Will a HELOC Boost or Tank Your Credit Score?

Table of Contents

At HELOC360, we often hear homeowners ask about the impact of HELOCs on their credit scores. It's a valid concern, as your credit score plays a crucial role in your financial life.

In this post, we'll explore how a HELOC credit line can affect your credit score, both in the short and long term. We'll also provide practical tips to help you manage your HELOC responsibly and potentially boost your credit score in the process.

What's a HELOC and How Does It Affect Your Credit?

Understanding Home Equity Lines of Credit

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against their home's equity. It functions similarly to a credit card, but with your house as collateral. HELOCs offer flexibility and potentially lower interest rates compared to unsecured loans.

The Anatomy of Credit Scores

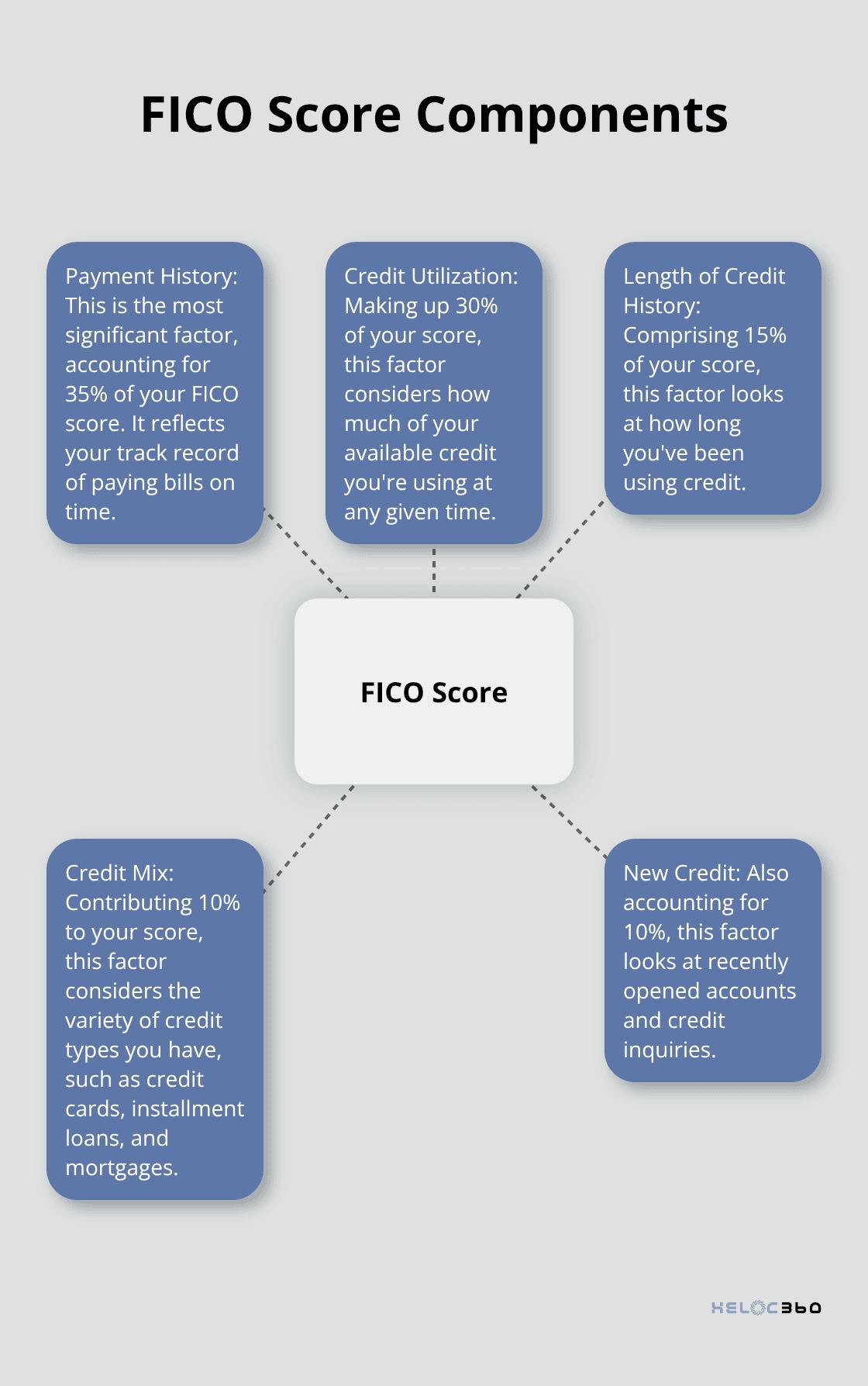

Your credit score numerically represents your creditworthiness. FICO scores range from 300 to 850, with a score in the mid to high 600s or above generally considered good. Higher scores indicate better credit health.

Five main factors influence your FICO score:

- Payment History (35%)

- Credit Utilization (30%)

- Length of Credit History (15%)

- Credit Mix (10%)

- New Credit (10%)

Understanding these components helps predict how a HELOC might impact your score.

HELOC's Interaction with Your Credit

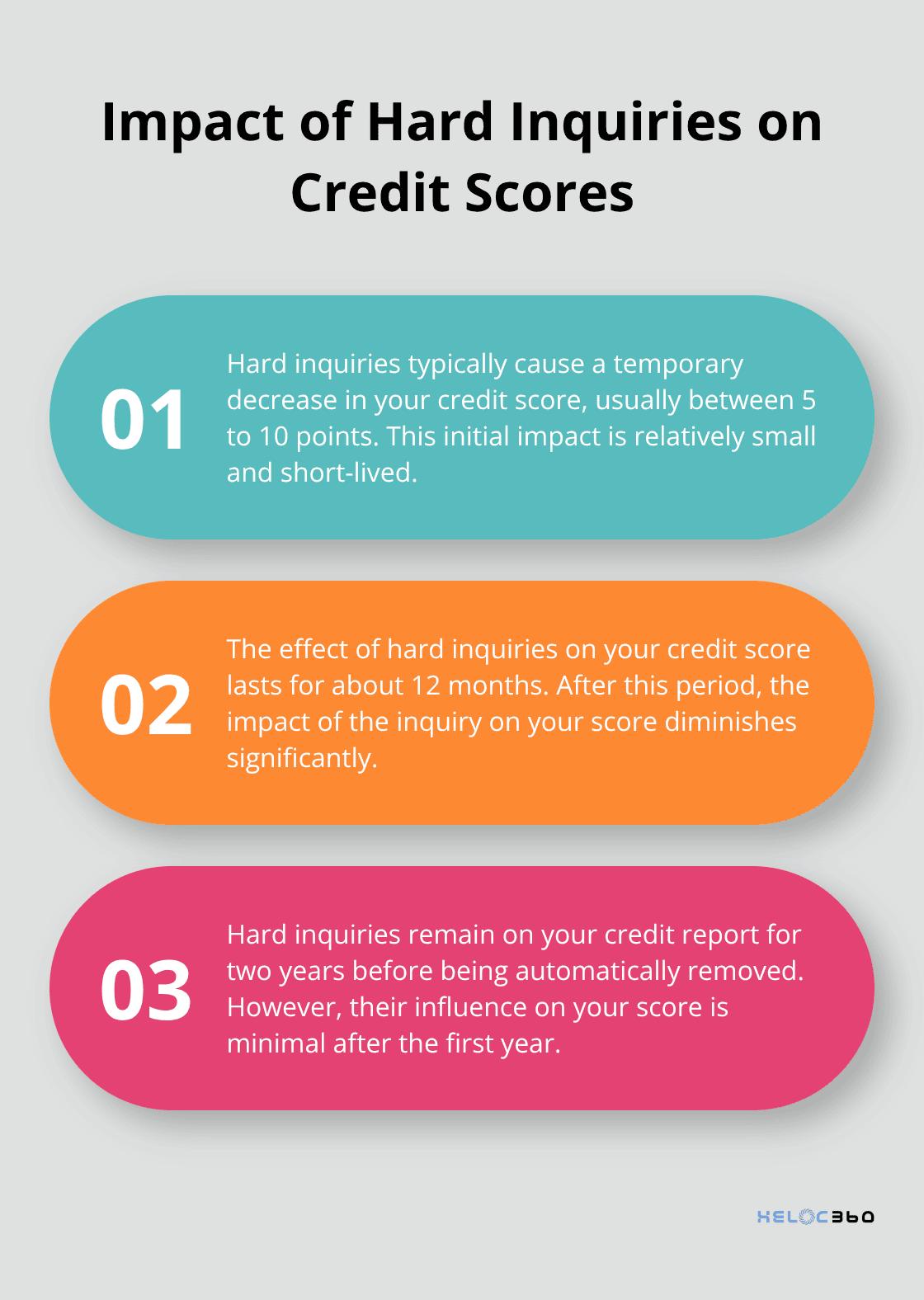

When you apply for a HELOC, the lender performs a hard inquiry on your credit report. This typically causes a temporary dip in your score. However, the long-term effects can be positive if managed correctly.

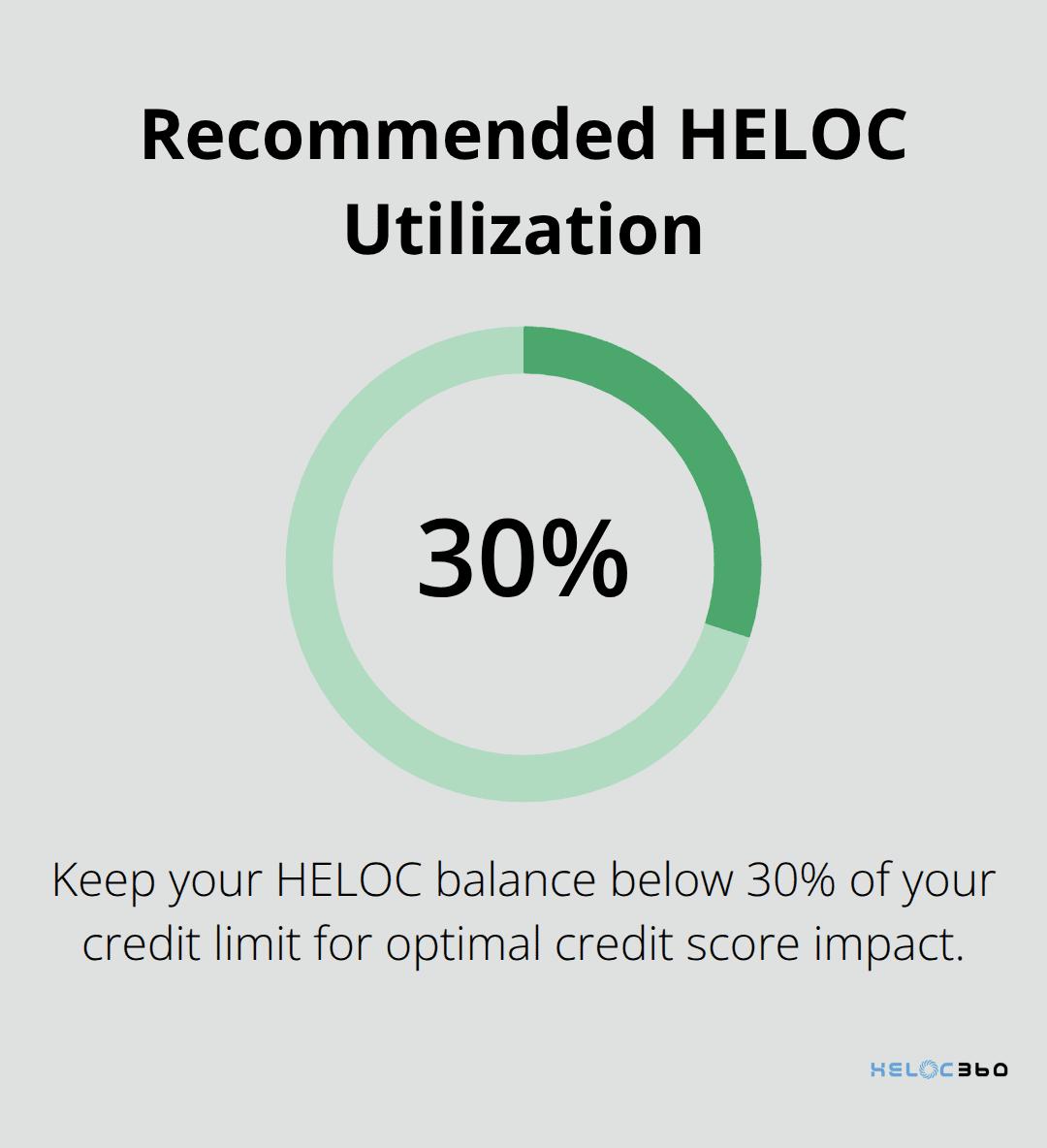

Lenders often report HELOCs as revolving credit, similar to credit cards. This means they can affect your credit utilization ratio, which could affect around 20% to 30% of your credit score depending on the scoring model. Try to keep this ratio low (ideally under 30%) for a beneficial impact on your score.

Interestingly, an unused HELOC can still affect your credit scores if the lender reports the account to the credit bureaus. This can benefit homeowners who keep HELOCs as financial backups.

The Dual Nature of HELOCs

HELOCs provide financial flexibility but also come with responsibilities. Timely payments are essential, as payment history is the most significant factor in your credit score calculation.

On the positive side, a HELOC can improve your credit mix (which accounts for 10% of your FICO score). Having different types of credit (revolving and installment) can positively impact your score.

A HELOC is secured by your home. While this often means lower interest rates, it also puts your home at risk if you default on payments. Always borrow responsibly and have a solid repayment plan in place.

As we move forward, let's explore the initial impact of obtaining a HELOC on your credit score, including the effects of hard inquiries and changes in credit utilization.

How a HELOC Impacts Your Credit Score

The Initial Credit Score Effect

When you apply for a Home Equity Line of Credit (HELOC), it triggers a hard inquiry on your credit report. This action typically results in a temporary decrease in your credit score, usually between 5 to 10 points. However, this impact is short-lived. Experian (one of the major credit bureaus) reports that hard inquiries only affect your score for about 12 months and disappear from your credit report after two years.

New Account Addition

After approval, your HELOC appears as a new account on your credit report. This addition can slightly lower the average age of your credit accounts, which constitutes about 15% of your FICO score. The impact is often minimal, especially if you have an established credit history.

Credit Utilization Shifts

Your credit utilization ratio can change with a HELOC. Applying for, opening and using a HELOC can help or hurt your credit scores depending on your overall credit profile and how you manage the account.

However, some lenders and other credit scoring models might include HELOCs in utilization calculations. If this occurs, maintaining a low HELOC balance relative to your credit limit can positively impact your score. Try to keep your utilization below 30% for the best effect on your credit score.

Long-Term Credit Benefits

Responsible use of a HELOC can improve your credit score over time. Timely payments and wise credit utilization demonstrate financial responsibility to lenders. This positive payment history (which accounts for 35% of your FICO score) can significantly boost your creditworthiness in the long run. If you close a HELOC that's in good standing, the closed account can stay on your credit reports for up to 10 years.

Credit Mix Enhancement

A HELOC can diversify your credit mix, which makes up 10% of your FICO score. Having different types of credit (both revolving and installment) can potentially influence your score. Applying for, opening and using a HELOC can help or hurt your credit scores depending on your overall credit profile and how you manage the account.

As we move forward, let's explore how a HELOC can affect your credit in the long term, including the potential for credit score improvements and best practices for HELOC management.

How a HELOC Affects Your Credit Long-Term

The Impact of Payment History

Your payment history constitutes 35% of your FICO score, making it the most significant factor. Consistent, on-time payments on your HELOC can boost your credit score substantially over time. To maximize the positive impact:

- Set up automatic payments to avoid missing due dates

- Pay more than the minimum when possible

- Monitor your payment due dates and amounts closely

Credit Mix Diversification

A HELOC adds variety to your credit mix (10% of your FICO score). Credit scoring models favor borrowers who manage various types of credit responsibly. Adding a HELOC to your credit profile demonstrates your ability to handle different credit types effectively. This proves particularly beneficial if your credit history primarily consists of credit cards or personal loans.

Potential Credit Utilization Advantages

Some scoring models exclude HELOCs from utilization calculations, while others include them. If your HELOC factors into your credit utilization, a low balance can positively impact your score. Try to maintain your utilization below 30% for optimal results. For instance, with a $100,000 HELOC, attempt to keep your balance under $30,000.

Strategic Debt Management

A HELOC can serve as a tool for strategic debt management. Some homeowners use their HELOC to pay off high-interest credit card debt, which can lower overall credit utilization and potentially improve their score. However, this strategy requires a solid repayment plan to avoid putting your home at risk.

Long-Term Credit Profile Enhancement

Responsible HELOC management can transform this financial tool into a credit-boosting asset. Make timely payments, maintain low balances, and use your HELOC strategically to reap long-term benefits. Over time, these actions can contribute to a stronger credit profile and potentially higher credit scores.

Final Thoughts

A HELOC can significantly impact your credit score, both positively and negatively. The initial hard inquiry might cause a small dip, but responsible management can lead to long-term credit improvements. Your payment history holds the most weight, so prioritize on-time payments for your HELOC credit.

Maintaining a low balance on your HELOC helps your credit utilization ratio and provides financial flexibility. If you use your HELOC for debt consolidation, create a solid repayment plan to protect your home. Don't open a HELOC solely for credit score improvement; ensure it aligns with your overall financial strategy.

We at HELOC360 provide tailored solutions to help you leverage your home's value effectively. Our platform offers expert guidance to navigate the complexities of home equity while maintaining your financial health. A HELOC is more than just a line of credit—it’s a tool to achieve your financial goals and secure your future.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.