HELOCs in Retirement Smart Move or Risky Bet?

Table of Contents

Retirement brings new financial challenges, and many retirees are exploring HELOCs as a potential solution. At HELOC360, we've seen an increasing number of seniors considering this option to tap into their home equity.

But is a HELOC in retirement a smart move or a risky bet? Let's examine the pros and cons to help you make an informed decision about your financial future.

How Do HELOCs Work in Retirement?

Understanding HELOCs for Retirees

A Home Equity Line of Credit (HELOC) allows homeowners to borrow, spend, and repay as they go, using their home as collateral. For retirees, HELOCs offer a flexible source of funds to supplement retirement income or cover unexpected expenses.

HELOCs function similarly to credit cards, but with your home as collateral. Lenders approve you for a credit limit based on your home's value and outstanding mortgage balance. The HELOC lifecycle consists of two phases: the draw period (typically 10 years) and the repayment period.

Why Retirees Choose HELOCs

Retirees often turn to HELOCs for their flexibility and potentially lower interest rates compared to other borrowing options. HELOCs can fund various needs, such as home improvements, medical expenses, or serve as a financial cushion for emergencies.

HELOCs can be a powerful tool as you age, allowing you to make your home more accessible, repair or improve your house, or pay off higher-interest debt.

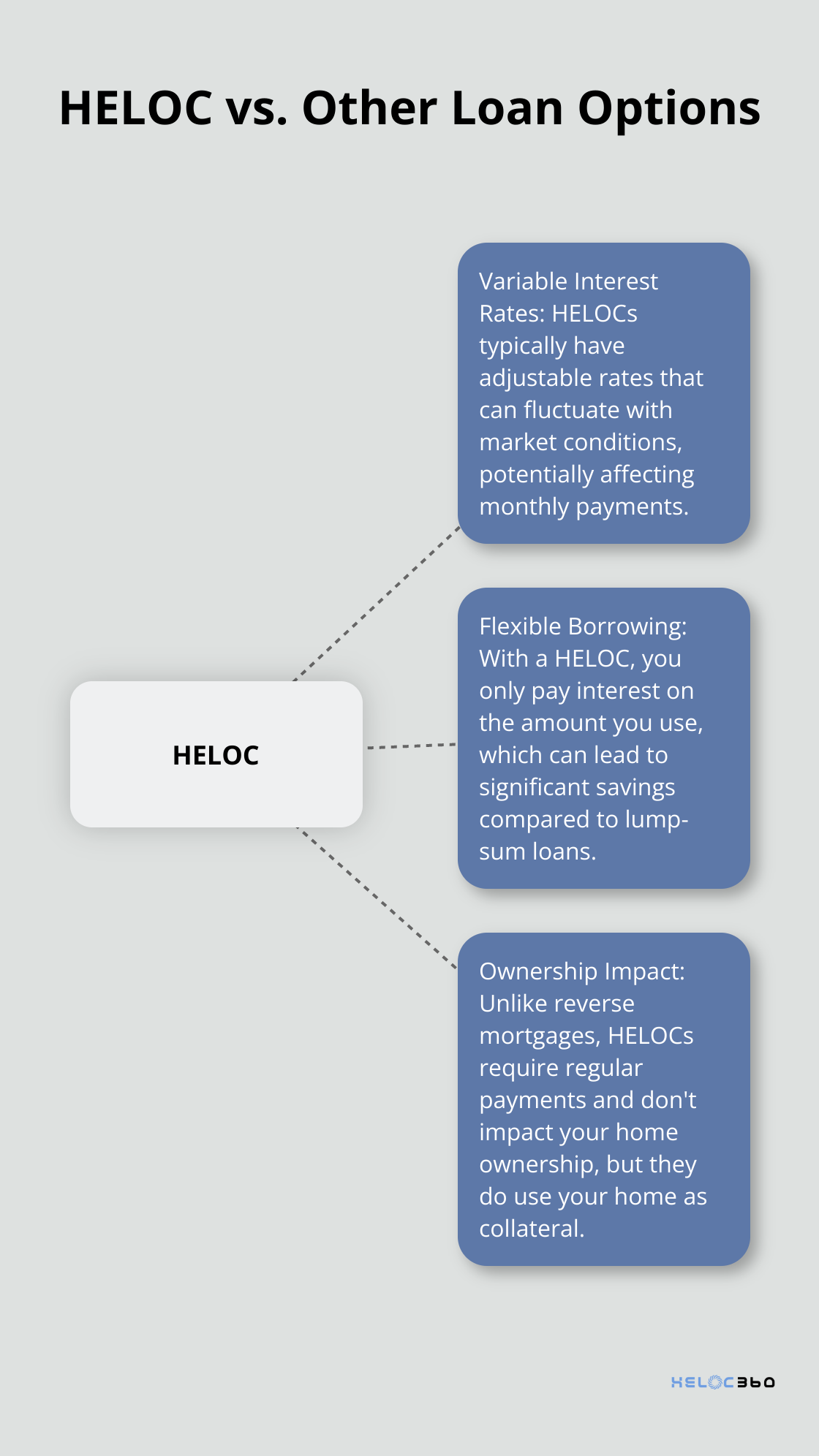

HELOCs vs. Alternative Loan Options

HELOCs differ from traditional loans in several key ways:

- Variable Interest Rates: Unlike fixed-rate home equity loans, HELOCs typically have variable interest rates. This means your payments can fluctuate based on market conditions.

- Flexible Borrowing: With a HELOC, you only pay interest on the amount you use, which can lead to significant savings compared to lump-sum loans.

- Ownership Impact: Compared to reverse mortgages (another popular option for seniors), HELOCs require regular payments and don't impact your home ownership. However, reverse mortgages don't require repayment until you sell the home or pass away.

Risks and Considerations

While HELOCs provide financial flexibility, they also come with risks. Your home serves as collateral, meaning defaulting on payments could lead to foreclosure. Always consider your long-term financial situation and ability to repay before taking out a HELOC in retirement.

As we move forward, let's explore the potential benefits that HELOCs can offer to retirees, including access to funds for unexpected expenses and the ability to leverage home equity without selling.

Unlocking Home Equity Benefits for Retirees

Accessing Home Equity Without Selling

Retirees often find themselves in a unique financial position. They may have significant equity in their homes but limited liquid assets. A Home Equity Line of Credit (HELOC) can transform this situation. HELOCs allow homeowners 62 and over to convert part of their home's equity into cash without monthly loan payments. This means retirees can stay in their homes while still benefiting from the wealth they've built up over the years.

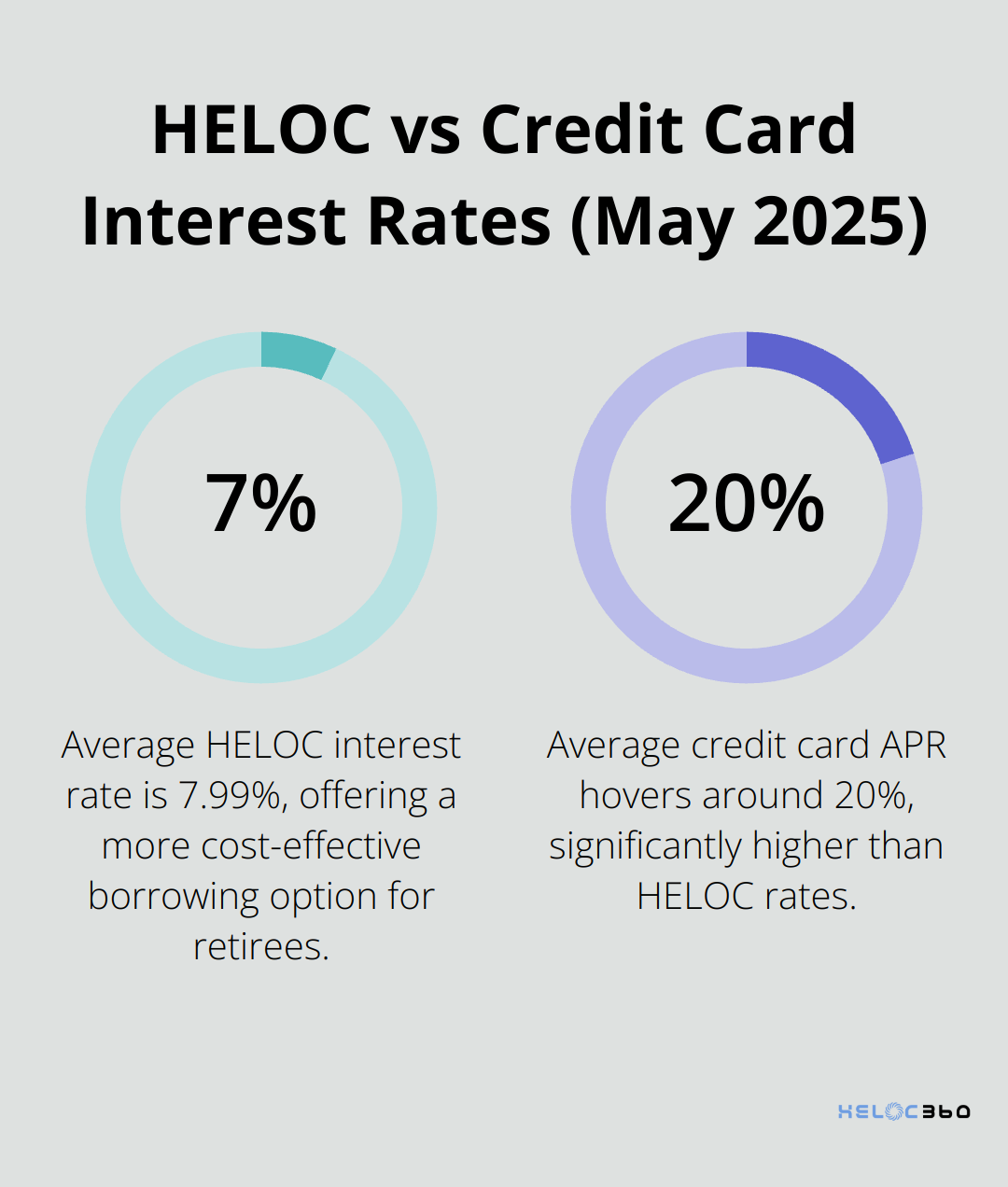

Cost-Effective Borrowing Option

HELOCs typically offer lower interest rates compared to credit cards or personal loans. As of May 7, 2025, the national average HELOC interest rate is 7.99%, according to Bankrate's latest survey of the nation's largest home equity lenders. This rate is significantly lower than the average credit card APR (which hovers around 20%).

For a retiree needing to borrow $50,000, choosing a HELOC over a credit card could save thousands in interest over the life of the loan.

Flexibility for Unexpected Expenses

Retirement often comes with unforeseen costs, from medical emergencies to home repairs. A HELOC provides a financial safety net, allowing retirees to access funds as needed. Unlike a lump-sum loan, you only pay interest on the amount you use. This flexibility can prove invaluable for managing cash flow in retirement.

Consider a scenario where a retiree faces an unexpected $15,000 medical bill. They can draw from their HELOC to cover the expense without disrupting their regular retirement income or liquidating investments at an inopportune time.

Tax Advantages

HELOCs may offer potential tax benefits for retirees. The interest paid on a home equity loan or a home equity line of credit (HELOC) might be tax-deductible (consult with a tax professional for specific advice). This advantage can further reduce the effective cost of borrowing for retirees who use their HELOC for home renovations or upgrades.

Investment Opportunities

Some retirees use HELOCs as a tool for investment. By accessing low-interest funds through a HELOC, they can invest in potentially higher-yielding assets. However, this strategy carries risks and should only be considered after thorough analysis and consultation with financial advisors.

While HELOCs offer retirees a powerful tool to enhance their financial flexibility and security, it's important to approach this option with a clear understanding of the associated risks and responsibilities. The next section will explore the potential drawbacks and considerations retirees should keep in mind when contemplating a HELOC.

Navigating HELOC Risks in Retirement

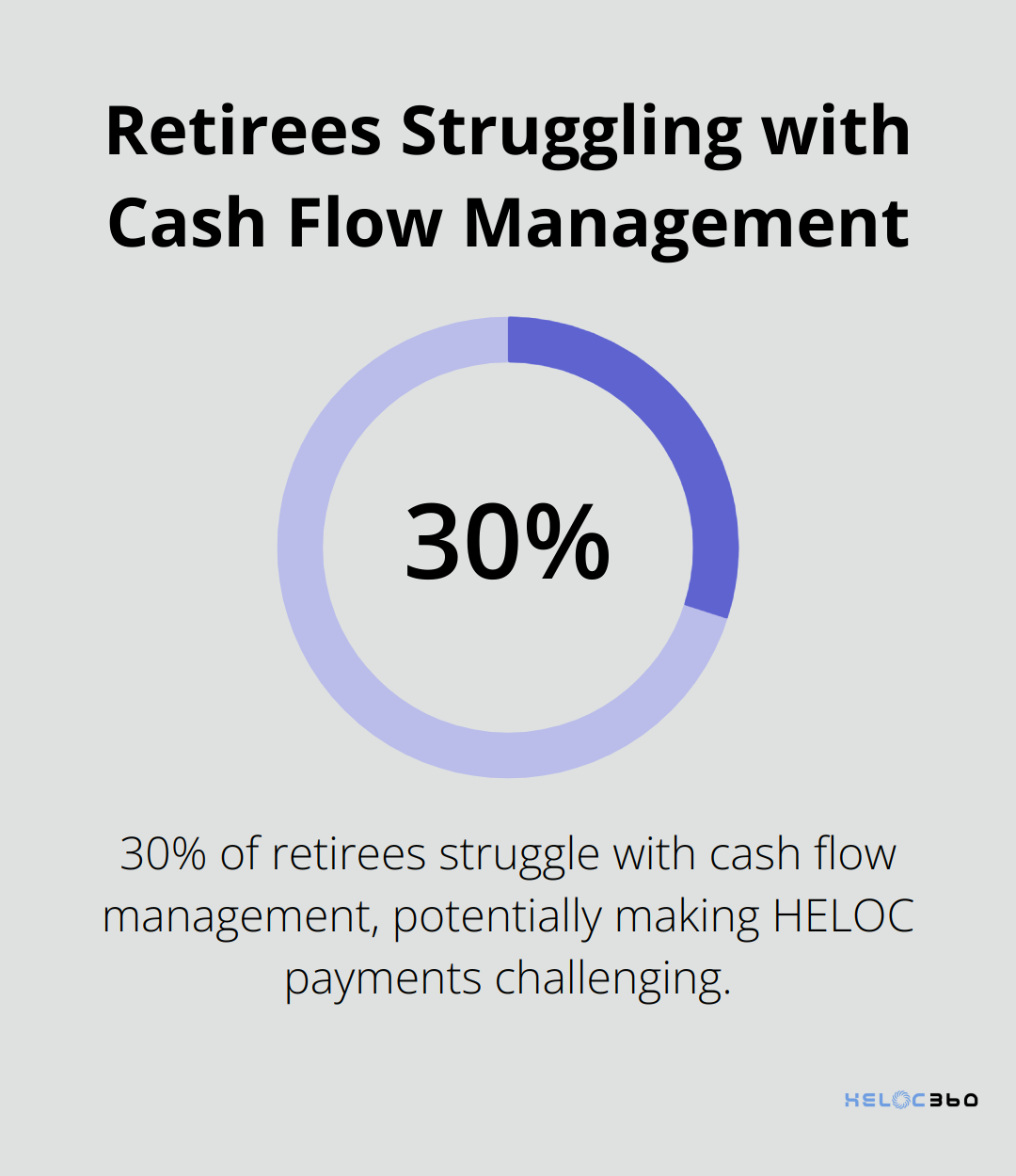

The Cash Flow Challenge

Retirees who consider a Home Equity Line of Credit (HELOC) must evaluate the potential risks against the benefits. HELOCs provide financial flexibility but also present significant considerations that could affect retirement security.

One primary concern for retirees using a HELOC is its impact on cash flow. A study by the Urban Institute reveals that 30% of retirees struggle with cash flow management. HELOC payments added to monthly expenses can worsen this issue.

For example, a $100,000 loan at a 7% interest rate results in a monthly interest-only payment of about $583 during the draw period. This amount increases substantially when principal payments begin in the repayment period.

To address this risk, create a detailed budget that includes HELOC payments alongside regular retirement expenses. Include potential increases in healthcare costs (the Fidelree Health Care Cost Estimate projects $315,000 for a couple retiring in 2025).

The Risk of Foreclosure

The most significant risk of a HELOC is the potential for foreclosure if payments are not met. Home equity contracts can be risky, with homeowners receiving cash upfront in exchange for future repayment. This arrangement can potentially lead to foreclosure if not managed carefully.

To protect yourself, establish an emergency fund that covers at least six months of HELOC payments. Explore options for HELOCs with flexible payment terms or the ability to convert to a fixed-rate loan, which can provide more predictable payments.

Market Volatility and Variable Rates

HELOCs typically come with variable interest rates, which makes them susceptible to market fluctuations. The Federal Reserve's actions can significantly impact these rates. In 2024, HELOC rates ranged from 6.5% to 9%, depending on market conditions.

To safeguard against rate hikes, consider a HELOC with a rate cap, which limits how high your interest rate can go. Some lenders offer this feature (potentially saving you thousands over the life of the loan).

Estate Planning Implications

A HELOC can affect your estate planning strategy. An outstanding HELOC balance becomes a liability against your estate if you pass away, potentially reducing the inheritance you leave to your heirs.

To address this, consider purchasing a term life insurance policy that covers the potential outstanding balance of your HELOC. This strategy ensures your heirs won't inherit the debt. Consult with an estate planning attorney to effectively integrate your HELOC into your overall estate plan.

Final Thoughts

HELOCs in retirement offer both opportunities and challenges for retirees. The flexibility and potential cost-effectiveness of HELOCs provide a valuable financial tool, but risks such as variable interest rates and potential foreclosure cannot be ignored. Careful financial planning becomes essential when considering a HELOC during retirement years.

A HELOC might benefit retirees with substantial home equity and stable income to manage payments. It can help cover large, one-time expenses like home renovations or medical bills. However, those with limited income or unstable finances should weigh the risks carefully before proceeding.

HELOC360 offers a platform to help navigate the HELOC process for retirees. The decision to use a HELOC in retirement should stem from a thorough evaluation of your financial situation, goals, and risk tolerance (consult with a financial advisor if needed). HELOC360 aims to provide the tools and information necessary for making informed decisions about leveraging home equity effectively in retirement.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.