Homeowners often wonder about the difference between a HELOC and a second mortgage. These two financial products share similarities but have distinct features that set them apart.

At HELOC360, we frequently encounter questions about whether a HELOC is considered a second mortgage. This blog post will clarify the key differences and similarities between these two popular home equity options.

What Are HELOCs and Second Mortgages?

Understanding HELOCs

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against their home’s equity. It functions like a credit card, providing a revolving line of credit with a predetermined limit. HELOCs typically come with variable interest rates, which can change over time.

McBride forecasts that HELOC rates will continue to fall in 2025, sending the average HELOC to 7.25 percent by the end of the year, a low not seen since 2022.

Defining Second Mortgages

A second mortgage is a lump-sum loan that uses your home as collateral. It ranks behind your primary mortgage in priority (hence the term “second”). Second mortgages usually offer fixed interest rates and set repayment terms.

As of March 19, 2025, HELOC rates have fallen near a two-year low of 8.03 percent and are forecast to retreat further in 2025.

Key Similarities

Both HELOCs and second mortgages:

- Use your home as collateral

- Require sufficient home equity (typically 15% to 20%)

- Carry the risk of foreclosure if you default on payments

Notable Differences

Fund Access

HELOCs allow you to draw money as needed during a draw period (usually 5-10 years). Second mortgages provide a one-time lump sum.

Repayment Structure

HELOCs often have interest-only payments during the draw period, followed by a repayment period for both principal and interest. Second mortgages typically require fixed monthly payments of principal and interest from the start.

Choosing the Right Option

Your financial needs and long-term goals should guide your decision. A HELOC might suit you better if you need ongoing access to funds for various projects. For a one-time large expense, a second mortgage could be the optimal choice.

The next section will explore the structural differences between HELOCs and second mortgages in more detail, helping you understand which option aligns best with your financial situation.

How Do HELOCs and Second Mortgages Differ?

HELOCs and second mortgages may appear similar at first glance, but they have distinct characteristics that set them apart. Homeowners who want to leverage their home equity effectively must understand these differences.

Loan Structure and Fund Access

HELOCs provide a revolving line of credit, similar to a credit card. You can borrow, repay, and borrow again up to your credit limit during the draw period, which typically lasts up to 10 years. During this time, you’re usually only required to pay interest on what you borrow. This flexibility suits ongoing expenses or projects with uncertain costs.

Second mortgages offer a lump sum upfront. You receive the funds and start repayment immediately. This structure works well for large, one-time expenses with known costs (such as a major home renovation or debt consolidation).

Interest Rates and Repayment Terms

HELOCs usually feature variable interest rates tied to the prime rate. These rates can fluctuate over time, which affects your monthly payments.

Second mortgages tend to have higher interest rates than first mortgages. A borrower who now has two mortgage payments to make may face additional financial challenges.

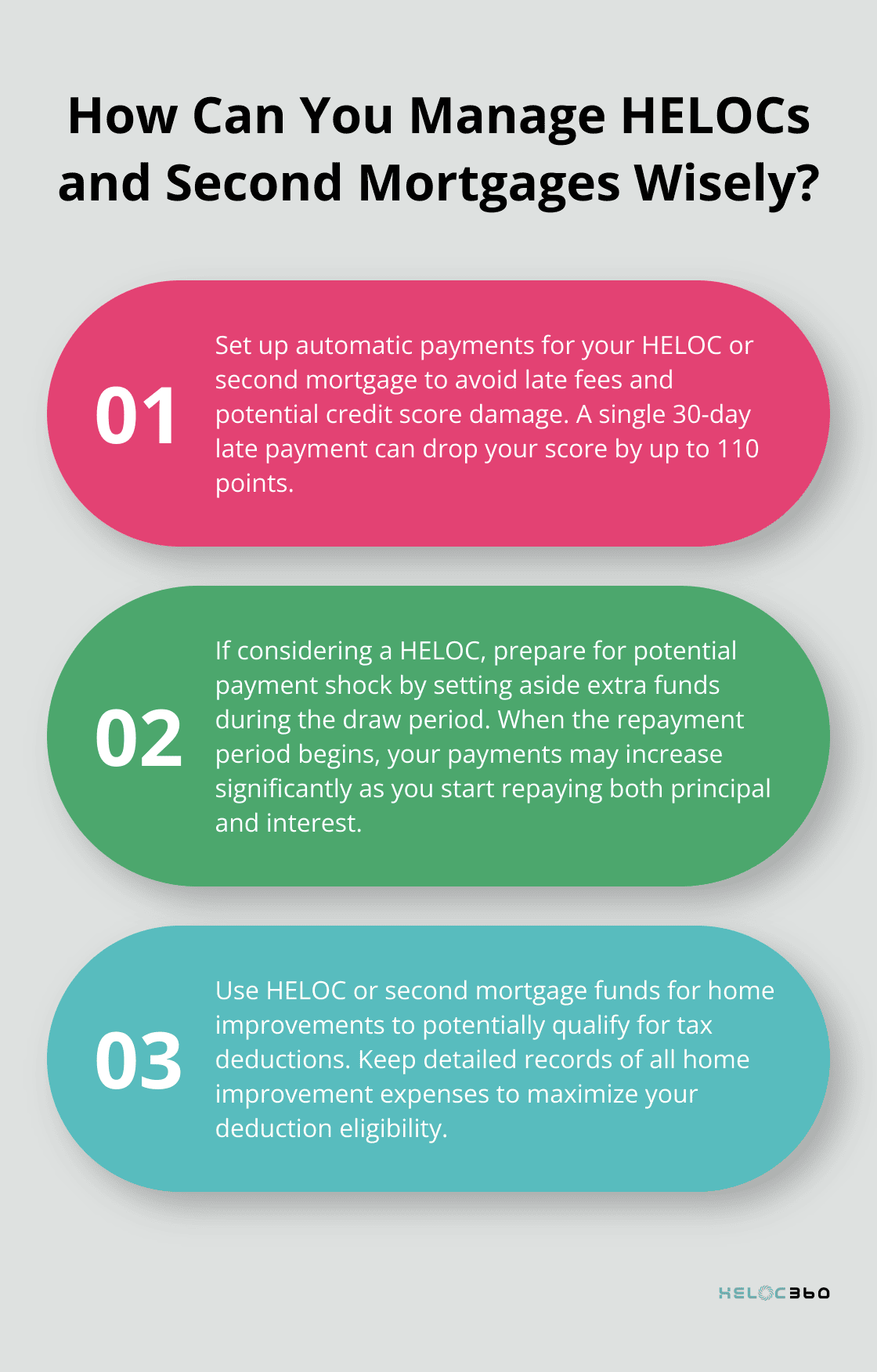

Repayment terms differ significantly. HELOCs often require interest-only payments during the draw period, followed by a repayment period where you pay both principal and interest. This can lead to a significant payment increase, sometimes called “payment shock.”

Second mortgages usually require fixed monthly payments of both principal and interest from the start, which spreads the cost evenly over the loan term.

Flexibility in Borrowing and Repayment

HELOCs offer unparalleled flexibility. You only borrow what you need, when you need it, and only pay interest on the amount you’ve drawn. This can result in lower overall interest costs if you manage your borrowing wisely.

Second mortgages offer less flexibility. You receive the entire loan amount upfront and start accruing interest on the full balance immediately. While this ensures you have all the funds you need for a large expense, it may result in paying interest on money you’re not using right away.

When you consider these options, you must assess your financial needs and long-term goals. The next section will explore the legal and financial implications of choosing a HELOC or a second mortgage, which will further help you make an informed decision.

Legal and Financial Implications of HELOCs and Second Mortgages

Lender Perspectives

Lenders view HELOCs and second mortgages differently. HELOCs offer more flexibility but come with potential risks due to variable rates and revolving nature. Second mortgages, with fixed terms and rates, appear more stable to lenders.

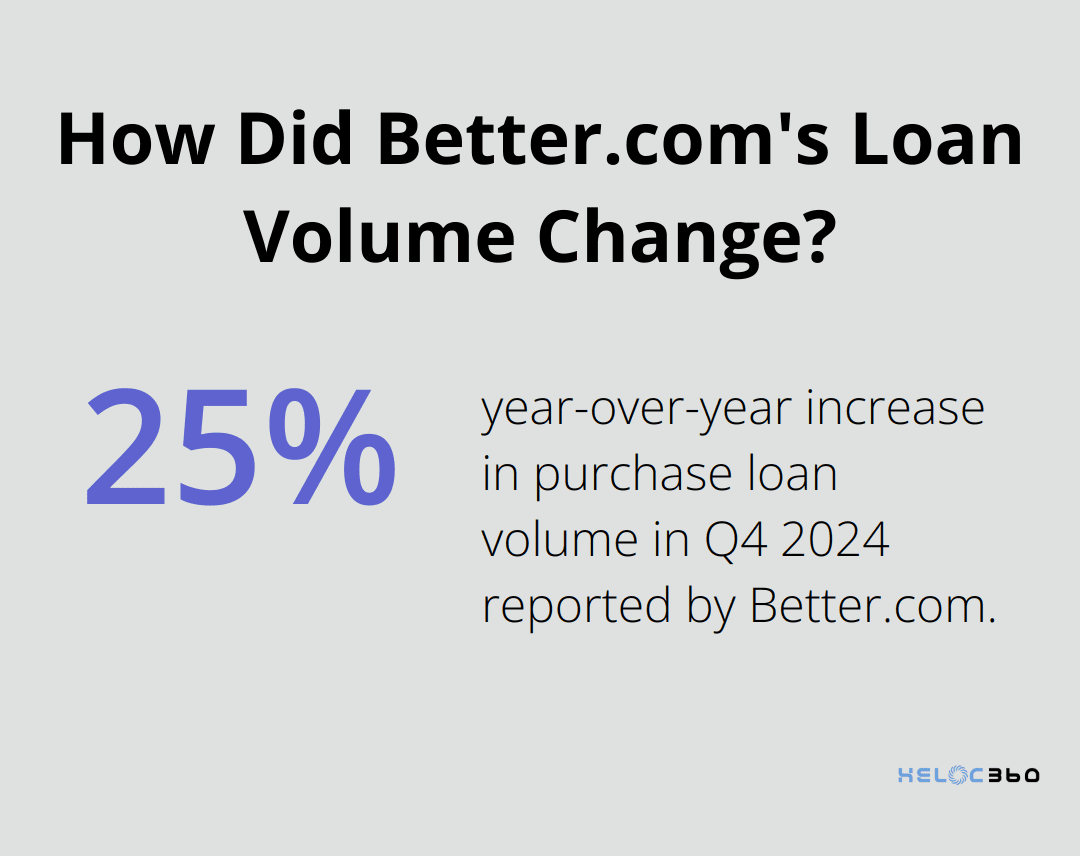

Better.com reports a 25% year-over-year increase in purchase loan volume in Q4 2024. This indicates growing lender confidence in these products. However, approval standards remain high. Most lenders require a credit score of at least 680 for HELOCs.

For second mortgages, lenders typically look for a debt-to-income ratio below 43%. This metric helps lenders assess your ability to manage additional monthly payments.

Credit Score Impact

HELOCs and second mortgages affect your credit score in different ways. A HELOC increases your available credit, which can positively impact your credit utilization ratio. However, it also adds a new account to your credit report, potentially lowering your average account age.

Second mortgages, as installment loans, don’t affect your credit utilization ratio but impact your overall debt levels. FICO reports that installment loans have less impact on credit scores than revolving credit lines like HELOCs.

Late payments on either type of loan can severely damage your credit score. A single 30-day late payment can drop your score by up to 110 points (according to FICO).

Tax Considerations

The Tax Cuts and Jobs Act of 2017 changed the rules for HELOC and second mortgage interest deductions. As of 2025, interest on HELOCs and second mortgages is only tax-deductible if you use the funds for home improvements.

For HELOCs, you can deduct interest on up to $750,000 of qualified residence loans ($375,000 if married filing separately). This limit applies to the combined amount of your first mortgage and HELOC.

Second mortgage interest follows similar rules. However, if you took out your second mortgage before December 15, 2017, you might still deduct interest on up to $1 million of qualified residence loans ($500,000 if married filing separately).

Always consult with a tax professional to understand how these deductions apply to your specific situation. The rules can change frequently and prove complex.

Risk Considerations

Both HELOCs and second mortgages use your home as collateral. This means if you default on payments, you risk foreclosure. Try to assess your financial stability and future income prospects before taking on additional debt secured by your home.

HELOCs come with the added risk of payment shock. When the draw period ends, your payments may increase significantly as you start repaying both principal and interest.

Second mortgages add another monthly payment to your budget from the start. This can strain your finances if you’re not prepared for the additional expense.

Final Thoughts

HELOCs and second mortgages provide homeowners with distinct ways to access their home equity. HELOCs offer flexible revolving credit with variable rates, while second mortgages provide stability through fixed rates and lump-sum payouts. Both options use your home as collateral and require careful evaluation of your financial situation and long-term objectives.

Your borrowing needs, risk tolerance, and repayment capacity should guide your decision between a HELOC and a second mortgage. Consider the purpose of the funds, your preference for fixed or variable rates, and your ability to manage potential payment changes. Tax implications and credit score impacts differ between these options, so factor these into your decision-making process.

We at HELOC360 understand the complexities of home equity financing and have developed a platform to simplify the process. Our expertise connects you with the right lenders for your unique situation, whether you prefer a HELOC or a second mortgage. HELOC360 can guide you through your options, helping you make an informed decision that aligns with your financial goals.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.