among lenders, with more stringent requirements for investment properties compared to primary residences. Shopping around and comparing offers from multiple lenders will help find the best terms for your situation.

For those who want to explore their options and gain a deeper understanding of HELOCs, HELOC360 offers comprehensive solutions and expert guidance. This platform helps property owners make informed decisions about leveraging their home equity (for investment properties or primary residences). Consulting with financial advisors and HELOC experts will provide personalized guidance based on your specific financial goals and circumstances.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.