Home Equity Lines of Credit (HELOCs) are powerful financial tools, but they’re often misunderstood. At HELOC360, we’ve noticed that many homeowners hesitate to explore HELOCs due to common misconceptions.

In this post, we’ll tackle some prevalent HELOC myths head-on, providing you with accurate information to make informed decisions about your home’s equity.

Are HELOCs Limited to Home Improvements?

Versatility Beyond Home Renovations

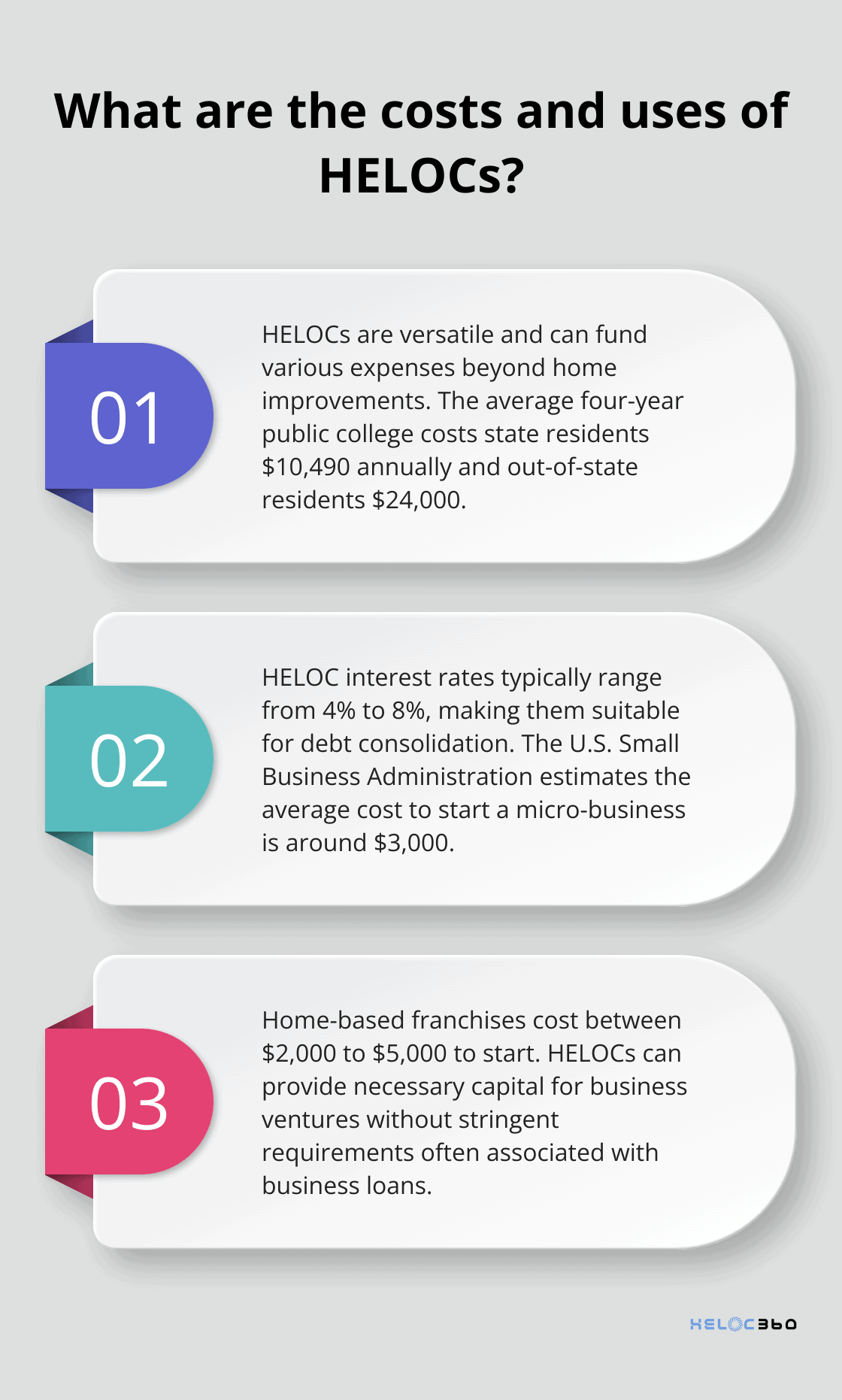

Many homeowners believe that Home Equity Lines of Credit (HELOCs) serve only for funding home improvements. This misconception often stops people from using their home’s equity for other valuable purposes. HELOCs offer remarkable flexibility and can address a wide range of financial needs.

Funding Higher Education

HELOCs can be a smart choice for various life expenses, including higher education. The average four-year public college or university costs state residents roughly $10,490 a year and out-of-state residents $24,000. A HELOC can help cover these substantial costs while potentially offering lower interest rates than traditional student loans.

Smart Debt Consolidation

HELOCs excel at debt consolidation. In contrast, HELOC rates typically range from 4% to 8% (depending on various factors). This significant difference means that using a HELOC to pay off high-interest debt could save thousands in interest payments over time.

Launching Business Ventures

Entrepreneurs often turn to HELOCs to fund their business ventures. The U.S. Small Business Administration estimates that the average cost to start a micro-business is around $3,000, while most home-based franchises cost $2,000 to $5,000. A HELOC can provide the necessary capital without the stringent requirements often associated with business loans.

The Importance of Responsible Usage

While HELOCs offer versatility, you must use them responsibly. Always consider the long-term implications of borrowing against your home equity. Evaluate your ability to repay the loan and ensure that the purpose aligns with your overall financial goals.

Homeowners use their HELOCs creatively and responsibly for various purposes beyond home improvements. From funding dream vacations to covering unexpected medical expenses, the applications are diverse. The key is to approach HELOC usage strategically, always keeping your long-term financial health in mind.

Now that we’ve explored the versatility of HELOCs, let’s address another common misconception: the belief that HELOCs always come with high interest rates.

Are HELOC Interest Rates Always High?

HELOC Rates vs. Other Loan Types

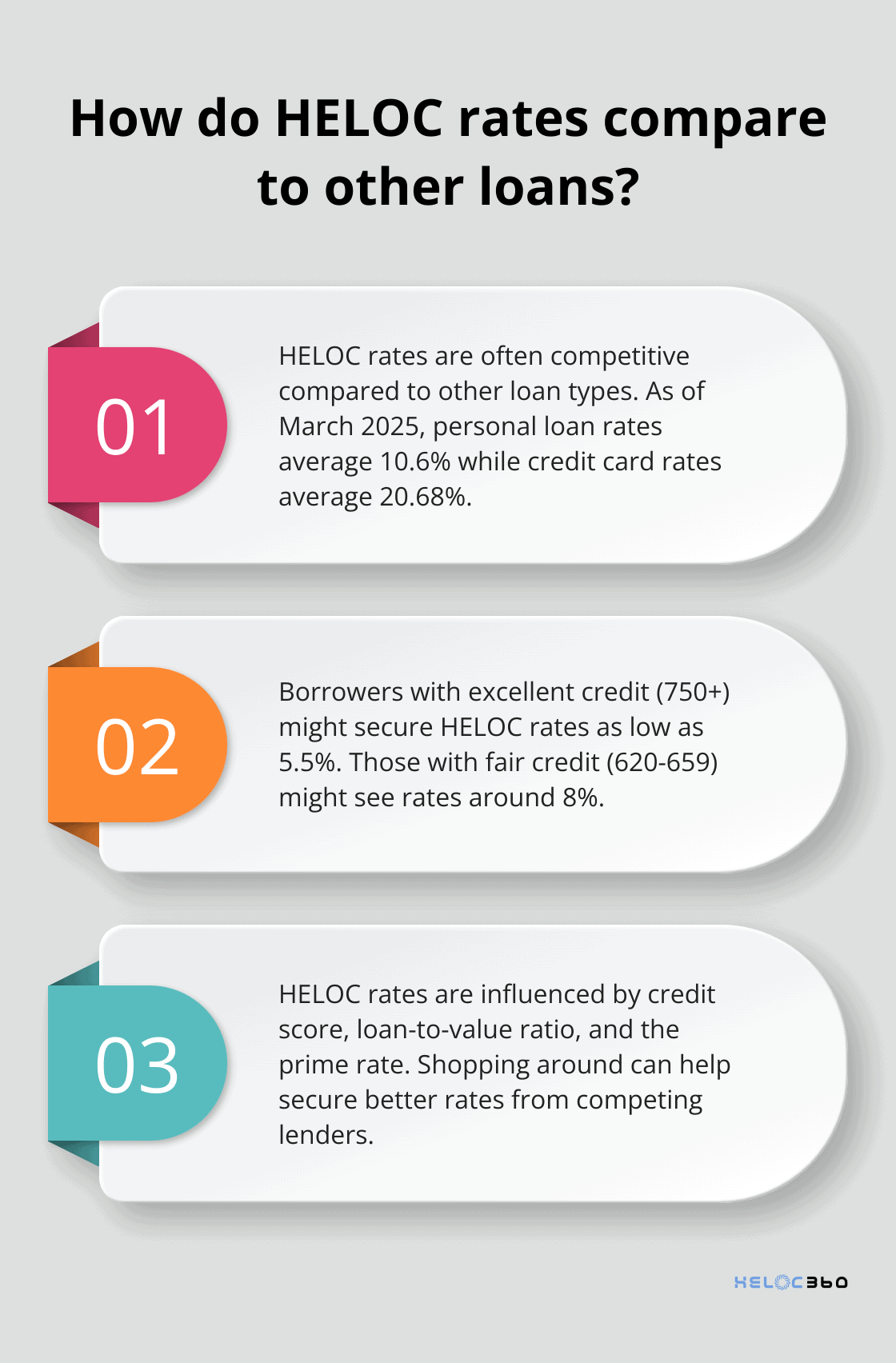

Home Equity Lines of Credit (HELOCs) don’t always come with sky-high interest rates. HELOCs often offer competitive rates compared to other loan types, making them an attractive option for many homeowners.

The Federal Reserve reports that as of March 2025, there have been no changes to the federal funds rate. In contrast, personal loan rates average around 10.6%, while credit card interest rates soar to an average of 20.68%. This stark difference highlights the potential savings HELOC borrowers can enjoy.

Factors Influencing HELOC Rates

Several factors determine your HELOC interest rate:

- Credit Score: A higher credit score typically leads to lower rates. Borrowers with excellent credit (750+) might secure rates as low as 5.5%, while those with fair credit (620-659) might see rates around 8%.

- Loan-to-Value Ratio (LTV): The amount you borrow compared to your home’s value affects your rate. You can calculate LTV by dividing your current loan balance by the current appraised value of your home.

- Prime Rate: HELOC rates often tie to the prime rate. When the prime rate is low, HELOC rates tend to be more attractive.

- Lender Competition: Shopping around can yield better rates. Comparing offers from multiple lenders increases your chances of securing a competitive rate.

Tax Advantages of HELOCs

HELOCs may offer tax benefits, potentially lowering your effective borrowing cost. The Tax Cuts and Jobs Act of 2017 allows interest deductions on HELOCs used for home improvements. For example, if you use your HELOC to add a new room to your house, you may deduct the interest on your taxes (effectively reducing your borrowing costs).

However, it’s important to consult with a tax professional to understand how these deductions apply to your specific situation. Tax laws can change over time, so staying informed is key to maximizing potential benefits.

The Impact of Economic Conditions

Economic conditions play a significant role in HELOC interest rates. During periods of economic growth, the Federal Reserve might increase interest rates to control inflation. This action can lead to higher HELOC rates. Conversely, during economic downturns, the Fed might lower rates to stimulate borrowing and spending, potentially resulting in more favorable HELOC rates.

Understanding these economic factors can help you time your HELOC application for potentially better rates. However, predicting economic trends with certainty is challenging, so it’s essential to focus on your current financial needs and goals when considering a HELOC.

Now that we’ve dispelled the myth of universally high HELOC interest rates, let’s address another common concern: the perceived risks associated with accessing home equity.

Is Accessing Home Equity Truly Risky?

Understanding Responsible Borrowing

Many homeowners avoid tapping into their home equity due to perceived risks. However, when used responsibly, accessing your home’s equity through a HELOC can become a strategic financial move. The key lies in borrowing within your means. Financial experts recommend that your debt-to-income ratio (DTI) should ideally be 36% or below for mortgage approval, with ratios above 50% making approval difficult.

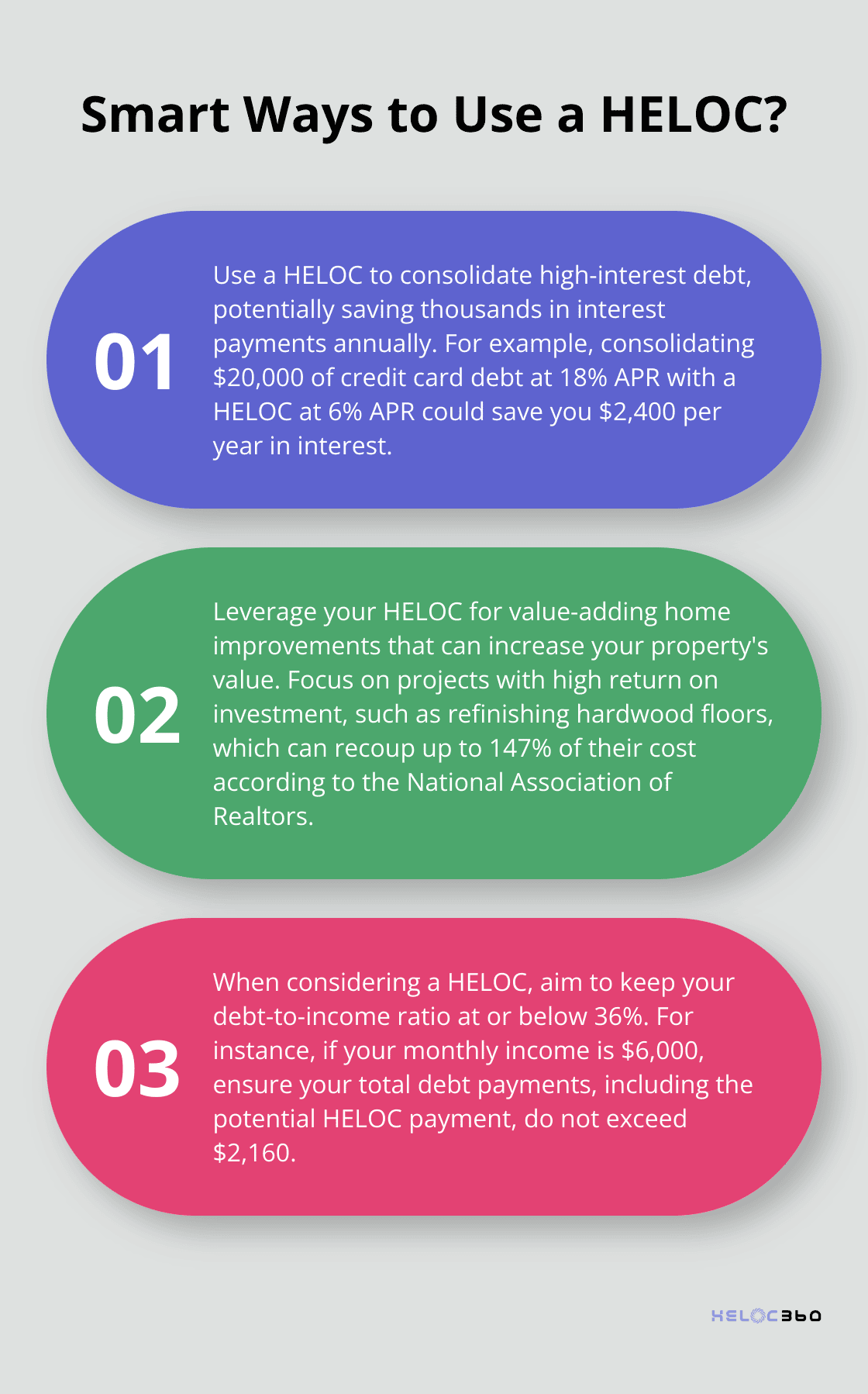

For example, if your monthly income is $6,000, your total debt payments (including your potential HELOC payment) should not exceed $2,160 for an ideal DTI of 36%. Adherence to this principle allows you to leverage your home’s equity without jeopardizing your financial stability.

HELOCs as Strategic Financial Tools

HELOCs can serve as powerful instruments for wealth building when used strategically. For instance, using a HELOC to fund home improvements can increase your property’s value. The National Association of Realtors reports that refinishing hardwood floors can recoup up to 147% of their cost, while installing new wood flooring can recover up to 118%.

Another strategic use involves debt consolidation. If you carry high-interest credit card debt, using a HELOC to pay it off can save you thousands in interest. Consider this scenario: you have $20,000 in credit card debt at 18% APR, which means you pay $3,600 in interest annually. By consolidating this debt with a HELOC at 6% APR, you could reduce your yearly interest to $1,200, saving $2,400 per year.

Best Practices for HELOC Usage

To use a HELOC responsibly, consider these best practices:

- Create a repayment plan before borrowing. Know exactly how you’ll repay the funds you draw.

- Use the funds for value-adding purposes. Avoid using a HELOC for discretionary spending like vacations or luxury items.

- Keep a close eye on interest rates. HELOCs have variable rates, but some lenders offer options to switch between variable and fixed rates.

- Don’t treat your home equity like an ATM. Your home’s equity represents a valuable asset, not a source for frivolous spending.

- Set up automatic payments to ensure you never miss a payment.

Mitigating Risks with Expert Guidance

Platforms designed to guide homeowners through the HELOC process can provide valuable insights and connect you with lenders that offer terms suited to your financial situation. This expert guidance further reduces the perceived risks of accessing your home equity.

Final Thoughts

This article has addressed several HELOC myths, showcasing their versatility beyond home improvements and their often competitive interest rates. We have also explained how responsible use of home equity can be a strategic financial move rather than a risky endeavor. These insights help homeowners make informed decisions about leveraging their home’s equity as a powerful financial tool.

Platforms like HELOC360 exist to simplify the complex world of HELOCs. We offer expert guidance and connect homeowners with lenders that match their unique needs. Our goal is to provide comprehensive information and personalized solutions, empowering homeowners to confidently use their home’s equity.

HELOCs can be valuable financial instruments when used wisely. Staying informed and seeking expert advice allows you to harness the power of your home’s equity to achieve your financial goals. Don’t let misconceptions about HELOCs prevent you from exploring this flexible financing option.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.