Why Choose a Fixed-Rate HELOC Option?

Table of Contents

Are you considering a HELOC but worried about unpredictable interest rates? A HELOC fixed rate option might be the solution you're looking for.

At HELOC360, we've seen how fixed-rate HELOCs can provide homeowners with financial stability and peace of mind. This blog post will explore why choosing a fixed-rate HELOC could be a smart move for your financial future.

What Is a Fixed-Rate HELOC?

Understanding the Basics

A fixed-rate HELOC combines the flexibility of a traditional Home Equity Line of Credit with the stability of a fixed interest rate. This financial product has gained popularity as homeowners seek more predictable borrowing solutions.

Unlike traditional HELOCs with variable interest rates that fluctuate monthly, a fixed-rate HELOC locks in your interest rate for a set period. This results in consistent monthly payments, which simplifies budgeting and future planning.

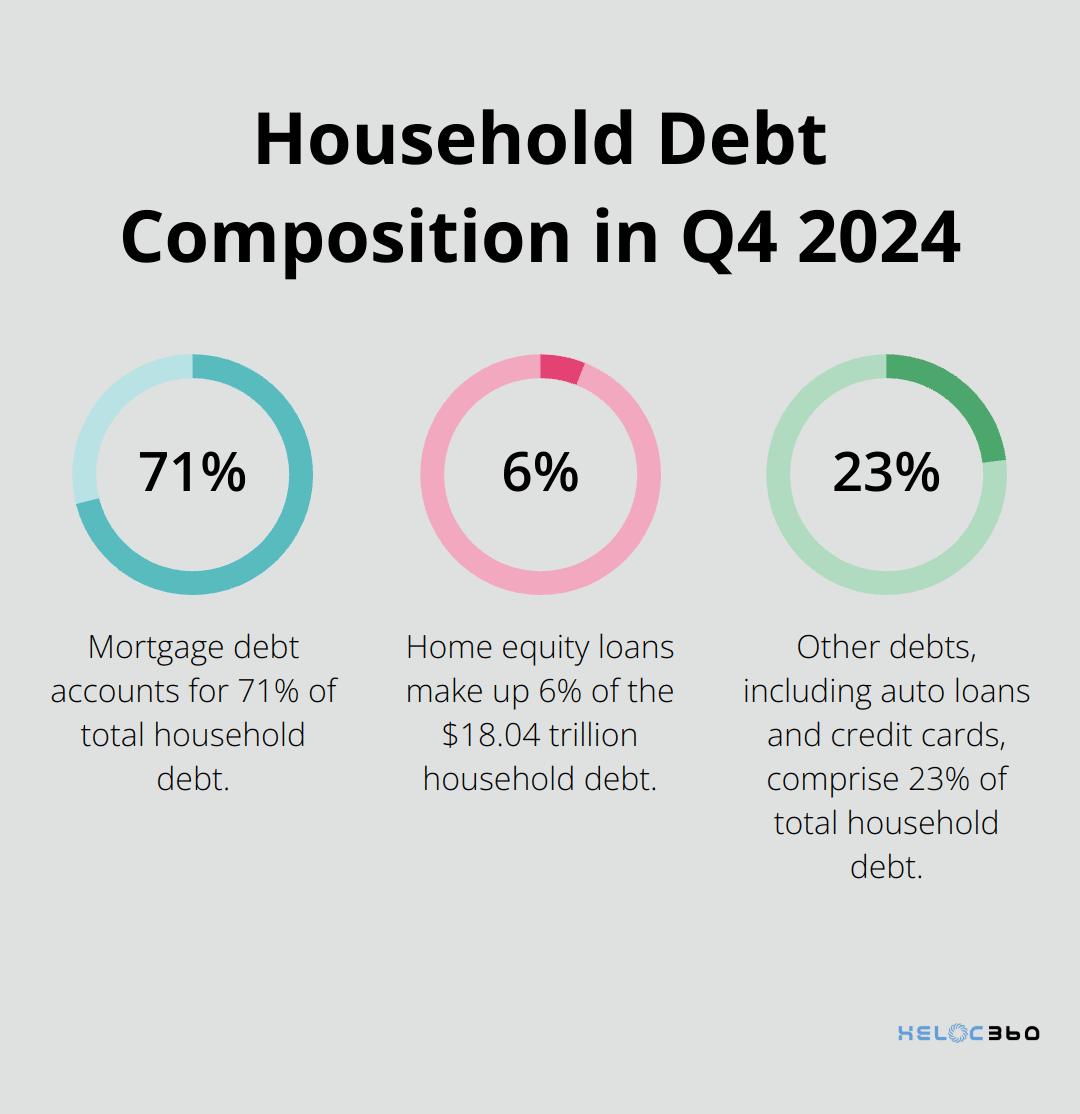

According to the Federal Reserve Bank of New York, household debt reached $18.04 trillion in Q4 2024, with home equity loans seeing renewed interest as homeowners explore financing options.

How Fixed-Rate HELOCs Function

When you opt for a fixed-rate HELOC, you create a hybrid product. You maintain the flexibility to draw funds as needed during your draw period, but you can lock in a fixed rate on the amount you borrow. Some lenders offer multiple fixed-rate portions within a single HELOC, providing even more control over your borrowing.

For instance, with a $100,000 HELOC, you could draw $30,000 for a home renovation project and lock that amount at a fixed rate. The remaining $70,000 stays available at a variable rate for future use.

Key Features to Consider

When you explore fixed-rate HELOC options, pay attention to these important features:

- Lock-in periods: These can range from five years to the length of the HELOC term, depending on the lender.

- Minimum draw amounts: Some lenders require a minimum amount (often $5,000 to $25,000) to qualify for a fixed rate.

- Conversion fees: Be aware that some lenders charge a fee to convert variable-rate balances to fixed-rate.

It's important to read the fine print and understand all terms before you commit to a fixed-rate HELOC. Many financial advisors recommend that you compare offers from multiple lenders to find terms that align with your financial goals.

As we move forward, let's examine the advantages that make fixed-rate HELOCs an attractive option for many homeowners.

Why Fixed-Rate HELOCs Make Financial Sense

Stability in an Uncertain Market

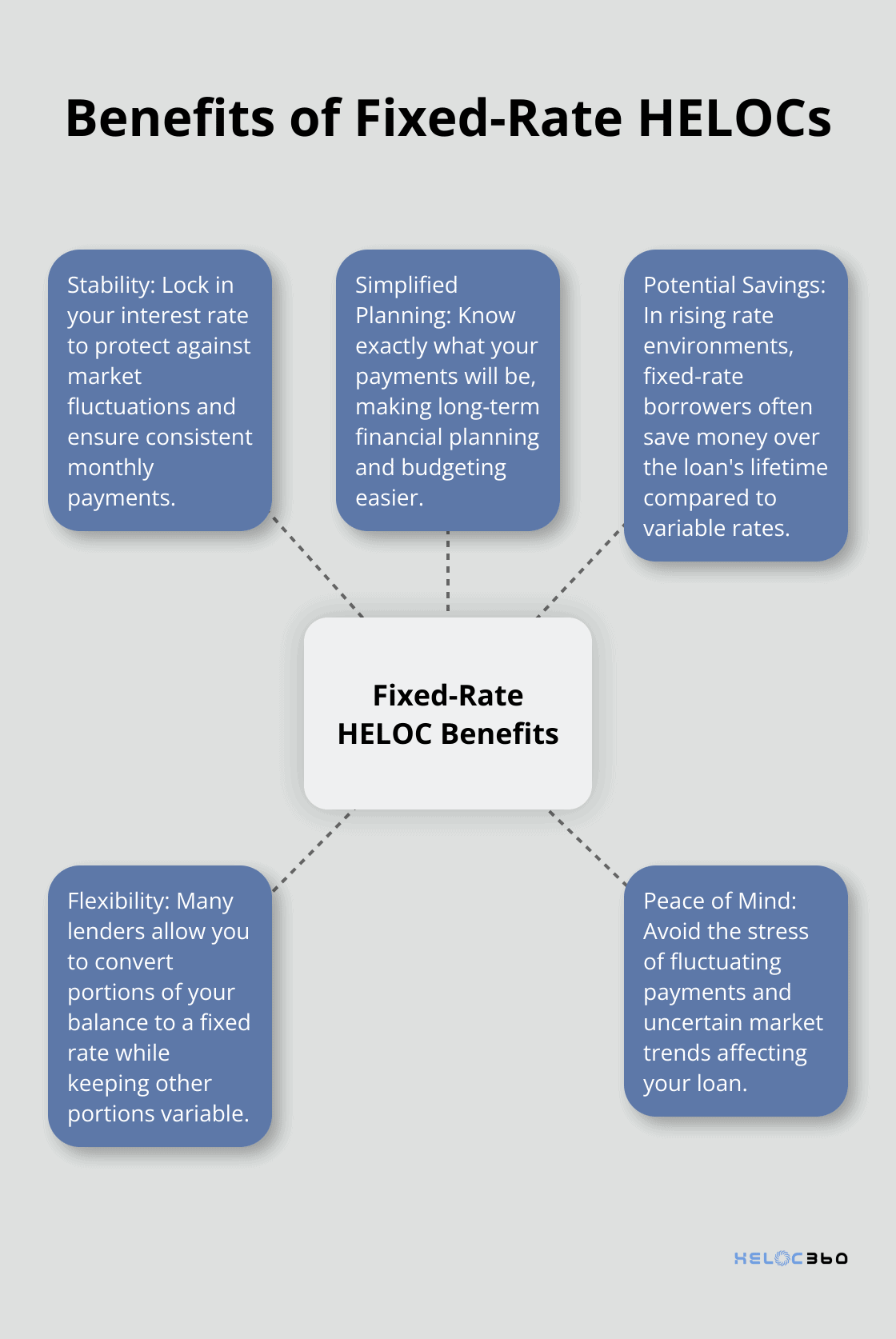

Fixed-rate HELOCs offer a safe harbor for borrowers in today's volatile economic climate. The Federal Reserve reports that interest rates have fluctuated more than usual in recent years, which makes variable-rate products less predictable. A fixed-rate HELOC shields you from these market swings, allowing you to borrow with confidence.

For instance, if you lock in a rate on a $50,000 draw, your payments will remain constant even if market rates climb. This stability can save you thousands over the life of your loan.

Simplified Financial Planning

One of the biggest advantages of a fixed-rate HELOC is the ease of budgeting it offers. You'll know exactly what your monthly payments will be for the duration of your loan term. This knowledge allows for more accurate long-term financial planning.

Financial advisors often recommend fixed-rate products for major expenses like home renovations or college tuition. With a clear repayment schedule, you can confidently allocate funds to other financial goals without worry about fluctuating HELOC payments throwing off your budget.

Potential for Significant Savings

While fixed rates may start slightly higher than variable rates, they can lead to substantial savings over time. The Consumer Financial Protection Bureau suggests that in rising rate environments, fixed-rate borrowers often come out ahead.

Let's consider an example: A $100,000 HELOC at a variable rate could end up costing much more if rates rise over a few years. In contrast, locking in a fixed rate from the start could save you thousands in interest over the loan's lifetime.

Protection Against Rate Hikes

A fixed-rate HELOC acts as a safeguard against unexpected rate increases. This protection becomes particularly valuable during periods of economic uncertainty or when the Federal Reserve signals potential rate hikes.

For homeowners who value predictability and want to avoid the stress of fluctuating payments, a fixed-rate HELOC provides peace of mind. You won't need to constantly monitor market trends or worry about how changing rates might impact your monthly budget.

Flexibility with Stability

While the term "fixed-rate" might suggest rigidity, many lenders offer flexible options within their fixed-rate HELOC products. Some allow you to convert portions of your balance to a fixed rate while keeping other portions variable (giving you the best of both worlds).

This flexibility allows you to tailor your borrowing strategy to your specific needs. You might choose to lock in a fixed rate for a large, one-time expense while keeping the rest of your credit line variable for ongoing or future needs.

As you weigh your options, consider how this stability and potential for savings align with your financial goals and risk tolerance. The next section will explore specific scenarios where a fixed-rate HELOC might be the ideal choice for your financial strategy.

When to Choose a Fixed-Rate HELOC

Funding Major Home Improvements

A fixed-rate HELOC proves an excellent financing option for substantial home renovation projects. If you plan to remodel your kitchen or add an extension to your home, you can draw a large sum at once and lock in a fixed rate. This approach provides you with the necessary funds while ensuring predictable repayment terms.

On average, renovating a small home might cost between $15,000 and $45,000, while larger properties could see costs soaring above $75,000. With a fixed-rate HELOC, you can borrow this amount without concern about fluctuating interest rates affecting your monthly payments over the loan's life.

Consolidating High-Interest Debt

Fixed-rate HELOCs serve as a powerful tool for debt consolidation. If you have multiple high-interest debts (such as credit card balances or personal loans), using a fixed-rate HELOC to pay them off can save you money and simplify your finances.

Consider this example: You have $50,000 in credit card debt with an average interest rate of 18%. Consolidating this debt with a fixed-rate HELOC could save you money over time. Plus, you'll know exactly what your monthly payments will be.

Planning for Long-Term Financial Goals

When you work towards long-term financial objectives (such as funding a child's education or planning for retirement), a fixed-rate HELOC can provide the stability you need. Locking in your interest rate allows you to accurately project your expenses and adjust your financial plan accordingly.

The College Board reports that the average cost of tuition and fees for the 2024-2025 academic year was $38,070 at private colleges and $10,740 for state residents at public colleges. A fixed-rate HELOC could help you secure the funds for education expenses without the uncertainty of variable rates.

Protecting Against Rising Interest Rates

In an environment where interest rates are expected to rise, a fixed-rate HELOC offers protection against increasing borrowing costs. This option becomes particularly attractive when economic indicators suggest potential rate hikes in the near future.

The Federal Reserve is projected to cut interest rates three more times in 2025, bringing the key borrowing benchmark to 3.5-3.75 percent. Locking in a fixed rate now could result in significant savings over the life of your HELOC.

Matching Your Risk Tolerance

Your personal risk tolerance plays a significant role in deciding whether a fixed-rate HELOC suits your needs. If you prefer stability and predictability in your financial obligations, a fixed-rate option aligns well with your risk profile.

A survey by the Financial Industry Regulatory Authority (FINRA) found that 50% of Americans have a low tolerance for financial risk. For these individuals, the predictable nature of fixed-rate HELOCs provides peace of mind and easier financial planning.

Final Thoughts

Fixed-rate HELOCs provide homeowners with stability and predictability in their borrowing. You can lock in your interest rate, which protects you against market fluctuations and simplifies your long-term financial planning. This option proves valuable for major expenses like home renovations, debt consolidation, or funding education costs.

A HELOC fixed rate offers more than just stability. You will enjoy easier budgeting, potential long-term savings, and the ability to tailor your borrowing strategy to your specific needs. In today's economic climate, where interest rates can be unpredictable, the fixed-rate HELOC offers a safe harbor for risk-averse borrowers.

We at HELOC360 want to help you explore the possibilities of a fixed-rate HELOC. Our platform empowers homeowners with knowledge and connects them with lenders that fit their unique needs. You can make informed decisions about leveraging your home equity with HELOC360.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.