Mastering HELOC Amortization Schedules

Table of Contents

HELOC amortization can be a complex topic for many homeowners. Understanding how your payments are structured over time is essential for managing your home equity line of credit effectively.

At HELOC360, we've seen firsthand how mastering HELOC amortization schedules can lead to better financial decisions and significant savings. This guide will break down the key components of HELOC amortization and provide practical strategies to optimize your borrowing experience.

What's a HELOC Amortization Schedule?

Understanding HELOC Basics

A Home Equity Line of Credit (HELOC) offers homeowners a flexible way to borrow against the available equity in their home, using the house as collateral for the line of credit. To use this financial tool effectively, you must understand how you'll repay the loan. This is where amortization schedules become essential.

Decoding HELOC Amortization

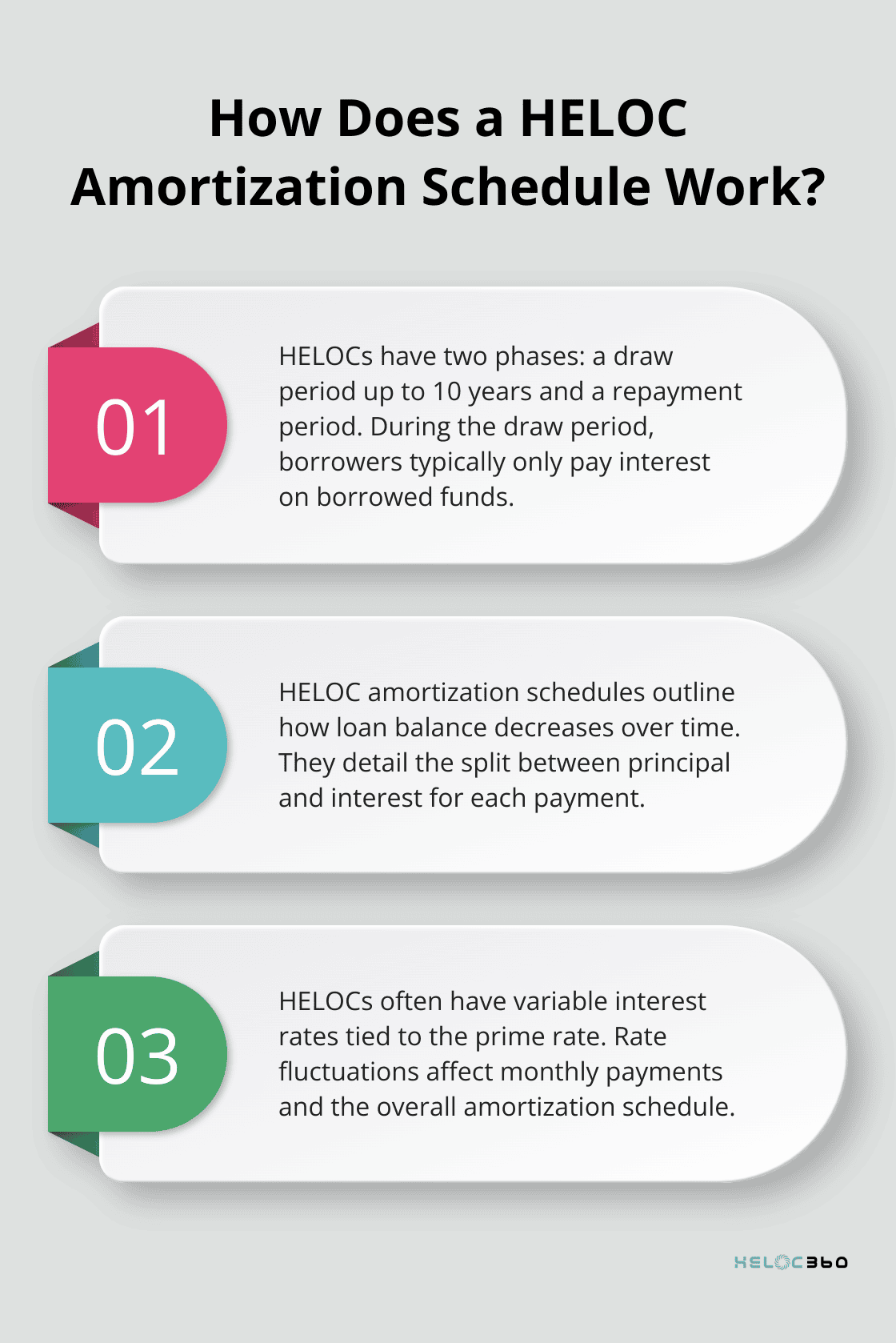

An amortization schedule for a HELOC outlines how your loan balance will decrease over time as you make payments. It serves as a roadmap for your loan repayment, detailing how each payment splits between principal and interest.

HELOCs differ from traditional loans by having two distinct phases:

- Draw Period: This typically lasts up to 10 years. During this time, you can borrow funds as needed and are usually only required to pay interest on what you borrow.

- Repayment Period: Following the draw period, you start to pay back both principal and interest.

The Importance of Amortization Schedules

Knowing your HELOC's amortization schedule is important for several reasons:

- Budget Planning: It helps you anticipate future payment amounts, especially when you transition from interest-only to full payments.

- Interest Savings: Understanding how much of each payment goes to interest can motivate you to make extra principal payments (potentially saving thousands in interest over the loan's life).

- Equity Building: The schedule shows how quickly you rebuild equity in your home, which is critical for future financial planning.

Key Components to Monitor

When you review your HELOC amortization schedule, pay attention to these elements:

- Payment Amount: This can change, especially when moving from the draw to the repayment period.

- Interest Rate: HELOCs often have variable rates typically tied to the prime rate. As the prime rate fluctuates, so will the interest rate on your HELOC, affecting your monthly payments.

- Principal Balance: Track how quickly your balance decreases over time.

- Interest Paid: Keep an eye on the total interest you'll pay over the life of the loan.

- Payoff Date: Know when you'll fully repay the loan if you stick to the minimum payments.

Flexibility in HELOC Amortization

Your HELOC amortization schedule isn't fixed. You can often make extra payments or adjust your borrowing to optimize your repayment strategy. Stay proactive and don't hesitate to reach out to financial advisors or use specialized tools to make the most of your home equity.

As we move into the next section, we'll explore how to calculate HELOC amortization, including the nuances of draw periods versus repayment periods and the factors that affect these calculations.

How HELOC Payments Function

Understanding the Draw Period

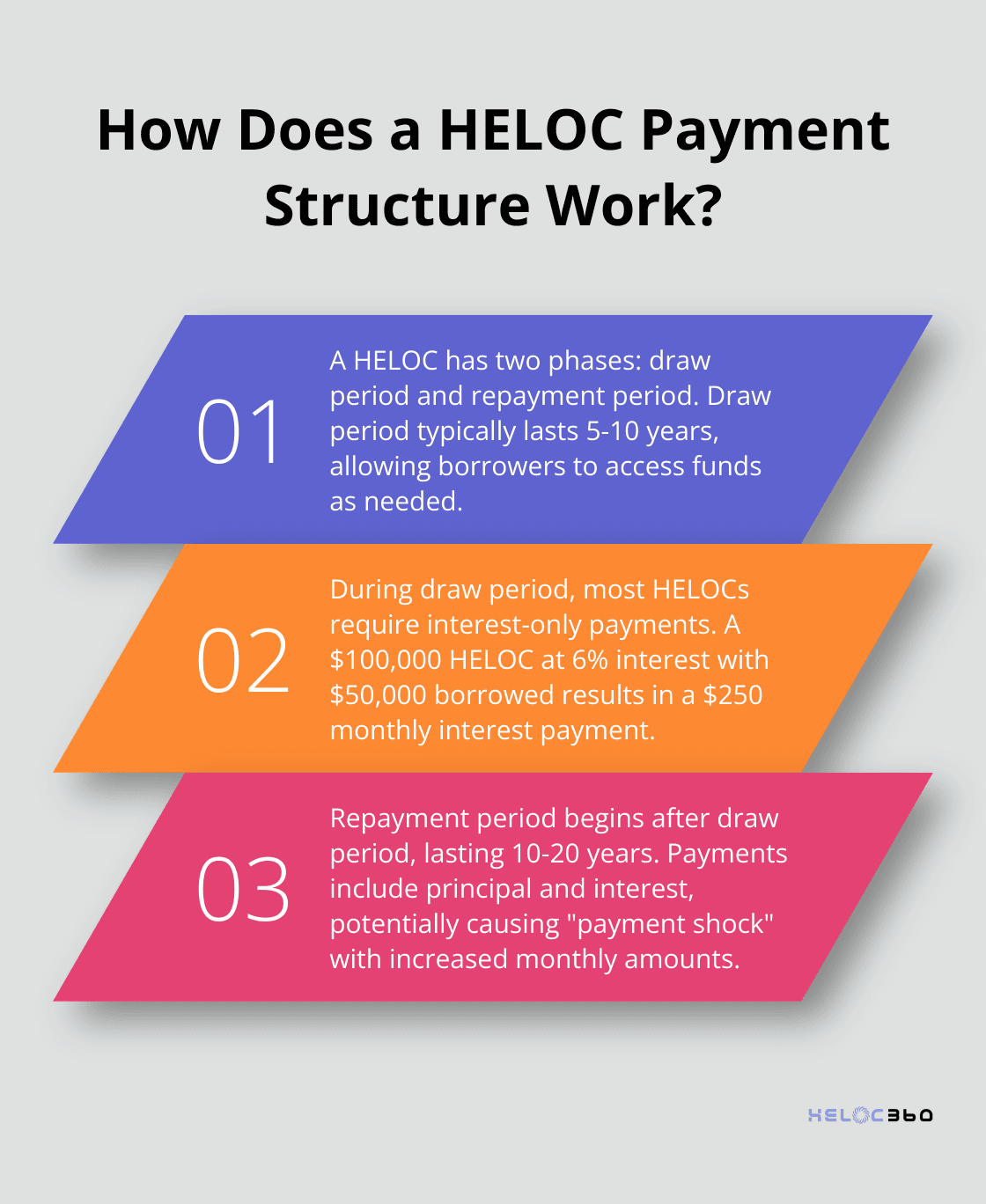

The draw period of a Home Equity Line of Credit (HELOC) typically spans 5 to 10 years. During this time, borrowers can access funds from their credit line as needed. Most HELOCs only require interest payments in this phase, resulting in relatively low monthly obligations. However, these payments do not reduce the principal balance.

For instance, a $100,000 HELOC with a 6% interest rate and a borrowed amount of $50,000 would result in a monthly interest-only payment of approximately $250. It's important to note that HELOC rates are directly tied to the Prime rate, so when the Prime rate rises or falls, your interest rate and monthly payment can change, too.

Navigating the Repayment Period

The repayment period begins once the draw period ends. At this point, payments include both principal and interest, often calculated over a 10 to 20-year term. This transition can lead to a substantial increase in monthly payments (sometimes referred to as "payment shock"). Once your draw period ends, your repayment begins, and you can only continue paying back what you borrowed – not borrow more.

Using the previous example, a $50,000 balance at the end of the draw period entering a 15-year repayment term at 6% interest would result in a monthly payment of about $422, covering both principal and interest.

Key Factors Influencing Amortization

Several elements can impact a HELOC amortization schedule:

- Interest Rate Fluctuations: Most HELOCs have variable rates. Even small rate increases can significantly affect payments and total interest paid.

- Additional Borrowing: Continued borrowing during the draw period increases the balance and future payments.

- Extra Payments: Making additional payments during the draw period can reduce the principal balance, potentially lowering payments during the repayment phase.

- Loan Terms: The duration of draw and repayment periods affects the speed of loan repayment and the size of payments.

Strategies for Effective HELOC Management

Active management of your HELOC can lead to better financial outcomes. Try to:

- Regularly review your amortization schedule

- Make extra payments when possible (especially during the draw period)

- Monitor interest rate changes and adjust your strategy accordingly

Tools for HELOC Planning

Various online calculators and tools can help visualize different HELOC scenarios. These resources allow borrowers to input different variables (such as interest rates, loan terms, and payment amounts) to see how they affect the overall amortization schedule.

HELOC360 offers a comprehensive platform for this purpose, providing tools to help users visualize various scenarios and make informed decisions about HELOC usage and repayment strategies.

The next section will explore strategies to optimize your HELOC amortization, including methods to reduce interest payments and balance HELOC obligations with other financial goals.

How to Optimize Your HELOC Amortization

Make Extra Payments to Reduce Interest

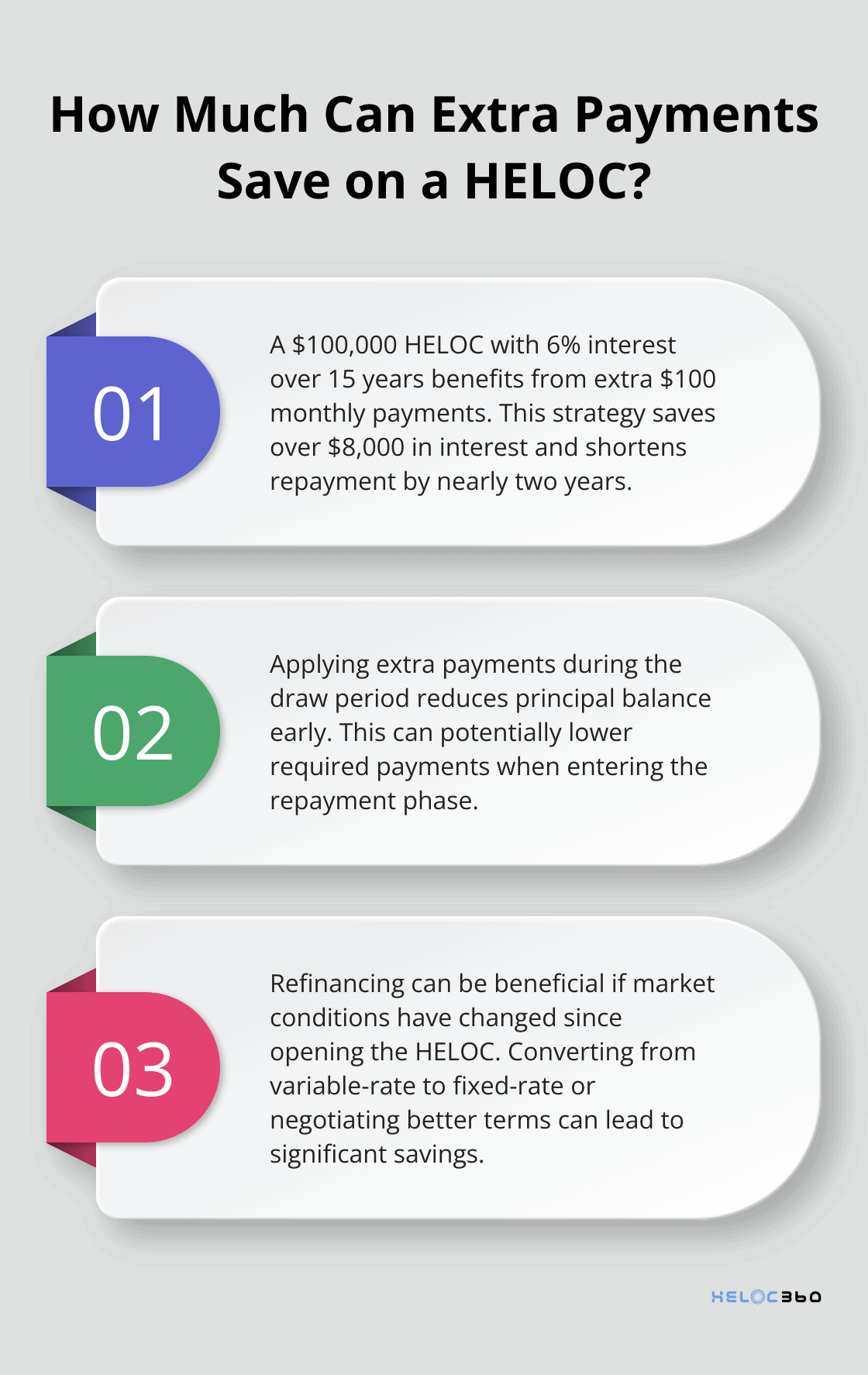

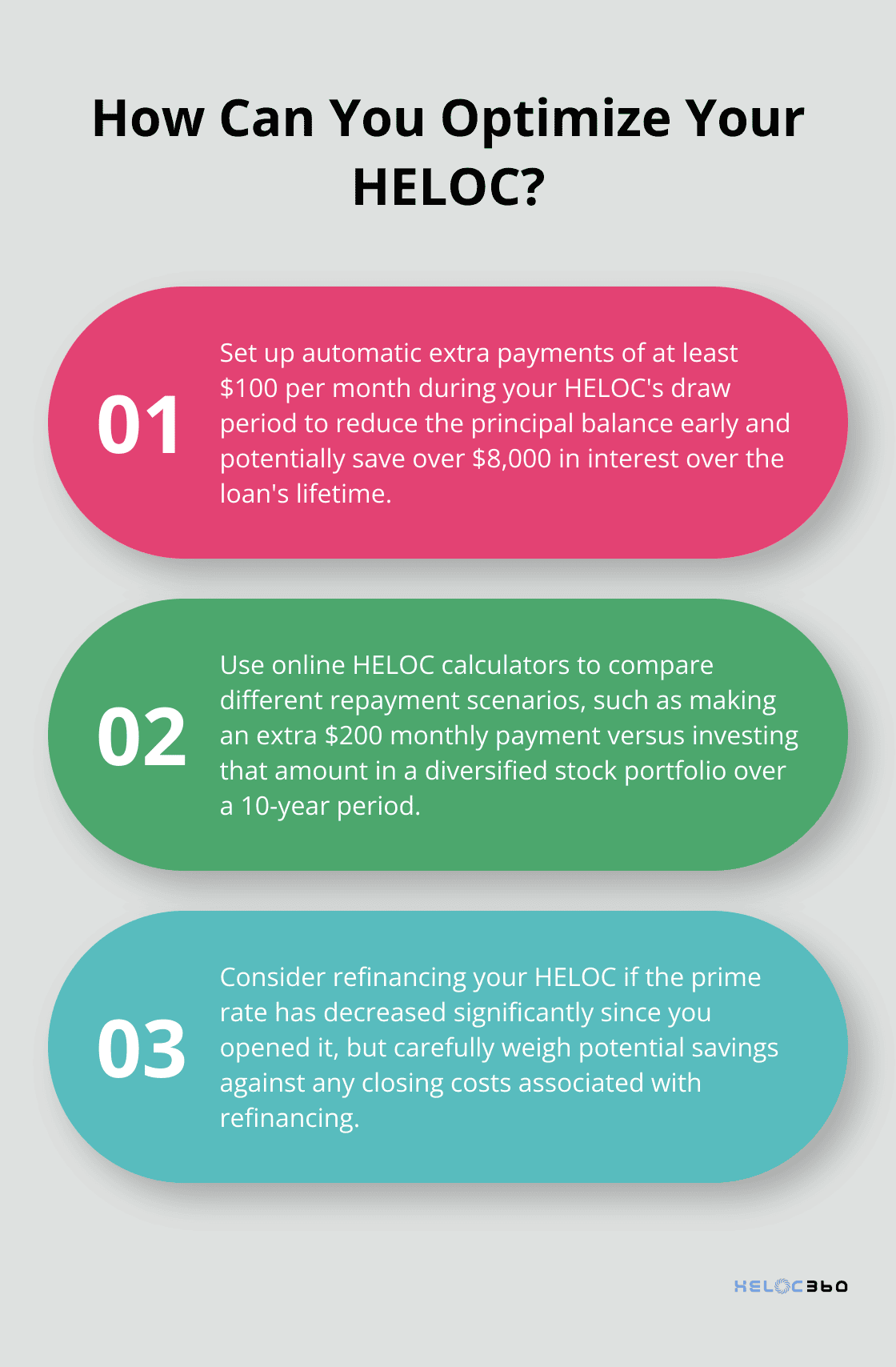

One of the most effective ways to optimize your HELOC involves making extra payments. Even small additional payments can have a significant impact over time. For example, a $100,000 HELOC with a 6% interest rate and a 15-year repayment term could benefit from an extra $100 monthly payment. This strategy could save over $8,000 in interest and shorten the repayment period by nearly two years.

To maximize the benefit of extra payments, apply them during the draw period. This action reduces your principal balance early on, potentially lowering your required payments when you enter the repayment phase. Some homeowners choose to make principal payments equal to their interest charges during the draw period, effectively treating their HELOC like a traditional amortizing loan from the start.

Consider Refinancing Options

If market conditions have changed since you opened your HELOC, refinancing might prove a smart move. This could involve converting your variable-rate HELOC to a fixed-rate home equity loan, or negotiating better terms with your current lender.

For instance, if you opened a HELOC when the prime rate was 5% and it's now 3%, you might save thousands by refinancing. However, factor in any closing costs associated with refinancing. Use comparison tools to weigh the potential savings against the costs of refinancing.

Use Technology for Scenario Planning

Modern tools can help you visualize different repayment scenarios. Many platforms allow you to input various payment amounts, interest rates, and terms to see how they affect your overall amortization schedule. This can prove particularly useful when deciding between making extra payments or investing that money elsewhere.

You might compare the interest savings from an extra $200 monthly payment against the potential returns from investing that same amount in a diversified stock portfolio. Over a 10-year period, the difference could prove substantial, helping you make an informed decision about the best use of your funds.

Balance HELOC Optimization with Other Financial Goals

While optimizing your HELOC holds importance, it shouldn't come at the expense of other financial priorities. Consider your overall financial picture when deciding how aggressively to pay down your HELOC.

A study by the Federal Reserve Bank of New York found that households with HELOCs were more likely to maintain emergency savings and invest in retirement accounts compared to those without HELOCs. This suggests that many homeowners successfully balance HELOC management with other financial goals.

Try to prioritize high-interest debt repayment, maintain an emergency fund, and continue contributing to retirement accounts. If you have extra cash flow after addressing these areas, then consider accelerating your HELOC repayment.

The right strategy depends on your individual financial situation (including factors such as income, expenses, and long-term goals). Financial advisors can help you create a personalized plan that aligns with your broader financial objectives while optimizing your HELOC usage.

Final Thoughts

HELOC amortization schedules provide homeowners with a roadmap for effective home equity management. You can minimize interest costs and accelerate repayment by understanding draw and repayment periods. This knowledge allows you to align your HELOC strategy with your broader financial objectives.

HELOCs offer powerful financial tools that can open doors to new opportunities when used wisely. However, the complexities of HELOC amortization schedules often present challenges for many homeowners. HELOC360 simplifies this process and provides the necessary tools and knowledge to maximize your home equity potential.

Our platform at HELOC360 offers comprehensive support for your HELOC journey (from comparing scenarios to connecting you with suitable lenders). You can confidently explore your options, optimize your HELOC amortization, and unlock the full value of your home with HELOC360. Take control of your financial future today and discover how we can help you achieve your goals.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.