Mastering HELOC Repayment Strategies

Table of Contents

Home Equity Lines of Credit (HELOCs) offer homeowners financial flexibility, but mastering HELOC repayment is crucial for long-term financial health.

At HELOC360, we've seen many homeowners struggle with repayment strategies, often leading to financial stress.

This guide will walk you through effective HELOC repayment techniques, common pitfalls to avoid, and how to optimize your repayment plan for maximum benefit.

Understanding HELOC Repayment Terms

Draw Period vs. Repayment Period

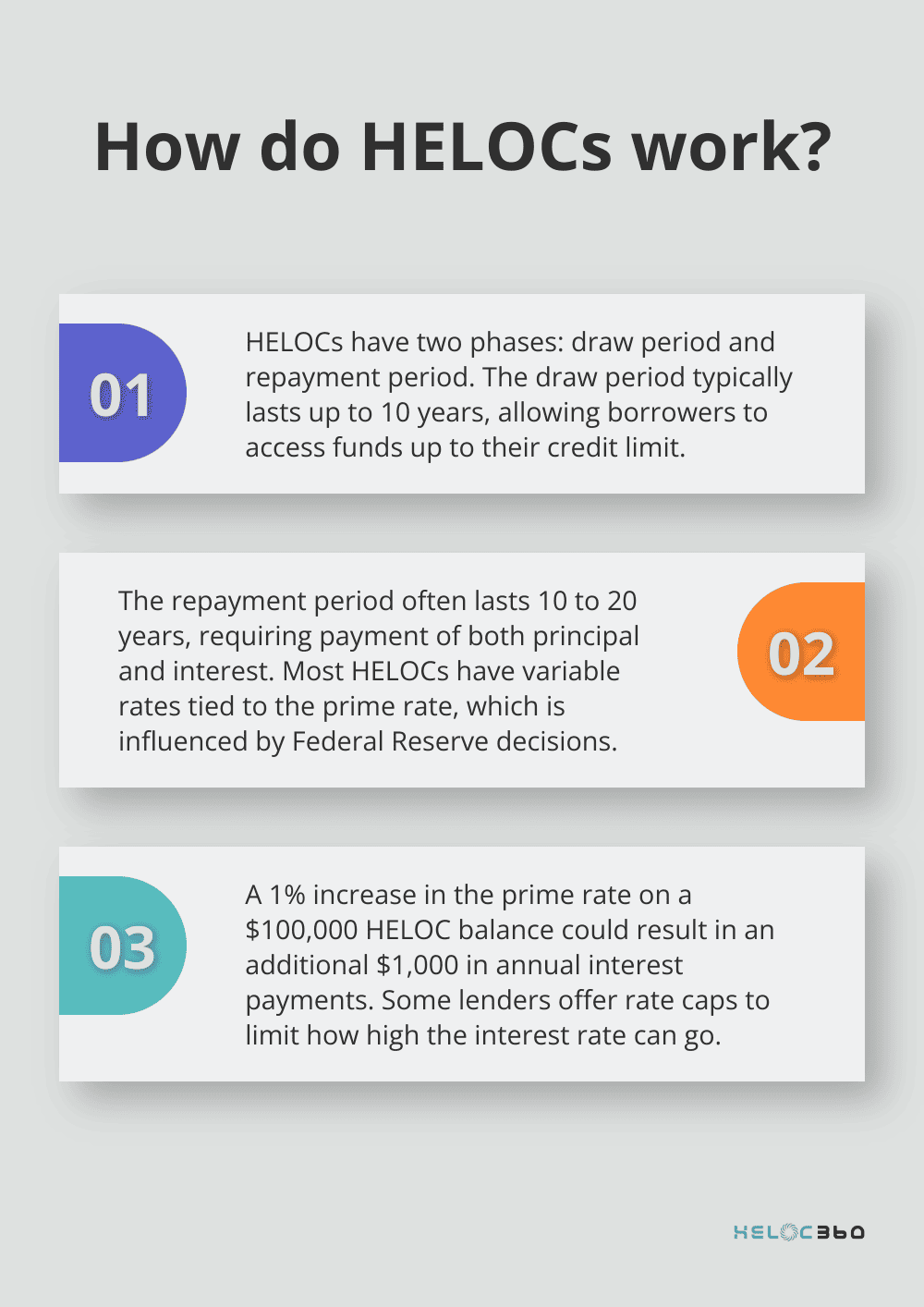

Home Equity Lines of Credit (HELOCs) operate in two distinct phases: the draw period and the repayment period. The draw period typically lasts up to 10 years, during which borrowers can access funds up to their credit limit. During this time, you're usually only required to pay interest on what you borrow.

When the draw period ends, the repayment period begins. This phase often lasts 10 to 20 years and requires borrowers to pay both principal and interest. The shift can shock those unprepared for the increase in monthly payments.

Types of HELOC Repayment Structures

HELOCs offer various repayment structures. The most common is the variable-rate HELOC, where interest rates fluctuate based on market conditions. Fixed-rate options provide stability but often come with a higher initial rate. Some lenders offer hybrid models, allowing borrowers to lock in rates on portions of their balance.

A less common but potentially beneficial structure is the interest-only HELOC. While it offers lower initial payments, it can lead to a significant payment shock when the repayment period begins.

Impact of Interest Rates on HELOC Repayments

Interest rates play a crucial role in HELOC repayments. Most HELOCs tie to the prime rate, which Federal Reserve decisions influence. When the Fed raises rates, HELOC payments typically increase. For example, a 1% increase in the prime rate on a $100,000 HELOC balance could result in an additional $1,000 in annual interest payments.

Some lenders offer rate caps, which limit how high your rate can go. These caps can provide peace of mind but may come with trade-offs like higher initial rates or fees. Always read the fine print and ask about rate caps when shopping for a HELOC.

Strategies to Manage Rate Changes

To mitigate the impact of rate changes, consider making principal payments during the draw period. This strategy can reduce your overall balance and lessen the effect of rate increases. Additionally, setting up automatic payments can help ensure you never miss a due date, potentially qualifying you for rate discounts offered by some lenders.

As we move forward, it's important to explore effective strategies for HELOC repayment that can help you navigate these terms and structures more efficiently.

How to Optimize Your HELOC Repayment

Pay More Than the Minimum During the Draw Period

One of the most effective strategies involves making more than the minimum payments during your draw period. While it might tempt you to only pay interest, adding even small amounts to your principal can make a big difference. For example, if you have a $100,000 HELOC with a 5% interest rate, paying an extra $100 per month towards the principal could save you over $7,000 in interest over a 15-year repayment period.

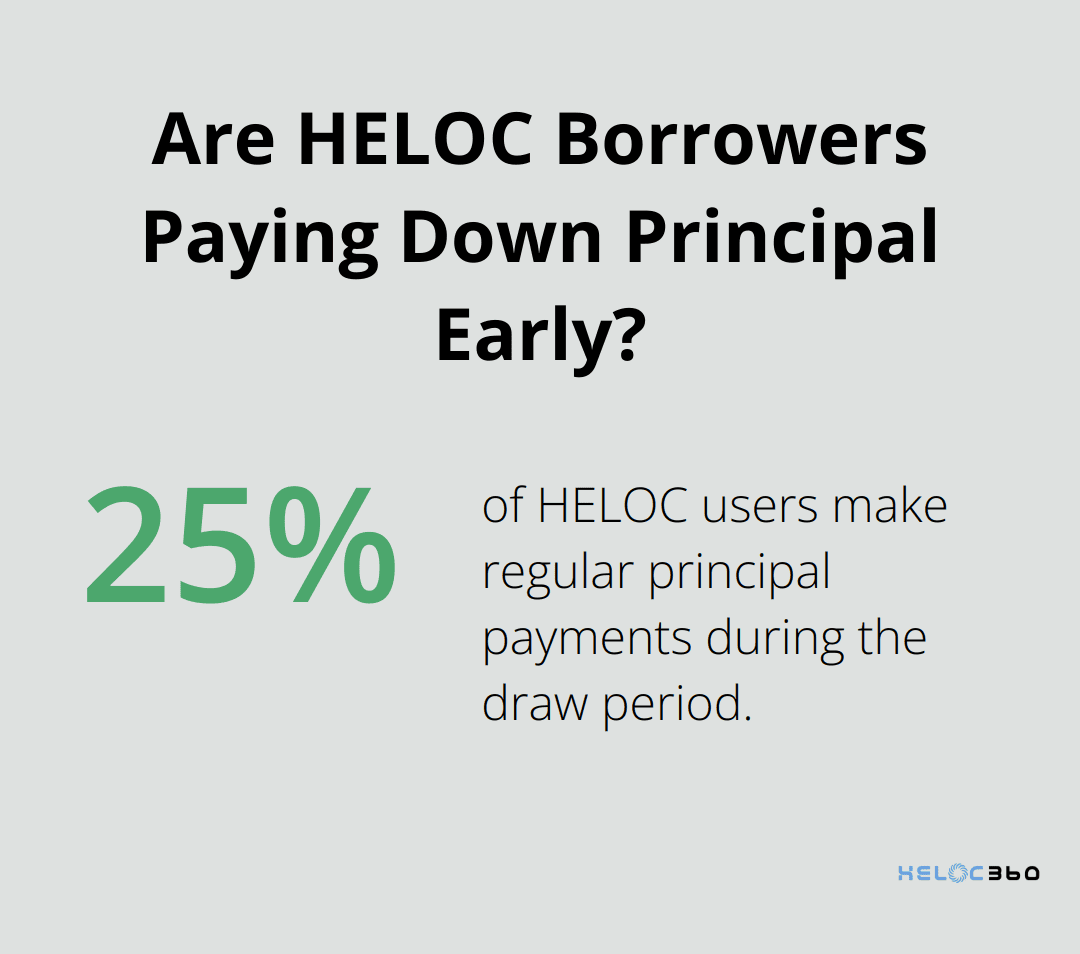

Many HELOC borrowers overlook this opportunity. A study by the Federal Reserve Bank of Philadelphia found that only about 25% of HELOC users make regular principal payments during the draw period. You can significantly reduce your overall debt burden by joining this savvy minority.

Convert to a Fixed-Rate Option

If you worry about interest rate volatility, converting part or all of your HELOC balance to a fixed rate can provide stability. Many lenders offer this option (sometimes called a "HELOC fix"). It allows you to freeze a portion or all of your balance at a fixed interest rate, protecting you against market fluctuations that impact rates.

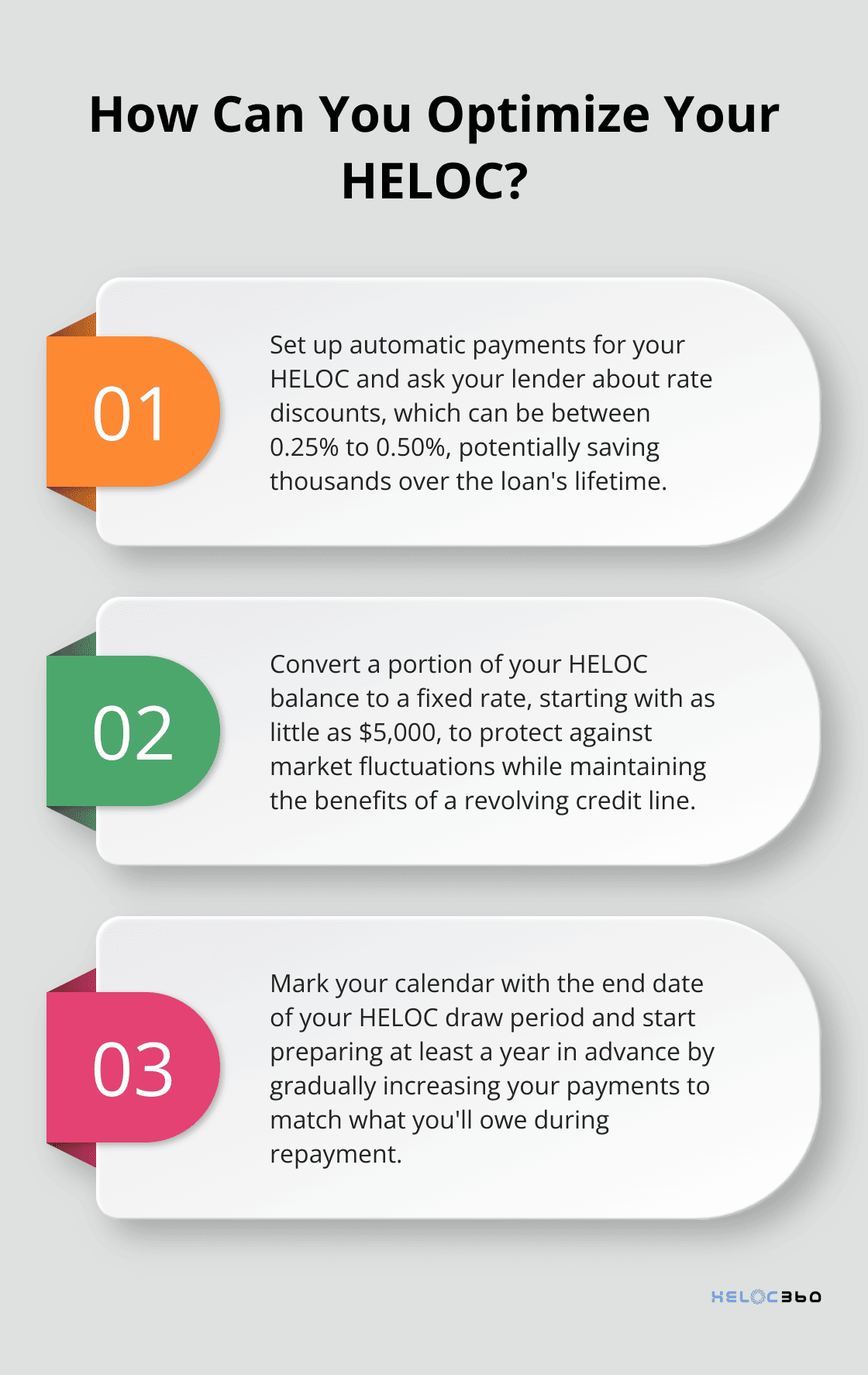

For instance, some banks offer a fixed-rate lock option on portions of HELOC balances as low as $5,000. This flexibility allows you to hedge against rate increases while maintaining the benefits of your HELOC's revolving credit line.

Explore Refinancing Options

Refinancing your HELOC can be a smart move if you can secure better terms. This is particularly relevant if your financial situation has improved since you first obtained the HELOC.

When you consider refinancing, look beyond just the interest rate. Pay attention to factors like closing costs, the new repayment term, and any changes to your credit limit. Some lenders offer refinancing options that allow you to extend your draw period, potentially giving you more financial flexibility.

Leverage Your Home's Appreciation

If your home has significantly appreciated in value since you took out your HELOC, you might negotiate better terms with your lender. A higher home value means more equity, which can translate to a lower interest rate or increased borrowing limit. Existing-home sales fell 4.9% month-over-month to a seasonally adjusted rate of 4.08 million in January 2025. Year-over-year, sales improved 2.0%.

Set Up Automatic Payments

Automating your HELOC payments not only ensures you never miss a due date but can also lead to rate discounts. Many lenders offer a 0.25% to 0.50% rate reduction for setting up automatic payments from a checking account. Over the life of your HELOC, this small reduction can result in thousands of dollars saved.

These strategies can help you take control of your HELOC repayment and potentially save significant amounts of money. However, optimizing your repayment is only part of the equation. It's equally important to avoid common pitfalls that can derail even the best-laid plans. Let's explore these potential traps and how to sidestep them in the next section.

How to Avoid HELOC Repayment Traps

The Draw Period Temptation

During the draw period, borrowers have the flexibility to borrow and repay funds multiple times, up to the approved credit limit. This flexibility can lead to overextension, creating future stress when the repayment period begins.

To avoid this trap, set a personal limit on your HELOC usage. Try to keep your utilization below 50% of your credit limit. This approach provides a buffer against market fluctuations and helps you manage future payments more effectively.

The Rate Change Blindside

Interest rate changes can significantly impact your HELOC payments. Most HELOCs have variable interest rates, meaning your interest rate will adjust many times over the course of the loan.

To stay ahead, set up rate change alerts with your lender or through financial apps. Consider creating a budget that accounts for potential rate increases. This proactive approach can help you adjust your finances before rate changes strain your budget.

The End-of-Draw Surprise

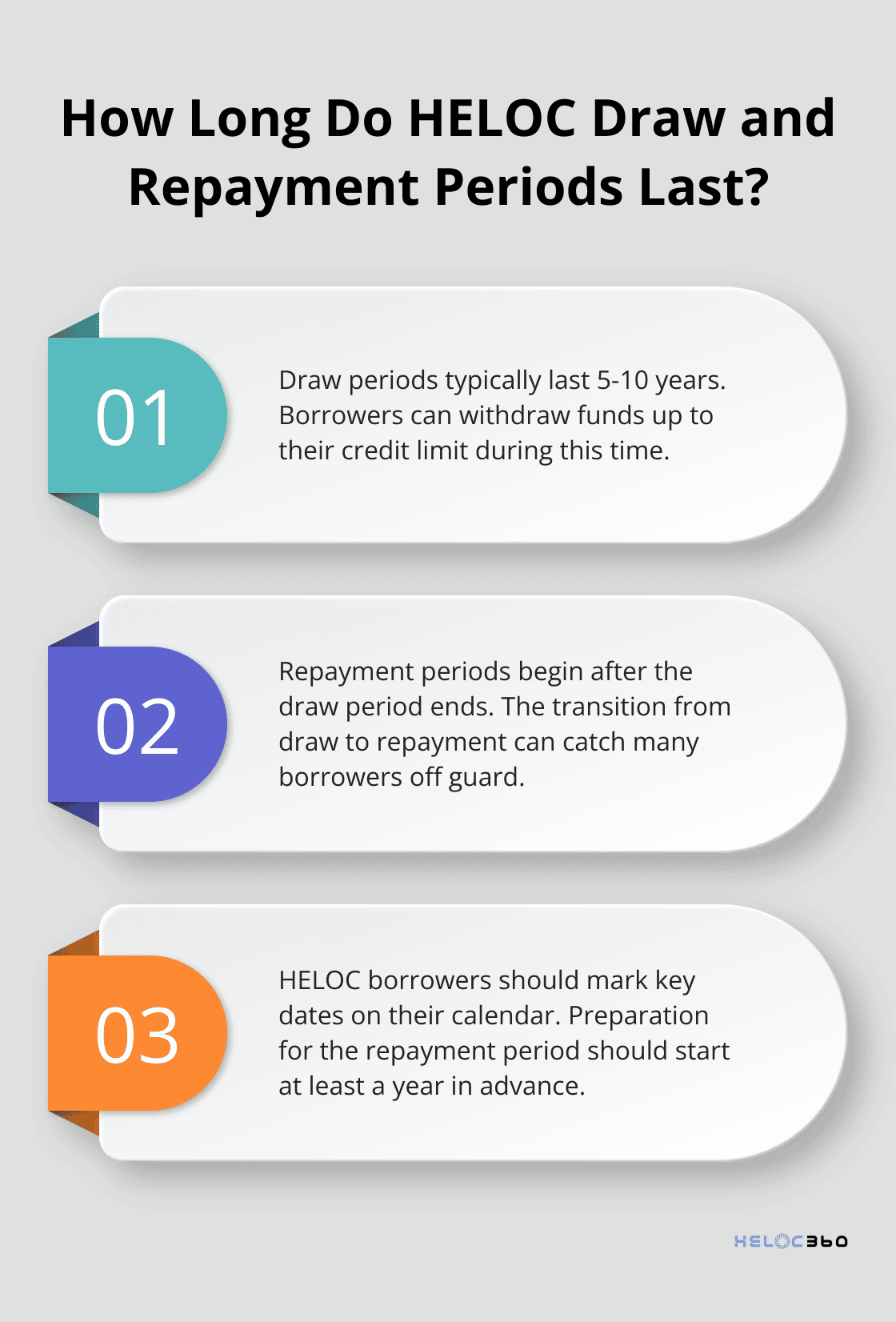

The transition from the draw period to the repayment period catches many HELOC borrowers off guard. The draw period typically lasts 5-10 years. During this time, borrowers can withdraw funds as needed up to their credit limit.

To avoid surprises, mark your calendar with key HELOC dates, including the end of your draw period. Start preparation at least a year in advance by gradually increasing your payments to match what you'll owe during repayment. This strategy can soften the transition and help you adjust your budget more smoothly.

The Minimum Payment Trap

Many borrowers fall into the trap of making only minimum payments during the draw period. While this approach might seem attractive in the short term, it can lead to a significant increase in your overall debt.

Instead, make a habit of paying more than the minimum whenever possible. Even small additional payments towards the principal can make a substantial difference over time. This practice will reduce your overall balance and make the transition to the repayment period less jarring.

The Market Value Miscalculation

Homeowners often overlook the impact of market fluctuations on their HELOC. A decrease in your home's value can result in a reduction of your credit line or even trigger a demand for immediate repayment.

To mitigate this risk, stay informed about your local real estate market. Regularly check your home's estimated value using online tools or consult with a local real estate professional. If you notice a downward trend, consider paying down your HELOC balance to maintain a healthy loan-to-value ratio.

Final Thoughts

HELOC repayment strategies empower homeowners to leverage their home equity effectively. Understanding draw and repayment periods, exploring repayment structures, and monitoring interest rate impacts allow confident HELOC navigation. Proactive management helps avoid common pitfalls, such as overextension during the draw period and rate change surprises.

Small actions lead to significant savings over time. Setting personal limits on HELOC usage, staying alert to rate changes, and preparing for the end of the draw period can prevent financial stress. Making additional principal payments or setting up automatic payments will optimize your HELOC management.

HELOC360 specializes in helping homeowners unlock their home equity's full potential. Our platform simplifies the process, offering expert guidance and connecting you with suitable lenders. HELOC360 provides tailored solutions to help you achieve your financial goals, whether you're funding renovations, consolidating debt, or creating financial flexibility.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.