Unlocking HELOC Tax Deductions [2025 Guide]

Table of Contents

At HELOC360, we understand that navigating HELOC tax deductions can be complex, especially with recent changes in tax laws.

This guide will help you understand how to maximize your tax benefits from a Home Equity Line of Credit in 2025.

We'll cover qualifying expenses, strategic planning, and best practices for documentation to ensure you're making the most of your HELOC.

How Do HELOC Tax Deductions Work in 2025?

Understanding HELOC Basics

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against their home's equity. In 2025, the tax implications of HELOCs remain a significant consideration for homeowners and investors.

Tax Deduction Fundamentals

The Tax Cuts and Jobs Act of 2017 significantly altered the rules for HELOC interest deductions. As of 2025, HELOC interest qualifies for tax deductions only when the funds are used to buy, build, or substantially improve the home that secures the loan. This restriction means that using your HELOC for personal expenses or debt consolidation disqualifies the interest from deduction.

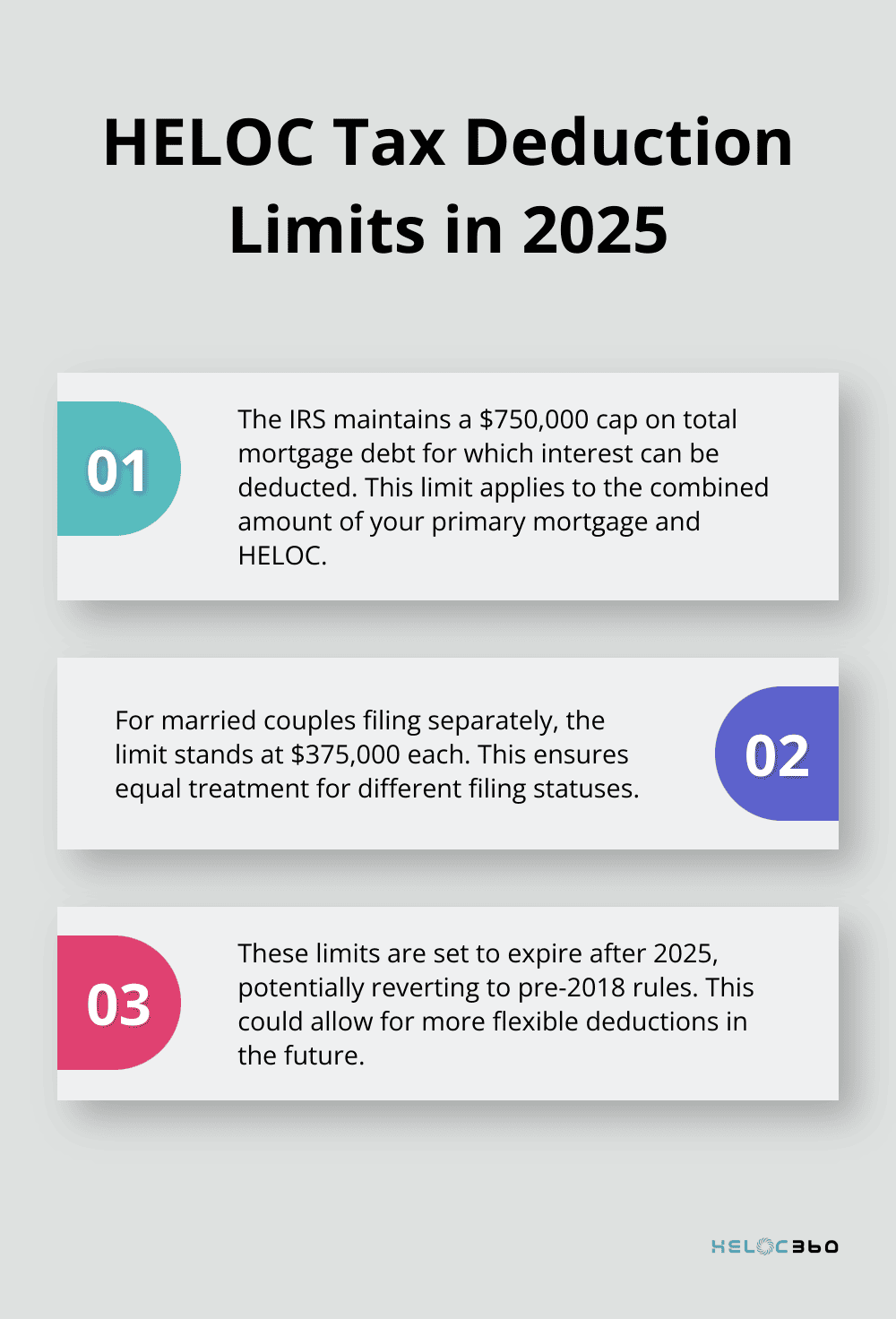

Current Limits on Deductions

The IRS maintains a $750,000 cap on total mortgage debt for which interest can be deducted. This limit applies to the combined amount of your primary mortgage and HELOC. For married couples filing separately, the limit stands at $375,000 each. It's important to note that these limits are set to expire after 2025, potentially reverting to pre-2018 rules (which allowed for more flexible deductions).

Documentation Requirements

Proper documentation plays a vital role in claiming HELOC tax deductions. Homeowners should keep detailed records of HELOC fund usage, including receipts for home improvements or renovations. Lenders provide Form 1098, which shows the mortgage interest of $600 or more received during the year-a necessary document for tax filing.

Professional Guidance

Tax professionals can offer invaluable assistance in navigating the complexities of HELOC tax benefits. They help maximize deductions while ensuring compliance with current tax laws, potentially saving homeowners from costly mistakes.

As we move forward, let's explore the specific expenses that qualify for HELOC tax deductions in 2025, providing you with a clear roadmap for leveraging your home equity effectively.

What Expenses Qualify for HELOC Tax Deductions?

Home Improvements and Renovations

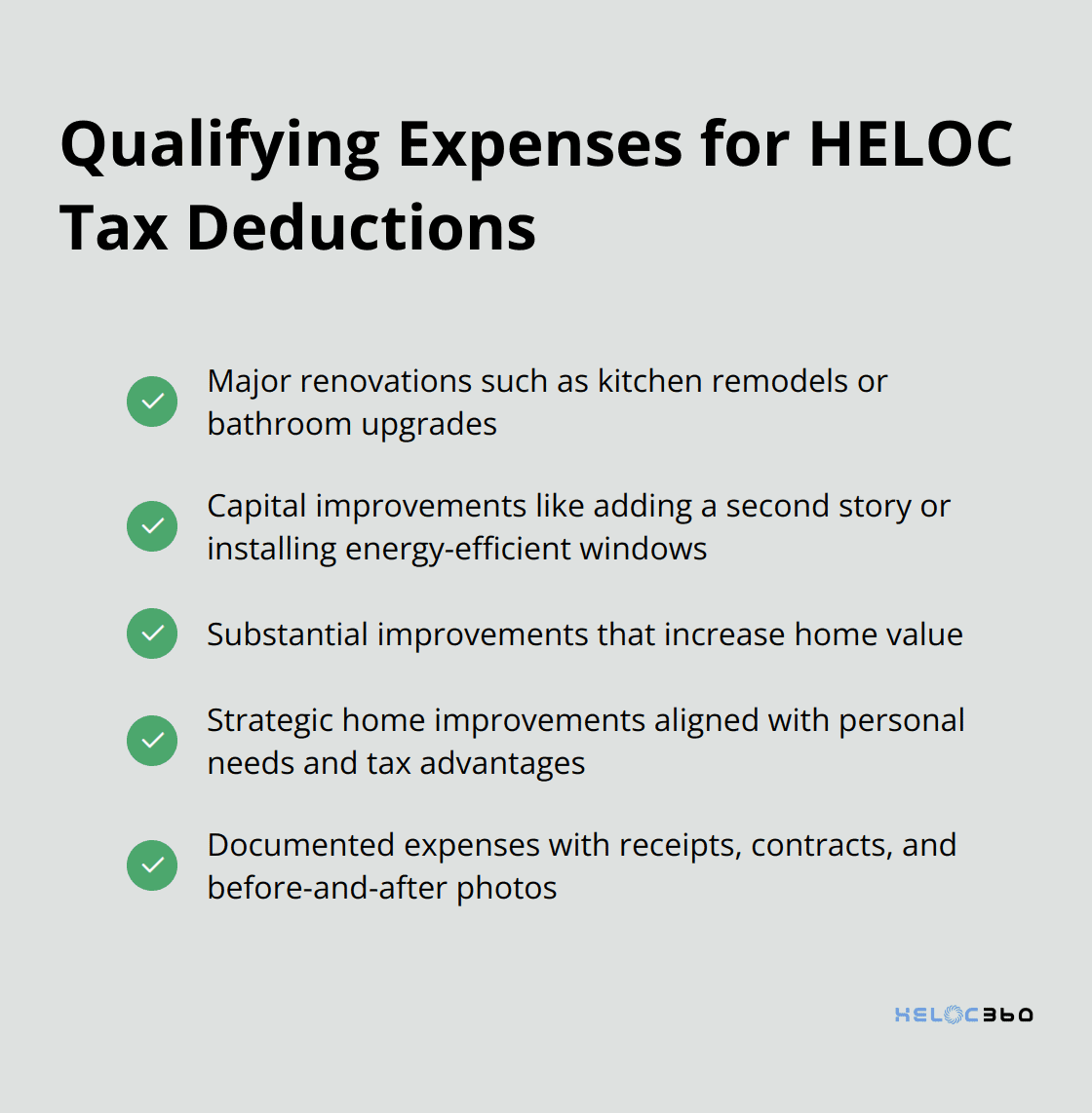

The IRS permits HELOC interest deductions for funds used to buy, build, or substantially improve the home securing the loan. This includes major renovations such as kitchen remodels, bathroom upgrades, or room additions. Routine maintenance or minor repairs don't qualify. For instance, replacing a roof or installing energy-efficient windows would likely qualify, while painting a room or fixing a leaky faucet wouldn't.

Americans spent an estimated $603 billion in 2024 on remodeling their homes. This combination of potential tax deductions and increased home value makes home improvements an attractive option for HELOC usage.

Capital Improvements vs. Repairs

It's essential to differentiate between capital improvements and repairs. Capital improvements are amounts paid to improve a unit of property, including betterments, restorations, or adaptations to new or different uses. These typically qualify for HELOC interest deductions. Repairs simply maintain your home's current condition and don't qualify.

For example, if you use your HELOC to add a second story to your home, that's a capital improvement. However, if you use it to fix a broken window, that's a repair and doesn't qualify for the deduction.

The Importance of Documentation

Meticulous record-keeping is vital. Save all receipts, contracts, and before-and-after photos of your home improvements. These documents will prove invaluable if the IRS questions your deductions.

Non-Qualifying Expenses

While debt consolidation, investment opportunities, and education expenses can be valid uses for a HELOC, they typically don't qualify for tax deductions under current IRS rules. Always consult with a tax professional to understand how your specific use of HELOC funds might impact your tax situation.

Strategic Planning for HELOC Usage

To maximize the benefits of your HELOC, consider planning your home improvements strategically. Try to align your renovation projects with both your personal needs and potential tax advantages. This approach can help you create a win-win situation where you enhance your living space while also optimizing your tax position.

As we move forward, let's explore how to maximize your HELOC tax benefits through careful tracking, professional guidance, and strategic timing of your withdrawals.

How to Maximize HELOC Tax Benefits

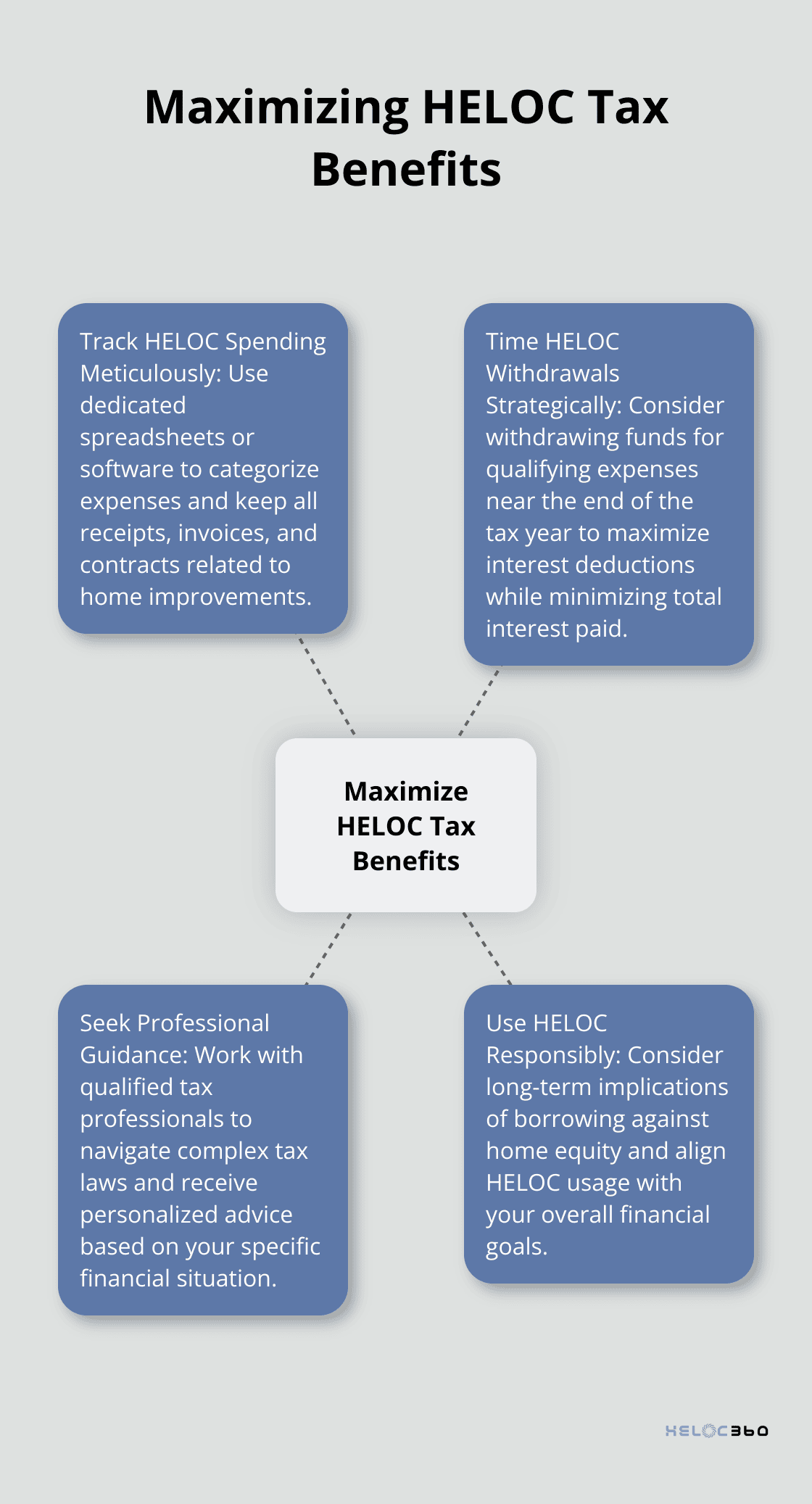

Track HELOC Spending Meticulously

Accurate record-keeping is essential for claiming HELOC interest deductions. Use a dedicated spreadsheet or financial software to track every dollar spent from your HELOC. Categorize expenses as either qualifying (home improvements) or non-qualifying. Keep all receipts, invoices, and contracts related to home improvements. Photos of before and after renovations can provide additional proof of how you used the funds.

Time HELOC Withdrawals Strategically

The timing of your HELOC withdrawals can significantly impact your tax benefits. Consider withdrawing funds for qualifying expenses near the end of the tax year. This strategy allows you to claim the maximum interest deduction for that year while minimizing the total interest paid.

For example, if you plan a major kitchen renovation, start the project in November or December. This could allow you to deduct a full year's worth of interest on your taxes, even though you've only paid interest for a couple of months.

Use HELOC Interest for Other Deductions

HELOC interest is only deductible for home improvements, but you can use the funds for various purposes. If you use HELOC funds for business expenses or investments, the interest may be deductible under different tax rules. For instance, interest on funds used for rental property improvements might be deductible as a business expense.

Seek Professional Guidance

Tax laws are complex and ever-changing. Work with a qualified tax professional to navigate the intricacies of HELOC tax benefits. They can provide personalized advice based on your specific financial situation and help you avoid costly mistakes.

Use Your HELOC Responsibly

While maximizing tax benefits is important, it's equally important to use your HELOC responsibly. Always consider the long-term implications of borrowing against your home equity. Try to understand these implications and connect with lenders who offer terms that align with your financial goals.

Final Thoughts

HELOC tax deductions in 2025 require careful planning and a thorough understanding of current tax laws. You can maximize the tax benefits of your HELOC if you focus on qualifying expenses like substantial home improvements, maintain meticulous records, and time your withdrawals strategically. The landscape of HELOC tax deductions may change, so it's essential to stay informed about any updates to tax legislation.

A well-managed HELOC can open doors to new opportunities when used responsibly. It's not just about claiming deductions; it's about leveraging your home's equity to improve your overall financial position. You can renovate your home to increase its value or use the funds for other strategic purposes (such as investing in a business).

At HELOC360, we connect you with lenders that align with your financial goals, making it easier to access the funds you need while understanding the tax implications. Professional advice can prove invaluable as you navigate the complexities of HELOCs and tax laws. Visit HELOC360 to learn more about how we can help you unlock the full potential of your home equity.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.