No Doc HELOC All You Need to Know

Table of Contents

Are you tired of jumping through hoops to secure a home equity line of credit? A no doc HELOC might be the solution you've been searching for.

At HELOC360, we understand that traditional lending processes don't always work for everyone. That's why we're here to shed light on this alternative financing option.

In this post, we'll explore what no doc HELOCs are, how they differ from conventional HELOCs, and who might benefit most from this unique lending approach.

What Is a No Doc HELOC?

Definition and Basics

A No Doc HELOC (No Documentation Home Equity Line of Credit) allows homeowners to borrow against their home's equity without providing extensive income or employment documentation. This financial product appeals to self-employed individuals, freelancers, and those with non-traditional income sources who often face challenges when qualifying for conventional loans.

How No Doc HELOCs Differ from Traditional HELOCs

Unlike traditional HELOCs, which require pay stubs, tax returns, and other financial documents, No Doc HELOCs primarily focus on the borrower's credit score and home equity. This streamlined approach can speed up the approval process and reduce paperwork significantly.

For instance, a freelance graphic designer with fluctuating income might struggle to prove steady earnings through traditional means. With a No Doc HELOC, they could potentially access their home equity based on their credit history and home value, rather than their income documentation.

Key Requirements for No Doc HELOCs

While No Doc HELOCs offer more flexibility, they still have specific requirements:

- Credit Score: Lenders typically look for higher credit scores (often 660 or above) to offset the increased risk associated with limited income verification. A credit score of 700 and above will help you secure the best rate and terms.

- Equity: Most No Doc HELOC providers require substantial equity in the home (usually 20% or more). Some lenders might even require up to 30-40% equity.

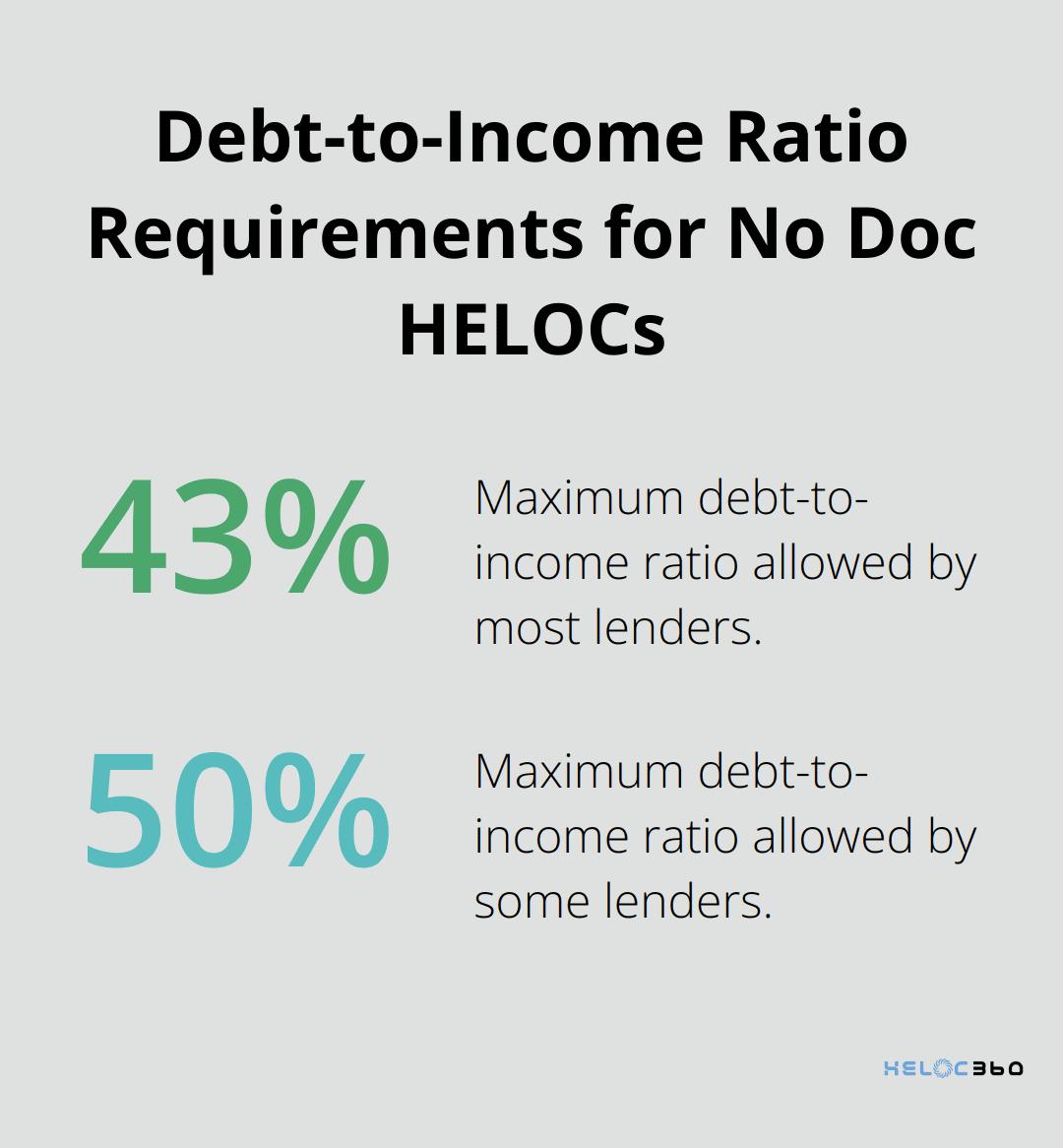

- Debt-to-Income Ratio: Although income documentation isn't required, lenders may still consider your overall debt-to-income ratio based on credit reports. Most lenders limit borrowers to a debt-to-income ratio of 43%, although some allow for a DTI ratio of up to 50%.

Trade-offs to Consider

The convenience of No Doc HELOCs often comes at a cost. Interest rates are typically higher than those for traditional HELOCs, reflecting the increased risk for lenders. Additionally, some lenders may impose stricter borrowing limits or shorter draw periods.

No Doc HELOCs can be a valuable tool for certain borrowers, but they're not suitable for everyone. It's important to weigh the benefits of easier qualification against potentially higher costs and stricter terms.

Now that we've covered the basics of No Doc HELOCs, let's explore their advantages and disadvantages in more detail. This will help you determine if this type of financing aligns with your financial goals and situation.

Are No Doc HELOCs Right for You?

Flexibility for Non-Traditional Borrowers

No Doc HELOCs offer a unique financing option for self-employed individuals, freelancers, and those with irregular income streams. A successful food truck owner, for example, might find it difficult to prove steady income through traditional means. With a No Doc HELOC, they can access their home equity based primarily on their credit score and property value.

This flexibility extends to retirees who live off investments or individuals with significant assets but low taxable income. A No Doc HELOC provides them with a financial cushion without the need to liquidate investments prematurely.

Higher Costs and Stricter Terms

The convenience of No Doc HELOCs comes at a price. HELOCs typically have a variable interest rate (one that changes) versus fixed rates, which are typical in a home equity loan.

Fees also tend to be steeper. Some lenders charge higher origination fees or annual maintenance fees to offset the increased risk. Origination fees of 1-2% of the credit line (compared to 0-1% for traditional HELOCs) are not uncommon.

Potential Risks to Consider

While No Doc HELOCs provide quick access to funds, they carry some risks. The most significant is the potential for overleveraging. Without thorough income verification, some borrowers might take on more debt than they can manage comfortably.

Another consideration is the variable interest rate structure of most HELOCs. If rates rise significantly, your monthly payments could increase substantially. This risk amplifies with No Doc HELOCs due to their higher starting rates.

Lastly, like all HELOCs, these loans use your home as collateral. Defaulting on payments could put your property at risk of foreclosure. This risk underscores the importance of careful financial planning before taking on any home equity debt.

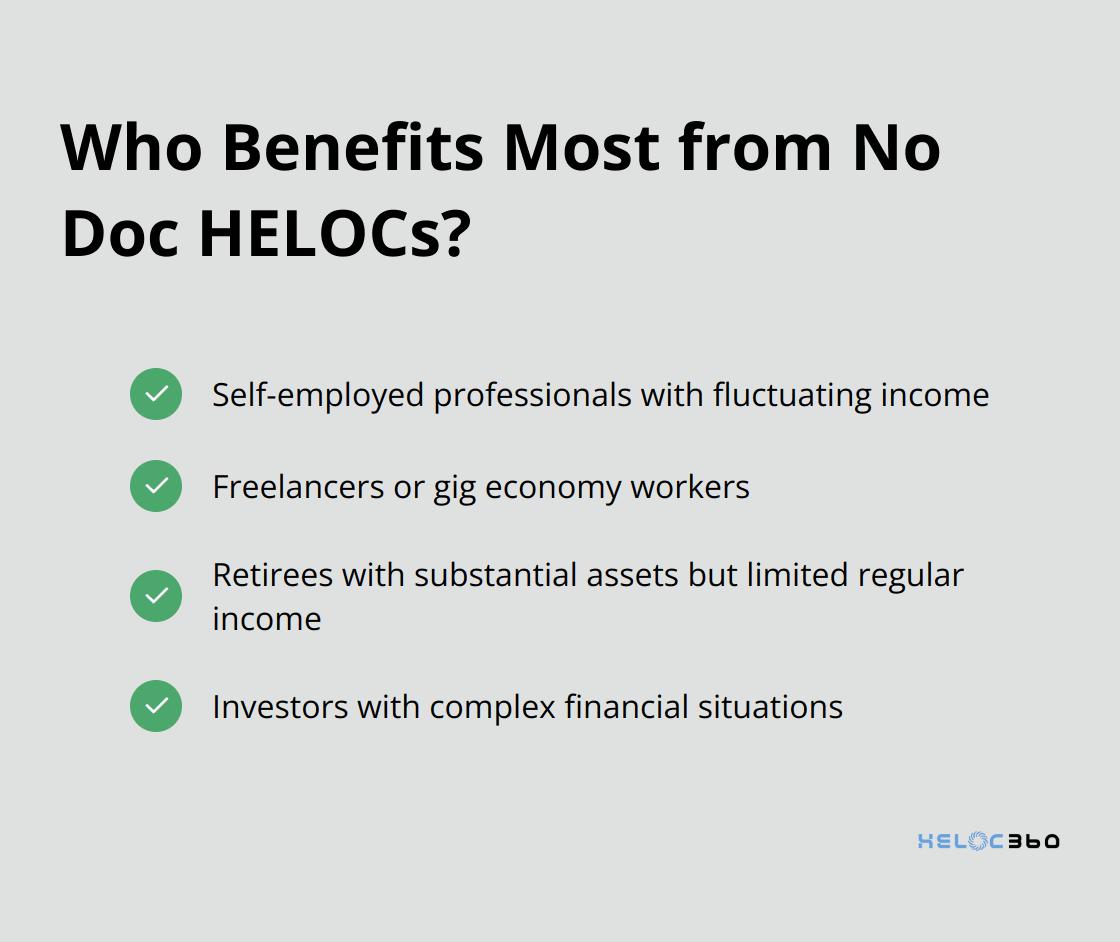

Who Benefits Most from No Doc HELOCs?

No Doc HELOCs work best for:

These borrowers often find traditional lending processes challenging due to their non-standard income structures. No Doc HELOCs offer them a path to leverage their home equity without extensive income documentation.

Alternatives to Consider

Before committing to a No Doc HELOC, explore other options:

- Traditional HELOCs (if you can provide income documentation)

- Cash-out refinancing

- Personal loans

- Home equity loans

Each option has its pros and cons. The best choice depends on your specific financial situation, credit score, and long-term goals.

As you weigh your options, you'll want to understand the qualification process for No Doc HELOCs. Let's explore the typical requirements and how lenders assess borrowers for these unique financial products.

How to Qualify for a No Doc HELOC

Qualifying for a No Doc HELOC differs from traditional lending processes, but it's achievable. Lenders focus on specific factors to assess your creditworthiness and repayment ability. Let's examine the key elements that can influence your No Doc HELOC application.

Credit Score: Your Financial Report Card

Your credit score takes center stage in No Doc HELOC applications. To qualify for a HELOC, you'll need a FICO score of 660 or higher. If your score falls short, focus on paying down existing debts and making timely payments to improve your creditworthiness.

Home Equity: Your Borrowing Power

Equity reigns supreme in the world of No Doc HELOCs. Lenders generally require a minimum of 15% to 20% equity in your home. To calculate your equity, subtract your current mortgage balance from your home's current market value. For example, if your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity (or 37.5%). This level of equity would make you an attractive candidate for many No Doc HELOC lenders.

Alternative Income Verification Methods

While traditional income documentation isn't required, lenders still need assurance of your ability to repay. They might consider:

- Bank statements: Some lenders offer bank statement HELOCs where they don't look at your taxes and just give you the income based on what is actually deposited into your account.

- Asset verification: Substantial savings or investment accounts can serve as a proxy for income.

- Debt-to-income ratio: Lenders may calculate this based on your credit report, aiming for 43% or lower.

Some lenders might also consider non-traditional income sources like rental income from investment properties or consistent freelance earnings.

Lender Specialization

Different lenders have varying requirements and specializations for No Doc HELOCs. Some focus on self-employed borrowers, while others cater to retirees or investors. Research and compare multiple lenders to find the best fit for your unique financial situation.

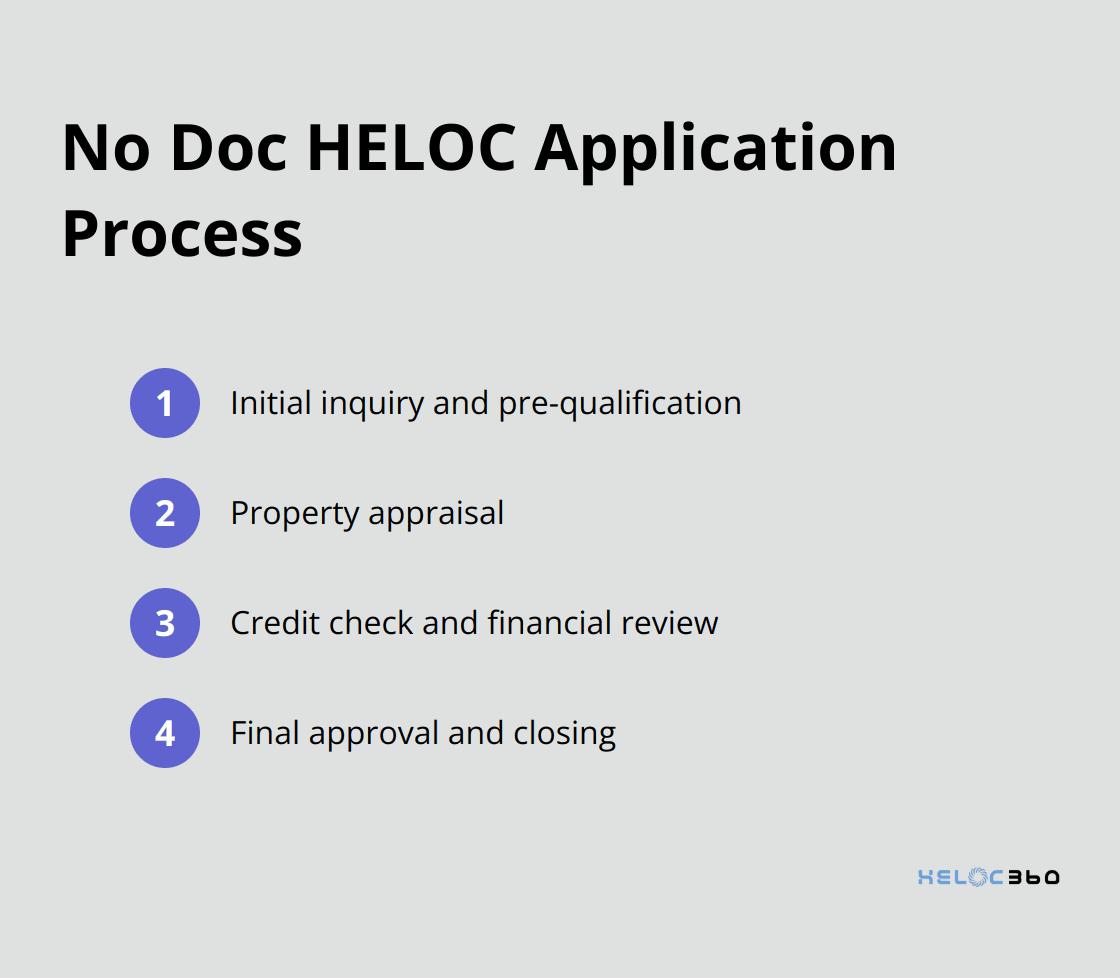

The Application Process

The application process for a No Doc HELOC typically involves:

While No Doc HELOCs offer more flexibility, they often come with higher interest rates to offset the increased risk for lenders. Always compare offers from multiple lenders to ensure you're getting the best deal possible.

Final Thoughts

No doc HELOCs offer unique financing for homeowners with non-traditional income sources. These loans provide flexibility and easier qualification, but come with higher interest rates and potential risks. Borrowers must carefully evaluate their financial situation and long-term goals before choosing this option.

A strong credit score and substantial home equity play key roles in the approval process for no doc HELOCs. Lenders may use alternative methods like bank statements or asset verification to assess financial stability. It's important to compare offers from multiple lenders to secure the best terms possible.

We at HELOC360 can help you explore your home equity options (including no doc HELOCs). Our platform simplifies the process and connects you with lenders that match your unique needs. Contact us today to unlock the full potential of your home's value and take confident steps toward achieving your financial aspirations.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.