HELOC or Refinance The Ultimate Showdown

Table of Contents

Are you torn between a HELOC and refinancing your mortgage? You're not alone. Many homeowners face this dilemma when looking to tap into their home equity or adjust their mortgage terms.

At HELOC360, we've helped countless clients navigate the HELOC vs refinance decision. In this post, we'll break down the key differences, pros, and cons of each option to help you make the best choice for your financial situation.

What Are HELOCs and Refinancing?

Understanding HELOCs

A Home Equity Line of Credit (HELOC) is a revolving form of credit with a variable interest rate, similar to a credit card, but secured by your home. During the draw period (typically 10 years), you can borrow, repay, and borrow again up to your credit limit. After this period, you enter the repayment phase where borrowing stops and you must pay back the outstanding balance.

HELOCs usually come with variable interest rates, which can move up and down, potentially leading to fluctuating payments. This flexibility suits ongoing projects or expenses but may result in less predictable monthly payments.

The Refinancing Process Explained

Refinancing involves replacing your current mortgage with a new one. Homeowners often refinance to secure lower interest rates, modify loan terms, or cash out some of their home's equity. The process mirrors that of obtaining your original mortgage: application, approval, and closing.

A cash-out refinance pays off your existing mortgage and gives you a new one, while a home equity loan is a separate loan considered a second mortgage. A cash-out refinance increases your loan amount, which reduces your home equity and might lead to higher monthly payments. However, you could benefit from a lower interest rate on your entire mortgage balance.

Key Differences: HELOC vs. Refinancing

The primary distinction lies in how you access your home's equity:

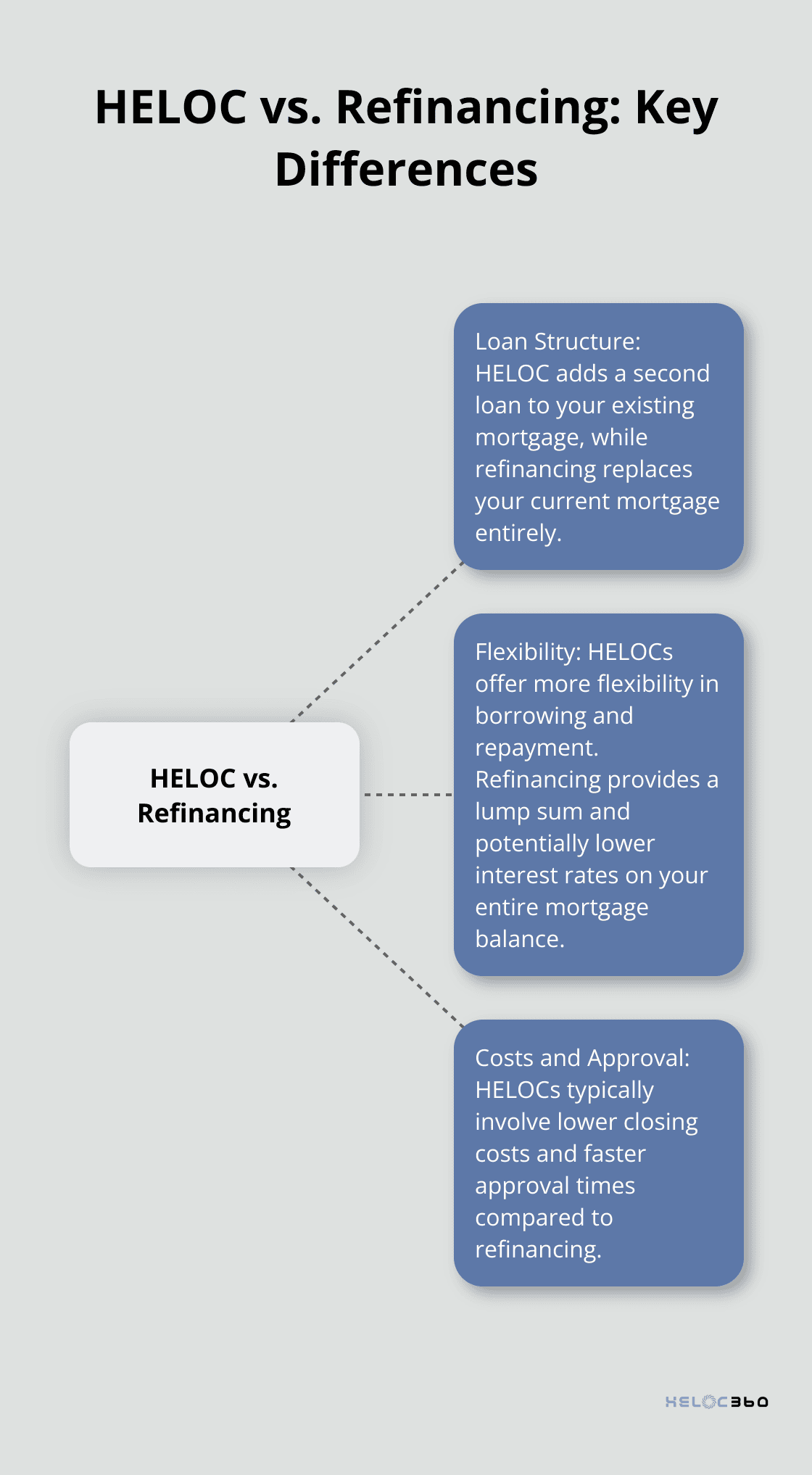

- Loan Structure: A HELOC adds a second loan to your existing mortgage, while refinancing replaces your current mortgage entirely.

- Flexibility: HELOCs offer more flexibility in borrowing and repayment. Refinancing provides a lump sum and potentially lower interest rates on your entire mortgage balance.

- Costs and Approval: HELOCs typically involve lower closing costs and faster approval times compared to refinancing.

Choosing Between HELOC and Refinancing

Your decision should align with your specific financial goals, current mortgage rate, and the amount of equity you need to access. Consider a HELOC if you need ongoing access to funds and want to maintain your current mortgage rate. Opt for refinancing if you aim to change your mortgage terms or require a large lump sum.

Factors to Consider

- Interest Rates: Compare current HELOC rates with potential refinancing rates.

- Loan Terms: Evaluate how each option affects your overall loan term and monthly payments.

- Closing Costs: Factor in the costs associated with each option (HELOCs generally have lower costs).

- Tax Implications: Consult with a tax advisor about potential deductions for each option.

As you weigh these options, it's essential to understand how they align with your long-term financial strategy. Let's explore the pros and cons of HELOCs to help you make an informed decision.

Are HELOCs Right for You?

Flexibility: A Powerful Tool

HELOCs offer unique advantages in accessing your home equity. Unlike traditional loans, you can borrow as needed during the draw period (typically 10 years). This feature benefits ongoing expenses or projects with uncertain costs. For example, if you renovate your home in stages, you can draw funds as needed, potentially saving on interest compared to taking out a lump sum upfront.

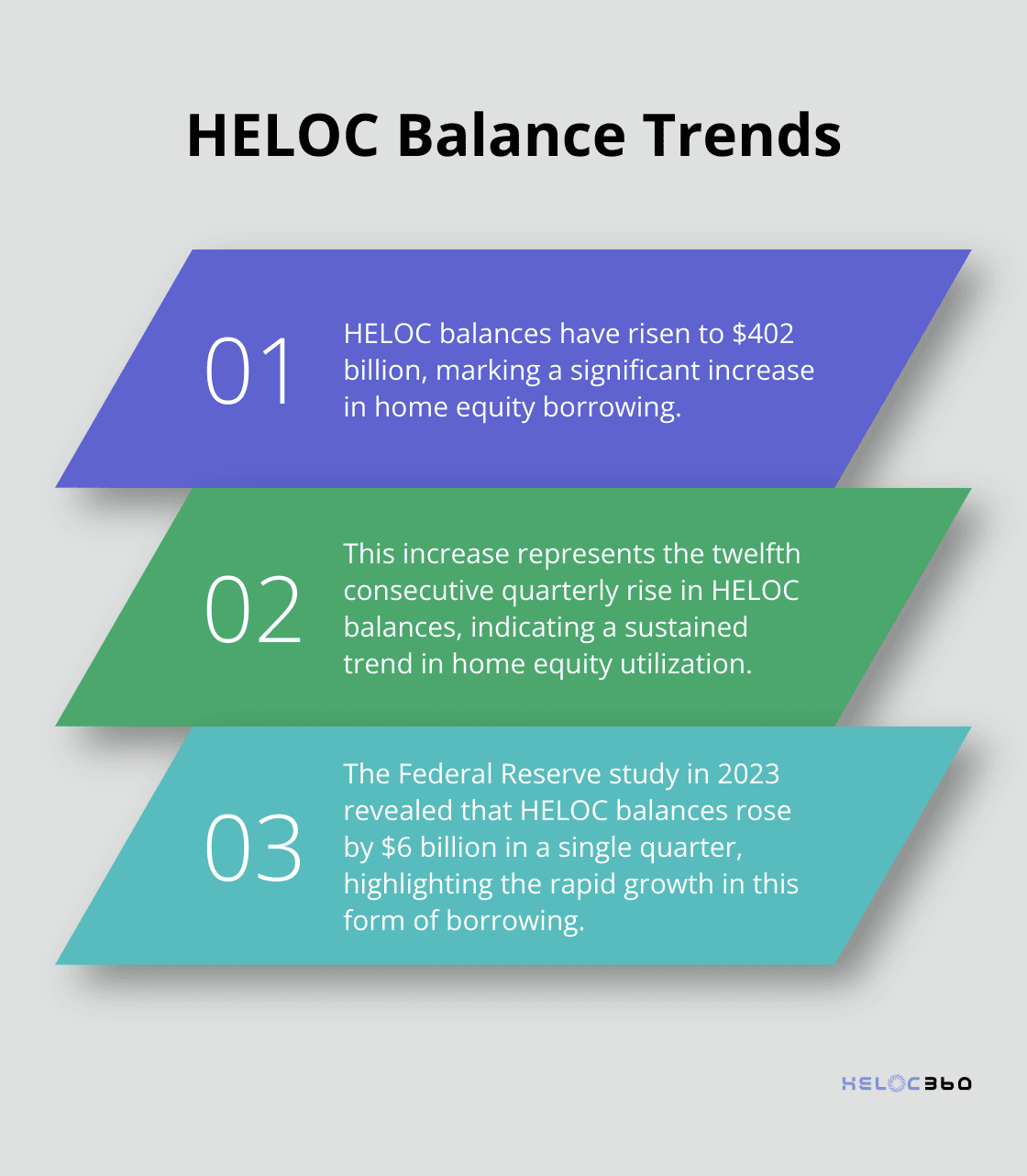

However, this flexibility requires careful management. A 2023 Federal Reserve study revealed that HELOC balances rose by $6 billion, marking the twelfth consecutive quarterly increase. There is now $402 billion in outstanding HELOC balances.

Interest Rates: Opportunities and Risks

HELOCs usually come with variable interest rates, which can be advantageous and risky. While these rates often fall below credit card rates, they fluctuate with market conditions.

If interest rates decrease, your HELOC payments could become more affordable. However, rising rates can lead to higher monthly payments. It's important to understand your budget's capacity to handle potential rate increases. Some lenders offer rate caps or the option to convert a portion of your balance to a fixed rate, which provides some protection against extreme rate hikes.

Credit Score Impact

Opening a HELOC can affect your credit score in several ways. It might thicken your credit file, decrease the age of your accounts, lead to on-time or late payments, add to your credit mix, and sometimes result in a hard inquiry.

Home Equity Considerations

A HELOC allows you to tap into your home's value without selling. This can be a powerful tool for wealth building if used wisely. For instance, using a HELOC to fund home improvements can increase your property's value, potentially offsetting the equity you've borrowed.

It's important to remember that a HELOC is secured by your home. Defaulting on payments could put your property at risk of foreclosure. Additionally, if home values decline, you could end up owing more than your home is worth (a situation known as being "underwater" on your mortgage).

Real-World Applications

HELOCs can fund various financial needs. Some common uses include:

- Education expenses

- High-interest debt consolidation

- Investment in rental properties

The key to success with a HELOC lies in having a clear plan for the funds and a solid strategy for repayment. Understanding these aspects of HELOCs will help you make an informed decision that aligns with your financial goals and risk tolerance.

Now that we've explored the ins and outs of HELOCs, let's turn our attention to refinancing and how it compares as an alternative option for accessing your home equity.

Is Refinancing Right for You?

The Interest Rate Advantage

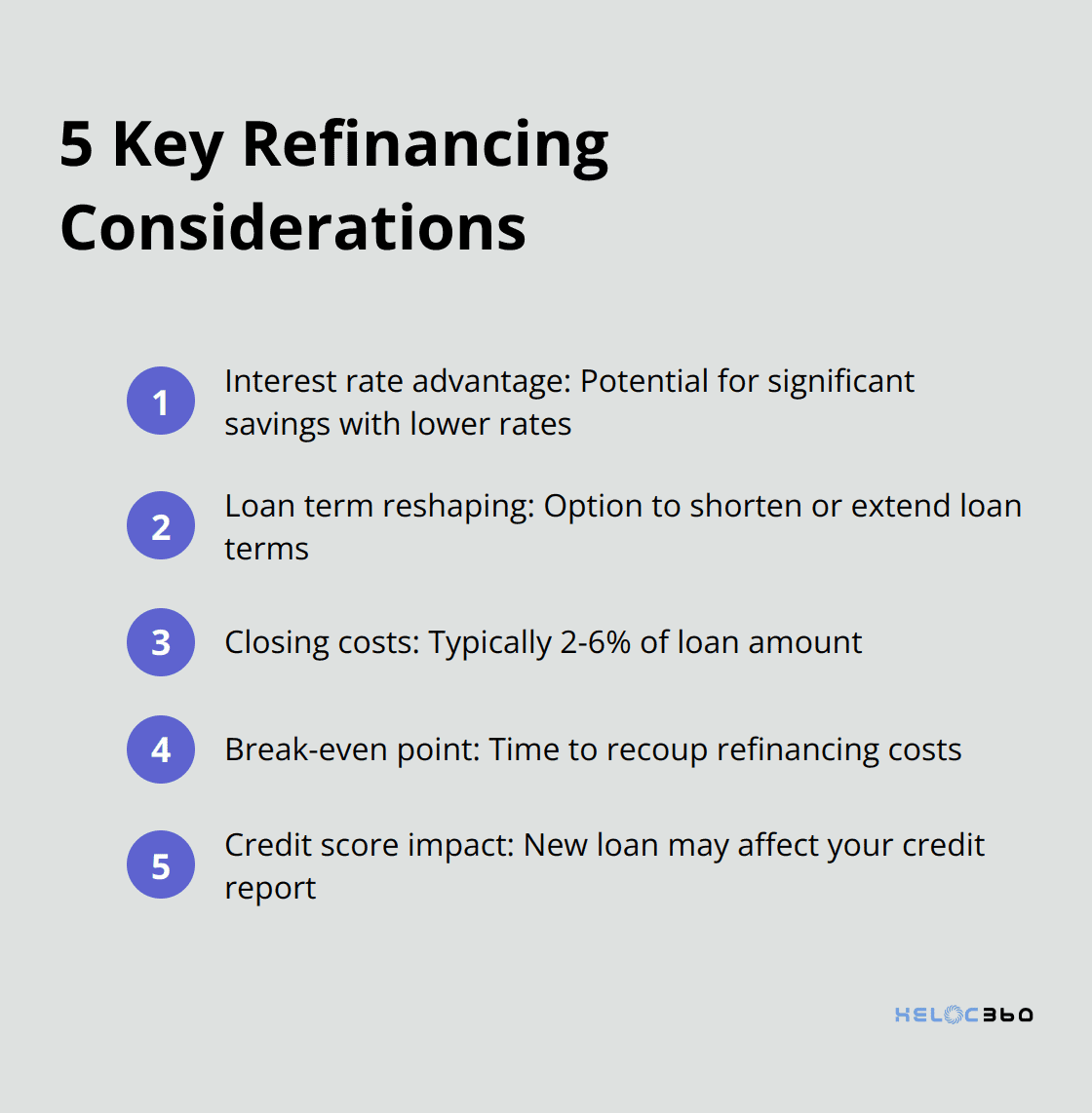

Refinancing your mortgage can transform your financial situation. Many homeowners consider refinancing to secure a lower interest rate. Mortgage rates continue to stay within a narrow range under 7% as of July 17, 2025. If you obtained your mortgage when rates were higher, refinancing could lead to substantial savings.

Consider this example: On a $300,000 mortgage, reducing your rate from 8% to 7% could save you about $200 per month. Over a 30-year loan, this amounts to $72,000 in savings. However, you must consider your break-even point – the time it takes for your monthly savings to offset the refinancing cost.

Reshaping Your Loan Terms

Loan modifications allow you to avoid the extensive process and costs associated with obtaining a new loan and can be a vital step in preventing foreclosure. You might choose to shorten your loan term from 30 years to 15 years, potentially saving tens of thousands in interest over the loan's life. Alternatively, extending your term can lower your monthly payments, freeing up cash flow for other financial goals.

Keep in mind that while lower monthly payments provide immediate relief, they may result in higher interest payments over time. Always calculate the total loan cost when considering term changes.

The Cost Factor

Refinancing comes with costs. Typical expenses include appraisal fees, title searches, and origination fees. These can total 2-6% of your loan amount. For a $300,000 mortgage, you might pay between $6,000 and $18,000 in closing costs.

Some lenders offer "no-cost" refinancing, but this usually means higher interest rates or rolling the costs into your loan balance. Either way, you pay for the refinance – it's just a matter of how and when.

Evaluating Your Options

Before proceeding, request a detailed breakdown of all fees and use a refinance calculator to determine if the long-term savings outweigh the upfront costs. If you plan to move within a few years, you might not recoup the refinancing costs.

Try to compare offers from multiple lenders (including HELOC360) to ensure you're getting the best deal. Look at the annual percentage rate (APR), which includes both the interest rate and fees, to get a true picture of the loan's cost.

Impact on Your Credit Score

Refinancing can affect your credit reports as a new loan. Several credit inquiries can impact your credit report, and skipping mortgage payments during the refinance process can also have an effect. If you're shopping around for rates, try to do so within a short timeframe (usually 14-45 days) as multiple inquiries for the same type of loan are often treated as a single inquiry by credit scoring models.

When considering your options, it's important to compare HELOC vs refinance to find the best fit for your financial goals. Additionally, if you're looking to consolidate high-interest debt, a cash-out refinance might be a suitable option to save money in the long run.

Final Thoughts

Choosing between a HELOC and refinancing will significantly impact your financial future. HELOCs offer flexibility and ongoing access to funds, while refinancing can potentially lower your interest rate or modify your loan terms. Your decision should depend on factors such as your current mortgage rate, equity needs, credit score, and long-term financial objectives.

We at HELOC360 understand the complexity of navigating these choices. Our platform helps homeowners make informed decisions about leveraging their home equity. We provide expert guidance and tailored solutions to explore your options and connect you with lenders that match your unique needs.

Whether you prefer a HELOC or consider refinancing, HELOC360 supports you throughout the process. We ensure you make the most of your home's value and achieve your financial goals. The right choice in the HELOC vs refinance debate depends on your individual circumstances.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.