How to Refinance Your HELOC Successfully

Table of Contents

HELOC refinancing can be a smart financial move, but it's not always straightforward. Many homeowners struggle to navigate the process effectively.

At HELOC360, we've seen firsthand how proper guidance can make all the difference in securing better terms and rates.

This guide will walk you through the essential steps to refinance your HELOC successfully, helping you make informed decisions about your home equity.

Why Refinance Your HELOC?

Understanding HELOC Refinancing

HELOC refinancing is a strategic financial move that can significantly impact your home equity management. At its core, refinancing your Home Equity Line of Credit (HELOC) means replacing your existing HELOC with a new one, often with more favorable terms.

Lowering Your Interest Rate

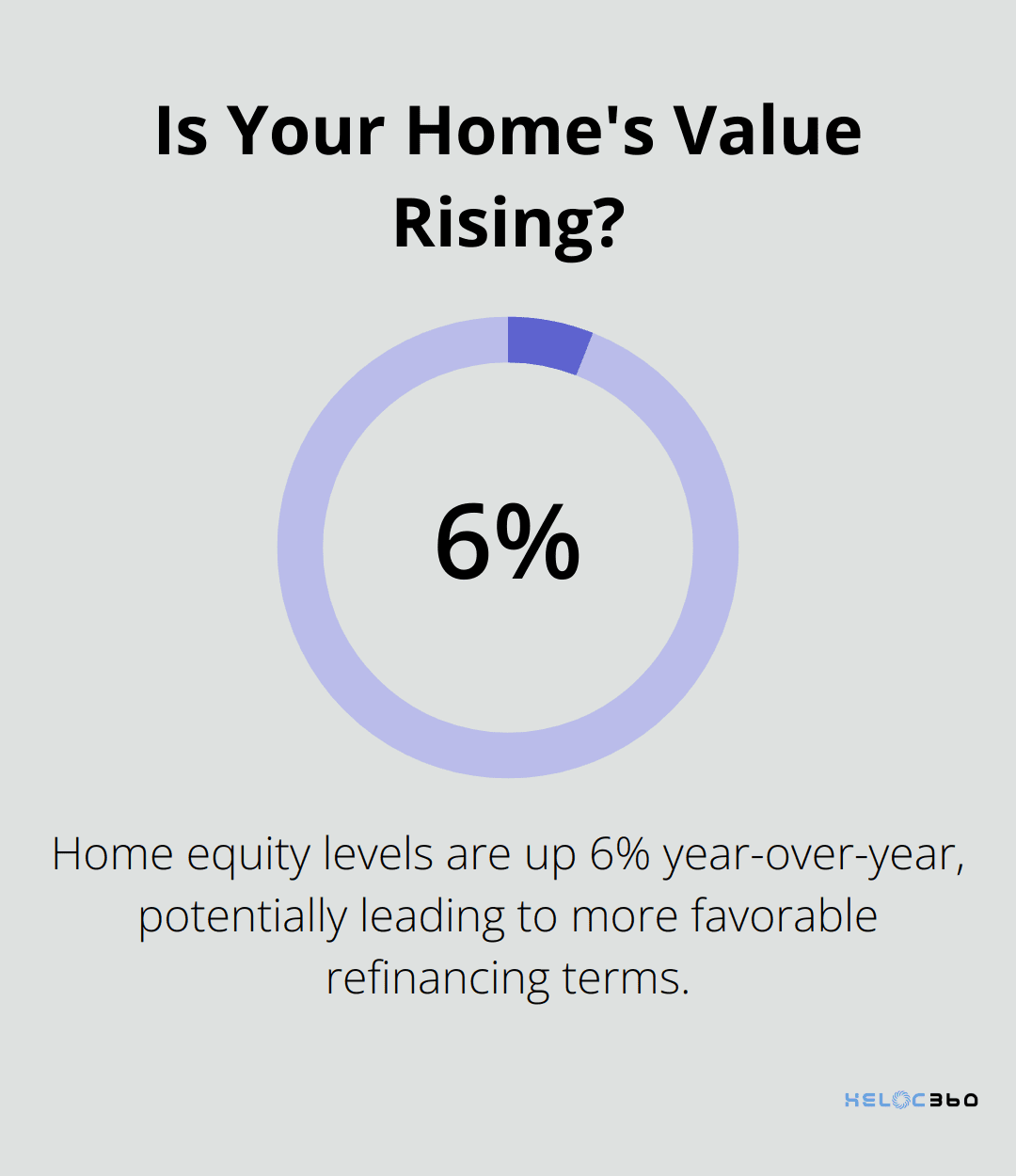

One of the primary reasons homeowners choose to refinance their HELOC is to secure a lower interest rate. While home equity levels are slightly down compared to what they were a few months ago, they're still up 6% year-over-year. This increase in home equity could potentially lead to more favorable refinancing terms.

Extending Your Draw Period

Another compelling reason to refinance is to extend your draw period. Once the draw period is over, the HELOC will transition to the repayment period. At this point, you can't borrow against the line of credit. Refinancing allows you to reset the clock on your draw period, which gives you more time to access funds and potentially lowers your monthly payments.

Switching from Variable to Fixed Rates

Many homeowners initially choose variable-rate HELOCs due to lower introductory rates. However, as market conditions change, these rates can increase dramatically. Refinancing allows you to switch to a fixed-rate HELOC. A fixed-rate loan has the same interest rate for the duration of the borrowing period, whereas variable rates can move up and down. This provides predictable payments and protects against future rate hikes.

How HELOC Refinancing Differs from Other Loans

HELOC refinancing is distinct from other loan refinancing options. Unlike mortgage refinancing, which typically replaces your entire mortgage, HELOC refinancing focuses solely on your home equity line of credit. This means the process is often quicker and involves less paperwork.

Moreover, HELOC refinancing differs from personal loan refinancing in that it's secured by your home equity, generally resulting in lower interest rates. However, this also means that failure to repay could put your home at risk.

Now that you understand the reasons and unique aspects of HELOC refinancing, let's explore how to prepare for this financial move in the next section.

How to Prepare for HELOC Refinancing

Evaluate Your Financial Health

Assess Your Monthly Expenses by evaluating your monthly expenses, including mortgage payments, utilities, property taxes, insurance, and maintenance costs. This will give you a clear picture of how much you can comfortably afford in HELOC payments. Ensure you don't stretch yourself too thin with your refinancing plans.

Review Your Credit Score and Report

Your credit score plays a vital role in HELOC refinancing. As of January 3, 2025, many lenders allow you to tap your equity with a credit score in the 600s, with 620 being common for HELOCs. Request your free credit report from AnnualCreditReport.com and check for any errors. If you find mistakes, dispute them immediately. This process can take up to 30 days, so start early.

Assess Your Home's Current Value

Home values can fluctuate significantly over time. Get a professional appraisal or use online tools like Zillow or Redfin for a rough estimate. Keep in mind that these online estimates can be off by 5% to 10%. A higher home value could mean more equity and potentially better refinancing terms.

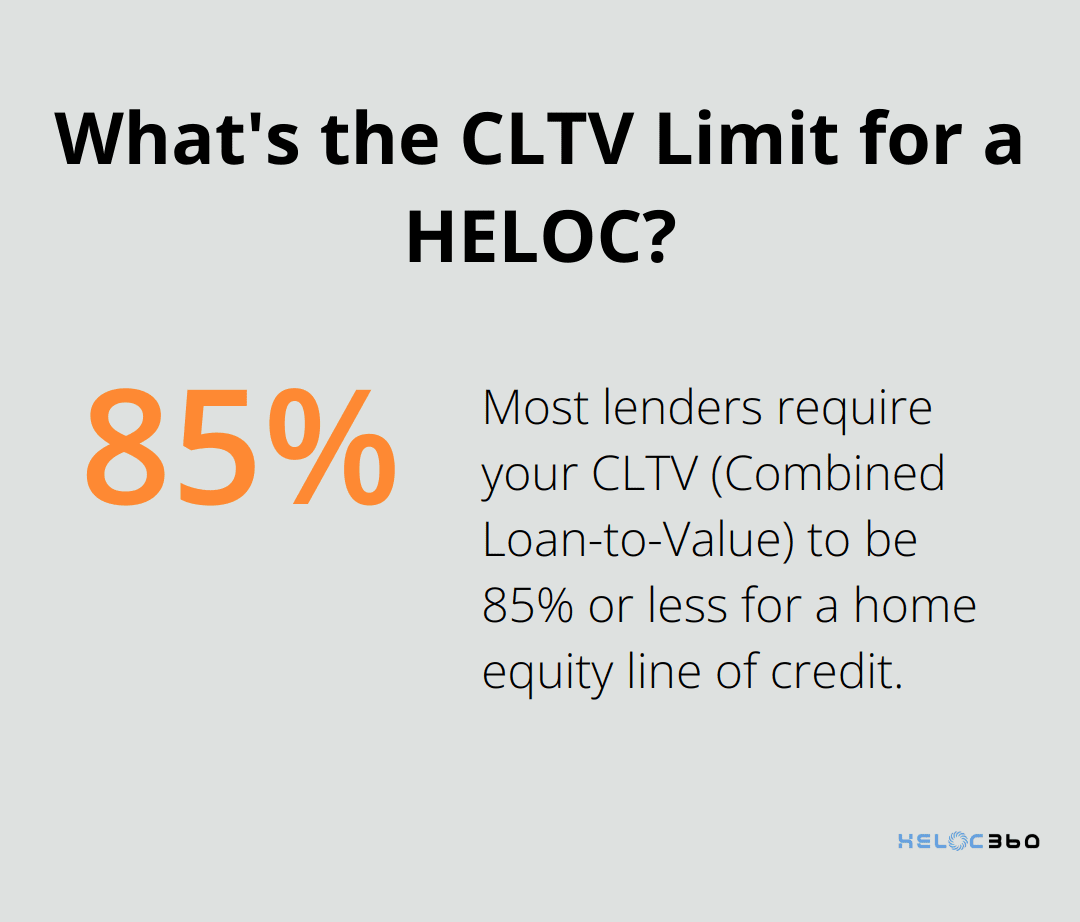

Calculate Your Loan-to-Value Ratio

Your loan-to-value (LTV) ratio is a key factor lenders consider. Most lenders require your CLTV (Combined Loan-to-Value) to be 85% or less for a home equity line of credit. If your CLTV is too high, you can either pay down your current loan amount or wait for your home's value to increase.

Gather Necessary Documentation

Prepare all the necessary documents for your HELOC refinancing application. This typically includes proof of income (pay stubs, W-2 forms, tax returns), bank statements, and information about your existing debts and assets. Having these documents ready will speed up the application process and demonstrate your financial responsibility to potential lenders.

Now that you've completed these preparatory steps, you're in a strong position to start shopping for HELOC refinancing options. The next chapter will guide you through the process of finding and comparing lenders to secure the best terms for your new HELOC.

How to Refinance Your HELOC

Research and Compare Lenders

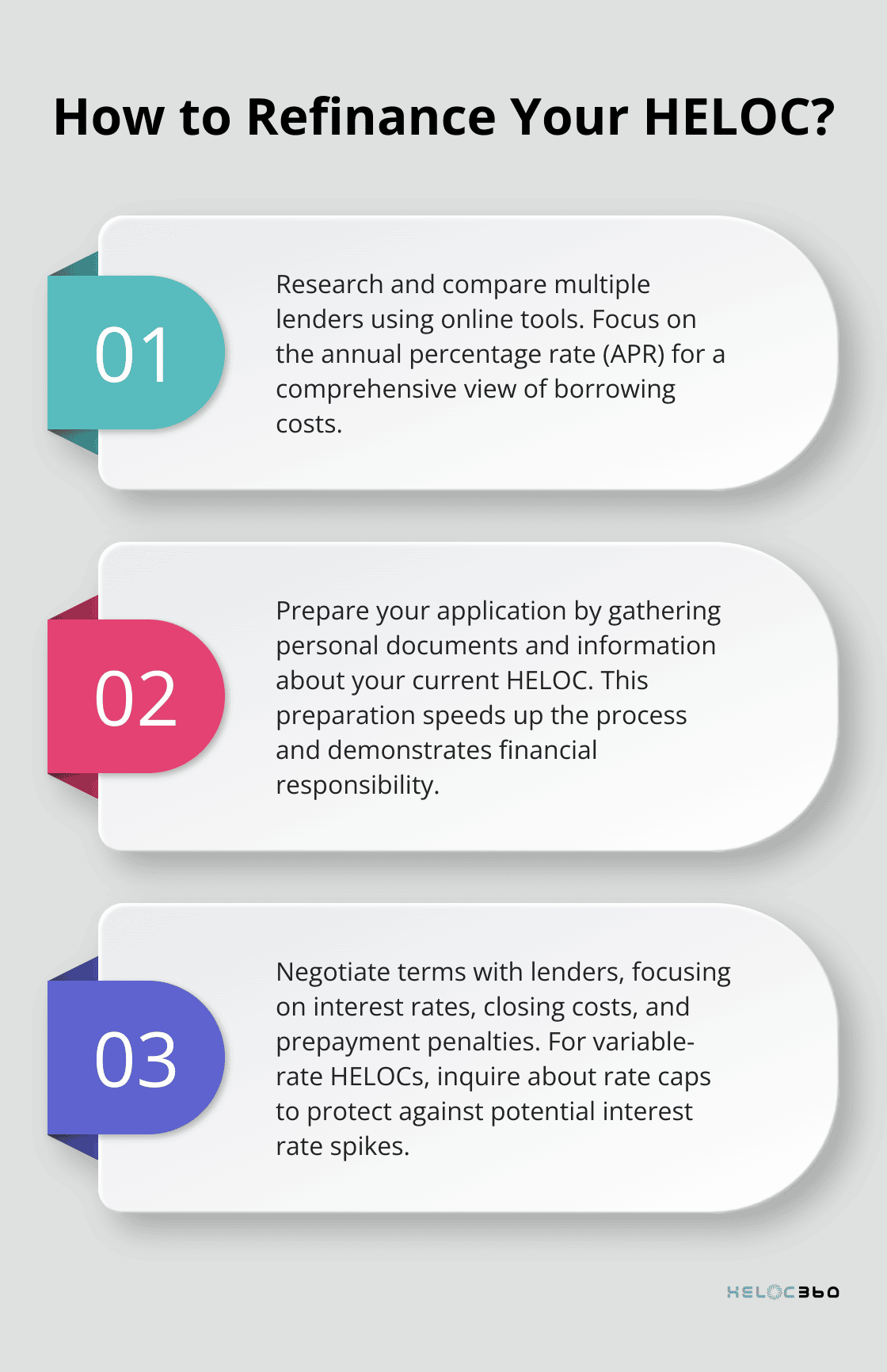

Start your HELOC refinancing journey by researching multiple lenders. Online tools let you customize sample rates by location and compare lenders. Look beyond your current bank - online lenders, credit unions, and mortgage companies often offer competitive rates.

Use comparison tools to evaluate offers side-by-side. Pay attention to interest rates, fees, and terms. The Consumer Financial Protection Bureau suggests focusing on the annual percentage rate (APR) as it provides a more comprehensive view of the total cost of borrowing.

Prepare Your Application

After you identify potential lenders, prepare your application. Collect documents such as your full legal name, Social Security number, date of birth, current address, and previous address if less than two years. Also, gather documents related to your current HELOC and any other outstanding debts.

This preparation can significantly speed up the process and demonstrate your financial responsibility to lenders.

Negotiate Terms

Once lenders provide loan estimates, seize the opportunity to negotiate. Don't hesitate to ask for better terms or lower fees. Consider negotiating closing costs, including lender fees and seller-paid costs.

Focus on the interest rate, closing costs, and any prepayment penalties. For variable-rate HELOCs, inquire about rate caps to protect yourself from potential interest rate spikes.

Close the Deal

After you agree on terms with a lender, enter the closing process. This typically involves a home appraisal. You'll also need to review and sign several legal documents.

Before signing, carefully examine the closing disclosure. This document outlines all the final terms of your new HELOC. Ensure it matches what you agreed upon with the lender. If anything seems unclear, ask questions or seek clarification.

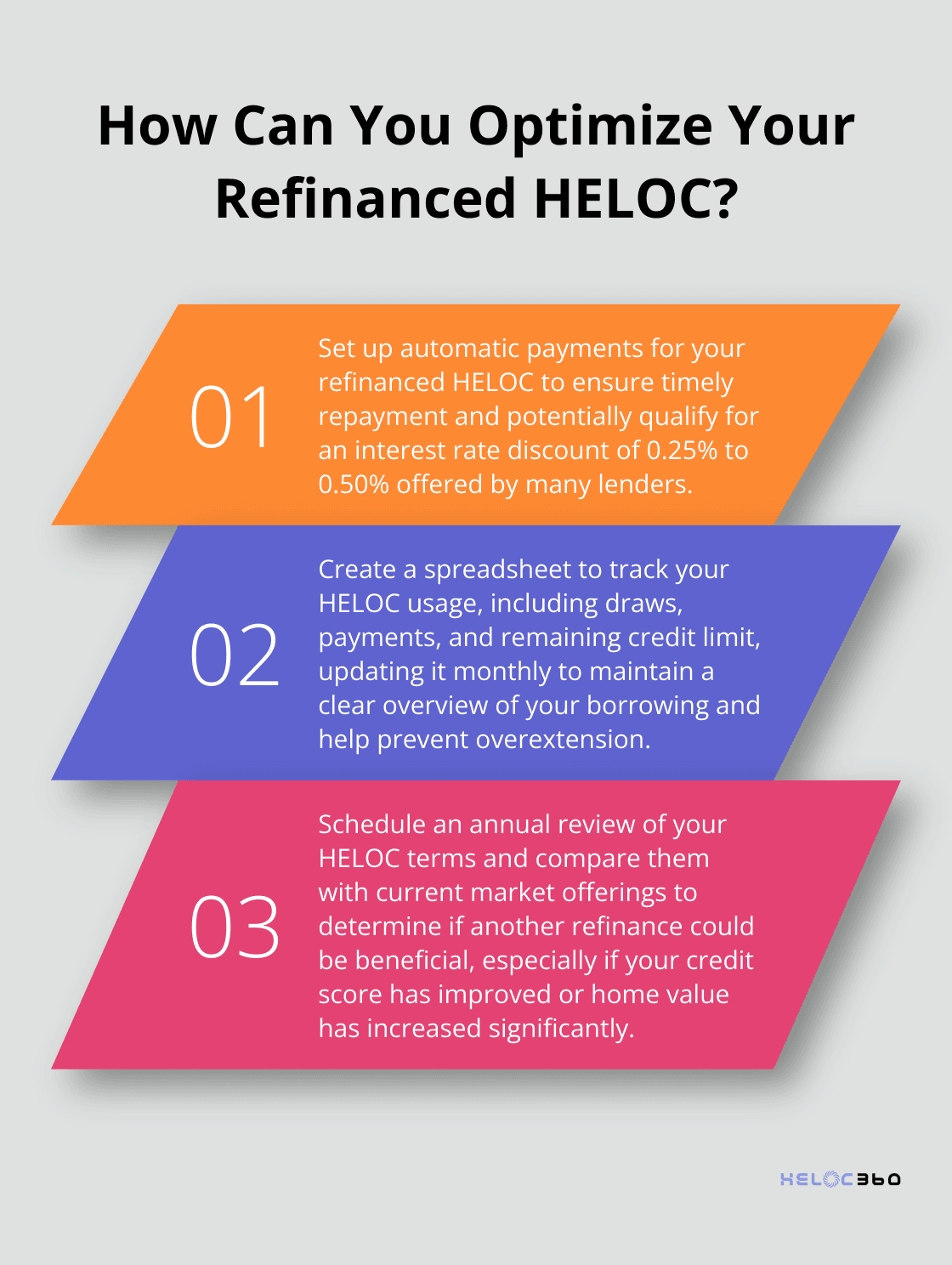

Maximize Your Refinanced HELOC

Once you've successfully refinanced, try to make the most of your new HELOC terms. Consider using the funds for high-value home improvements or consolidating high-interest debt. Always keep track of your draw period and repayment terms to avoid any surprises down the line.

Final Thoughts

HELOC refinancing can transform your financial situation when you execute it correctly. You must understand your current financial status, including your credit score and home value. Take time to research and compare lenders, considering overall terms and costs beyond interest rates. Don't hesitate to negotiate, as it could lead to substantial savings over your loan's lifetime.

HELOC360 simplifies the refinancing process and connects you with lenders that match your specific needs. We aim to help you maximize your home equity, whether you want to fund renovations, consolidate debt, or create financial flexibility. Our platform provides the knowledge and support you need to make decisions aligned with your financial goals.

Your home's equity is a valuable asset that you can leverage with careful planning. HELOC refinancing can become a powerful tool to achieve your financial aspirations when you approach it with the right guidance. Consider your options, prepare thoroughly, and make informed choices. Visit HELOC360 to start your HELOC refinancing journey today.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.