Understanding Your HELOC Amortization Schedule [Guide]

![Understanding Your HELOC Amortization Schedule [Guide]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2F2a445j5i%2Fproduction%2Fea99f076c08b25d5a38c99a4f81abddeaf711d50-1344x768.jpg%3Fauto%3Dformat&w=3840&q=75)

Table of Contents

Are you struggling to make sense of your HELOC amortization schedule? You're not alone.

At HELOC360, we understand that deciphering these financial documents can be challenging, especially for those new to home equity lines of credit (HELOCs).

This guide will break down the key components of a HELOC amortization schedule, helping you understand how your payments are applied and how interest accrues over time.

What's a HELOC Amortization Schedule?

The Blueprint of Your HELOC Repayment

A HELOC amortization schedule serves as a financial blueprint that outlines how your Home Equity Line of Credit will be repaid over time. This tool is essential for effective HELOC management and helps you avoid unexpected financial surprises.

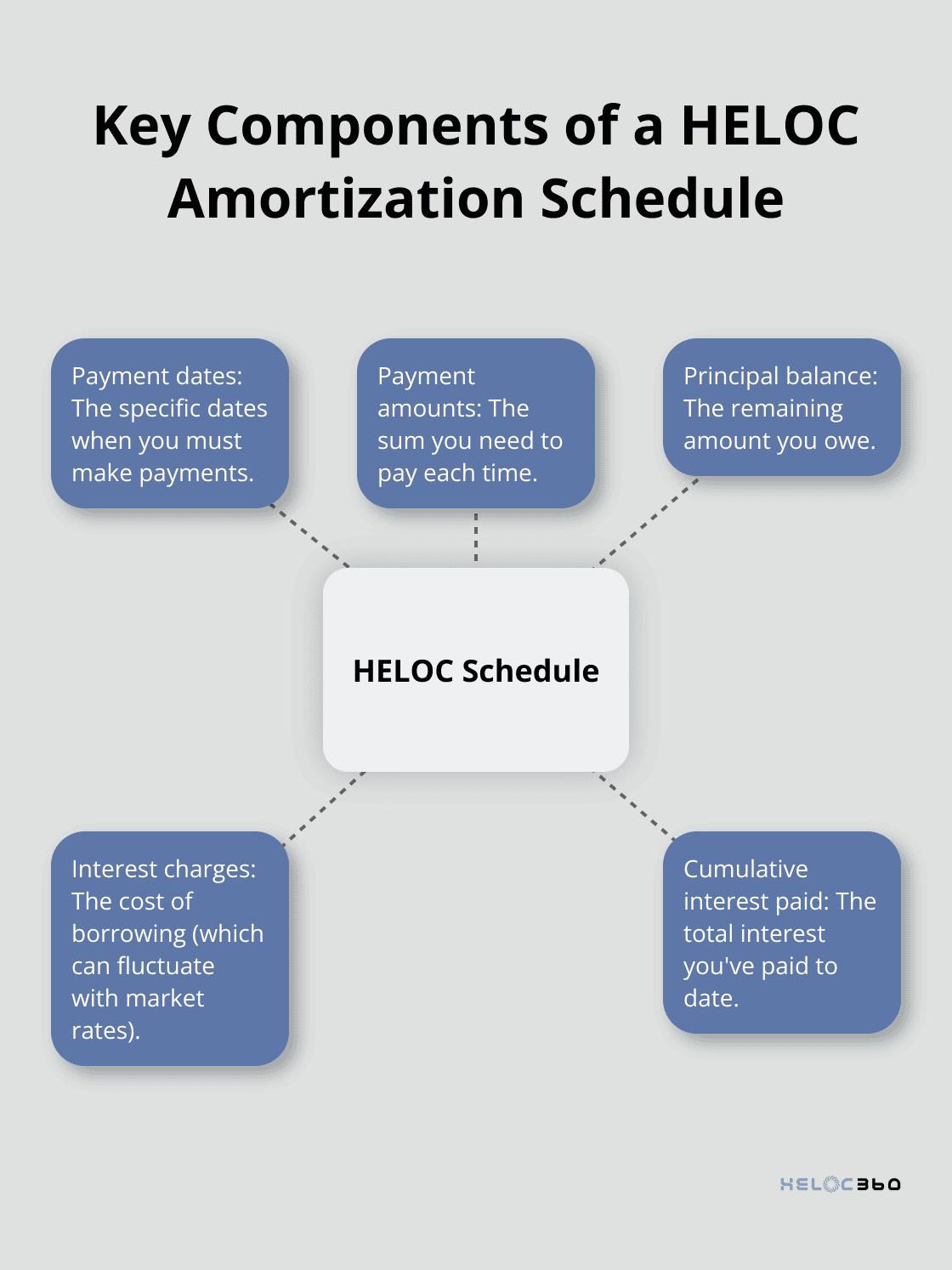

Key Components of Your HELOC Schedule

Your HELOC amortization schedule typically includes several important elements:

- Payment dates: The specific dates when you must make payments.

- Payment amounts: The sum you need to pay each time.

- Principal balance: The remaining amount you owe on your HELOC.

- Interest charges: The cost of borrowing (which can fluctuate with market rates).

- Cumulative interest paid: The total interest you've paid to date on your HELOC.

These components work in tandem to provide a clear picture of your HELOC's progression from start to finish.

HELOC Schedules vs. Traditional Mortgages

HELOC schedules differ significantly from traditional mortgage amortization schedules. While a mortgage schedule shows a steady decrease in the principal balance over time, a HELOC schedule is more dynamic.

During the draw period (typically 5-10 years), you might only need to make interest payments. This means your principal balance could remain unchanged or even increase if you continue to draw funds.

The repayment period follows, where you'll see your balance start to decrease as you pay both principal and interest. This two-phase structure (unique to HELOCs) can significantly impact your long-term financial planning.

The Importance of Schedule Comprehension

Understanding how to read and interpret your HELOC amortization schedule is important for several reasons:

- It helps you create more effective budgets by anticipating future payment amounts.

- You can identify potential payment spikes, especially when transitioning from the draw period to the repayment period.

- It allows you to calculate the total cost of borrowing over the life of your HELOC.

Mastering your HELOC amortization schedule equips you to make informed decisions about your home equity and overall financial strategy. If you're ever unsure about any aspect of your HELOC, don't hesitate to reach out to financial professionals or trusted platforms for guidance. Using an amortization calculator can help you understand how long it will take to repay your HELOC based on different payment amounts.

Now that we've covered the basics of a HELOC amortization schedule, let's explore how to read and interpret these financial documents in more detail.

How to Read Your HELOC Amortization Schedule

Decoding the Columns and Rows

Your HELOC amortization schedule contains several columns, each representing a key aspect of your loan:

- Payment Date: The due date for each payment

- Payment Amount: The total sum you must pay each period

- Interest Paid: The portion of your payment that covers interest

- Principal Paid: The amount that reduces your HELOC balance

- Remaining Balance: Your outstanding HELOC debt after each payment

Each row represents a single payment period (usually monthly). As you progress down the rows, you'll observe how your HELOC balance decreases over time.

Understanding the Two HELOC Phases

HELOCs typically consist of two distinct periods: the draw period and the repayment period.

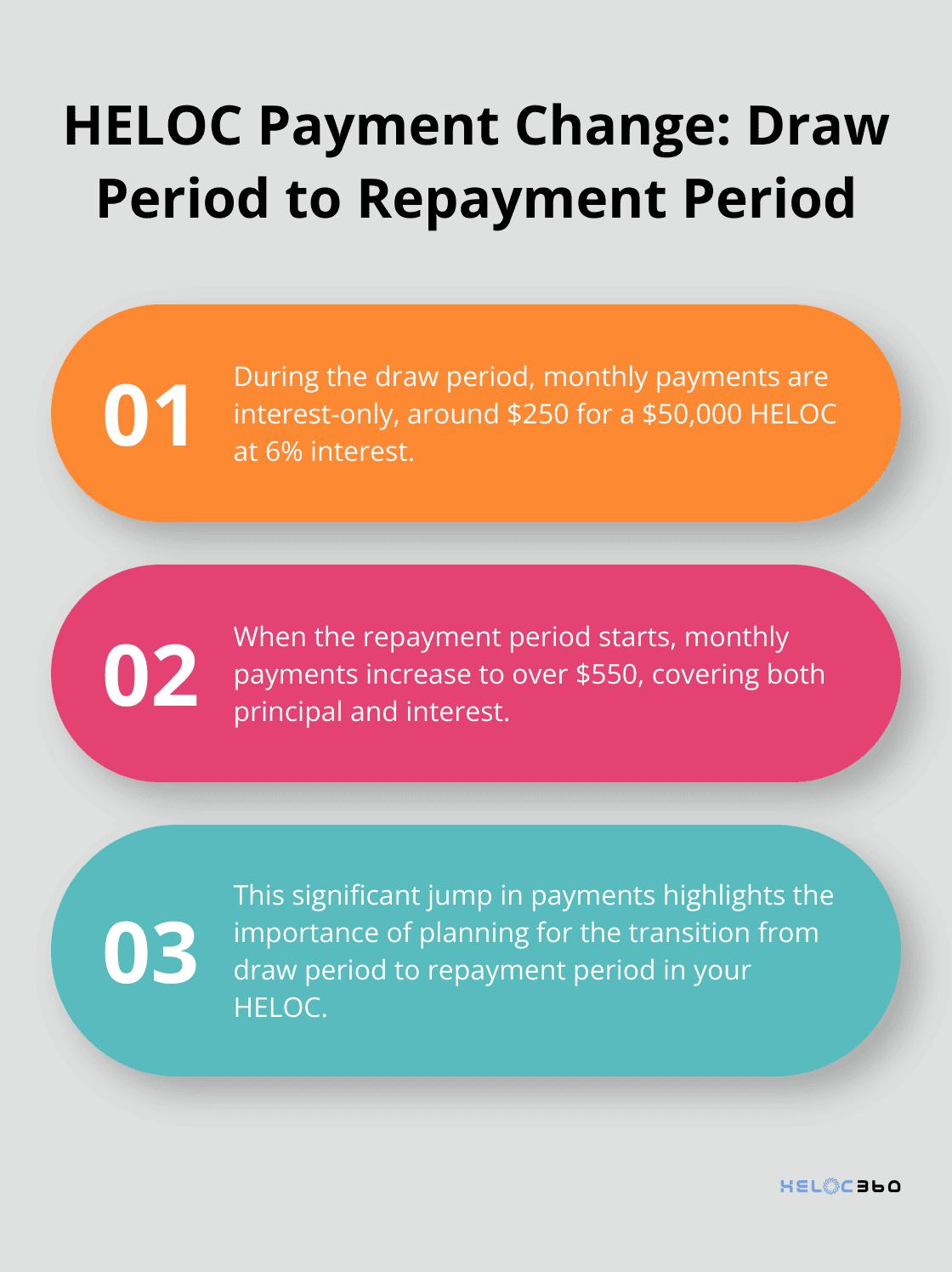

The draw period is usually 10 years, during which you can withdraw funds up to your HELOC limit. You might only need to make interest payments during this time. Your principal balance won't decrease unless you choose to pay extra. Making only minimum payments during this time can result in a significant payment increase when the repayment period begins.

The repayment period marks the start of paying both principal and interest. Your payments will likely increase during this phase, sometimes substantially. For example, a $50,000 HELOC balance at 6% interest could see monthly payments jump from about $250 (interest-only) to over $550 (principal and interest) when the repayment period starts.

How to Calculate Your Total Interest

To determine the total interest over the life of your HELOC, add up all the interest payments in the "Interest Paid" column. This total can provide motivation to make extra payments and reduce your overall costs.

Consider this example: On a $100,000 HELOC at 6% interest (with a 10-year draw period and 20-year repayment period), you could end up paying over $120,000 in interest if you only make minimum payments. However, an extra $100 per month could save nearly $30,000 in interest and help you pay off your HELOC years earlier.

Leveraging Your Schedule for Financial Planning

Your HELOC amortization schedule serves as a powerful financial tool. It allows you to:

- Create more effective budgets by anticipating future payment amounts

- Identify potential payment spikes, especially when transitioning from the draw period to the repayment period

- Calculate the total cost of borrowing over the life of your HELOC

Many homeowners use their amortization schedules to explore different payment scenarios and find the most cost-effective repayment strategy for their situation.

Now that you understand how to read and interpret your HELOC amortization schedule, let's explore the factors that can affect it and how you can adapt your strategy accordingly.

What Impacts Your HELOC Amortization?

The Rollercoaster of Interest Rates

Interest rates stand as the most volatile factor affecting your HELOC amortization. HELOCs typically come with variable interest rates that fluctuate based on market conditions. These changes can substantially impact your monthly payments and the total interest you'll pay over the life of your HELOC.

For example, if you have a $100,000 HELOC balance and your interest rate increases by 1%, your monthly payment could jump by $83 or more. Over a year, that's an extra $1,000 in interest payments. Conversely, if rates decrease, you could see savings.

To protect yourself from rate hikes, set aside extra funds during periods of lower rates. This buffer can help you manage potential payment increases without straining your budget. Some lenders offer rate caps (which limit how high your rate can go). Always ask about these features when shopping for a HELOC.

The Impact of Additional Draws and Payments

HELOCs allow you to draw funds as needed during the draw period. Each time you take money out, you increase your balance and potentially the amount of interest you'll pay over time.

Consider this scenario: You have a $150,000 HELOC and you've drawn $50,000. If you make another $20,000 draw for a home renovation, your balance jumps to $70,000. This increase will affect your amortization schedule, potentially extending the time it takes to pay off your HELOC or increasing your monthly payments during the repayment period.

On the flip side, making additional payments can significantly reduce your interest costs and shorten your repayment timeline. Even small extra payments can make a big difference. For instance, paying an extra $100 per month on a $100,000 HELOC at 6% interest could save you over $30,000 in interest and help you pay off your HELOC 5 years earlier.

The Timing Game: Draw and Repayment Periods

The length of your draw and repayment periods can dramatically affect your HELOC amortization. Typically, HELOCs have a 10-year draw period followed by a 20-year repayment period, but these terms can vary by lender.

A longer draw period gives you more time to access funds, but it also means you'll have less time to repay the balance. This can result in higher monthly payments during the repayment period. For example, if you have a $100,000 HELOC balance at 6% interest, your monthly payment could jump from $500 (interest-only during a 10-year draw period) to over $700 (principal and interest during a 15-year repayment period).

Conversely, a longer repayment period can lower your monthly payments but may result in paying more interest over time. It's a balancing act between manageable payments and minimizing total interest costs.

Understanding these factors empowers you to make informed decisions about your HELOC. Stay aware of interest rate trends, carefully consider additional draws, and understand the impact of your HELOC's timeline to better manage your home equity and overall financial health.

Final Thoughts

Your HELOC amortization schedule provides a clear roadmap of your borrowing journey. It helps you anticipate payment changes, track interest costs, and make informed decisions about your home equity use. By understanding your schedule, you can navigate variable interest rates, manage additional draws wisely, and plan for the transition from draw to repayment periods.

To manage your HELOC effectively, review your amortization schedule regularly, especially when market conditions change. Make extra payments when possible to reduce your overall interest costs and potentially shorten your repayment timeline. Be strategic about additional draws during your draw period, always weighing the long-term impact on your finances.

Ready to take control of your HELOC? At HELOC360, we're here to help you unlock the full potential of your home equity. Our platform simplifies the HELOC process, offers expert guidance, and connects you with lenders that fit your unique needs. Whether you're funding renovations, consolidating debt, or creating financial flexibility, we can help you make the most of your HELOC.

Take the next step in optimizing your HELOC strategy. Visit HELOC360.com today to explore our tools, resources, and personalized HELOC solutions. Don't let your home equity work harder for you – start maximizing your HELOC potential now!

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.