HELOC Interest Rate Predictions for 2025 and Beyond

Table of Contents

At HELOC360, we're constantly monitoring the financial landscape to provide you with the most up-to-date information on home equity lines of credit.

As we approach 2025, many homeowners are wondering about the future of HELOC interest rates.

In this post, we'll explore current trends, economic indicators, and expert HELOC predictions to give you a clear picture of what to expect in the coming years.

What's Happening with HELOC Rates?

The Current HELOC Landscape

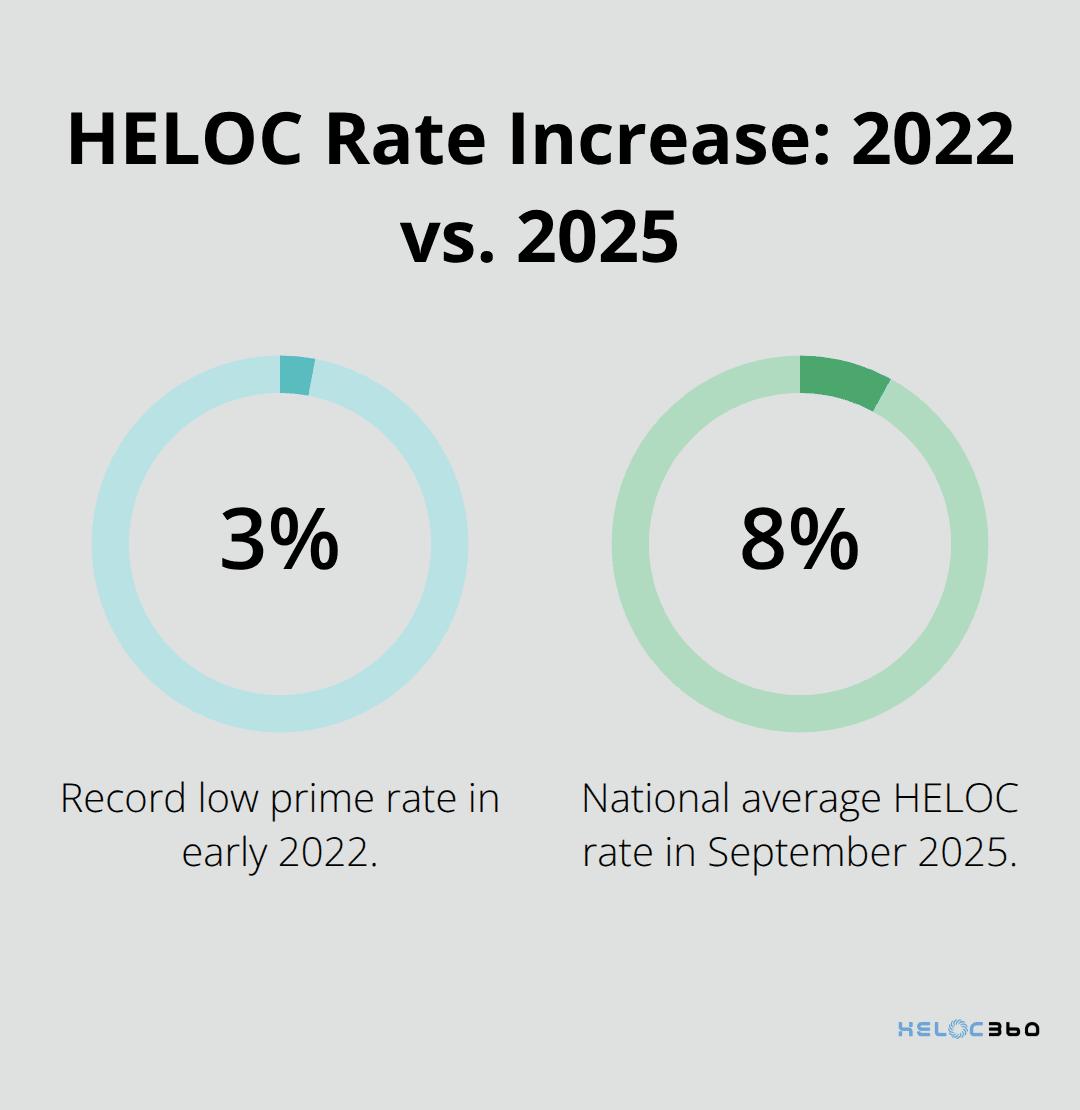

HELOC interest rates have taken a wild ride recently. As of September 2025, the national average HELOC rate sits at 8.90% (according to Bankrate's survey of major lenders). This marks a substantial increase from the record lows of early 2022, when the prime rate was a mere 3.25%.

The Federal Reserve's Influence

The Federal Reserve's rate decisions have significantly impacted HELOC rates. As of August 2025, U.S. Federal Reserve officials expect to cut interest rates two times in 2024, which could alleviate significant upward pressure on rates. This trend will likely continue, with the CME FedWatch Tool tracking the probabilities of changes to the Fed rate, as implied by 30-Day Fed Funds futures prices.

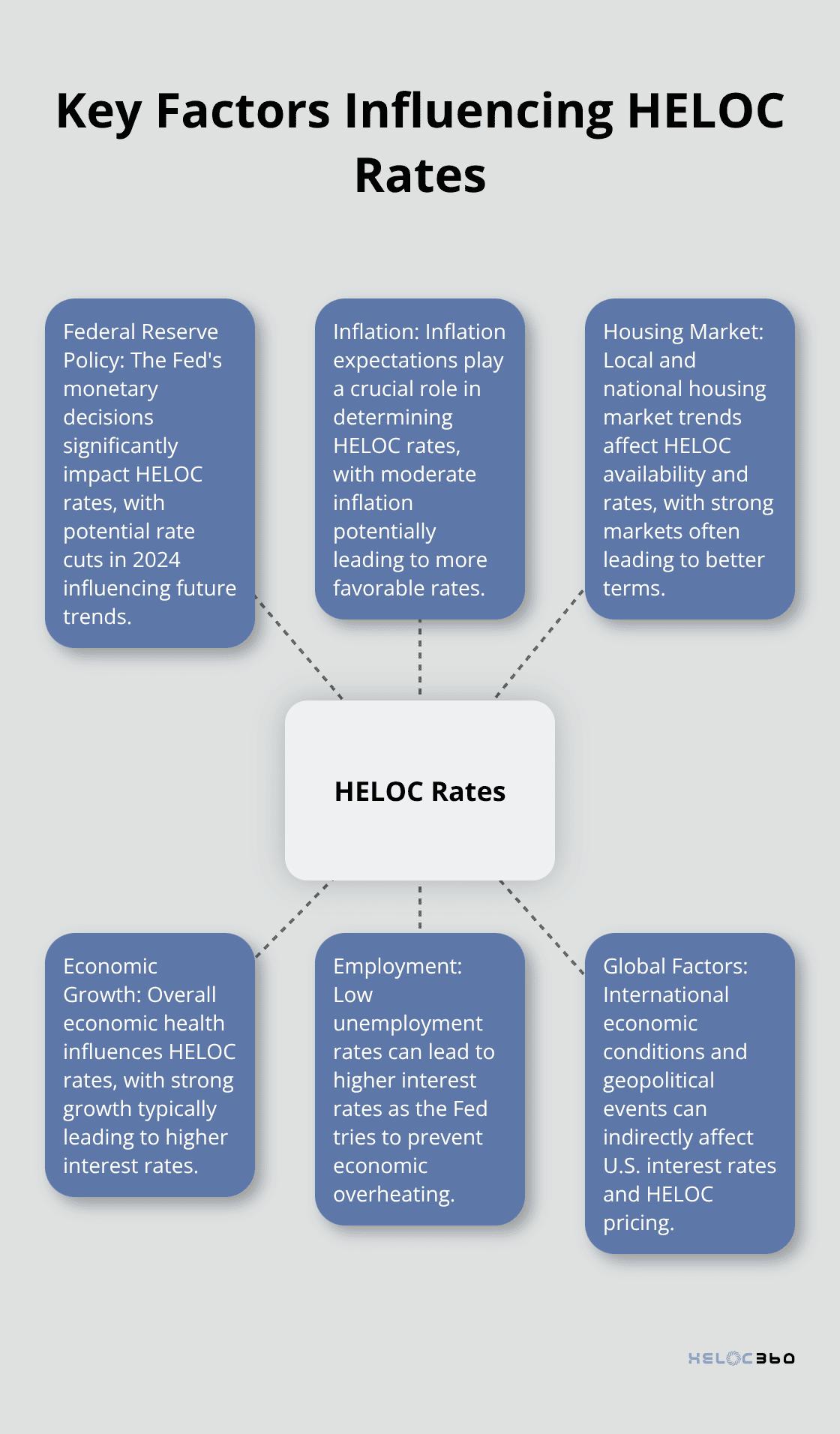

Key Factors Shaping HELOC Rates

Several elements influence current HELOC rates:

- Credit Score: Borrowers with excellent credit scores (typically above 700) secure the most competitive rates.

- Loan-to-Value Ratio: A lower combined loan-to-value ratio often leads to better terms.

- Economic Conditions: Inflation rates and overall economic health play a pivotal role in determining HELOC rates.

HELOCs vs. Alternative Loan Products

When compared to other loan options, HELOCs hold their ground. The average fixed mortgage rate hovers around 7%, making HELOCs an attractive alternative to cash-out refinancing for many homeowners. Personal loans, which often carry higher interest rates, appeal less to those with significant home equity.

Self-employed individuals find HELOCs particularly advantageous. The use of home equity as collateral often makes these lines of credit easier to obtain than unsecured personal loans, even without extensive income documentation.

The Future of the HELOC Market

The HELOC market stands poised for potential growth. A key factor driving this trend is the "rate lock" effect, with 77% of homeowners locked into 6% or lower mortgage rates. This suggests a dynamic future for home equity lending, with opportunities for both lenders and borrowers.

As we move forward, understanding these market dynamics becomes essential for anyone considering a HELOC. The next section will explore the economic indicators that will shape HELOC rates in the coming years, providing you with valuable insights for your financial planning.

What Will Shape HELOC Rates in the Coming Years?

Federal Reserve's Monetary Policy

The Federal Reserve's actions significantly influence HELOC rates. As of September 2025, the Fed has indicated a potential shift towards a more accommodative monetary policy. This shift could result in lower HELOC rates in the near future.

Most forecasts suggest rates will stay in the 6% range well into 2026—perhaps even remaining in mid-6% territory. This outlook marks a change from the rate hikes observed in recent years.

However, the Fed's decisions depend on economic data. Unexpected economic developments could alter this outlook. We recommend that you monitor Fed announcements and economic reports closely to anticipate potential rate changes.

Inflation's Impact on HELOC Rates

Inflation expectations significantly determine HELOC rates. As of late 2025, inflation has shown signs of moderation, though exact figures are uncertain.

If inflation moderates in the coming months, the Fed may consider cuts later in 2025 — but that's far from guaranteed.

For HELOC borrowers, this situation necessitates vigilance about inflation trends. Higher-than-expected inflation could increase borrowing costs, while lower inflation might result in more favorable rates.

Housing Market Trends and HELOC Rates

The housing market's state significantly affects HELOC rates and availability. As of 2025, the housing market presents a mixed picture.

Home prices have shown varied trends after the rapid growth observed in the early 2020s. Recent data shows that month-over-month pending sales declined in the Northeast and Midwest, held essentially flat in the South, and rose in the West in July 2025. These regional variations can affect your ability to secure a favorable HELOC rate.

We advise potential HELOC borrowers to monitor their local housing market closely. A strong local market can lead to better HELOC terms, as lenders feel more confident about the underlying collateral.

Economic Growth and Employment

The overall health of the economy plays a significant role in shaping HELOC rates. Strong economic growth and low unemployment rates typically lead to higher interest rates, as the Fed tries to prevent the economy from overheating.

As of late 2025, the U.S. economy has shown resilience, though specific figures may vary. These conditions suggest a stable economic environment, which could support moderate HELOC rates.

However, economic conditions can change rapidly. Any significant shifts in GDP growth or employment figures could prompt the Fed to adjust its monetary policy, directly impacting HELOC rates.

Global Economic Factors

While domestic factors primarily drive HELOC rates, global economic conditions also play a role. International trade tensions, geopolitical events, or major economic shifts in other countries can indirectly affect U.S. interest rates.

For example, a global economic slowdown could lead to lower demand for credit, potentially pushing HELOC rates down. Conversely, strong global growth might increase inflationary pressures, leading to higher rates.

As we look towards 2026 and beyond, these economic indicators will continue to shape the HELOC rate environment. Understanding these factors can help you make informed decisions about when to apply for a HELOC and how to manage your existing line of credit. In the next section, we'll explore specific predictions for HELOC interest rates in 2025 and beyond, based on current trends and expert analyses.

What Will HELOC Rates Look Like in 2025?

HELOC rates are set to undergo interesting shifts as we approach 2025 and beyond. We've analyzed current trends and expert forecasts to provide a clear picture of what to expect.

Short-Term Outlook: 2023–2024

HELOC rates will likely remain relatively stable in the immediate future. The Federal Reserve's recent pause in rate hikes suggests that HELOC rates might adjust within a month or two after any Fed rate change.

The Mortgage Bankers Association expects the average HELOC rate to drop to around 8.5% by the end of 2024. This modest decrease from current levels could offer some relief to borrowers.

Long-Term Projections: 2025 and Beyond

The outlook becomes more optimistic for HELOC borrowers as we look further ahead. Most economic forecasts point to a gradual decline in interest rates starting in 2025.

The Federal Reserve Bank of Cleveland's inflation forecasting model predicts inflation for the third quarter of 2025. This moderation in inflation could lead to lower HELOC rates.

We anticipate HELOC rates to potentially fall to the 7–8% range by late 2025 (assuming economic conditions remain stable). However, these projections may change based on various economic factors.

Factors That Could Alter Rate Trajectories

While our baseline forecast suggests a gradual decline in HELOC rates, several scenarios could change this trajectory:

- Economic Surprises: An unexpected economic boom could lead to higher inflation, prompting the Fed to maintain higher rates. A recession might accelerate rate cuts.

- Housing Market Shifts: A significant cooling in the housing market could make lenders more cautious, potentially leading to higher HELOC rates despite overall rate trends.

- Global Events: Major international economic or geopolitical events could impact U.S. monetary policy and, consequently, HELOC rates.

- Policy Changes: New financial regulations or changes in tax policies related to home equity borrowing could influence HELOC rates and terms.

Implications for Homeowners

These projections suggest that waiting until 2025 might result in more favorable rates for homeowners considering a HELOC. However, individual circumstances vary, and current rates might still be advantageous for many borrowers, especially when compared to other forms of credit.

To navigate these changing conditions, it's important to stay informed and work with experienced professionals. Tools and resources are available to help you make the best decision based on your unique financial situation and goals.

Final Thoughts

HELOC interest rates will likely decline gradually towards 2025. Our analysis predicts rates could fall to the 7–8% range by late 2025, assuming stable economic conditions. This trend offers potential opportunities for homeowners who want to tap into their home equity.

The future rate environment requires a strategic approach. You should monitor economic indicators, Federal Reserve decisions, and housing market trends. These factors will shape HELOC rates in the coming years (HELOC predictions suggest a downward trend).

At HELOC360, we help homeowners unlock the full potential of their home equity. Our platform simplifies the process and offers expert guidance. We connect you with lenders that fit your specific needs.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.