How to Fund Your Dream Home Renovation with a HELOC

Table of Contents

Dreaming of a home makeover but unsure how to finance it? A HELOC renovation might be the perfect solution.

At HELOC360, we've seen countless homeowners transform their living spaces using this flexible financing option.

In this post, we'll explore how you can use a Home Equity Line of Credit to fund your renovation projects, maximize your investment, and turn your dream home into reality.

What Is a HELOC and How Can It Fund Your Renovation?

A Home Equity Line of Credit (HELOC) transforms your home improvement dreams into reality. This financial tool allows you to borrow against your home's equity, providing a flexible source of funds for renovations.

How HELOCs Work

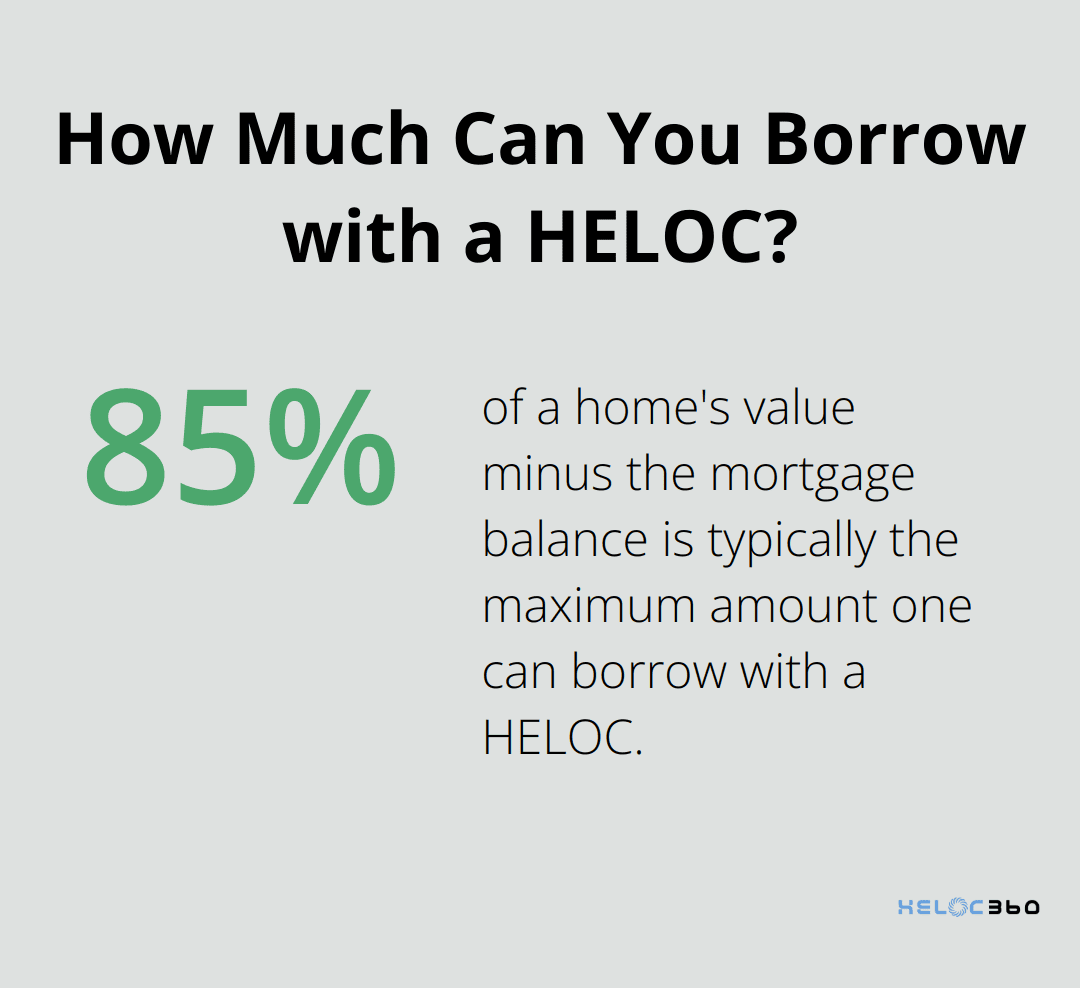

When you open a HELOC, you receive a credit limit based on your home's value and your outstanding mortgage balance. You can typically borrow up to 85% of your home's value minus your mortgage balance. For instance, if your home is worth $400,000 and you owe $250,000 on your mortgage, you might qualify for a HELOC of up to $90,000 (85% of $400,000 = $340,000 - $250,000 = $90,000).

HELOCs usually have two phases: a draw period and a repayment period. The draw period (often 10 years) allows you to borrow funds as needed, paying interest only on what you use. This flexibility suits ongoing renovation projects where costs may fluctuate.

Benefits for Home Improvements

Using a HELOC for renovations offers several advantages:

- Lower interest rates: HELOCs typically have lower rates than credit cards or personal loans because your home secures the credit line. This leads to significant savings on large projects.

- Pay interest only on used funds: You only pay interest on the amount you actually use, not the entire credit line. This feature benefits phased renovations where you might not need all the funds at once.

- Potential tax benefits: Interest may be tax-deductible when used for home improvements (consult a tax professional for current regulations).

HELOC vs. Other Financing Options

HELOCs often outperform other renovation financing methods:

- Personal loans provide a lump sum with fixed payments, while HELOCs offer more flexibility in borrowing and repayment.

- Credit cards, while convenient, usually carry much higher interest rates. A $30,000 kitchen remodel financed at 18% APR on a credit card could cost thousands more in interest compared to a HELOC with a 7% APR.

- Cash-out refinancing replaces your entire mortgage, which may not be ideal if you already have a low interest rate on your existing loan.

For those seeking flexibility, cost-effectiveness, and ease of use, HELOC stands out as a top choice. Our platform connects you with lenders offering competitive rates and terms, ensuring you find the best HELOC for your renovation needs.

Responsible Borrowing

While HELOCs offer many benefits, they use your home as collateral. Borrow responsibly and create a solid repayment plan. With careful planning and the right HELOC, you can fund your dream renovation while building long-term value in your home.

As you consider using a HELOC for your home improvements, it's essential to plan your renovation project carefully. Let's explore how to assess your home's value, prioritize projects, and create a realistic budget in the next section.

How to Plan Your Dream Renovation

Assess Your Home's Value and Equity

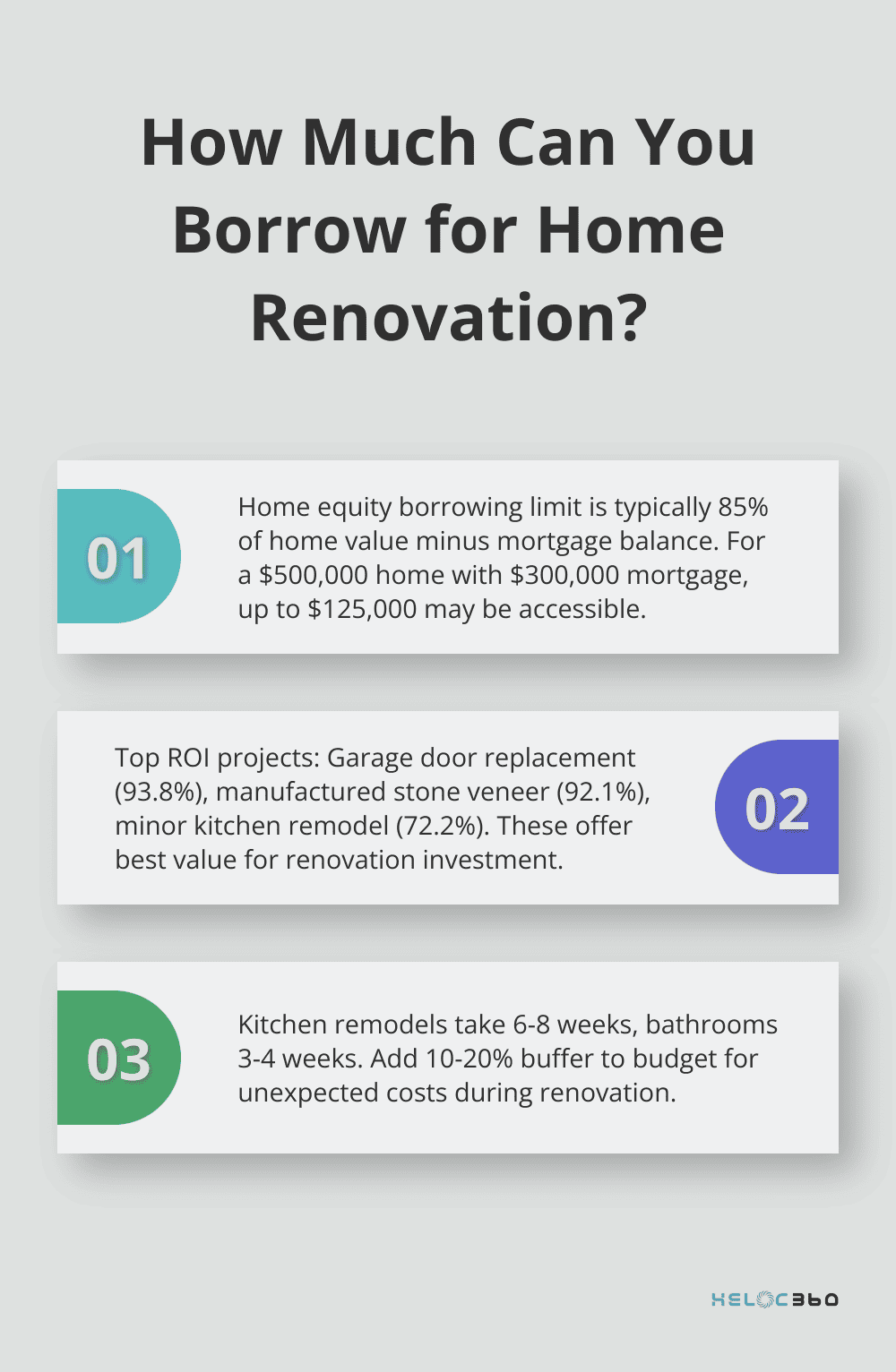

Before you start your renovation plans, you need to know your home's current value and available equity. Get a professional appraisal or use online valuation tools. Most lenders allow you to borrow up to 85% of your home's value minus your outstanding mortgage balance.

For example, if your home is worth $500,000 and you owe $300,000 on your mortgage, you might access up to $125,000 in equity (85% of $500,000 = $425,000 - $300,000 = $125,000). This figure provides a clear picture of your renovation budget ceiling.

Choose High-Impact Projects

Not all renovations offer equal return on investment (ROI). According to Remodeling Magazine's 2021 Cost vs. Value Report, these projects offer the highest ROI:

- Garage Door Replacement: 93.8% ROI

- Manufactured Stone Veneer: 92.1% ROI

- Minor Kitchen Remodel: 72.2% ROI

Focus on projects that improve your living space and add significant value to your home. A modern, energy-efficient kitchen or an updated bathroom often tops the list for both enjoyment and resale value.

Create a Realistic Budget

After you identify your priority projects, it's time to crunch the numbers. Get detailed quotes from at least three contractors for each major renovation. Don't forget to factor in permits, materials, and a 10-20% buffer for unexpected costs.

Set a Realistic Timeline

A full kitchen remodel can take 6-8 weeks, while a bathroom overhaul might require 3-4 weeks. Always add extra time to account for delays in material delivery or unforeseen issues.

To keep your project on track, create a detailed schedule with your contractor. This should include start and end dates for each phase of the renovation (from demolition to final inspections).

Consider Financing Options

As you plan your renovation, explore various financing options. While personal loans and credit cards are available, a Home Equity Line of Credit (HELOC) often provides more flexibility and lower interest rates. HELOCs work by offering an available credit limit determined by your home's value, the amount owed on the mortgage, and the lender's criteria.

With your renovation plan in place, it's time to explore how to maximize your HELOC for home improvements. Let's look at strategies for efficient fund utilization and tips for managing draw periods and repayment in the next section.

How to Maximize Your HELOC for Home Improvements

Use Funds Strategically

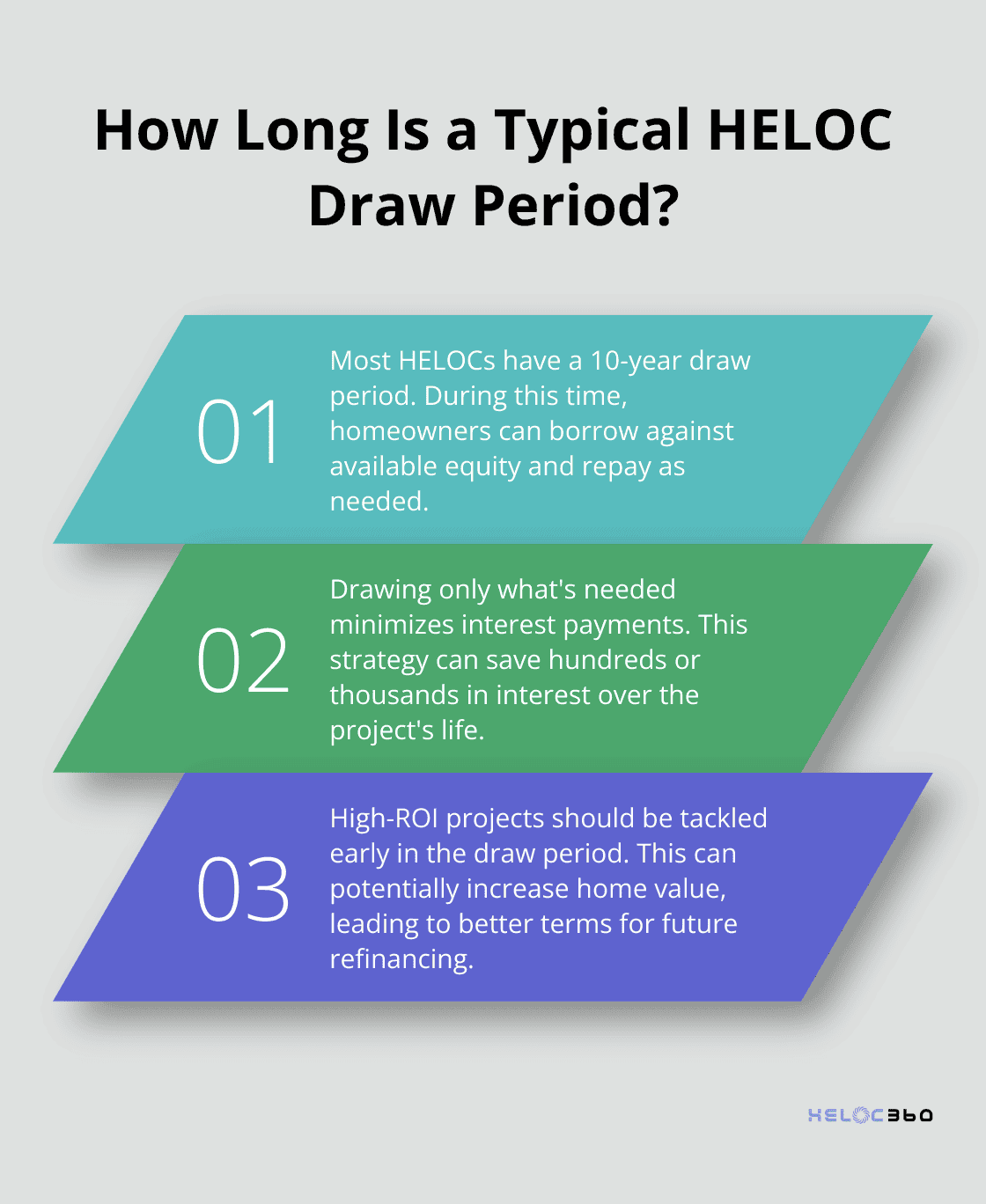

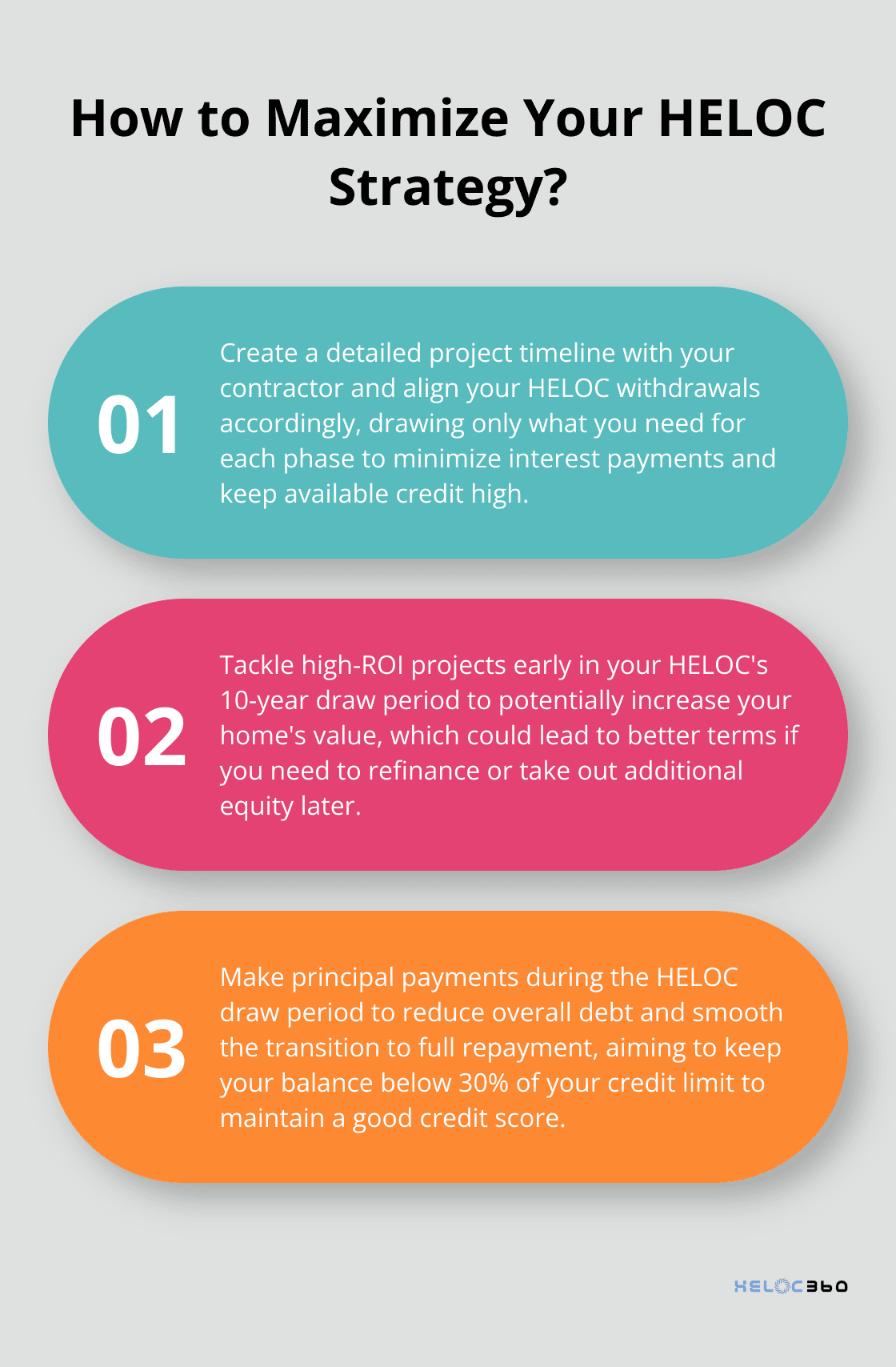

Draw only what you need, when you need it. This approach minimizes interest payments and keeps your available credit high. If you're doing a kitchen remodel in phases, only withdraw funds for each phase as it begins. This strategy can save you hundreds (or even thousands) in interest over the life of your project.

Many homeowners make the mistake of withdrawing their entire HELOC amount upfront. This leads to unnecessary interest charges on unused funds. Instead, create a detailed project timeline with your contractor and align your withdrawals accordingly.

Manage Your Draw Period Effectively

Most HELOCs have a 10-year draw period. During this time, you can borrow against your available equity, repay that amount, and use it again as needed. Take advantage of this flexibility by timing your renovations strategically.

Consider tackling high-ROI projects early in your draw period. This allows you to potentially increase your home's value, which could lead to better terms if you need to refinance or take out additional equity later.

Plan for Repayment

After the draw period ends, you'll enter the repayment phase. Be prepared for potentially higher monthly payments as you start paying back principal along with interest.

One effective strategy involves making principal payments during the draw period. This reduces your overall debt and can make the transition to full repayment smoother. If you borrow $50,000 for a renovation but manage to pay back $10,000 during the draw period, you'll have less to repay when the repayment phase begins.

Leverage Potential Tax Benefits

The interest on a home equity loan used for home improvements may be tax-deductible, provided the funds were used to buy or build a home, or make improvements to one, as defined by the IRS. However, tax laws change, and individual situations vary. Always consult with a qualified tax professional to understand your specific circumstances.

If you're eligible, this deduction can significantly reduce the effective cost of your renovation. If you're in the 24% tax bracket and pay $3,000 in deductible HELOC interest, you could potentially save $720 on your taxes.

Monitor Your Credit Utilization

Your HELOC affects your credit utilization ratio, which impacts your credit score. Try to keep your HELOC balance below 30% of your credit limit to maintain a good credit score. This practice not only helps your credit score but also ensures you have funds available for unexpected renovation costs.

Final Thoughts

A HELOC renovation offers a flexible and cost-effective way to transform your living space. You can tap into your home's equity, access funds at competitive rates, and tackle projects that enhance your quality of life and property value. The ability to draw funds as needed during renovations provides unparalleled financial control, ensuring you only pay interest on the amount you use.

Careful planning and budgeting are essential for a successful HELOC renovation. You should assess your home's value, prioritize projects with high ROI, and create a realistic timeline and budget. Effective management of your draw period and repayment planning will maximize the benefits of your HELOC while minimizing financial stress.

We at HELOC360 want to help you navigate the world of home equity financing. Our platform connects you with lenders offering competitive rates and terms tailored to your specific needs. We provide guidance and resources to help you make informed decisions about your HELOC (ensuring you get the most value from your home's equity).

Related Articles

When Is the Right Time to Consider a HELOC?

Optimize your HELOC timing to enhance your financial position. Learn key market trends and personal indicators for securing a Home Equity Line of Credit.

Using a HELOC for Debt Consolidation: Pros and Cons

Explore the pros and cons of using a HELOC for debt consolidation. Understand its impact on finances and find out if it fits your needs.

Equity Line vs Equity Loan: Making the Right Choice

Explore the key differences between equity line vs equity loan and find the best fit for your financial needs by comparing flexibility, rates, and benefits.