Navigating Variable HELOC Rates in 2025

Table of Contents

Variable HELOC rates are shaking up the home equity market in 2025. At HELOC360, we've seen a surge of homeowners seeking guidance on navigating these fluctuating rates.

Understanding the ins and outs of HELOC variable rates is key to making informed decisions about your home equity. This post will explore current trends, strategies for managing rate changes, and how to leverage variable rates to your advantage.

What Are Variable HELOC Rates?

The Mechanics of Variable HELOC Rates

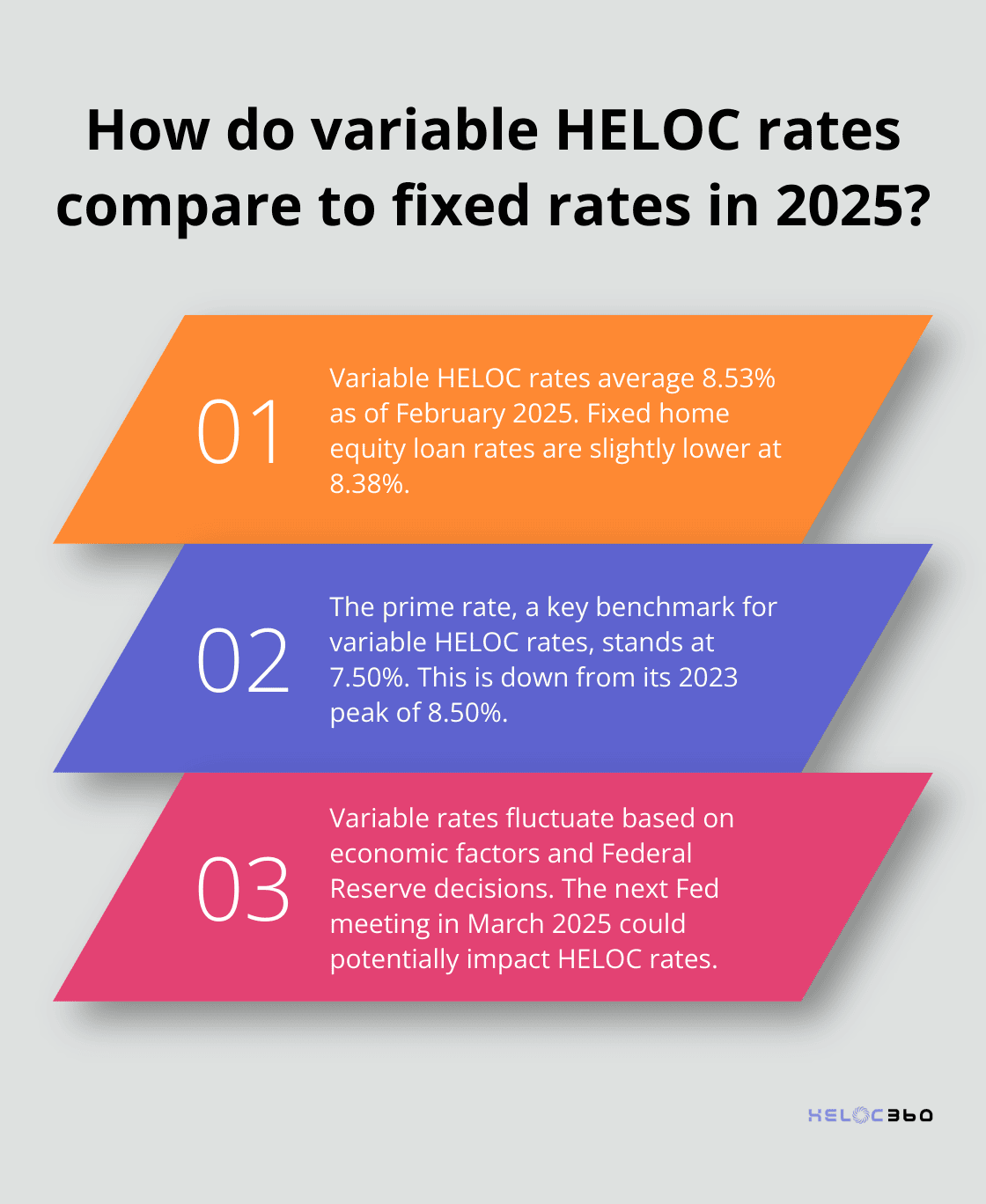

Variable HELOC rates form a key component of Home Equity Lines of Credit that significantly impact borrowing costs. These rates fluctuate based on a benchmark index, typically the prime rate. As of February 2025, the prime rate stands at 7.50%, down from its 2023 peak of 8.50%. Your HELOC rate changes as the index moves, directly affecting your monthly payments.

For example, if your HELOC has a margin of 1% above prime, your current rate would be 8.50%. However, this rate isn't fixed and can change monthly or quarterly (depending on your lender's terms).

Factors Driving Rate Changes

Several elements influence HELOC rate fluctuations:

- Federal Reserve Decisions: The Fed's monetary policy directly impacts the prime rate. With another Federal Reserve meeting set for March, potential home equity borrowers should consider their moves now.

- Economic Indicators: Inflation (currently at 2.7%) and GDP growth play crucial roles. Higher inflation often leads to rate increases to curb economic overheating.

- Market Conditions: Broader financial market trends can indirectly affect HELOC rates through their impact on the prime rate.

Variable vs. Fixed-Rate HELOCs

While variable rates offer potential savings when rates drop, they also carry risks. Fixed-rate HELOCs, though less common, provide stability but often at a higher initial rate.

Recent data shows variable HELOC rates average 8.53%, while fixed home equity loan rates are slightly lower at 8.38%. This small difference highlights the current preference for stability in the market.

Homeowners who can tolerate some uncertainty often choose variable rates for their potential savings. However, those planning large, immediate withdrawals might prefer the predictability of fixed rates.

The Impact on Borrowers

The choice between variable and fixed rates can significantly affect a homeowner's financial strategy. Variable rates can lead to lower initial payments, but they also introduce an element of unpredictability. Fixed rates, while potentially higher at the outset, offer peace of mind through consistent payments.

Consider a $100,000 HELOC with a 10-year draw period and a 20-year repayment period. This calculator helps determine both your interest-only payments and the impact of choosing to make additional principal payments.

Understanding these dynamics proves essential for making informed decisions about your home equity. As we move forward, we'll explore current trends and strategies to help you navigate the variable HELOC landscape in 2025.

What's Happening with HELOC Rates in 2025?

Recent Rate Movements

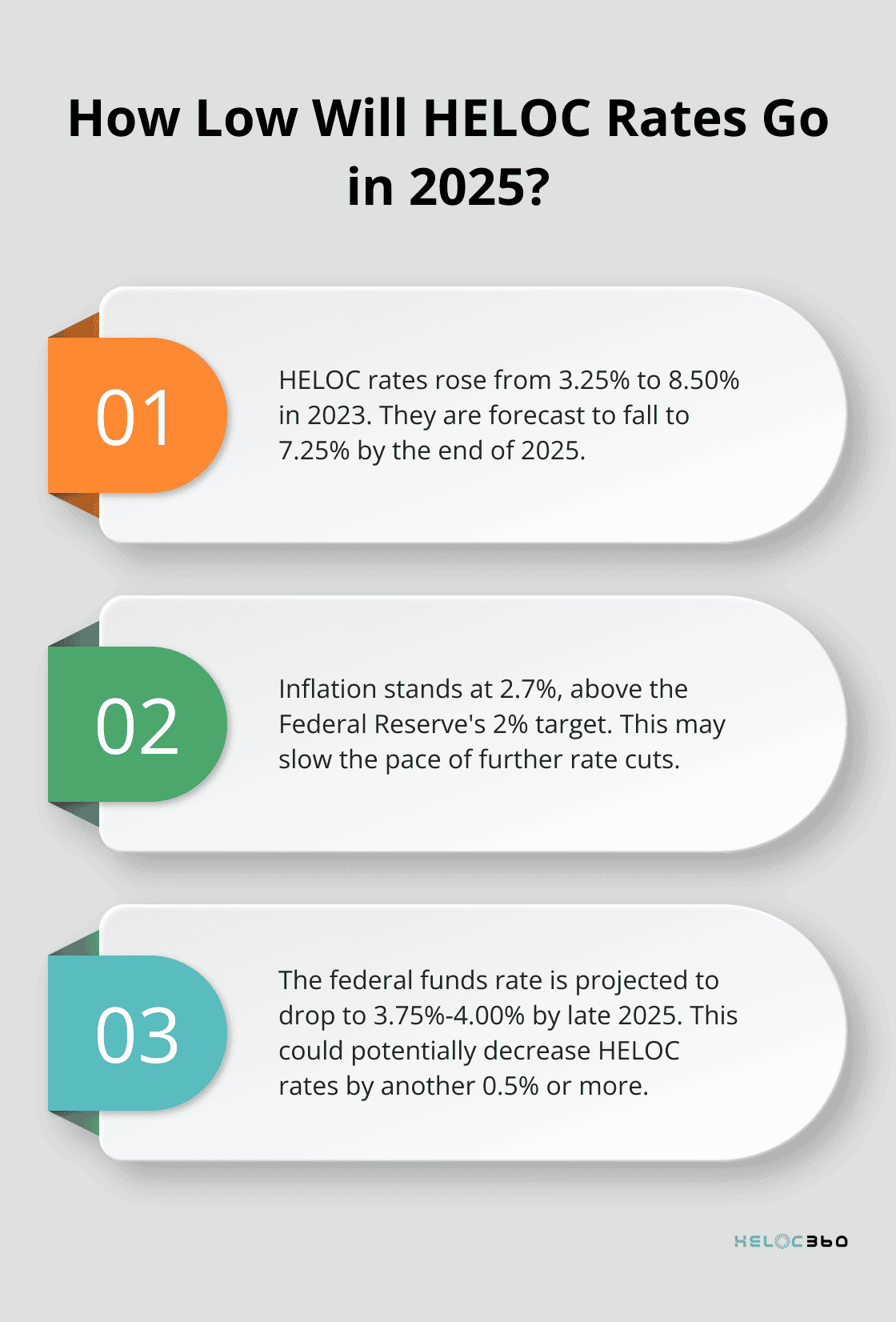

HELOC rates have experienced significant fluctuations since early 2022. They rose from 3.25% to 8.50% in 2023, mirroring the Federal Reserve's aggressive rate hikes. However, 2024 brought a reversal of this trend. The Fed cut its target rate by 100 basis points, which provided some relief for HELOC borrowers.

As of February 2025, McBride forecasts that HELOC rates will continue to fall in 2025, sending the average HELOC to 7.25 percent by the end of the year, a low not seen since 2022. This marks an improvement from the 2023 peak but remains significantly higher than pre-2022 levels. Homeowners should note that while rates have decreased, they still exceed historical norms.

Economic Factors Influencing Rates

Several economic factors impact HELOC rates in 2025:

- Inflation: At 2.7%, inflation exceeds the Federal Reserve's 2% target. This persistent inflationary pressure prevents more aggressive rate cuts.

- GDP Growth: The pace of economic growth influences Fed decisions. Robust growth could lead to inflationary pressures, potentially slowing the pace of rate cuts.

- Labor Market: Employment figures and wage growth affect the Fed's decisions. A strong labor market might delay further rate reductions.

- Global Economic Conditions: International economic events and trade relations can indirectly affect HELOC rates by influencing the overall U.S. economic outlook.

Rate Predictions for 2025

Current trends and economic indicators suggest a continued downward trajectory for HELOC rates in 2025. The CME FedWatch Tool can be used to track the probabilities of changes to the Fed rate, as implied by 30-Day Fed Funds futures prices. This tool provides insights into potential future rate movements.

Experts project that the federal funds rate could drop to a range of 3.75% to 4.00% by late 2025. If these predictions hold true, HELOC rates could potentially decrease by another 0.5% or more.

However, economic conditions can change rapidly. Unexpected events or shifts in economic data could alter the Fed's rate decision timeline. Homeowners considering a HELOC should stay informed about these economic indicators and their potential impact on rates.

Strategies for Homeowners

Given the current rate environment, homeowners might consider the following strategies:

- Lock in current rates: If you believe rates will rise, secure a HELOC now.

- Wait for potential drops: If you can delay your borrowing needs, wait for further rate cuts (which could result in savings).

- Compare lenders: HELOC margins can vary significantly between lenders. Shop around for better rates.

- Consider fixed-rate options: Some lenders offer the ability to lock in a portion of your HELOC at a fixed rate, providing stability in an uncertain environment.

- Leverage your credit score: A high credit score can lead to more favorable HELOC terms. Improve your credit if possible before applying.

As the HELOC landscape continues to evolve, homeowners must adapt their strategies to navigate these variable rates effectively. The next section will explore specific techniques to manage and optimize your HELOC in this dynamic environment.

How to Optimize Your HELOC Strategy

Time Your Application Strategically

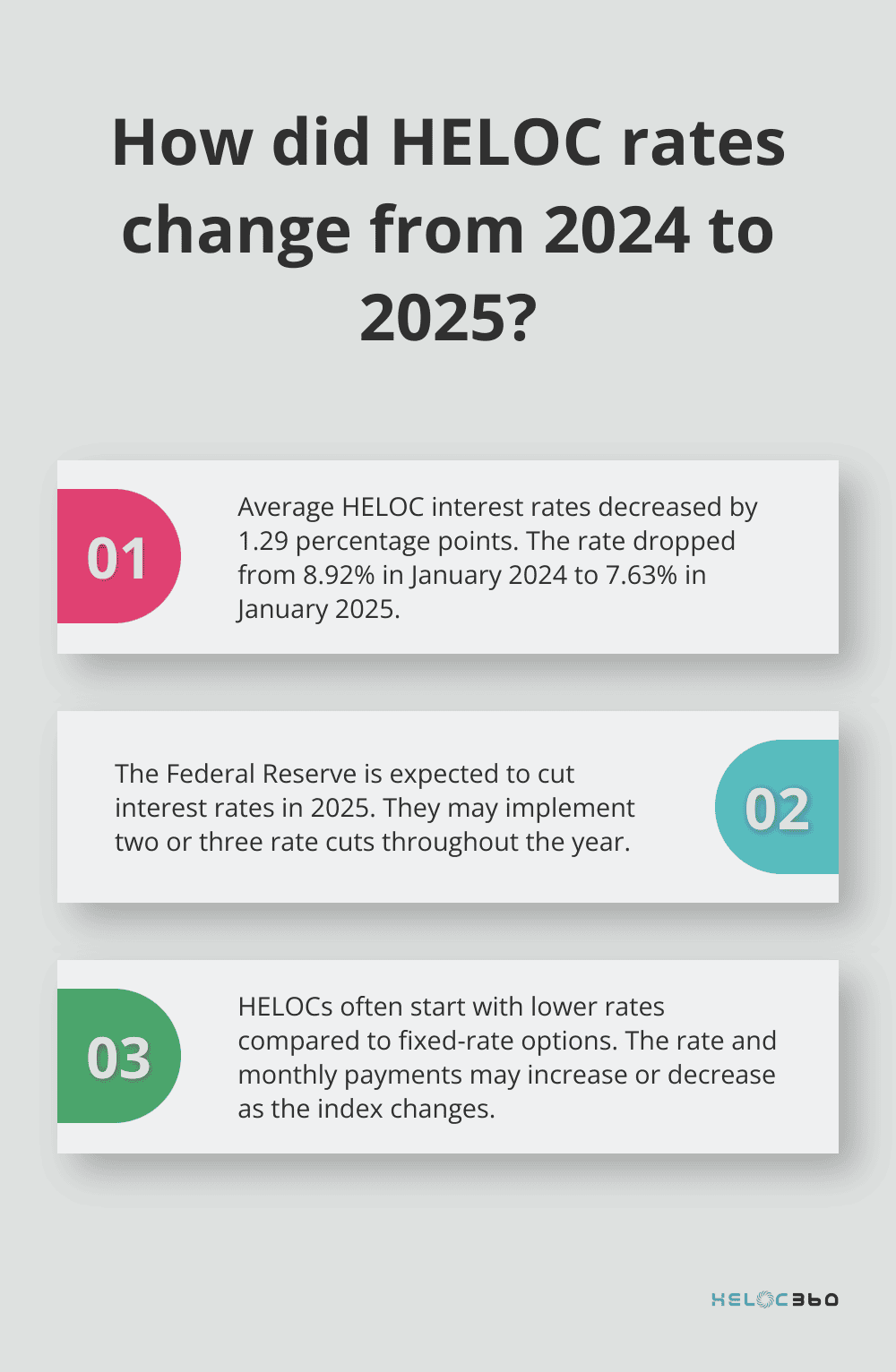

Timing matters when you apply for a HELOC. The Fed is expected to cut interest rates in 2025, perhaps two or three times, which might tempt you to wait. However, delay isn't always the best choice.

If you need funds soon, secure a HELOC now. Current rates, while higher than historical lows, remain favorable compared to recent peaks. You can always refinance your HELOC if rates drop significantly.

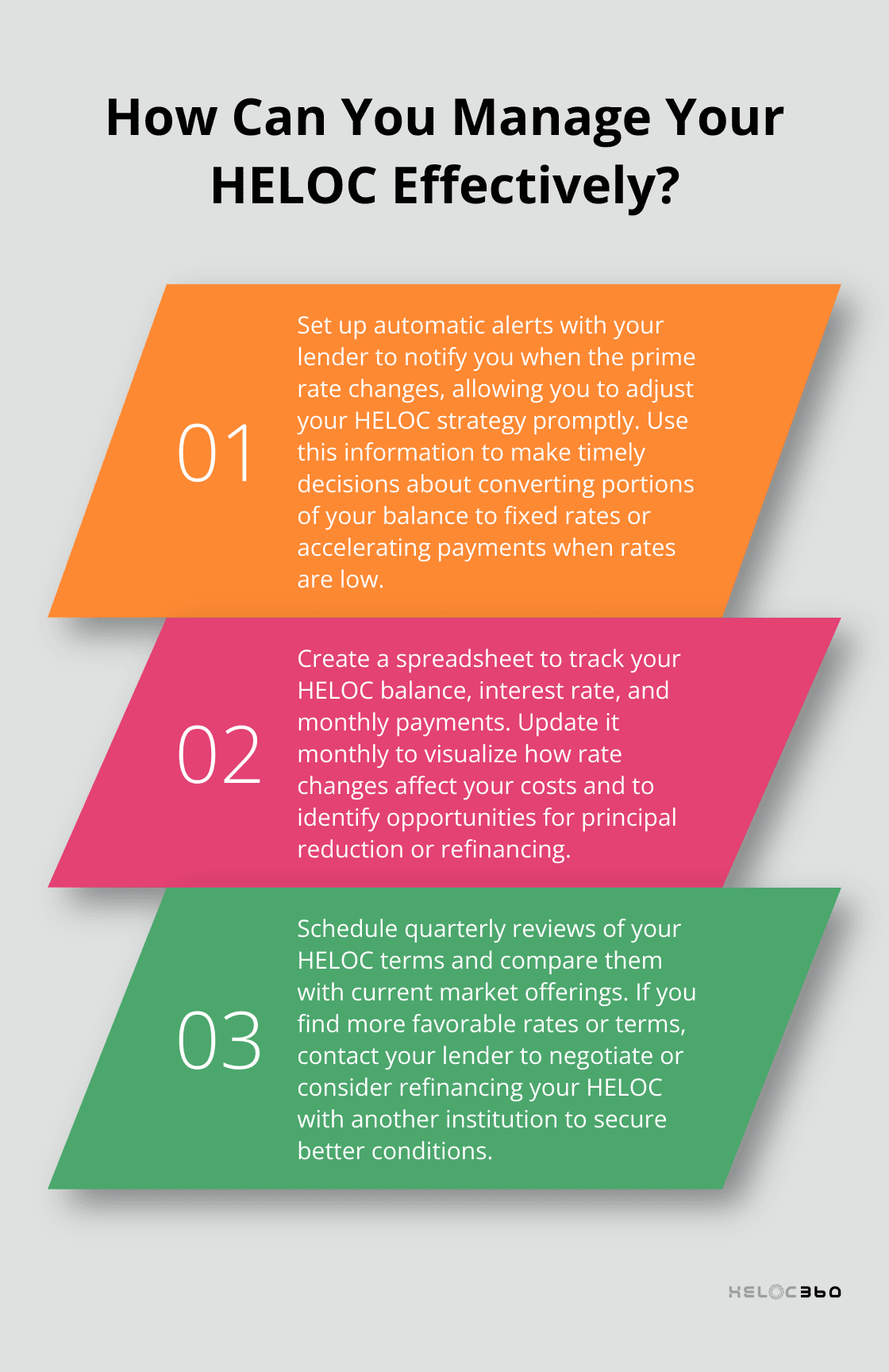

Those with flexibility should watch economic indicators. Pay attention to the Consumer Price Index (CPI) and the Federal Reserve's statements. Decreasing inflation often precedes rate cuts.

Negotiate Effectively

Don't accept the first offer you receive. Lenders have room to maneuver, and negotiation can lead to better terms. Here's how to negotiate effectively:

- Obtain multiple quotes: Try to get at least three offers from different lenders. This provides leverage and a clear market picture.

- Emphasize your strengths: A high credit score (720+) or low loan-to-value ratio can warrant better rates. Inform lenders about your financial strengths.

- Inquire about discounts: Many lenders offer rate discounts for existing customers or automatic payments setup. These can reduce your rate by 0.25% to 0.50%.

- Request fee waivers: Application fees, annual fees, and closing costs are often negotiable. Ask for these to be reduced or waived.

Protect Against Rate Increases

While rates might decrease, protect yourself against potential increases. Consider these strategies:

- Choose a HELOC with a rate cap: This limits your rate's maximum, providing security in uncertain times. Average HELOC interest rates dropped by 1.29 percentage points between January 2024 and January 2025 (from 8.92% to 7.63%).

- Pay principal during the draw period: This reduces your balance and the impact of rate increases on your payments.

- Use a HELOC for short-term needs: You can minimize exposure to rate fluctuations if you only need funds briefly.

Explore Conversion Options

Many lenders allow you to convert part or all of your variable-rate HELOC balance to a fixed rate. This can be a powerful tool in your HELOC strategy.

For instance, if you've drawn a large amount and rates are low, a fixed-rate conversion can lock in those favorable terms. As the index changes, your rate and monthly payments may increase or decrease. HELOCs often start with low rates compared to fixed-rate options.

Be aware of any fees associated with conversions. Also, fixed rates typically exceed the initial variable rate, so weigh long-term costs against predictability benefits.

Final Thoughts

Variable HELOC rates in 2025 require market awareness, strategic planning, and proactive management. Economic factors, especially Federal Reserve decisions, influence these rates. Homeowners must time their HELOC applications, negotiate with lenders, and protect against rate increases to optimize their strategy.

Economic indicators, Fed meetings, and market trends provide valuable insights for HELOC decisions. Lower rates appeal to many, but individual financial situations should guide choices. HELOC variable rates fluctuate, so homeowners must adapt their strategies as conditions change.

HELOC360 offers support for homeowners navigating HELOCs and variable rates. Our platform simplifies the process of understanding and leveraging home equity. We connect you with suitable lenders and provide expert guidance to help you make informed decisions about your HELOC.

Related Articles

Chase Bank HELOC Rates: Current Offers and Trends

Explore the latest on HELOC loan Chase offers, interest rates, and trends for 2025. Find practical tips for securing the best deal.