How to Flip Houses Using a HELOC [2025 Guide]

![How to Flip Houses Using a HELOC [2025 Guide]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2F2a445j5i%2Fproduction%2F6a6d45ab91707fe592dfdeb49936ad561b3f75d6-1024x585.jpg%3Fauto%3Dformat&w=3840&q=75)

Table of Contents

House flipping with a HELOC is becoming increasingly popular among real estate investors in 2025. This strategy allows you to leverage your home equity to fund property purchases and renovations, potentially leading to significant profits.

At HELOC360, we've seen a surge in interest for HELOC flipping, and for good reason. It offers flexibility, competitive rates, and the ability to access funds as needed during the renovation process.

In this guide, we'll walk you through the steps, benefits, and risks of using a HELOC for house flipping, helping you make informed decisions in your real estate investment journey.

What Is a HELOC and How Can It Boost Your House Flipping Success?

Understanding HELOCs for Real Estate Investors

A Home Equity Line of Credit (HELOC) on an investment property is a loan taken out against a piece of real estate that generates income or a potential profit through resale. This financial tool can supercharge your house flipping ventures in 2025 by providing a flexible source of funds for property investments.

How HELOCs Work for House Flipping

When you secure a HELOC, you open a revolving line of credit backed by your home's equity. This means you can draw funds as needed during your house flipping projects, paying interest only on the amount you use. The average HELOC interest rate is 8.90% as of September 3, 2025, according to Bankrate's latest survey of the nation's largest home equity lenders, making it a cost-effective option compared to many other financing methods.

For house flippers, this flexibility proves invaluable. You can access funds for property purchases, renovations, and unexpected expenses without the need for multiple loans. The National Association of Realtors indicates that properties undergoing light renovations can increase in value by 10–15% (highlighting the potential for significant returns when using a HELOC strategically).

Maximizing HELOC Benefits for Your Flipping Business

One of the key advantages of using a HELOC for house flipping is the ability to leverage your existing assets without liquidating them. This means you can keep your savings intact while still pursuing lucrative flipping opportunities. Additionally, the interest on your HELOC may qualify for tax deductions when used for home improvements, potentially reducing your overall costs.

Successful flippers often use their HELOCs to fund multiple projects simultaneously. Through careful management of your credit line, you can create a pipeline of flips, potentially increasing your annual profits. The key lies in maintaining a quick turnaround time on your projects to minimize interest payments and maximize your returns.

Meeting HELOC Eligibility Requirements

To qualify for a HELOC suitable for house flipping, you must meet certain criteria. Most lenders require a credit score of at least 700, though some may accept scores as low as 620. Your debt-to-income ratio should typically fall below 43%, and you'll need to have sufficient equity in your home – usually at least 15–20% of its value.

It's important to shop around for the best HELOC terms. While many traditional banks offer HELOCs, online lenders and credit unions often provide competitive rates and more flexible terms. An increasing number of investors successfully secure HELOCs with favorable terms by demonstrating a solid flipping track record and a well-thought-out business plan.

Mitigating Risks in HELOC-Funded Flips

While HELOCs can serve as an excellent tool for house flipping, they do come with risks. Your home serves as collateral, so it's vital to have a solid exit strategy for each flip. Careful selection of properties, management of your renovation budget, and staying attuned to market trends can help you leverage a HELOC to build a thriving house flipping business in 2025 and beyond.

As you explore the potential of using a HELOC for your house flipping ventures, it's essential to understand the steps involved in this process. Let's move on to the practical aspects of flipping houses using a HELOC, starting with assessing your home equity and borrowing capacity.

How to Flip Houses Using a HELOC: A Step-by-Step Guide

Evaluate Your Financial Position

Start by assessing your home equity and borrowing capacity. Most lenders allow you to borrow up to 85% of your home's value, minus your existing mortgage balance. For example, if your home is worth $500,000 and you owe $300,000, you could potentially access up to $125,000 through a HELOC.

To determine your borrowing capacity, check your credit score and debt-to-income ratio. Try to achieve a credit score above 700 and a debt-to-income ratio below 43% to secure the best HELOC terms. Use online calculators or consult with a financial advisor to get a clear picture of your borrowing potential.

Find the Right Property

Research local real estate markets to identify areas with high potential for appreciation. Look for neighborhoods with improving infrastructure, rising property values, and increasing demand. Online platforms can provide valuable data on market trends and property values.

When evaluating potential flip properties, focus on homes priced below market value that require cosmetic updates rather than major structural repairs.

Plan Your Flip

Create a detailed budget and renovation plan. Break down costs for materials, labor, permits, and unexpected expenses. Industry experts recommend setting aside 15–20% of your budget for unforeseen issues.

Prioritize renovations that offer the highest return on investment. Focus on updates that appeal to the broadest range of buyers in your target market.

Secure Your HELOC

Apply for your HELOC with multiple lenders to compare rates and terms. As of September 2025, the average HELOC interest rate is 8.90%, but rates can vary significantly between lenders. Look for HELOCs with competitive rates, low fees, and flexible draw periods.

When applying, be prepared to provide extensive documentation, including proof of income, tax returns, and property appraisals. Some lenders may require in-person appraisals for investment properties (which can add time to the approval process).

Execute Your Flip

Once your HELOC is approved, move quickly to purchase and renovate the property. Time is money in house flipping, so create a tight timeline for renovations. Work with reliable contractors who can deliver quality work on schedule.

Monitor your budget closely throughout the renovation process. Use your HELOC funds strategically, drawing only what you need to minimize interest charges. Keep detailed records of all expenses for tax purposes and future project planning.

As you progress through these steps, it's important to consider the potential risks and challenges that come with using a HELOC for house flipping. Let's explore these considerations in more detail to ensure you're fully prepared for your investment journey.

Navigating the Risks of HELOC House Flipping

Market Volatility and Property Values

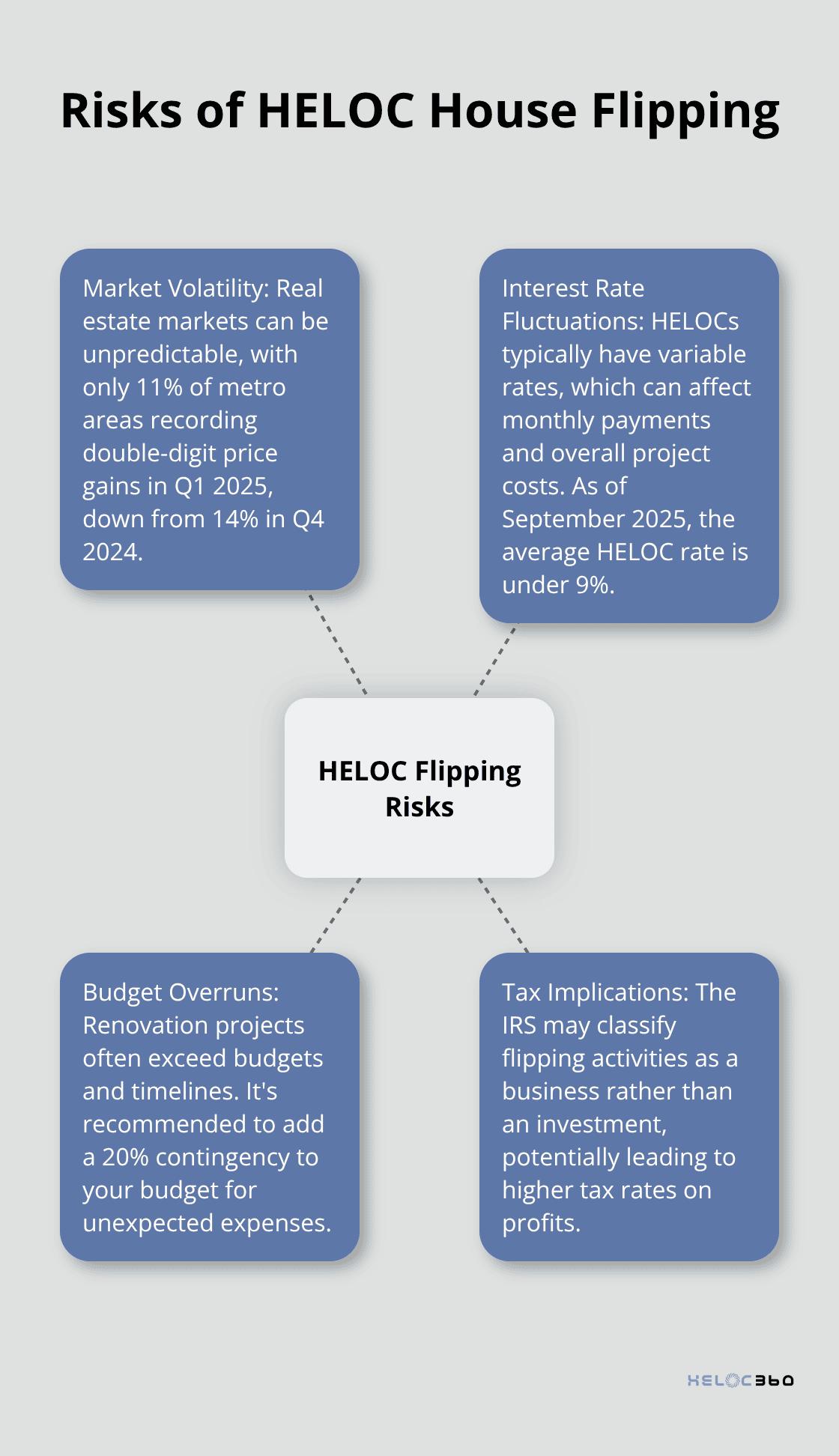

Real estate markets can be unpredictable. In 2025, increased volatility stems from economic shifts and changing buyer preferences. The National Association of Realtors reports that 11% of tracked metro areas recorded double-digit price gains in Q1 2025, down from 14% in Q4 2024. This volatility can impact your profit margins significantly.

To reduce this risk, select properties in stable neighborhoods with consistent demand. Analyze local market trends, including average days on market and price-to-rent ratios. Consider properties that can generate rental income if the market turns unfavorable for selling.

Interest Rate Fluctuations

HELOCs typically come with variable interest rates, which can affect your monthly payments and overall project costs. As of September 2025, the average HELOC rate is well under 9%, putting a HELOC monthly payment under $400 for a $50,000 draw.

To protect yourself from rate hikes, set aside a portion of your budget as a buffer. Some lenders offer rate caps or fixed-rate options for a portion of your HELOC balance (these can create more predictability in your expenses).

Budget and Timeline Overruns

Renovation projects often exceed budgets and timelines. House flipping costs and financing options can vary significantly, impacting overall project success.

To avoid this pitfall, add a 20% contingency to your budget for unexpected expenses. Work with experienced contractors who can provide accurate estimates and adhere to timelines. Use project management tools to track progress and expenses in real-time.

Tax Implications

The tax landscape for house flipping can be complex. The IRS may classify your flipping activities as a business rather than an investment, potentially leading to higher tax rates on your profits.

Consult with a tax professional specializing in real estate investments before you start your flipping journey. Keep meticulous records of all expenses, including HELOC interest payments, as these may be deductible. Consider strategies like 1031 exchanges to defer capital gains taxes if you plan to reinvest your profits into more properties.

Mitigating Risks with Expert Guidance

While these risks are significant, you can overcome them with careful planning and market research. Platforms like HELOC360 provide tools and resources to help you make informed decisions throughout your flipping journey, from initial property selection to final sale.

Final Thoughts

HELOC flipping offers a powerful strategy for real estate investors in 2025. This approach leverages home equity to fund multiple property investments, but it requires careful planning and risk management. Investors must analyze local real estate trends, understand their borrowing capacity, and create detailed budgets for each flip.

Tax considerations play a vital role in flipping strategy. Consultation with tax professionals helps understand investment implications and explore potential deductions. Meticulous record-keeping of all flip-related expenses (including HELOC interest payments) proves essential for successful investors.

HELOC360 provides valuable resources for those interested in HELOC flipping. Our platform connects investors with suitable lenders and offers expert insights to support informed decision-making. We strive to help you unlock your home equity's full potential and achieve your real estate investment goals.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.