HELOC or Home Equity Loan Which Fits Your Lifestyle?

Table of Contents

Choosing between a HELOC and a home equity loan can be a game-changer for your financial future.

At HELOC360, we understand that your lifestyle and financial goals play a crucial role in this decision.

This guide will break down the key differences between HELOC vs HELOAN, helping you determine which option aligns best with your unique situation.

What Are HELOCs and Home Equity Loans?

HELOCs and home equity loans offer two distinct ways to access your home's equity. Each option has unique features that cater to different financial needs and lifestyles. Let's explore these options to help you determine which aligns best with your situation.

Home Equity Loans: The Lump Sum Solution

A home equity loan provides a one-time lump sum of money. You repay this loan in fixed monthly installments over a set term (typically 5 to 30 years). The interest rate usually remains fixed, ensuring consistent payments throughout the loan term.

Home equity loans excel for large, one-time expenses. If you plan a major home renovation with a clear budget, a home equity loan could serve you well. You'll know exactly how much you're borrowing and what your monthly payments will be.

HELOCs: Flexible Borrowing Power

A Home Equity Line of Credit (HELOC) functions more like a credit card. You receive approval for a maximum credit limit and can borrow as much or as little as you need, when you need it, during the draw period (usually 10 years).

HELOCs typically feature variable interest rates, which means your payments can change based on market conditions. During the draw period, you might only need to make interest payments on the amount you've borrowed.

HELOCs prove particularly useful when you need ongoing access to funds or aren't certain about the total amount you'll require. They suit long-term projects with uncertain costs or create a financial safety net.

Key Differences to Consider

The primary distinction between these options lies in flexibility versus predictability. HELOCs may be better for lower interest rates - at least in the short-term, while home equity loans might be preferable if you're thinking long-term.

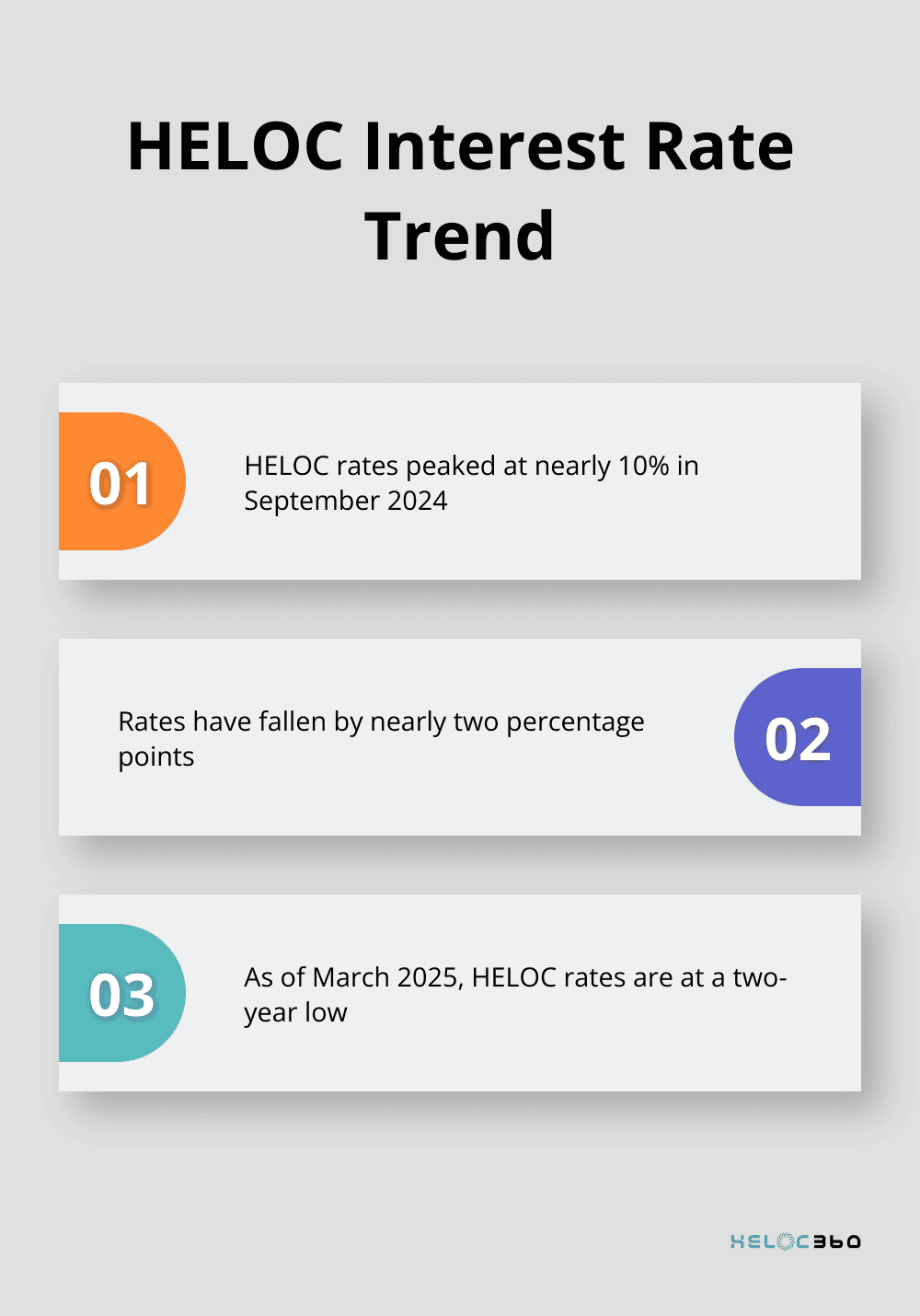

From a near-10-percent peak in September 2024, average HELOC rates have fallen nearly two percentage points and are at a two-year low as of March 2025.

Borrowers who choose HELOCs often save money in the long run because they only pay interest on the amount they actually use. Those who opt for home equity loans appreciate the discipline of fixed payments and the ability to lock in rates when they're low.

Both options use your home as collateral, which results in lower interest rates compared to unsecured loans. However, this also means your home is at risk if you miss payments or owe more than your home's worth. Always consider your long-term financial stability before choosing either option.

As we move forward, let's examine the factors you should weigh when deciding between a HELOC and a home equity loan. Your financial goals, current market conditions, and personal financial situation all play crucial roles in making the right choice.

What Shapes Your HELOC vs Home Equity Loan Decision?

Financial Goals and Borrowing Needs

Your borrowing purpose impacts which option suits you best. Home equity loans and HELOCs use home equity as collateral to lend you money. Equity loans offer lump sum cash while HELOCs offer a line of credit. For a one-time, large expense with a clear budget (like a major home renovation), a home equity loan might be your best choice. You'll receive a lump sum and benefit from fixed monthly payments, which simplifies budgeting.

For ongoing or uncertain expenses, a HELOC offers more flexibility. If you're starting a business or funding a child's education over several years, a HELOC allows you to borrow as needed, potentially reducing interest costs.

Interest Rate Environment

The current interest rate landscape can influence your decision. Average HELOC rates are currently around 8%, which is higher than current average mortgage rates. However, you must consider future rate projections.

If rates are expected to increase, locking in a fixed rate with a home equity loan could save you money long-term. If rates are projected to remain stable or decrease, a HELOC's variable rate might work in your favor.

Your Credit Score and Financial Health

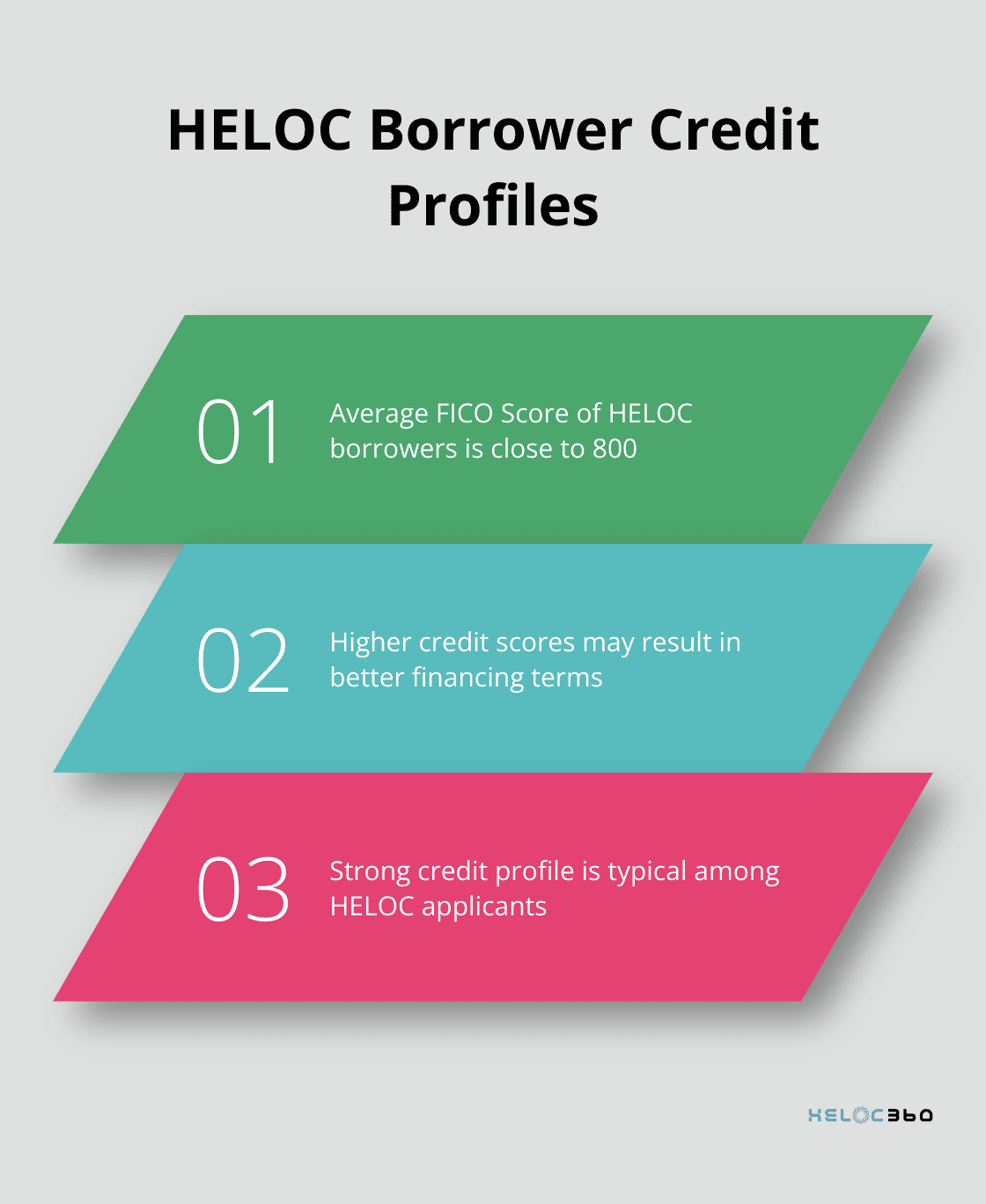

Your credit score significantly affects the interest rates you'll qualify for. Better scores may result in even better financing terms. Indeed, the average FICO® Score among HELOC borrowers in most states is close to 800.

A lower credit score might result in higher interest rates. In this case, a home equity loan's fixed rate could provide more stability and predictability in your monthly budget.

Your debt-to-income (DTI) ratio also plays a key role. A high DTI might affect your ability to qualify for either option, as lenders may view you as a riskier borrower.

Managing Variable Interest Rates

Your comfort level with financial uncertainty is a key consideration. HELOCs typically come with variable interest rates, which can fluctuate based on market conditions.

If you're on a fixed income or prefer consistent monthly payments, a home equity loan's fixed rate might be more suitable. However, if you're comfortable with potential payment changes and believe you can benefit from possible rate decreases, a HELOC could be advantageous.

Some HELOC lenders offer the option to convert a portion of your balance to a fixed rate, providing a middle ground between flexibility and predictability.

Now that we've explored the factors that shape your decision, let's examine how these options fit into different lifestyle scenarios and financial goals.

Which Option Fits Your Financial Goals?

Home Renovations and Improvements

Your choice between a HELOC and a home equity loan for home renovations depends on the project's nature. A HELOC works well for ongoing renovations or projects with uncertain costs. You can draw funds as needed, which potentially saves on interest. For a kitchen remodel in stages, a HELOC allows you to borrow only what you need at each phase.

For a one-time, large-scale renovation with a fixed budget, a home equity loan might suit you better. It provides a lump sum and fixed monthly payments, which makes it easier to budget for your project.

Debt Consolidation

Both options can effectively consolidate high-interest debt, but a home equity loan often proves more advantageous. The fixed interest rate and consistent monthly payments make it easier to plan your debt payoff strategy. Taking out a home equity line of credit just got more affordable, which could make it an attractive option for debt consolidation.

If you need to consolidate variable amounts of debt over time, a HELOC's flexibility might benefit you more. You can pay off debts as they arise and only pay interest on the amount you use.

Education Expenses

For education expenses, a HELOC often proves more advantageous. College costs can vary year to year, and a HELOC allows you to borrow only what you need each semester. This flexibility can lead to significant savings compared to taking out a larger lump sum with a home equity loan.

Home equity financing offers additional options to pay for college, but it's important to note that there is a risk when you use your house as collateral.

Emergency Fund and Financial Flexibility

A HELOC serves as an excellent backup emergency fund. It provides quick access to funds without the obligation to borrow until needed. This flexibility can save you financially during unexpected events like job loss or medical emergencies.

However, you must resist the temptation to tap into this fund for non-emergencies. Try to treat your HELOC emergency fund like any other - use it only when absolutely necessary.

Business Startup or Expansion

For entrepreneurs, a HELOC often proves more beneficial than a home equity loan. Business needs can be unpredictable, and a HELOC's flexibility allows you to adapt to changing circumstances. You can draw funds as needed for inventory, equipment, or operating expenses.

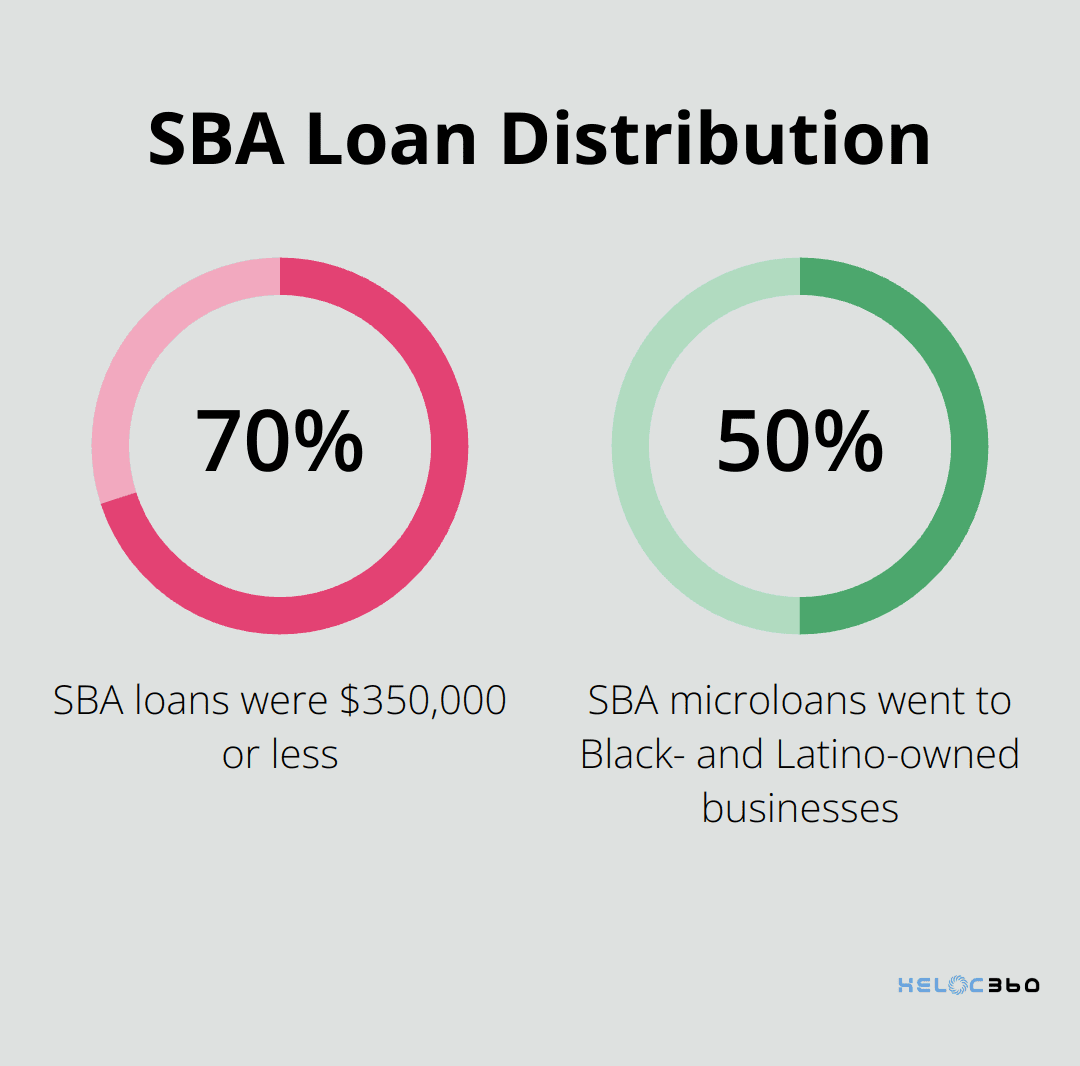

According to a recent report, nearly 70% of SBA loans were $350,000 or less, and 50% of SBA microloans went to Black- and Latino-owned businesses. This indicates that smaller, flexible loans are popular among small businesses, which aligns with the advantages of using a HELOC for business purposes.

Final Thoughts

Your choice between a HELOC and a home equity loan depends on your financial situation and goals. HELOCs offer flexibility with variable rates and ongoing access to funds, while home equity loans provide stability with fixed rates and lump-sum payouts. Your decision in the HELOC vs HELOAN debate should align with your financial objectives, risk tolerance, and current market conditions.

Consider factors like your credit score, debt-to-income ratio, and comfort with potential interest rate fluctuations. Both options use your home as collateral, so you must borrow responsibly. At HELOC360, we understand that navigating these choices can be complex.

We've developed a platform to simplify the process and connect you with lenders that match your specific needs. Our expert guidance helps you make informed decisions about leveraging your home equity (whether for renovations, debt consolidation, or creating financial flexibility). HELOC360 empowers you to unlock your home's full potential, turning your property's value into a pathway for achieving your financial aspirations.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.