HELOC Payment Calculator How to Estimate Your Monthly Costs

Table of Contents

Curious about your potential HELOC payments? You're not alone. Many homeowners find themselves puzzled when it comes to estimating the costs of a Home Equity Line of Credit.

At HELOC360, we understand the importance of financial clarity. That's why we've created this guide to help you navigate the world of HELOC payment calculators and estimate your monthly expenses with confidence.

How Do HELOC Payments Work?

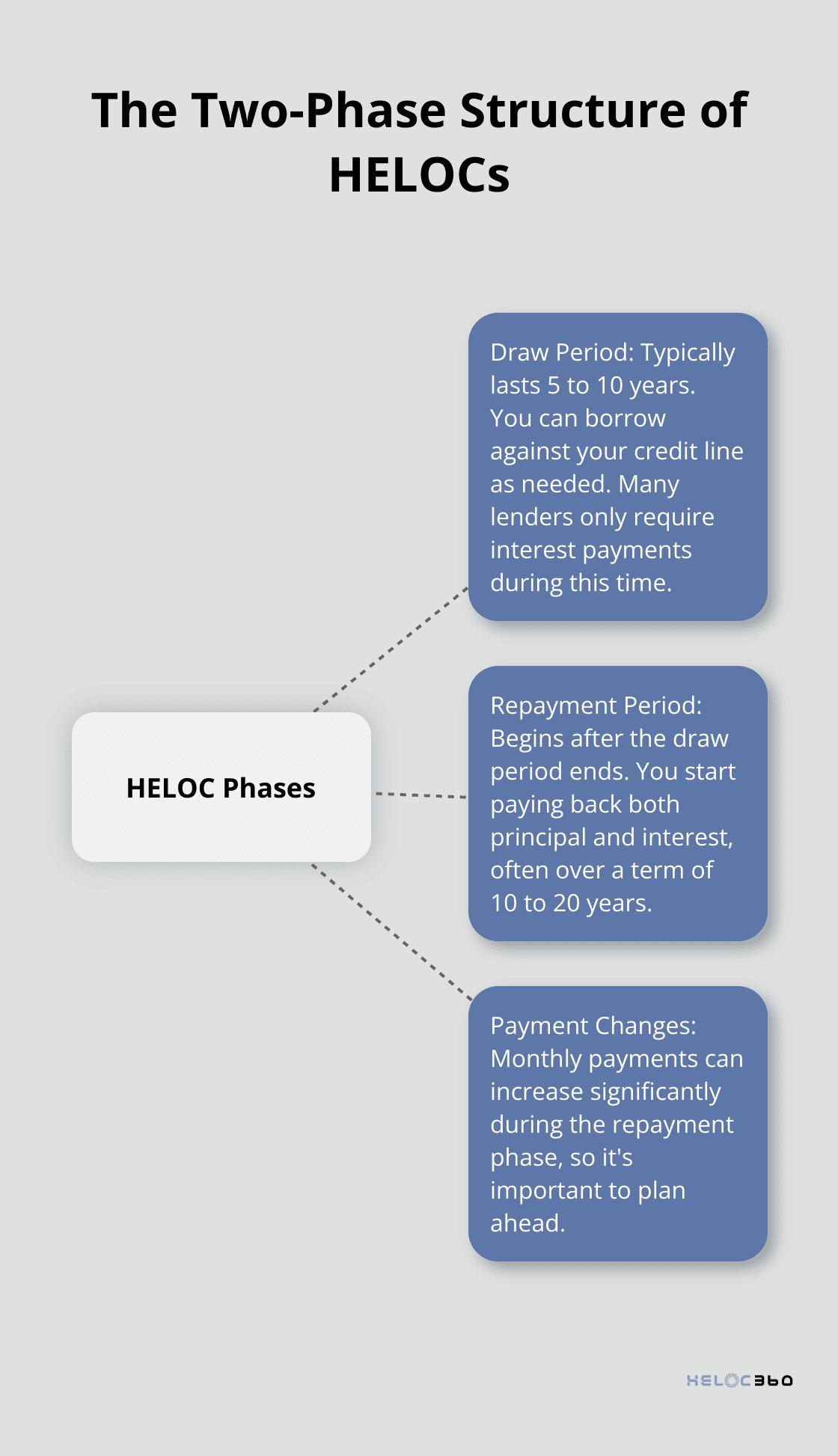

The Two-Phase Structure of HELOCs

HELOCs typically have two phases: the draw period and the repayment period. The draw period typically lasts 5 to 10 years, during which you can borrow against your credit line as needed. Many lenders only require interest payments during this time, resulting in lower monthly costs. However, making interest-only payments means you don't reduce your principal balance.

After the draw period ends, you enter the repayment phase. This is when you start paying back both principal and interest, often over a term of 10 to 20 years. Your monthly payments can increase significantly during this phase, so it's important to plan ahead.

Factors Influencing Your HELOC Payments

Several key factors affect your HELOC payments:

- Interest Rate: Most HELOCs have variable interest rates tied to the prime rate. As of August 6, 2025, the average HELOC rate is 8.13% according to Bankrate's latest survey of the nation's largest home equity lenders. However, this can fluctuate based on market conditions and your creditworthiness.

- Amount Borrowed: Your payment depends on how much you've actually drawn from your credit line, not your total available credit.

- Payment Structure: Some lenders offer options like interest-only payments during the draw period or fixed-rate conversion options for portions of your balance.

- Credit Score: A higher credit score can often secure you a lower interest rate, directly impacting your monthly payments.

The Impact of Variable Rates

It's important to understand that HELOC rates can change frequently. For example, if the Federal Reserve cuts interest rates, your HELOC rate will likely decrease, but it could take one or two statement cycles to reflect in your payments. This means your monthly payments could go down, potentially providing some financial relief.

To illustrate, let's consider a $50,000 HELOC balance with a 10-year repayment term. If your rate decreases from 8% to 6%, your monthly payment could drop from about $607 to $555 - a difference of $52 per month (or $6,240 over the life of the loan).

Planning for HELOC Payments

To effectively plan for your HELOC payments:

- Calculate potential payment scenarios using different interest rates.

- Consider making principal payments during the draw period to reduce your overall debt.

- Set up automatic payments to ensure you never miss a due date.

- Monitor interest rate trends to anticipate potential changes in your payments.

Understanding these aspects of HELOC payments is essential for effective financial planning. As we move forward, let's explore the key components of a HELOC payment calculator, which will help you estimate your monthly costs more accurately.

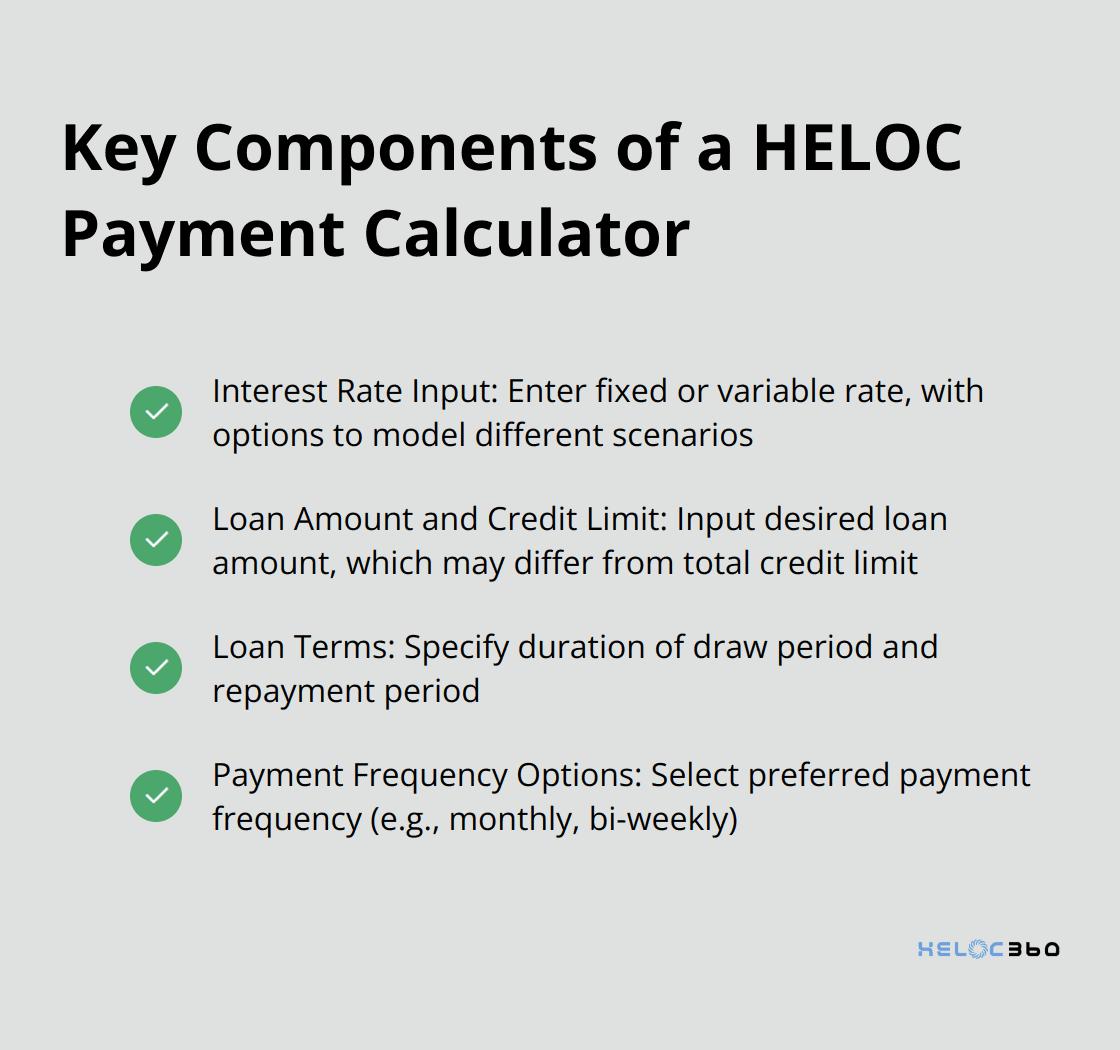

What's Inside a HELOC Payment Calculator?

A HELOC payment calculator serves as a powerful tool for estimating your monthly costs. Let's break down the key components you'll typically find in these calculators.

Interest Rate Input

The interest rate forms the cornerstone of your HELOC payment calculation. Most calculators allow you to input either a fixed or variable rate. As of August 2025, the average HELOC rate remains unchanged. Your actual rate may differ based on factors like credit score and loan-to-value ratio. Some calculators even let you model different rate scenarios, which proves invaluable given the variable nature of most HELOCs.

Loan Amount and Credit Limit

You'll need to input your desired loan amount, which is the amount you plan to borrow. This might differ from your total credit limit. For instance, if you have a $100,000 credit limit but only plan to use $50,000, you'd enter $50,000 as your loan amount. This distinction matters because your payments depend on the amount borrowed, not your total available credit.

Loan Terms

HELOC calculators typically ask for the duration of your draw period and repayment period. Standard terms often include a 10-year draw period where you can withdraw funds up to your limit. The repayment period is when you can no longer borrow from your HELOC. Some lenders offer 5-year draw periods or 15-year repayment terms. The calculator uses these inputs to determine how long you'll make interest-only payments versus principal-and-interest payments.

Payment Frequency Options

While monthly payments prevail as the most common, some HELOCs offer bi-weekly or even weekly payment options. A good calculator will allow you to select your preferred payment frequency. This feature can particularly help with budgeting purposes or for those who want to pay down their HELOC faster.

These components allow you to more accurately estimate your HELOC costs. While calculators provide excellent planning tools, they offer estimates based on the information you input. For the most accurate and personalized HELOC assessment, speaking with a financial advisor or a HELOC specialist can provide additional insights.

Now that we've explored the key components of a HELOC payment calculator, let's move on to how you can effectively use these tools to estimate your monthly costs.

How to Calculate Your HELOC Payments

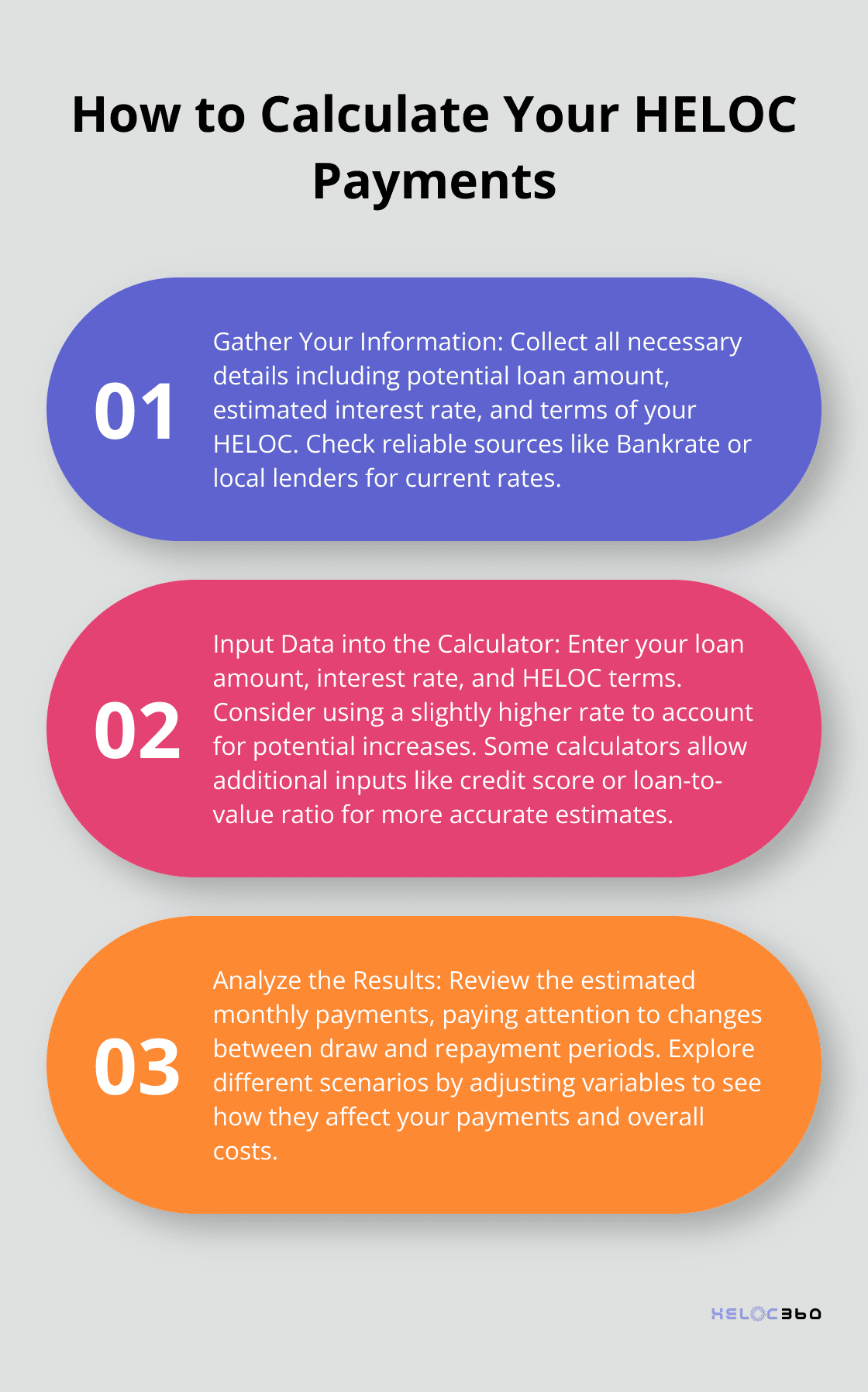

Gather Your Information

Before you start, collect all the necessary details. You'll need your potential loan amount, estimated interest rate, and the terms of your HELOC. If you're uncertain about the current rates, check reliable sources like Bankrate or your local lenders for the most up-to-date information.

Input Data into the Calculator

Start by entering your loan amount (the total amount you plan to borrow, not your credit limit). Next, input the interest rate. HELOCs typically have variable rates, so consider using a slightly higher rate to account for potential increases.

Enter the terms of your HELOC, including the length of your draw period and repayment period. Most calculators will ask for these separately. For example, you might have a 10-year draw period followed by a 20-year repayment period.

Some advanced calculators allow you to input additional details like your credit score or loan-to-value ratio. If available, use these features for a more accurate estimate.

Analyze the Results

Once you've entered all the information, the calculator will provide an estimate of your monthly payments. Pay close attention to how these payments change between the draw period and repayment period. During the draw period, you might only need to make interest payments (which can be significantly lower than the principal-and-interest payments during the repayment period).

Look for a breakdown of your total costs over the life of the loan. This can be eye-opening, showing you the long-term impact of interest rates on your borrowing.

Explore Different Scenarios

Don't stop at your first calculation. Try adjusting different variables to see how they affect your payments. For instance:

- Increase the interest rate by 1-2% to see how a rate hike would impact your monthly costs.

- Change the loan amount to see how borrowing more or less affects your payments.

- Calculate scenarios where you make additional principal payments during the draw period (this can significantly reduce your overall interest costs and make the transition to the repayment period less jarring).

This thorough exploration of scenarios will give you a comprehensive understanding of your potential HELOC costs. This knowledge empowers you to make informed decisions about your home equity borrowing strategy.

While calculators are powerful tools, they provide estimates. For the most accurate and personalized assessment, you should speak with a HELOC specialist or financial advisor. Platforms like HELOC360 can connect you with experts who can provide tailored advice based on your specific financial situation and goals.

Final Thoughts

A HELOC payment calculator provides valuable insights into potential monthly costs. This tool allows you to plan effectively for both draw and repayment periods, empowering you to explore various scenarios and visualize the long-term impact of your borrowing choices. You can make strategic decisions that optimize your home equity usage while maintaining financial stability.

Your unique financial situation may require personalized guidance beyond calculator estimates. HELOC360 simplifies the process, offers expert guidance, and connects you with lenders that fit your specific needs. We provide tailored solutions to help you achieve your financial aspirations, whether you're considering home renovations, debt consolidation, or creating financial flexibility.

Use the insights gained from HELOC payment calculators (coupled with expert advice) to make confident decisions about leveraging your home equity. You can transform your home's value into a gateway for new opportunities and financial growth with the right tools and guidance. HELOC360 stands ready to assist you in unlocking the full potential of your home equity.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.