Home Equity Line vs Home Equity Loan: Key Distinctions

Table of Contents

Homeowners often face a crucial decision when tapping into their property's value: home equity line vs home equity loan. These two financial tools offer distinct advantages and drawbacks.

At HELOC360, we understand the importance of making an informed choice that aligns with your financial goals. This guide will break down the key differences between HELOCs and home equity loans, helping you navigate your options with confidence.

What Is a Home Equity Line of Credit?

Definition and Structure

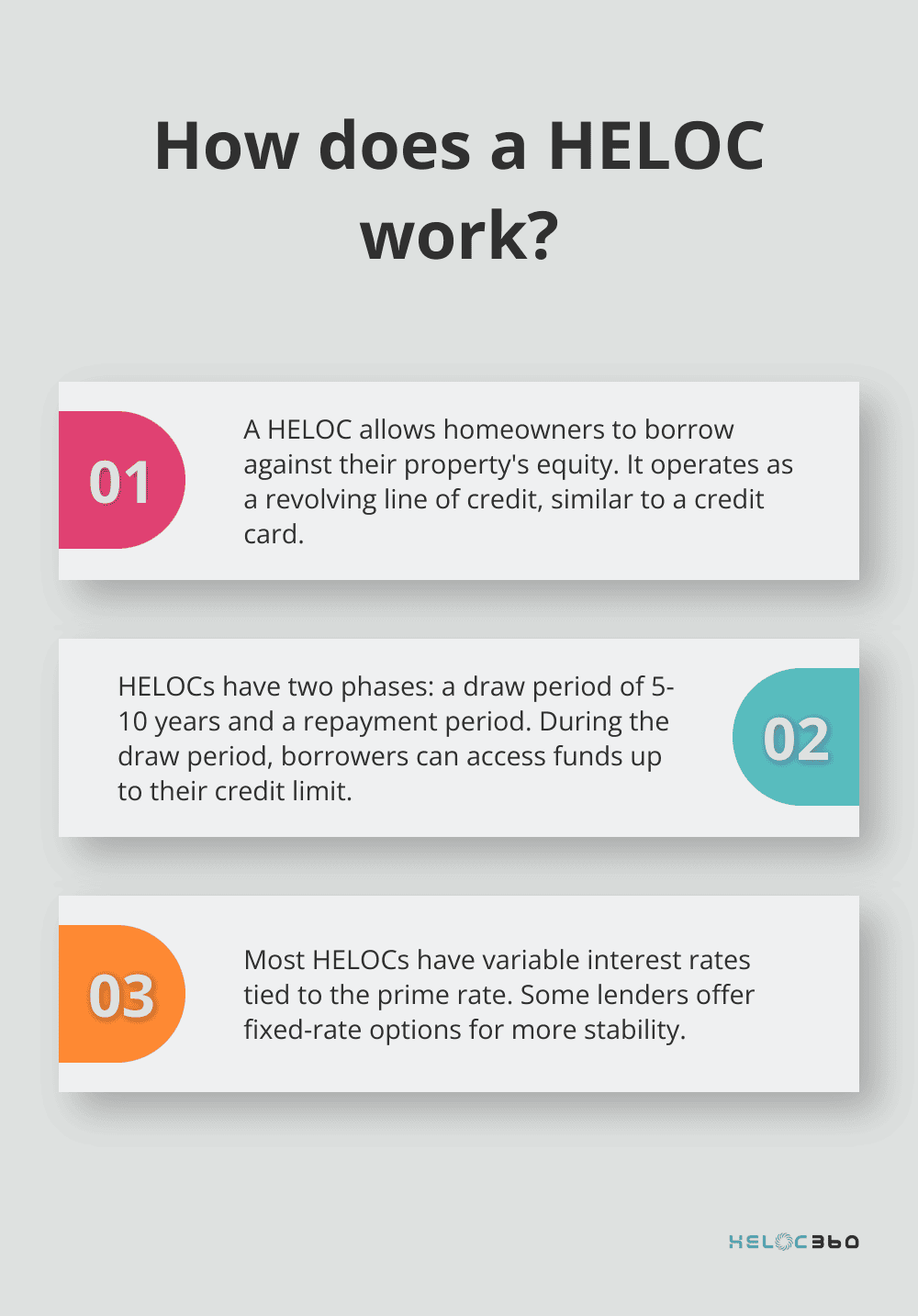

A Home Equity Line of Credit (HELOC) is a financial product that allows homeowners to borrow against their property's equity. Unlike a conventional loan, a HELOC is a revolving line of credit, allowing you to borrow more than once. In that way, it's like a credit card, except with a different collateral structure.

Draw and Repayment Periods

HELOCs operate in two distinct phases:

- Draw Period: This phase typically lasts 5-10 years. During this time, you can borrow up to your credit limit as needed. You'll only pay interest on the amount you've borrowed.

- Repayment Period: Once the draw period ends, you enter this phase. You can no longer borrow and must repay both principal and interest.

Interest Rates and Payment Structures

Most HELOCs feature variable interest rates, often tied to the prime rate. This can result in fluctuating payments over time. Some lenders offer fixed-rate options for those seeking more stability.

During the draw period, you may have the option to make interest-only payments. While this keeps initial costs low, it can lead to higher payments during the repayment phase. It's important to plan for these potential increases.

Flexibility and Uses

The versatility of a HELOC is one of its primary advantages. You can use the funds for various purposes, including:

- Home improvements

- Debt consolidation

- Emergency funds

- Education expenses

- Business startups

This flexibility, however, requires responsible management. It's easy to overspend when you have access to a large credit line. Financial experts recommend creating a clear plan for the funds before opening a HELOC. Responsible borrowing is key, as a HELOC provides access to a line of credit that you can draw from again and again for as long as 10 to 15 years.

Many homeowners have successfully used HELOCs for major renovations, funding education, or even launching businesses. The key to success lies in developing a solid repayment strategy.

As we transition to our next topic, it's important to understand that while HELOCs offer flexibility, they're not the only option for accessing your home's equity. Let's explore another popular choice: the home equity loan.

What Is a Home Equity Loan?

Definition and Structure

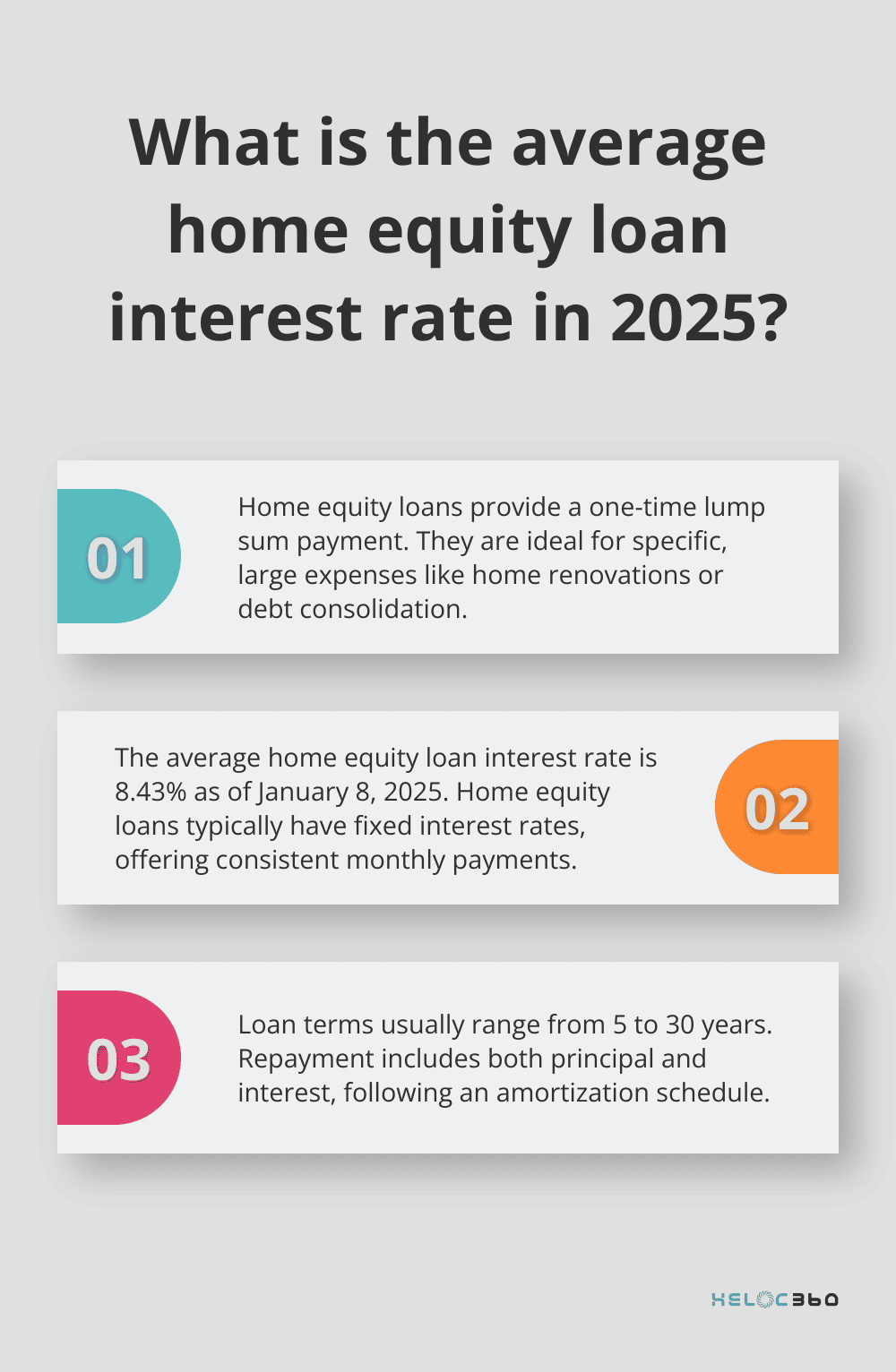

Home equity loans offer a distinct approach to leveraging your property's value. Unlike the revolving credit of a HELOC, a home equity loan provides a one-time lump sum payment. This structure makes it ideal for homeowners with specific, large expenses in mind.

Fixed Rates for Predictable Payments

One of the most attractive features of home equity loans is their fixed interest rates. This means your monthly payments remain consistent throughout the loan term, typically ranging from 5 to 30 years. As of January 8, 2025, the average home equity loan interest rate is 8.43%.

This predictability allows for easier budgeting and long-term financial planning. You'll know exactly how much you owe each month, which can particularly benefit those on fixed incomes or with tight budgets.

Lump Sum Disbursement

When you take out a home equity loan, you receive the entire loan amount upfront. This makes it an excellent option for major, one-time expenses such as:

- Home renovations

- Debt consolidation

- College tuition

- Wedding expenses

Repayment Structure

Home equity loans typically follow a straightforward repayment structure. You'll make regular monthly payments that include both principal and interest. This amortization schedule ensures that you steadily pay down your loan balance over time.

It's worth noting that while home equity loans offer stability, they may have higher interest rates compared to HELOCs (especially during the initial draw period). However, this trade-off often provides peace of mind for borrowers who prefer consistent payments.

Many homeowners successfully use home equity loans to fund significant life events or make substantial home improvements. The key is to have a clear plan for the funds and ensure that the repayment terms align with your long-term financial goals.

As we move forward, it's important to understand how home equity loans compare to HELOCs. Each option has its unique advantages and potential drawbacks, which we'll explore in detail in the next section.

Which Option Fits Your Financial Needs?

Interest Rates and Payment Structures

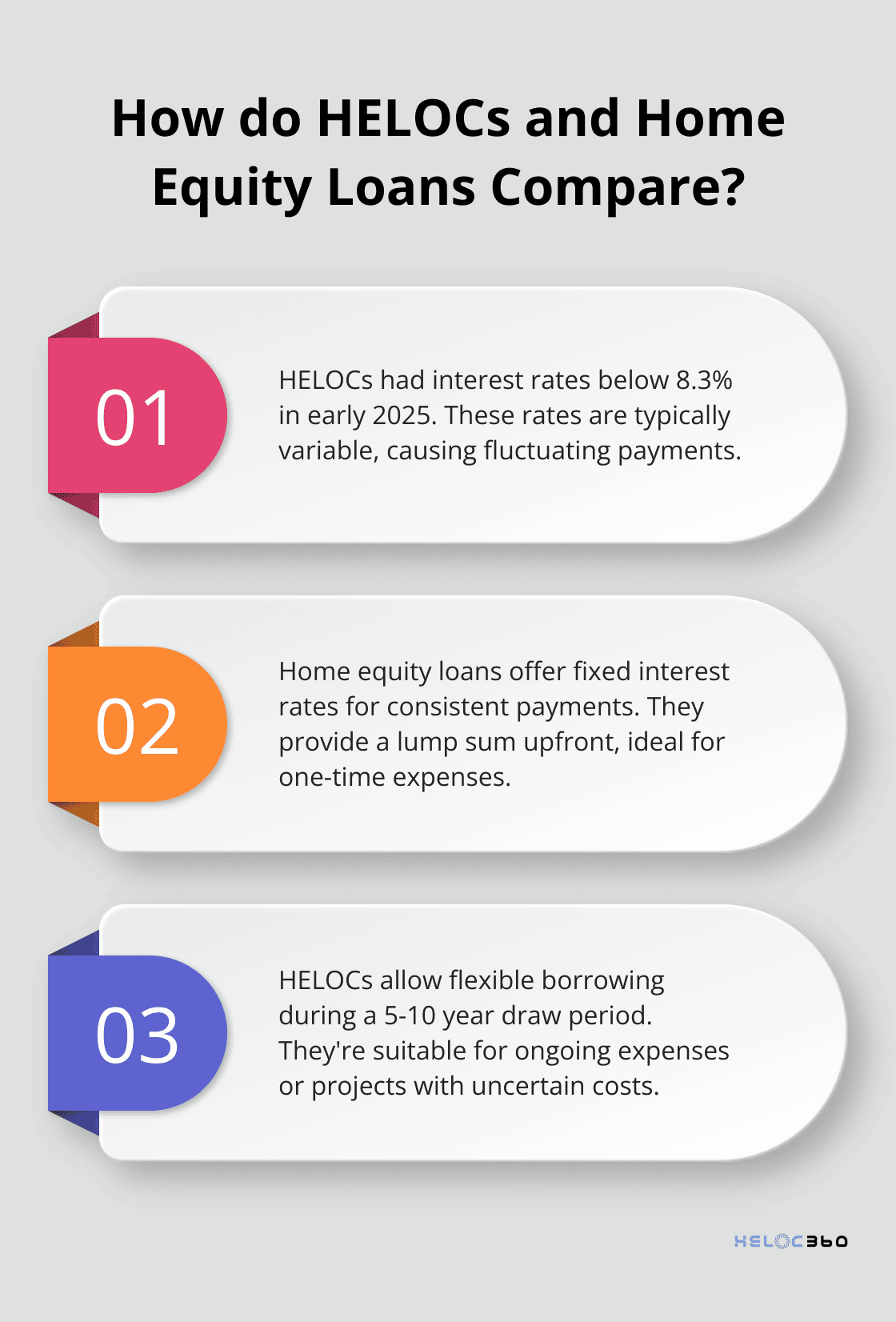

HELOCs dropped below 8.3 percent at the beginning of the year and, along with home equity loans, are forecast to retreat further in 2025. However, these rates are usually variable, which means your payments can fluctuate over time.

Home equity loans provide fixed interest rates. This means your payments remain consistent throughout the loan term, making budgeting easier. If you prefer predictability in your monthly expenses, a home equity loan might be the better choice.

Borrowing Flexibility vs. Predictability

HELOCs offer more flexibility in borrowing. You can draw funds as needed during the draw period (typically 5-10 years). This makes HELOCs ideal for ongoing expenses or projects with uncertain costs.

Home equity loans provide a lump sum upfront. If you have a specific, one-time expense in mind (such as a major home renovation or debt consolidation), this option might be more suitable.

Impact on Credit Scores

Both HELOCs and home equity loans can affect your credit score. It can have a small impact on your credit score when you apply for one, but a larger one if payments are late or missed.

With a HELOC, your credit utilization ratio (the amount of credit you're using compared to your credit limit) can fluctuate as you borrow and repay, potentially causing more variability in your credit score.

Tax Considerations

As of 2025, the interest on both HELOCs and home equity loans may be tax-deductible if you use the funds for home improvements. However, it's important to consult with a tax professional for the most up-to-date information, as tax laws can change.

Matching Your Financial Goals

Consider your long-term financial objectives when choosing between these options. If you plan a series of home improvements over time, a HELOC's flexibility might be advantageous. For a one-time expense with a known cost, like paying for a child's college tuition, a home equity loan could be more appropriate.

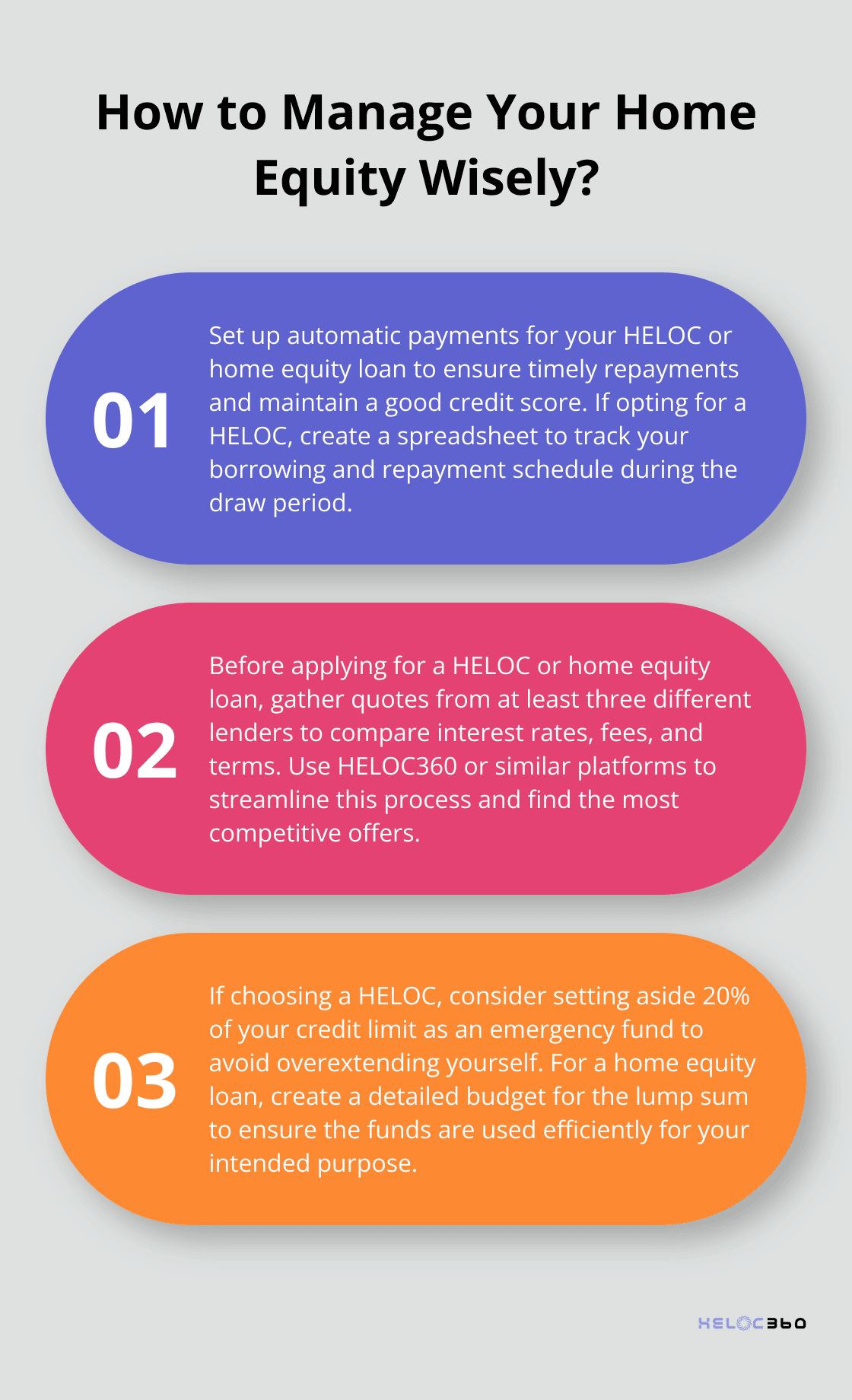

Both options use your home as collateral, so it's essential to have a solid repayment plan in place. If you're unsure which option best suits your needs, platforms like HELOC360 can provide personalized guidance and connect you with suitable lenders, ensuring you make the most of your home's equity while aligning with your financial goals.

Final Thoughts

Your choice between a home equity line of credit and a home equity loan depends on your financial situation and goals. HELOCs provide flexibility with variable rates and revolving credit, while home equity loans offer stability with fixed rates and lump-sum payouts. Your decision should align with your long-term financial objectives, considering factors like interest rates, payment structures, and intended use of funds.

We at HELOC360 understand the complexities of leveraging your home's equity. Our platform simplifies the process, offering expert guidance and connecting you with suitable lenders. Whether you prefer a home equity line vs home equity loan, HELOC360 can help you make an informed decision.

You should assess your financial health, future income prospects, and risk tolerance before making a decision. Consulting with financial advisors or lenders can provide valuable insights tailored to your specific circumstances. Your home's equity is a powerful tool - use it wisely to achieve your goals and secure your financial well-being.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.