Can You Get a HELOC on an Underwater Home?

Table of Contents

Owning a home with negative equity can be a challenging financial situation. Many homeowners in this position wonder if they can still access their home's equity through a HELOC.

At HELOC360, we often receive questions about getting a HELOC on an underwater home. This blog post will explore the possibilities, challenges, and alternatives for homeowners facing negative equity.

What Is an Underwater Home?

Definition of Negative Equity

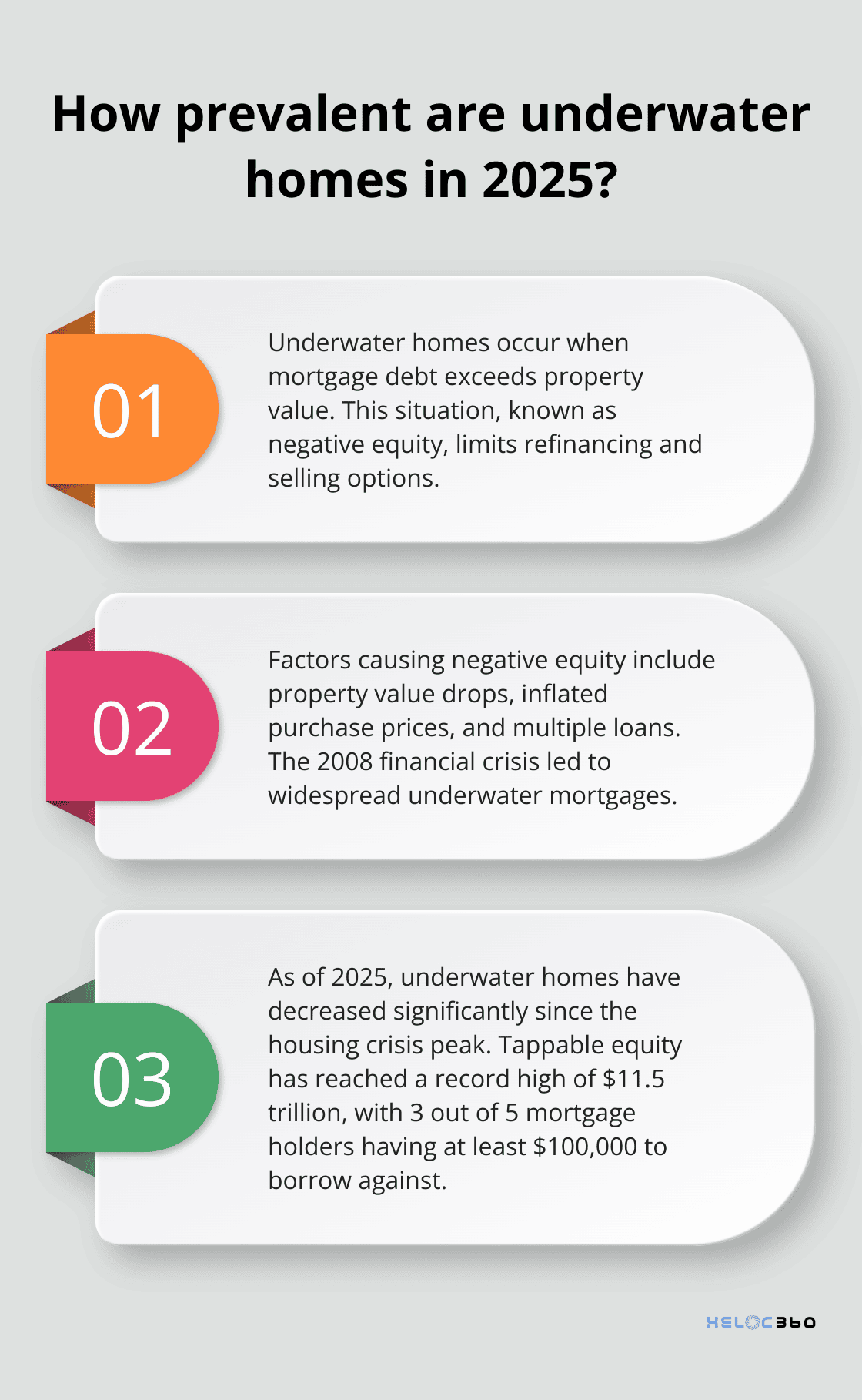

An underwater home occurs when a homeowner owes more on their mortgage than the current market value of their property. This financial predicament (also known as negative equity) can severely limit a homeowner's options for refinancing or selling their property.

Causes of Negative Equity

Several factors can lead to a home becoming underwater:

- Significant drops in local property values: This often happens during economic downturns or housing market crashes. For example, during the 2008 financial crisis, many homeowners found themselves underwater when housing prices plummeted across the United States.

- Purchasing properties at inflated prices: When homeowners buy during housing market bubbles and these bubbles burst, property values can quickly decline, leaving homeowners with mortgages that exceed their home's worth.

- Multiple loans against a property: Taking out second mortgages or home equity lines of credit (HELOCs) that, when combined with the primary mortgage, exceed the home's value can also lead to negative equity.

Current Underwater Home Statistics

As of 2025, the number of underwater homes in the US has decreased significantly since the peak of the housing crisis. However, it remains a concern for many homeowners. According to Ice Mortgage Technology, tappable equity has hit a record high of $11.5 trillion, with 3 out of 5 mortgage holders having at least $100,000 to borrow against.

The prevalence of underwater homes varies by region. Areas that experienced rapid price appreciation followed by sharp declines are more likely to have higher rates of negative equity. For instance, some parts of the West Coast and South have seen recent declines in home values, potentially increasing the risk of underwater mortgages in these regions.

Impact on Homeowners

Being underwater on a mortgage can have serious financial implications. It makes it difficult (if not impossible) to sell the home without bringing additional funds to the closing table. Refinancing options are also limited, as most lenders require at least 15% (preferably 20% or higher) equity in the home to qualify for a new loan or a HELOC.

For homeowners facing this situation, exploring all available options is essential. While obtaining a HELOC on an underwater home presents challenges, other solutions may exist. In the next section, we'll examine the specific hurdles homeowners face when trying to secure a HELOC on an underwater property and discuss potential alternatives.

Why Getting a HELOC on an Underwater Home Is Challenging

The Lender's Risk Assessment

Obtaining a Home Equity Line of Credit (HELOC) on an underwater home presents significant obstacles for homeowners. Lenders view underwater properties as high-risk investments, which makes them hesitant to extend additional credit.

From a lender's perspective, an underwater home poses a substantial risk. If the borrower defaults, the lender might not recover the full loan amount through foreclosure. This risk aversion has resulted in stricter lending criteria, especially since the 2008 financial crisis.

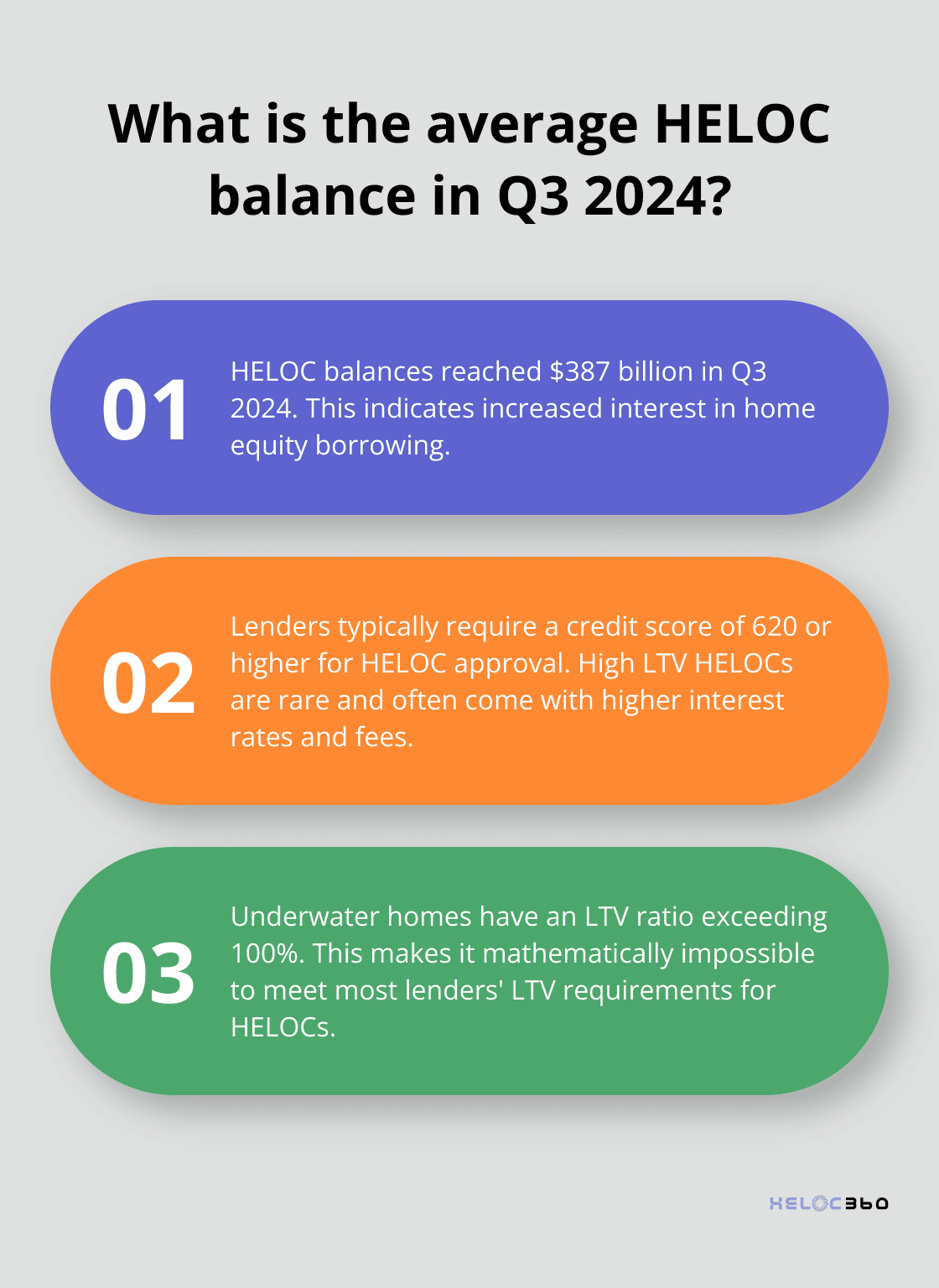

The Federal Reserve Bank of New York reports that HELOC balances reached $387 billion in Q3 2024, indicating increased interest in home equity borrowing. However, this growth primarily benefits homeowners with positive equity.

Loan-to-Value Ratio Hurdles

The loan-to-value (LTV) ratio plays a critical role in HELOC approval. Many lenders allow you to tap your equity with a credit score in the 600s, with 620 becoming more common, especially for HELOCs. For underwater homes (where the LTV exceeds 100%), meeting this requirement becomes mathematically impossible.

Some lenders offer high LTV HELOCs, but these are rare and often come with higher interest rates and fees. The Federal Housing Administration (FHA) occasionally provides programs for homeowners with high LTVs, but these typically focus on refinancing rather than HELOCs.

Credit Score and Income Requirements

A strong credit score and stable income are always important for loan approval, but they become even more vital when dealing with an underwater home. Lenders may require higher credit scores and lower debt-to-income ratios to offset the increased risk.

However, even with excellent credit and income, the fundamental issue of negative equity remains a significant barrier. A Bankrate survey shows that Americans still value homeownership, even though they feel their finances are standing in their way, highlighting the broader challenges in the housing market.

Exploring Alternatives

Given these challenges, homeowners with underwater mortgages often need to consider other options. Some alternatives include:

- Waiting for market conditions to improve

- Making extra mortgage payments to build equity faster

- Exploring government assistance programs for underwater homeowners

- Considering personal loans or other unsecured borrowing options (which may come with higher interest rates)

While traditional HELOCs might be out of reach for underwater homeowners, it's important to explore all available avenues. The next section will discuss alternative financing options and strategies for homeowners facing negative equity situations.

What Options Do Underwater Homeowners Have?

Government Assistance Programs

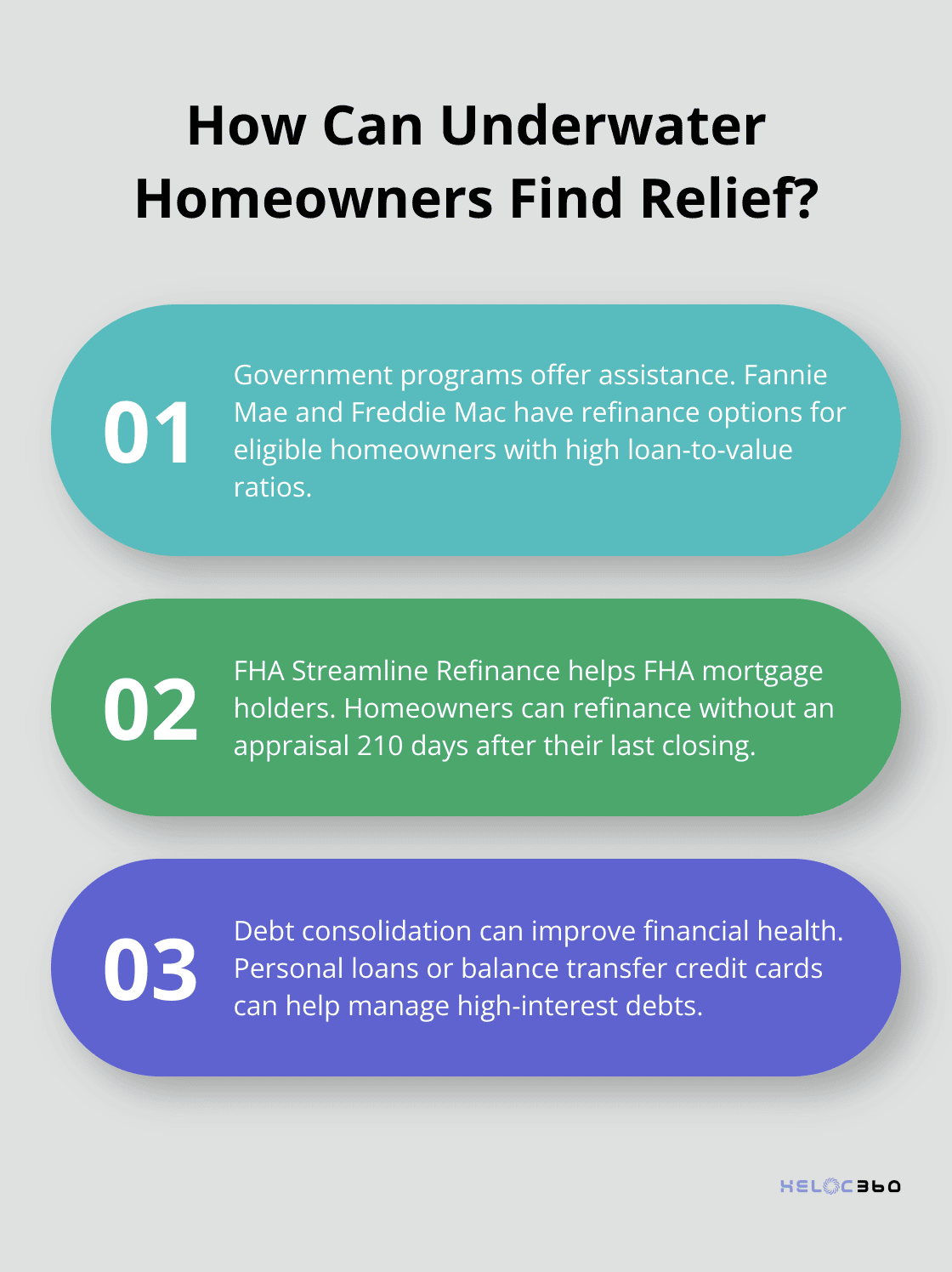

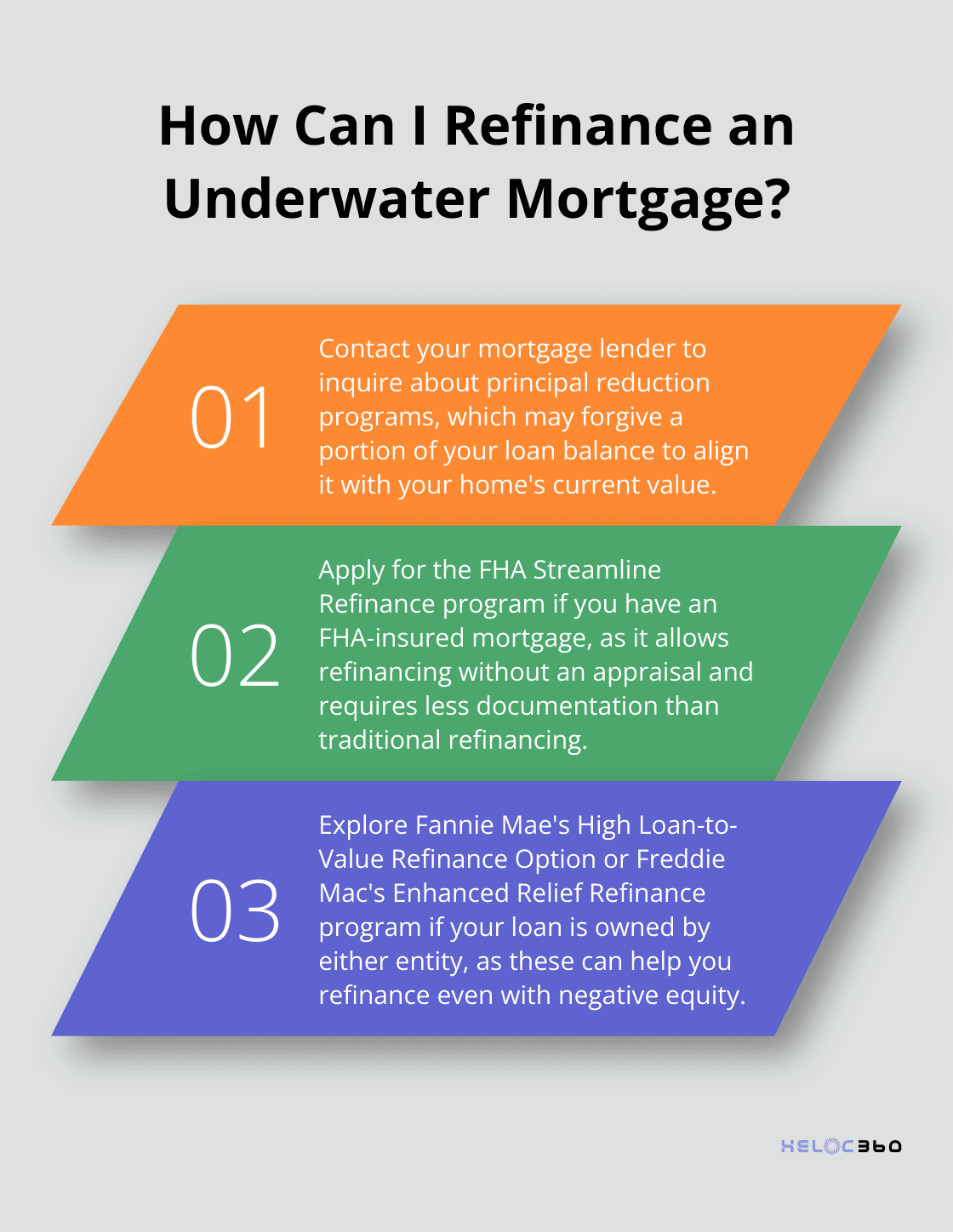

The federal government offers programs to help homeowners with underwater mortgages. Although the Home Affordable Refinance Program (HARP) ended in 2018, new initiatives have taken its place. Fannie Mae's High Loan-to-Value Refinance Option and Freddie Mac's Enhanced Relief Refinance program can help eligible homeowners refinance their mortgages even if they owe more than their home is worth.

These programs typically require that Fannie Mae or Freddie Mac owns your loan and that you're current on your mortgage payments. While they don't reduce the principal amount owed, they can lower monthly payments and interest rates, providing much-needed financial relief.

FHA Streamline Refinance

For homeowners with FHA-insured mortgages, the FHA Streamline Refinance program offers a potential solution. This option allows you to refinance without an appraisal, making it suitable for underwater homes. The process is typically faster and requires less documentation than traditional refinancing. To qualify, you must be current on your mortgage payments and show that the refinance will result in a tangible benefit (such as a lower interest rate or monthly payment). FHA homeowners are eligible for a Streamline Refinance 210 days after their last closing, meaning you must have made six consecutive mortgage payments.

Debt Consolidation Strategies

While debt consolidation doesn't directly address the underwater mortgage issue, it can improve overall financial health. Personal loans or balance transfer credit cards can consolidate high-interest debts, potentially freeing up cash flow that you can direct towards your mortgage.

A balance transfer card with a 0% introductory APR period could provide temporary relief from credit card debt. However, it's important to create a solid repayment plan before the promotional period ends to avoid accumulating more debt.

Principal Reduction Programs

Some lenders offer principal reduction programs for underwater homeowners. These programs involve the lender agreeing to forgive a portion of the mortgage principal, bringing the loan balance more in line with the home's current value. While not widely available, it's worth asking your lender about such options, especially if you're at risk of default.

Exploring Alternative Financing Options

If traditional refinancing options aren't available, you might consider alternative financing methods. These could include:

- Personal loans (which don't require home equity but may have higher interest rates)

- 401(k) loans (if your plan allows it, though this option comes with risks)

- Cash-out refinancing (if you have some equity but are still underwater)

It's important to weigh the pros and cons of each option carefully. Consider consulting with a financial advisor to determine the best course of action for your specific situation.

Final Thoughts

Obtaining a HELOC on an underwater home presents significant challenges due to lender risk assessments and strict loan-to-value requirements. Underwater homeowners should explore alternative options such as government assistance programs, FHA Streamline Refinancing, or debt consolidation strategies. Some lenders offer principal reduction programs, while personal loans or 401(k) loans might provide viable alternatives depending on individual circumstances.

We at HELOC360 understand the complexities of managing home equity in challenging situations like underwater mortgages. Our platform helps homeowners unlock their home's potential by providing comprehensive solutions tailored to various financial goals. Although a HELOC might not work for underwater homes, we can guide you through other options that align with your unique needs.

Every homeowner's situation differs, so it's important to seek expert advice and evaluate all options before making decisions. HELOC360 provides the tools and resources you need to navigate these complex waters and move towards a more stable financial position. With the right information and support, you can work to improve your financial standing and potentially regain positive equity in your home.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.