Understanding HELOC Minimum Payments A Guide

Table of Contents

At HELOC360, we understand that navigating HELOC minimum payments can be challenging for homeowners and investors alike.

This guide will demystify the concept of HELOC minimum payments, exploring how they're calculated and what factors influence them.

We'll also share practical strategies to help you manage these payments effectively, ensuring you make the most of your home equity line of credit.

What's a HELOC Minimum Payment?

Understanding the Basics

A HELOC minimum payment represents the smallest amount you must pay each month on your Home Equity Line of Credit. Many homeowners find these payments confusing, so let's clarify the concept.

HELOCs operate differently from traditional loans. During the draw period (typically 5-10 years), you can borrow money as needed up to your credit limit. Your minimum payment during this time usually covers only the interest on the amount you've borrowed.

For instance, if you borrow $50,000 at a 5% annual interest rate, your monthly minimum payment would be approximately $208 (covering only the interest, not the principal).

Calculation Methods

Lenders use various approaches to calculate HELOC minimum payments:

- Percentage of balance: You pay a fixed percentage of your outstanding balance monthly.

- Interest-only: You pay only the interest accrued on your balance.

- Fixed amount: You pay a set dollar amount monthly, regardless of your balance.

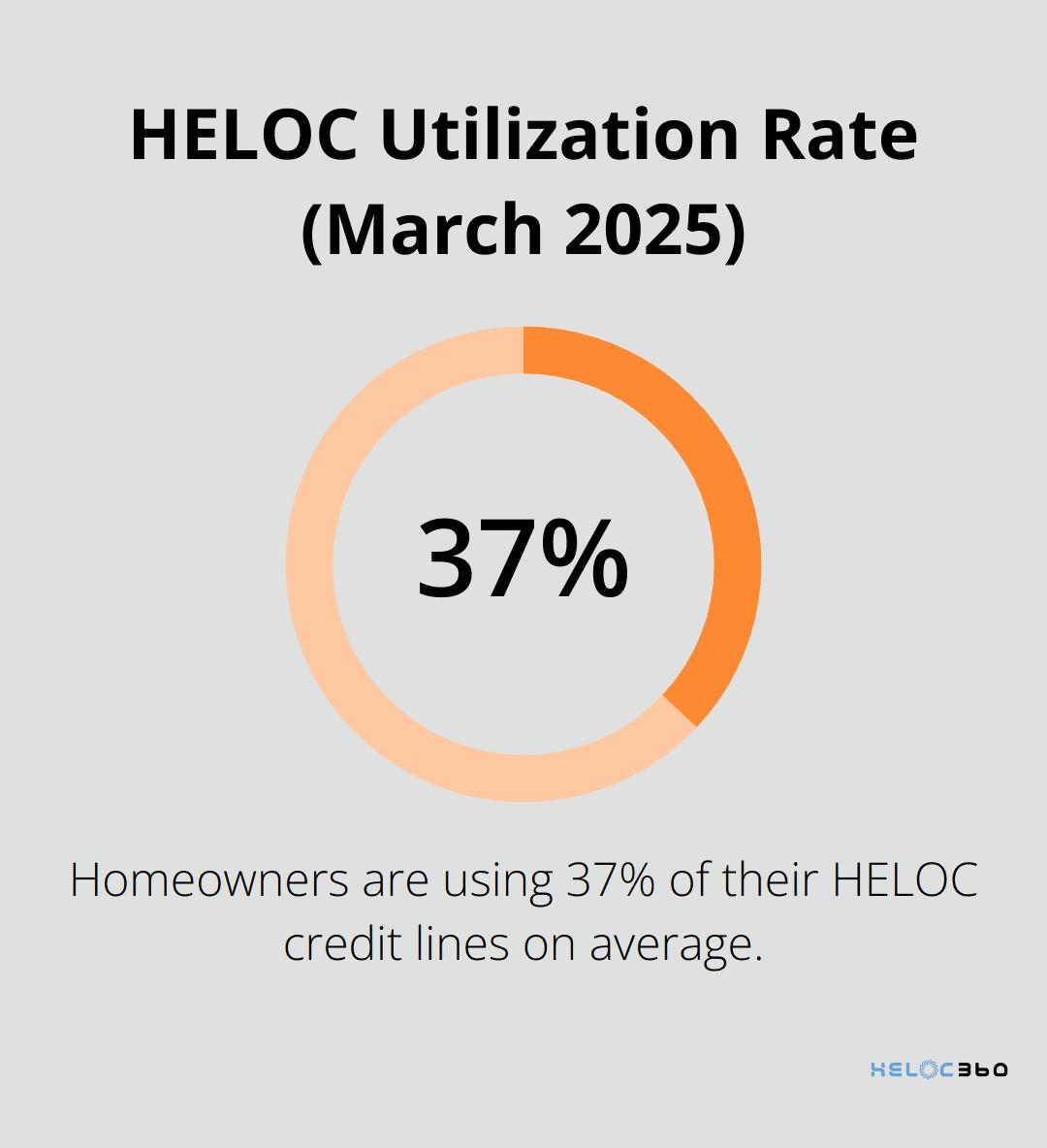

Based on an average HELOC balance of $45,157, homeowners with HELOC balances are collectively using about 37% of their lines of credit as of March 2025.

Interest-Only vs. Principal-Plus-Interest

Most HELOCs require interest-only minimum payments during the draw period. This keeps your payments low but doesn't reduce your principal balance.

Once you enter the repayment period, your minimum payments will include both principal and interest. This shift can cause a significant increase in your monthly payment, often called "payment shock."

Consider this example: If you have a $100,000 HELOC balance at 5% interest, your interest-only payment would be about $417 per month. However, in a 20-year repayment period, your principal-plus-interest payment increases to about $660 per month.

Understanding these differences plays a key role in effective financial planning. You should consider your long-term financial goals when deciding how much to pay each month, even during the draw period.

The Impact on Your Finances

The structure of HELOC minimum payments can significantly affect your financial situation. Interest-only payments during the draw period might seem attractive due to their lower amounts, but they can lead to a larger debt burden in the long run.

On the other hand, making principal-plus-interest payments from the start can help you build equity faster and reduce the overall cost of borrowing. However, this approach requires higher monthly payments, which might strain your budget.

Your choice between these options depends on your financial goals, cash flow, and debt-to-income ratio. As of May 2025, lenders typically want you to have a debt-to-income ratio of 43% to 50% at most, although some may require it to be even lower. As you weigh your options, consider how different payment structures align with your long-term financial strategy.

Now that we've covered the basics of HELOC minimum payments, let's explore the factors that influence these payments and how they can vary over time.

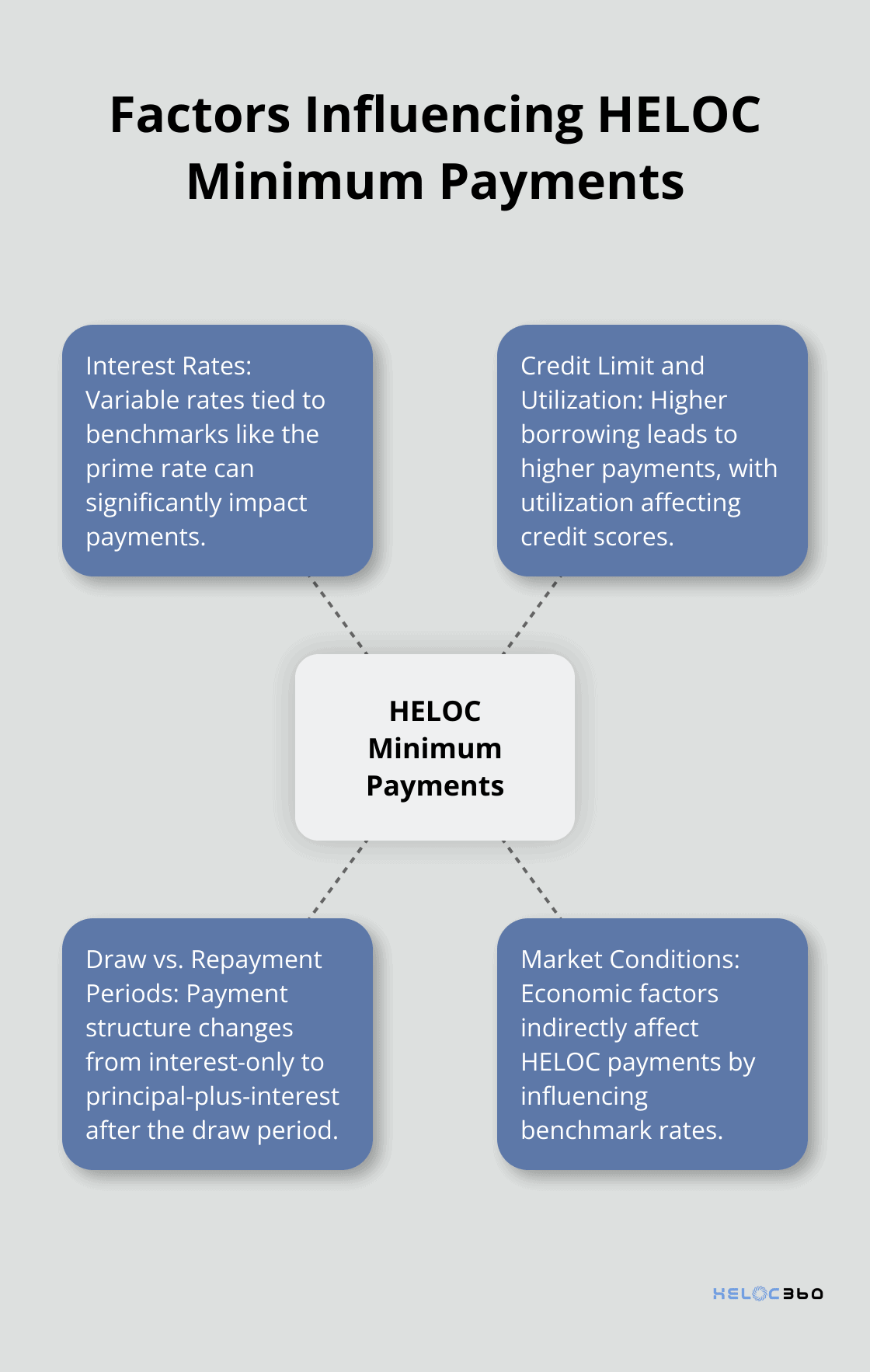

What Influences Your HELOC Minimum Payments?

Understanding the factors that affect your HELOC minimum payments will help you plan your finances effectively. Several variables can impact your budget and long-term financial health.

The Power of Interest Rates

Interest rates significantly determine your HELOC minimum payments. Most HELOCs have variable interest rates tied to a benchmark like the prime rate. As of August 2025, the national average home equity loan interest rate is 8.25% according to Bankrate's latest survey.

When interest rates increase, your minimum payments rise, even if you haven't borrowed additional funds. For instance, a 1% increase in your HELOC's interest rate could add $83 to your monthly payment on a $100,000 balance.

To protect against this risk, some lenders offer rate caps. These caps limit the amount your rate can increase over a specific period or the life of the loan. Ask potential lenders about their rate cap policies to better understand your long-term costs.

Credit Limit and Utilization Impact

Your credit limit and the amount you use also affect your minimum payments. The more you borrow, the higher your payments will be. HELOC balances rose in Q2 2025 for the 13th consecutive quarter, by $9 billion to $411 billion, according to the Federal Reserve Bank.

High utilization can also impact your credit score. Credit bureaus generally view utilization rates above 30% negatively. Try to keep your HELOC balance below this threshold if possible to maintain a healthy credit profile.

Draw vs. Repayment Periods: A Tale of Two Phases

The structure of your HELOC's draw and repayment periods significantly influences your minimum payments. During the draw period (typically 5-10 years), you might only need to pay interest on the amount borrowed. This can result in deceptively low minimum payments.

However, when the repayment period begins, your minimum payments will include both principal and interest. This shift can lead to a substantial increase in your monthly obligations. For example, if you've borrowed $50,000 at 5% interest, your monthly payment could jump from $208 (interest-only) to $330 (principal and interest over a 20-year repayment period).

To avoid payment shock, you can make principal payments during the draw period or set aside funds to prepare for higher future payments. Some lenders offer flexible repayment options to help ease this transition.

The Influence of Market Conditions

Market conditions play a significant role in shaping your HELOC minimum payments. Economic factors (such as inflation rates and Federal Reserve policies) can indirectly affect your HELOC by influencing the benchmark rates to which your HELOC is tied.

For instance, during periods of economic growth, interest rates tend to rise, potentially increasing your HELOC payments. Conversely, during economic downturns, rates might decrease, potentially lowering your payments.

Understanding these influencing factors will help you manage your HELOC effectively. Monitor interest rate trends, keep an eye on your utilization, and plan for the repayment period. These strategies will enable you to maximize your home equity while maintaining financial stability. In the next section, we'll explore practical strategies to manage your HELOC minimum payments effectively.

How to Optimize Your HELOC Payments

Managing your HELOC payments effectively will maintain your financial stability and maximize the benefits of your home equity line of credit. We present several practical approaches for you to consider:

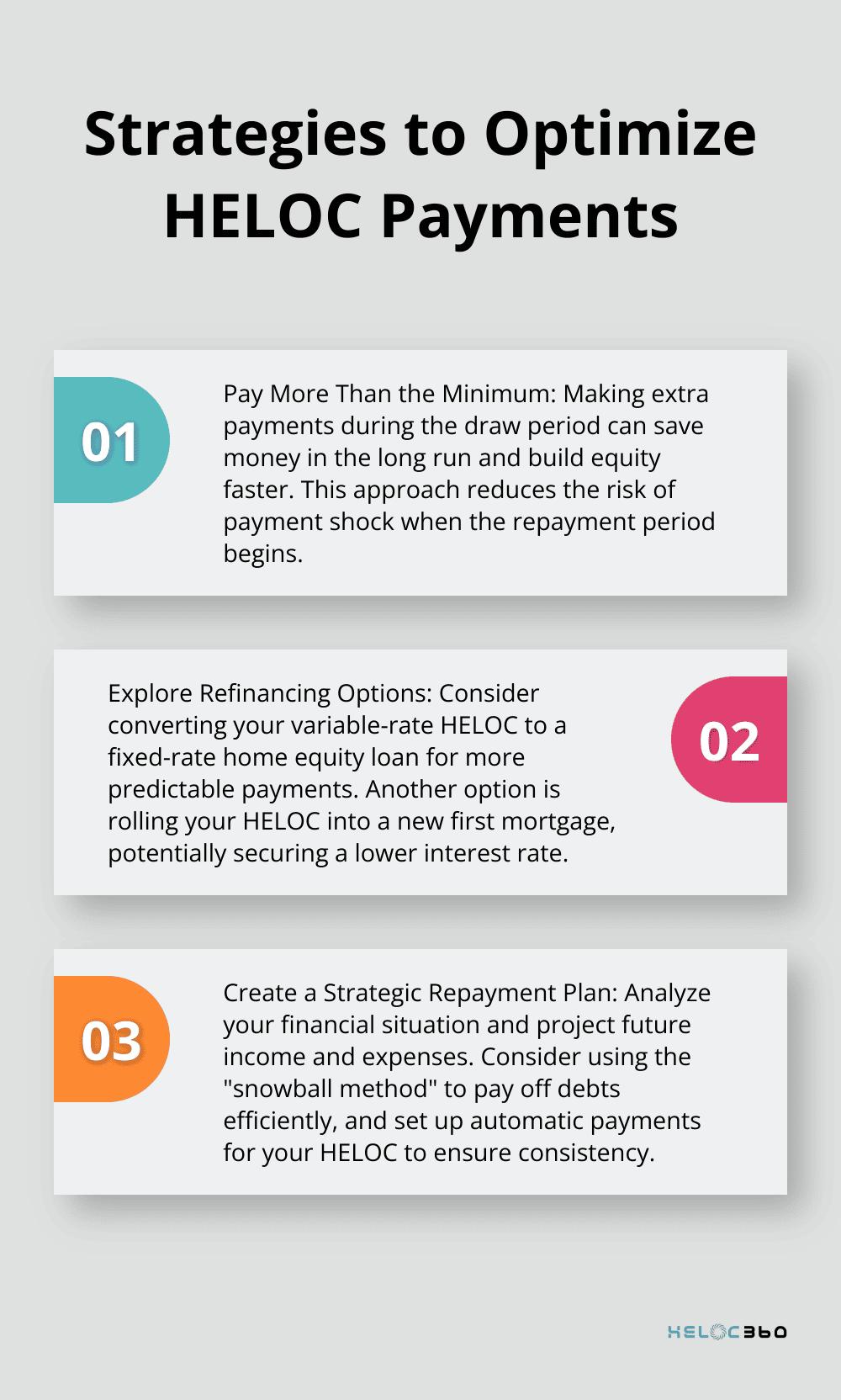

Pay More Than the Minimum

While minimum payments seem tempting, especially during the draw period, extra payments will save you money in the long run. HELOC payments can streamline your finances, increase flexibility, and potentially improve your credit score over time.

You can treat your HELOC like a mortgage from the start. Instead of making interest-only payments during the draw period, calculate what your payments would be if you paid both principal and interest over the full HELOC term. These larger payments from the beginning will build equity faster and reduce the risk of payment shock when the repayment period begins.

Explore Refinancing Options

If you struggle with your HELOC payments or anticipate future difficulties, refinancing could provide a solution. As of August 2025, many lenders offer competitive refinancing options for HELOCs.

One popular option converts your variable-rate HELOC to a fixed-rate home equity loan. This option provides more predictable payments and protection against future interest rate hikes. Recent data from the Mortgage Bankers Association shows HELOC and home equity loan debt outstanding grew 10.3 percent, with lenders expecting year-over-year growth of almost 10 percent for HELOC debt.

Another refinancing strategy rolls your HELOC into a new first mortgage. This strategy can be particularly beneficial if you secure a lower interest rate on the new mortgage. However, factor in closing costs and the potential extension of your loan term when considering this option.

Create a Strategic Repayment Plan

A comprehensive repayment plan is essential for long-term HELOC management. Start by analyzing your current financial situation and projecting your future income and expenses. This analysis will help you determine how much you can realistically allocate towards your HELOC payments each month.

The "snowball method" offers an effective approach. Pay extra on your HELOC while maintaining minimum payments on other debts. Once you pay off the HELOC, apply the amount you were paying towards it to your next highest-interest debt. This strategy will help you build momentum and reduce your overall debt more quickly.

Setting up automatic payments for your HELOC is also wise. Regular reviews and adjustments to your approach will ensure it continues to serve your unique situation effectively.

Your repayment strategy should align with your broader financial goals (whether you aim to pay off your HELOC quickly or maintain lower payments for cash flow flexibility). Regular reviews and adjustments to your approach will ensure it continues to serve your unique situation effectively.

Final Thoughts

HELOC minimum payments require careful consideration. These payments often cover only interest during the draw period, leading to low monthly obligations. However, homeowners must prepare for the repayment phase when payments increase to include both principal and interest.

Effective HELOC management involves more than meeting minimum payments. Homeowners can optimize their HELOC by paying extra when possible, exploring refinancing options, and creating a strategic repayment plan. These strategies help achieve financial goals more efficiently and maximize the benefits of this powerful financial tool.

For those seeking to leverage their home equity, HELOC360 offers tailored solutions to simplify the process. Our platform provides expert guidance and connects homeowners with suitable lenders (matching their unique requirements). With HELOC360, you can transform your home's value into a pathway for achieving your financial aspirations.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.