- ***PAID ADVERTISEMENT**

- ACHIEVE LOANS – HOME EQUITY EXPERTISE

- FLEXIBLE FINANCING SOLUTIONS

- PERSONALIZED SUPPORT

- RECOMMENDED FICO SCORE: 640+

- COMPETITIVE RATES STREAMLINED APPLICATION PROCESS

Are you struggling to understand your HELOC payments? You’re not alone. Many homeowners find it challenging to navigate the complexities of Home Equity Lines of Credit.

At HELOC360, we’ve developed a powerful HELOC calculator to simplify this process for you. This tool will help you master your payments and make informed financial decisions.

- Approval in 5 minutes. Funding in as few as 5 days

- Borrow $20K-$400K

- Consolidate debt or finance home projects

- Fastest way to turn home equity into cash

- 100% online application

How HELOC Payments Work

The Two Phases of HELOC Payments

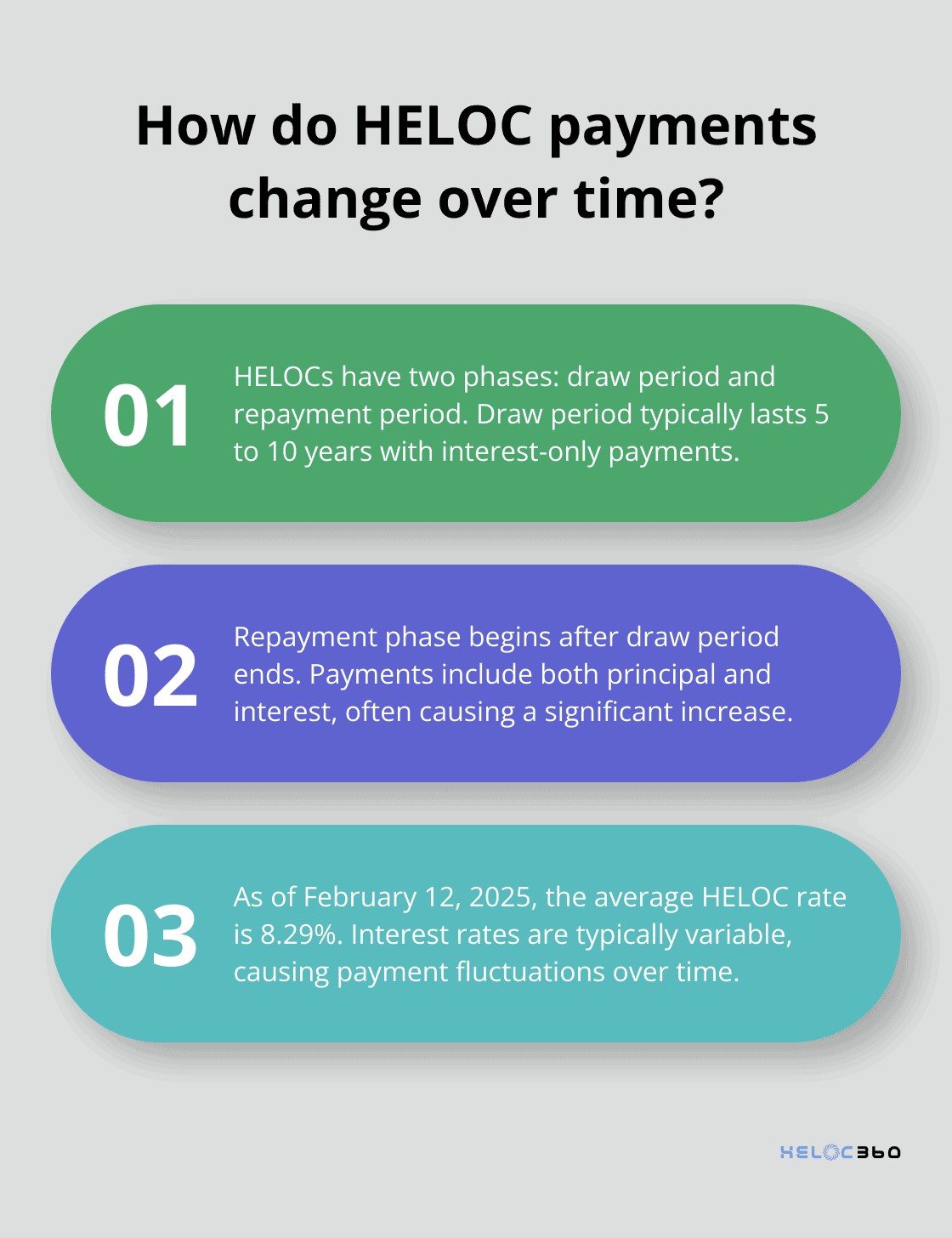

Home Equity Lines of Credit (HELOCs) have a unique payment structure that distinguishes them from traditional loans. This structure consists of two distinct phases: the draw period and the repayment period.

During the draw period (typically 5 to 10 years), you can borrow against your credit line as needed. Your payments often cover only the interest, which results in lower monthly obligations but can lead to potential risks if you don’t prepare for the transition to the repayment phase.

The repayment phase begins when the draw period ends. At this point, you can no longer borrow from the credit line, and your payments include both principal and interest. This transition often causes a significant increase in monthly payments, sometimes referred to as “payment shock”.

Factors That Influence Your HELOC Payments

Several elements affect your HELOC payments:

- Interest Rate: This is typically variable and tied to a benchmark like the prime rate. As of February 12, 2025, the average HELOC rate is 8.29%. The variability of this rate can cause your payments to fluctuate over time, which complicates budgeting.

- Credit Score: A higher score can lead to more favorable interest rates. For example, improving your credit score from 680 to 740 could lower your rate by 0.5%, potentially saving you $500 annually on a $100,000 HELOC.

- Loan Amount: The amount you borrow directly impacts your payments. A larger loan means higher payments, both during the draw and repayment periods.

- Draw Period Length: A longer draw period can result in lower initial payments but may lead to a more significant payment increase when the repayment period begins.

The Value of Accurate Payment Calculations

Calculating your HELOC payments accurately serves several important purposes:

- Effective Budgeting: Precise calculations help you meet your financial obligations without strain.

- Planning for Transitions: Accurate projections allow you to prepare for the shift from the draw period to the repayment period, avoiding unexpected financial stress.

- Comparing Offers: Precise calculations enable you to effectively compare different HELOC offers. For instance, a HELOC with a lower interest rate but higher fees might cost more long-term than one with a slightly higher rate but no fees.

- Determining Borrowing Capacity: Accurate calculations help you determine how much you can afford to borrow, preventing overextension that could lead to financial stress or default.

Using reliable tools to calculate your HELOC payments empowers you to make informed decisions that align with your financial goals and capabilities. As we move forward, we’ll introduce a powerful calculator designed to simplify this process and help you master your HELOC payments with ease.

How Our HELOC Calculator Works

Key Features of the HELOC Calculator

We developed a powerful HELOC calculator to simplify the complex world of Home Equity Lines of Credit. This tool gives you a clear picture of your potential payments and helps you make informed decisions about your financial future.

The calculator takes into account several important factors that influence your HELOC payments. These include your credit limit, interest rate, draw period length, and repayment period. When you input these details, you’ll get a comprehensive breakdown of your expected payments during both the draw and repayment phases.

One standout feature is the ability to see how different interest rate scenarios affect your payments. Given that HELOC rates are variable, this insight proves invaluable for long-term planning. The Federal Reserve cut interest rates three times in 2024, sending the average HELOC interest rate to a one-and-a-half-year low.

How to Use the Calculator Effectively

To get the most accurate results, gather all relevant information about your potential HELOC before using the calculator. This includes the credit limit you’re considering, the current interest rate offered by your lender, and the terms of the draw and repayment periods.

Once you input this data, experiment with different scenarios. Try adjusting the amount you plan to borrow or the length of your draw period. This will help you understand how these changes affect your payments and find the option that best fits your financial situation.

Benefits of Using a HELOC Calculator

A HELOC calculator offers several significant benefits. HELOCs have the most flexibility in terms of how much you can borrow and when you can pay it off, compared with other home equity products. First, it provides clarity on your future financial obligations. Many homeowners find themselves caught off guard by the jump in payments when transitioning from the draw period to the repayment period. Our calculator helps you avoid this surprise by clearly showing the difference between these two phases.

Moreover, this tool allows you to compare different HELOC offers effectively. When you input the terms from various lenders, you can see which one truly offers the best deal in the long run. This comparison goes beyond just looking at interest rates, taking into account the full payment structure over the life of the HELOC.

Lastly, the calculator serves as a powerful budgeting tool. It provides accurate payment projections, which helps you determine if a HELOC aligns with your current and future financial plans. This foresight can prevent overextension and ensure that your HELOC enhances (rather than hinders) your financial health.

The next chapter will explore strategies to optimize your HELOC payments, building on the insights gained from using the calculator. You’ll learn practical tips for managing interest rates, techniques for accelerating repayment, and ways to leverage your HELOC for various financial goals.

How to Optimize Your HELOC Payments

Manage Interest Rates Effectively

Interest rates significantly impact your HELOC payments. You can’t control market fluctuations, but you can minimize their impact. Pay attention to rate caps, which limit how much your rate can increase over time. For example, a 2% annual cap means your rate won’t increase more than 2% in a year, even if market rates soar higher.

Consider converting a portion of your HELOC balance to a fixed-rate option if your lender offers this feature. This approach shields part of your debt from rate fluctuations, providing more stability in your monthly payments.

Speed Up Your Repayment

Pay more than the minimum during the draw period to reduce your overall interest costs and prepare for the repayment phase. The Consumer Financial Protection Bureau states that some home equity plans permit consumers to repay all or part of the balance during the draw period.

Set up automatic extra payments. An additional $100 per month on a $50,000 HELOC could save you thousands in interest over the life of the loan and shorten your repayment period by years.

Use Your HELOC Strategically

Your HELOC can become a powerful financial tool when used wisely. Consider using it for debt consolidation. If you have high-interest credit card debt, transfer it to your HELOC to save money. For instance, if you’re paying 18% on credit card balances, moving that debt to a HELOC with a lower rate could significantly cut your interest costs.

Another approach involves using your HELOC for home improvements that increase your property value. The National Association of Realtors found that certain home improvements can recover a high percentage of their cost, with refinishing hardwood floors recovering 147% and new wood flooring recovering 118%.

Monitor Your HELOC Terms

Stay informed about your HELOC terms and conditions. Regularly review your statements and keep track of any changes in interest rates or payment structures. This vigilance allows you to adjust your strategy as needed and avoid any surprises in your financial obligations.

Seek Professional Advice

Try to consult with a financial advisor or a HELOC specialist to create a personalized strategy for your situation. These professionals can provide insights on market trends, tax implications, and optimization techniques specific to your financial goals and circumstances.

Final Thoughts

Understanding and managing your HELOC payments will improve your financial well-being. Our HELOC calculator provides valuable insights into your payment structure, allowing you to make informed decisions about borrowing and repayment strategies. This tool empowers you to plan for both draw and repayment periods, avoiding unexpected financial strain and maximizing the benefits of your home equity line of credit.

We at HELOC360 encourage you to use our HELOC calculator to explore different scenarios and find the best approach for your unique financial situation. You can input various credit limits, interest rates, and term lengths to visualize how these factors impact your payments over time. This knowledge proves invaluable when comparing offers from different lenders or deciding how much to borrow.

A HELOC is a powerful financial tool when used wisely. It can help you fund home improvements, consolidate high-interest debt, or provide a financial safety net. HELOC360 offers expert guidance, connects you with suitable lenders, and provides resources to help you make the most of your home equity.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.