What Is The Minimum Credit Score For A HELOC?

Table of Contents

At HELOC360, we often get asked about the minimum credit score for a HELOC. It's a crucial factor in determining your eligibility for this type of loan.

A Home Equity Line of Credit (HELOC) can be a powerful financial tool, but lenders have specific requirements to manage their risk. Understanding these credit score thresholds can help you prepare for a successful application.

What's a HELOC and Why Does Credit Matter?

Understanding HELOCs

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against their property's equity. It functions as a loan that allows you to borrow, spend, and repay as you go, using your home as collateral. You can draw funds during a specific period (typically 10 years) and then enter the repayment phase.

HELOCs offer flexibility for various financial needs, such as home improvements or debt consolidation. Their versatility makes them an attractive option for many homeowners.

The Importance of Credit Scores

Your credit score serves as a financial report card, representing your creditworthiness. It considers factors like payment history, credit utilization, and length of credit history. For HELOC applications, this score plays a pivotal role.

Most lenders require a minimum credit score of 620 for HELOC approval. However, scores of 680 or higher often secure better rates and terms. Some lenders may prefer scores of 720 or above for the most favorable conditions.

How Lenders Evaluate Your Score

Lenders use your credit score to assess the risk of lending to you. A higher score indicates a higher likelihood of timely repayment. This assessment affects not only approval but also your interest rate and credit limit.

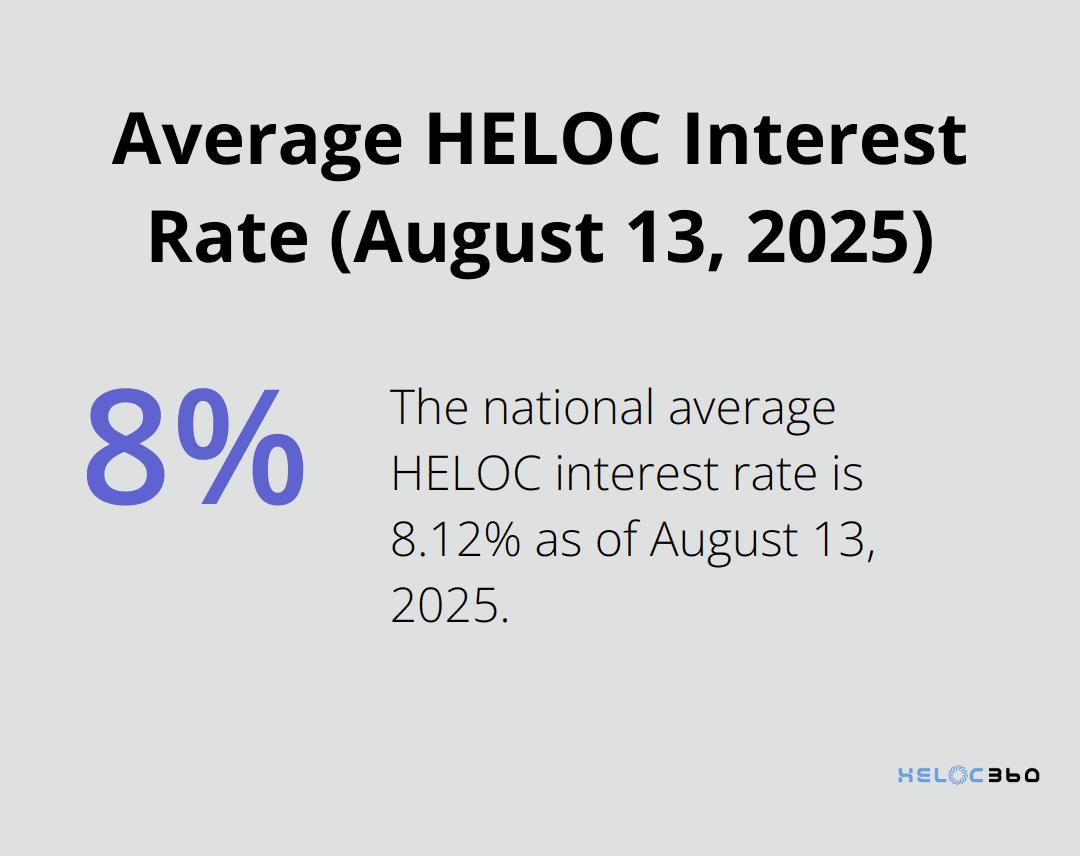

For instance, a higher credit score might qualify you for a HELOC with a better interest rate. According to Bankrate's latest survey, the national average HELOC interest rate is 8.12% as of August 13, 2025. These percentage points can significantly impact your HELOC's overall cost.

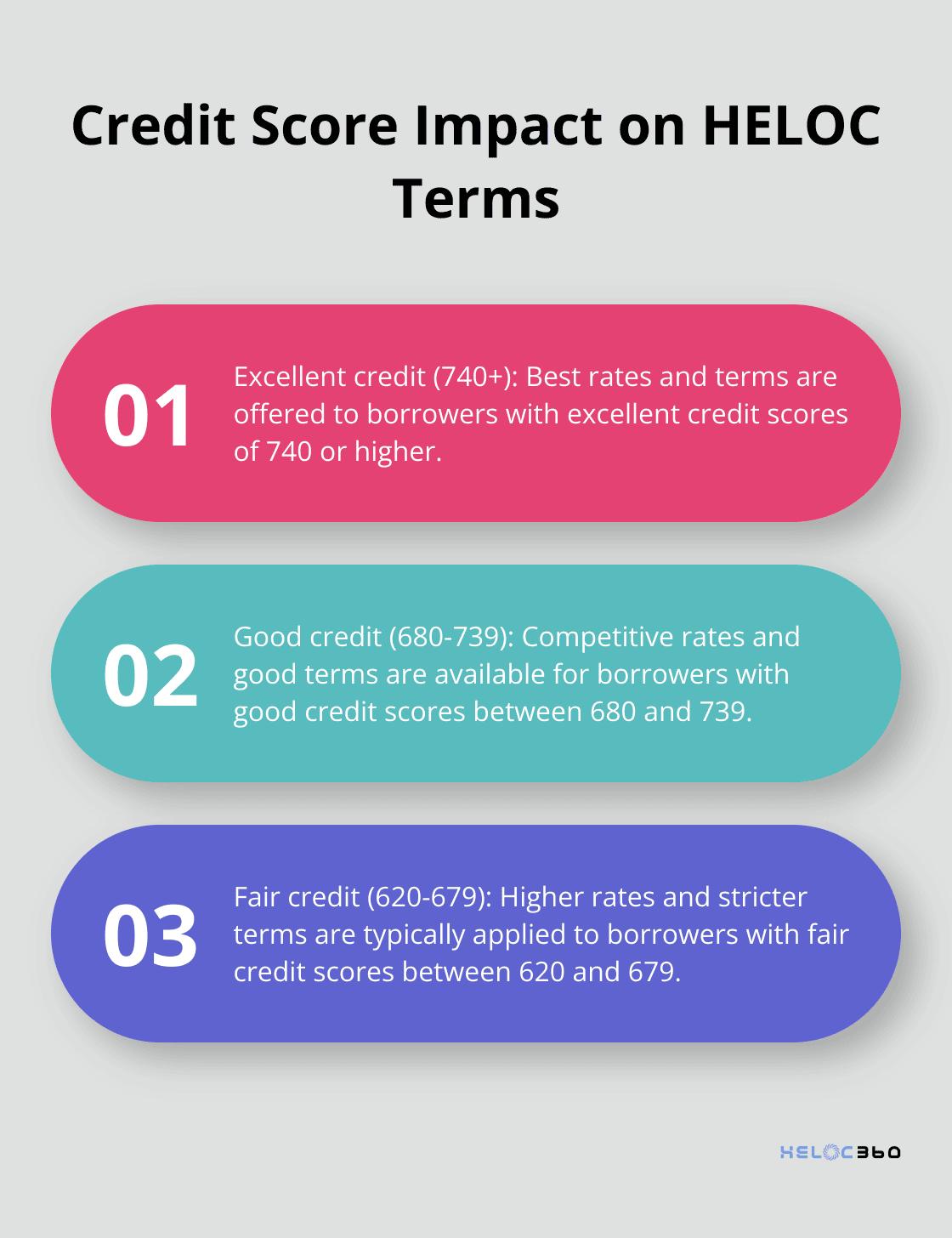

The Impact on HELOC Terms

Your credit score can make a substantial difference in HELOC terms. Here's a quick breakdown:

- Excellent credit (740+): Best rates and terms

- Good credit (680–739): Competitive rates, good terms

- Fair credit (620–679): Higher rates, stricter terms

- Poor credit (below 620): Difficulty qualifying, very high rates if approved

Preparing for Your HELOC Application

To improve your chances of securing favorable HELOC terms, try to boost your credit score before applying. Pay bills on time, reduce credit card balances, and avoid opening new credit accounts in the months leading up to your application.

Understanding the relationship between credit scores and HELOCs empowers you to make informed decisions. As we move forward, let's explore the typical credit score requirements across different lenders and how they might vary.

What Credit Score Do You Need for a HELOC?

The Baseline for HELOC Approval

Many lenders allow you to tap your equity with a credit score in the 600s. While 680 was once common, the norm is now closer to 620, especially for HELOCs. This range serves as a starting point, not a guarantee of approval or favorable terms.

A 2025 survey by LendingTree revealed that the average minimum credit score across top HELOC lenders was 645. However, this average masks significant variations among lenders. Some accept lower scores, while others demand higher ones.

Variations Among Lenders

Credit unions often offer more flexible credit requirements. Understanding the nuances of these loans, especially when comparing credit unions with traditional banks, can lead to more informed and beneficial decisions. For example, some lenders provide HELOCs with a minimum credit score of 600. In contrast, traditional banks like Wells Fargo and Bank of America typically look for scores of 680 or higher.

Online lenders and fintech companies sometimes set more lenient credit requirements. However, they may offset this increased risk with higher interest rates or fees.

Beyond the Credit Score

Your credit score plays a significant role, but it's not the only factor lenders consider. Other elements can influence HELOC approval and terms:

- Debt-to-Income Ratio (DTI): The maximum DTI varies for different lenders. Overall, the lower your debt-to-income ratio, the easier it can be to qualify for a HELOC.

- Loan-to-Value Ratio (LTV): Lenders typically cap combined LTV (including your first mortgage) at 80–85%. Significant equity might offset a lower credit score.

- Payment History: A solid record of on-time payments can work in your favor, even if your overall score isn't perfect.

- Income Stability: Consistent, verifiable income strengthens your application (especially important for self-employed individuals).

- Property Type and Location: Some lenders impose stricter requirements for certain property types or locations they deem riskier.

The Impact of Credit Scores on HELOC Terms

Your credit score can significantly affect your HELOC terms. Here's a quick breakdown:

These categories (and their associated scores) can vary between lenders, but they provide a general guideline for what to expect.

Now that you understand the role of credit scores in HELOC applications, let's explore strategies to improve your credit score and boost your chances of approval.

How to Boost Your Credit Score for a HELOC

A higher credit score can lead to more favorable HELOC offers. Here's how you can improve your score effectively:

Pay Down Your Debts

One of the quickest ways to improve your credit score is to reduce your credit utilization ratio. This ratio represents how much of your available credit you use. Try to keep it below 30% for each credit card and across all your accounts.

For example, if you have a $10,000 credit limit, keep your balance below $3,000. Closing a HELOC could increase your credit utilization ratio for VantageScore credit scores because you'll have less available credit.

Set Up Automatic Payments

Late payments can severely impact your credit score. Setting up automatic payments ensures you never miss a due date. Making HELOC payments on time could help your credit scores, but missing a payment by 30 days or more can negatively impact your score.

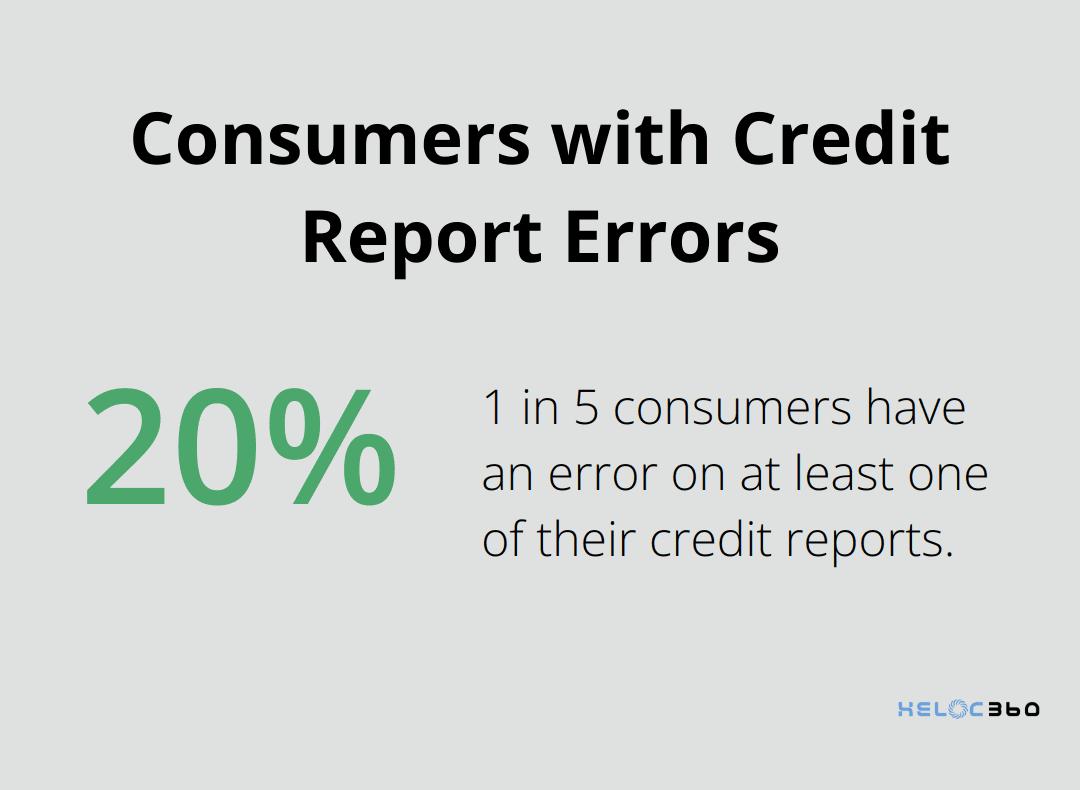

Dispute Errors on Your Credit Report

Check your credit reports regularly for inaccuracies. A Federal Trade Commission study found that 1 in 5 consumers had an error on at least one of their credit reports. Disputing and correcting these errors can lead to a quick boost in your score.

Become an Authorized User

Ask a family member or close friend with excellent credit to add you as an authorized user on their credit card. Their positive payment history can boost your score.

Keep Old Accounts Open

The length of your credit history accounts for about 15% of your FICO score. Keep old accounts open, even if you're not using them, to maintain a longer average credit age. Use these cards occasionally to keep them active.

Final Thoughts

The minimum credit score for HELOC approval typically starts at 620, with some lenders accepting scores as low as 600. You should try to achieve a score of 680 or higher to improve your chances of approval and secure more favorable terms. Your credit score, debt-to-income ratio, loan-to-value ratio, and income stability all play important roles in the approval process.

Good credit maintenance benefits your overall financial health. Consistent bill payments, low credit utilization, and regular credit report monitoring help build a strong credit profile. This effort results in better loan terms, lower interest rates, and increased financial opportunities.

We at HELOC360 understand the complexities of home equity. Our platform simplifies the process and provides the knowledge and tools you need to make informed decisions about your home's equity (whether you're ready to apply for a HELOC or still working on improving your credit score). HELOC360 offers solutions to help you achieve your financial goals and unlock the full potential of your home equity.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.