Why HELOC Rates Fluctuate and How It Affects You

Table of Contents

HELOC rates can be a rollercoaster ride for homeowners. These fluctuations are influenced by various factors, from broad economic trends to individual financial circumstances.

At HELOC360, we understand how these changes can impact your financial planning and decision-making. This post will explore the reasons behind HELOC rate fluctuations and provide practical strategies to help you navigate this dynamic landscape.

What Drives HELOC Rate Changes?

HELOC rates don't change in isolation. A complex interplay of factors, both macro and micro, influences them. Understanding these drivers will help you make informed decisions about your HELOC.

The Federal Reserve's Impact

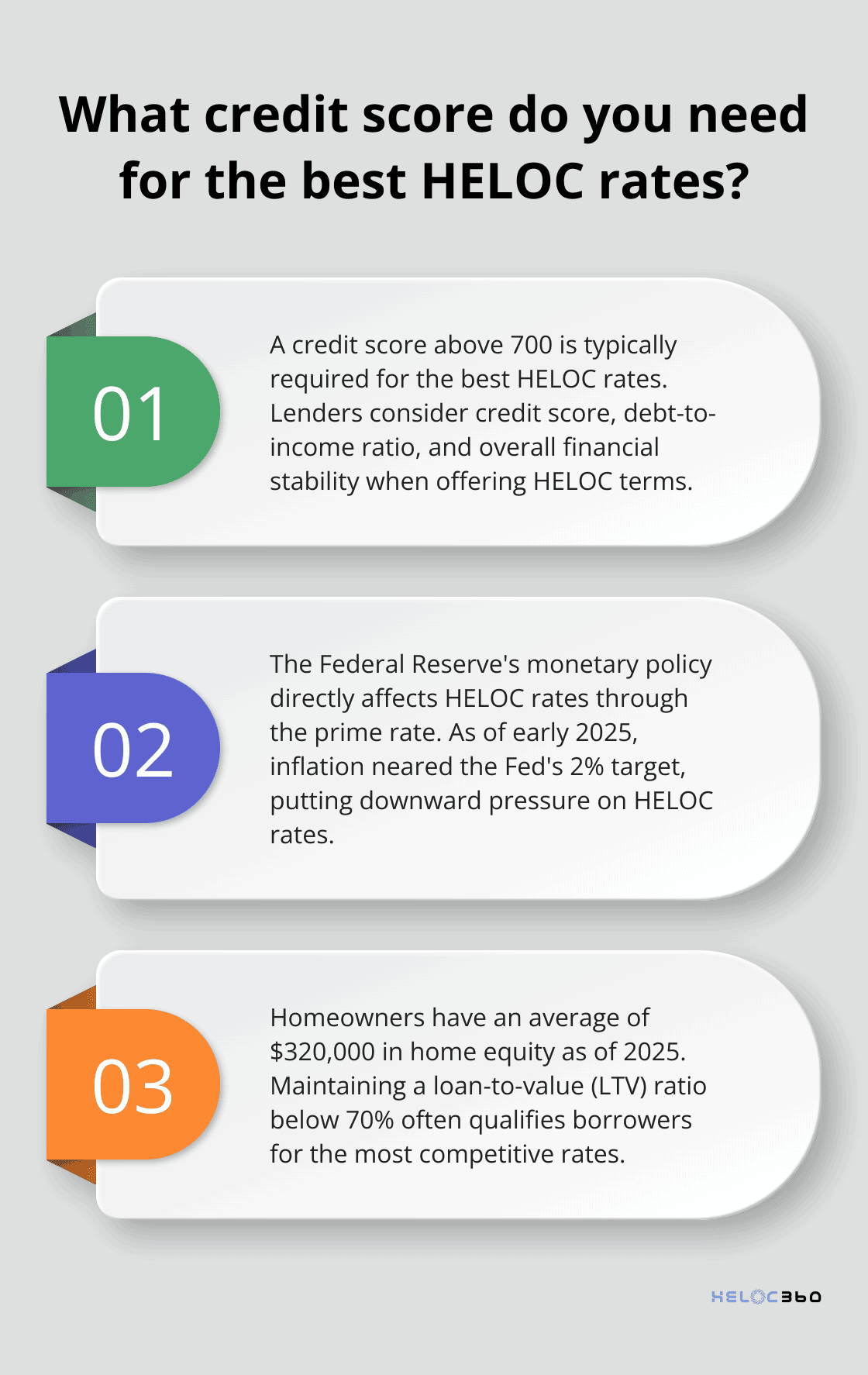

The Federal Reserve's monetary policy plays a pivotal role in HELOC rates. When the Fed adjusts its benchmark rate, it directly affects the prime rate (the basis for most HELOC rates). The rate on a HELOC floats with the prime rate, and the Fed is likely to continue to cut rates again in the next year.

Economic Indicators and Market Conditions

Broader economic factors also sway HELOC rates. Inflation, employment data, and GDP growth all factor into lenders' decisions. As of early 2025, inflation neared the Fed's 2% target, which put downward pressure on HELOC rates. The CME Group's FedWatch Tool indicates a high probability of further rate cuts, which could result in even lower HELOC rates in the coming months.

Your Financial Health Matters

Your personal financial situation significantly impacts the HELOC rate you're offered. Lenders typically look for a credit score above 700 to qualify for the best rates. They also consider your debt-to-income ratio and overall financial stability. Improving these factors can lead to more favorable HELOC terms.

Property Values and Equity

The amount of equity in your home and its current value play a key role in determining your HELOC rate. Most lenders set a maximum loan-to-value (LTV) ratio around 80%. As of 2025, homeowners have an average of $320,000 in home equity, which provides substantial borrowing power. Maintaining a lower LTV ratio can help you secure better rates.

Homeowners who keep their LTV ratio below 70% often qualify for the most competitive rates. This occurs because lenders view these borrowers as lower risk, given their substantial equity cushion.

Understanding these factors can help you anticipate rate changes and make strategic decisions about when to apply for or draw from your HELOC. While general trends are important, your specific situation will ultimately determine your HELOC rate. That's why you should shop around and compare offers from multiple lenders to ensure you're getting the best deal possible.

Now that we've explored the factors that influence HELOC rates, let's examine how these fluctuations can impact you as a borrower.

How HELOC Rate Changes Affect Your Finances

Your Monthly Payments Will Fluctuate

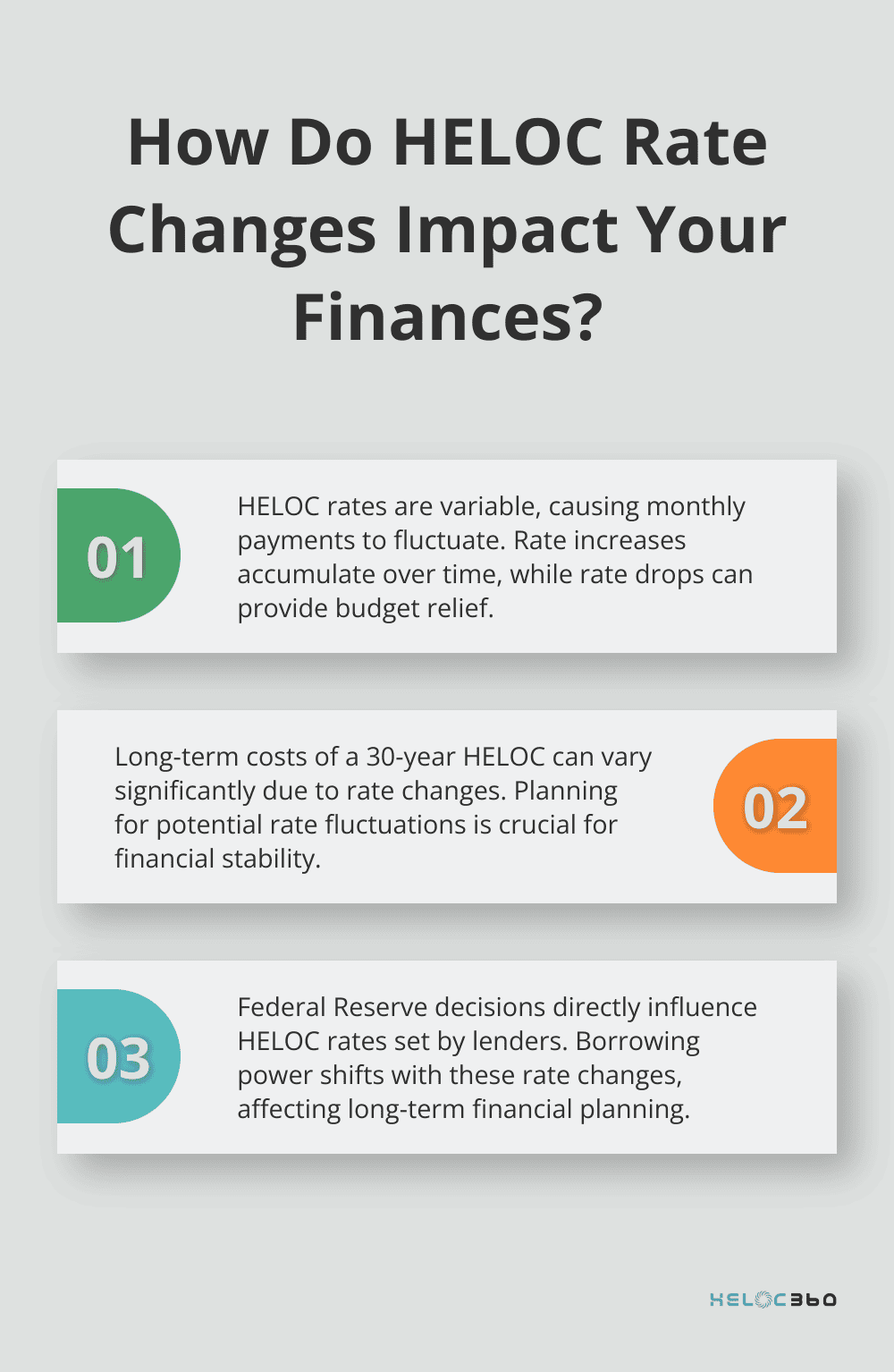

HELOC rate changes directly impact your monthly payments. Remember that HELOCs typically have variable rates, so your payments could increase from month to month. While this might seem small, it accumulates over time. On the flip side, rate drops can provide welcome relief to your monthly budget.

Long-Term Costs Can Vary Significantly

The cumulative effect of rate changes on your long-term costs can be substantial. A 30-year HELOC offers flexibility if you want to tap into your home equity to fund your financial goals. This highlights the importance of planning for potential rate fluctuations.

Your Borrowing Power Will Shift

Your borrowing power will shift. When the Fed lowers its key rate, it causes the rates that lenders ultimately set for HELOCs and new home equity loans also to drop, and vice versa. It's important to consider your long-term needs when setting up a HELOC.

Refinancing Decisions Become More Complex

Rate fluctuations create opportunities and challenges for refinancing. Significant rate drops might make refinancing your HELOC to lock in a lower rate attractive. However, this decision isn't straightforward. You'll need to weigh potential savings against refinancing costs (typically 2% to 5% of the loan amount).

HELOC rate changes offer both savings opportunities and financial risks. Staying informed about rate trends and understanding their impact on your specific situation will help you make smarter decisions about using your home equity. As you navigate these fluctuations, it's essential to have strategies in place to manage them effectively. Let's explore some practical approaches to handle HELOC rate changes in the next section.

How to Navigate HELOC Rate Changes

Monitor Economic Trends

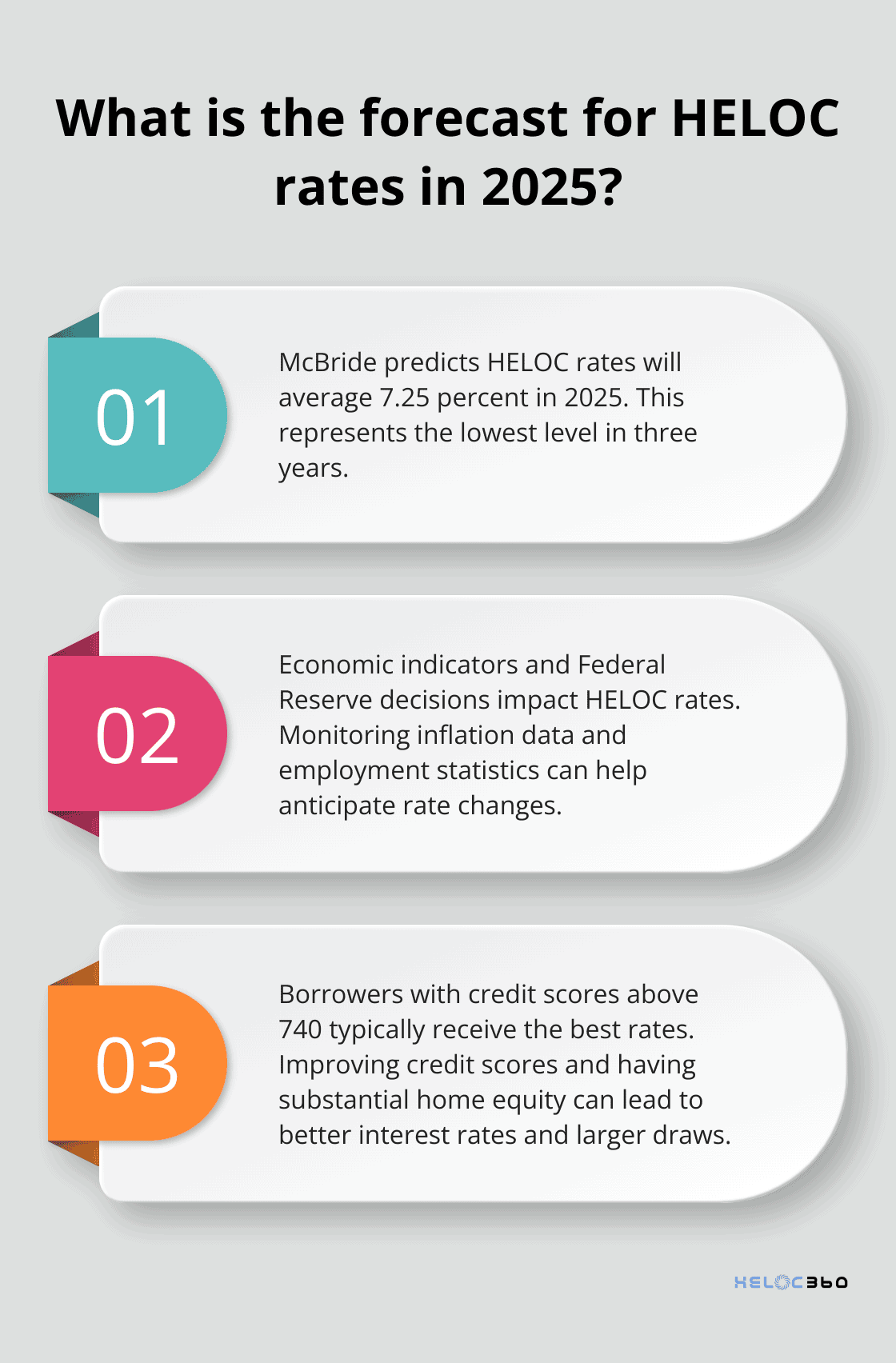

Economic indicators provide valuable insights into potential HELOC rate movements. The Federal Reserve's decisions on interest rates directly impact HELOC rates. McBride forecasts that HELOC rates will continue to decline in 2025, averaging 7.25 percent, their lowest level in three years.

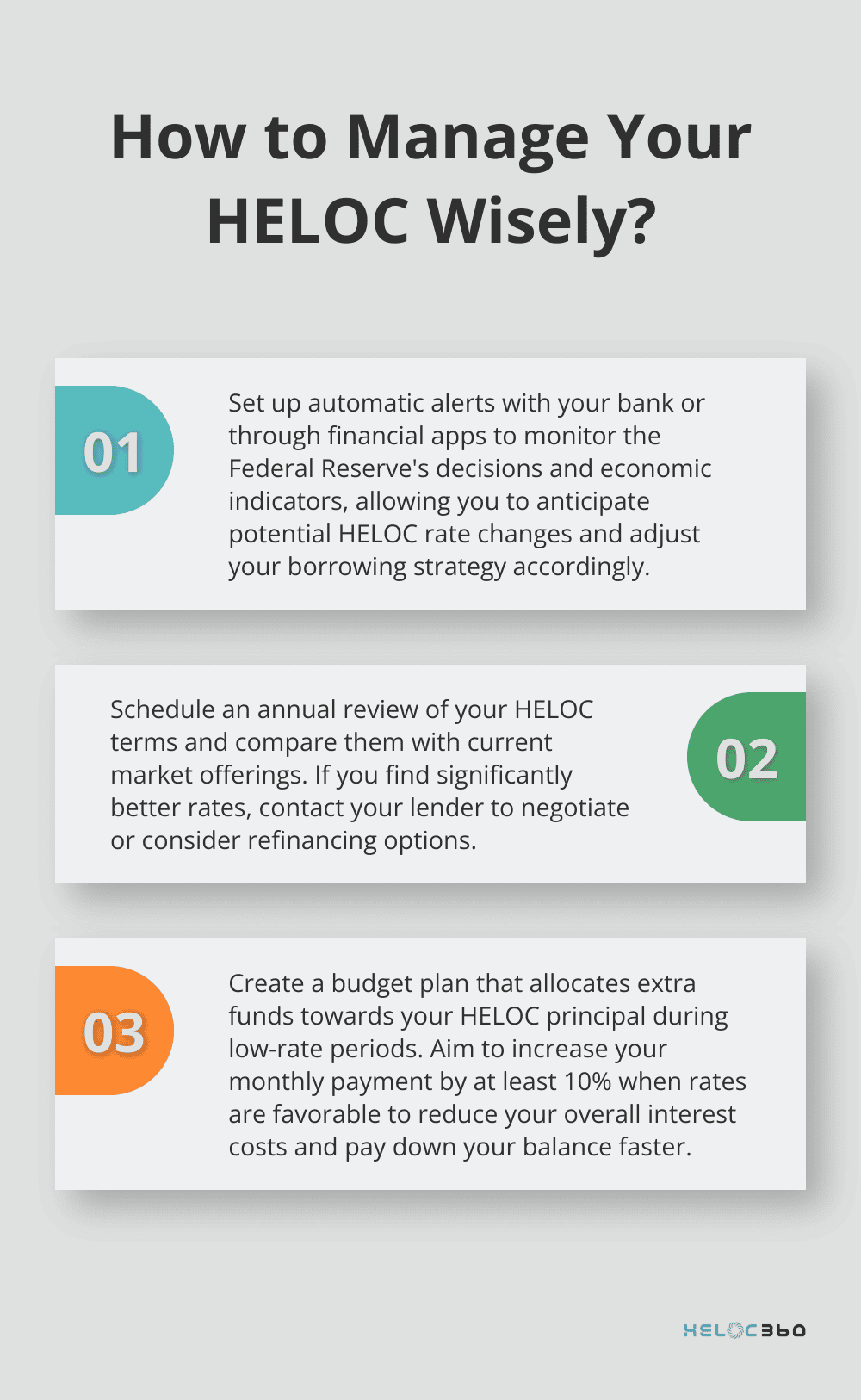

Pay attention to inflation data and employment statistics, as these factors influence the Fed's decisions. Financial news outlets and the Federal Reserve's official communications serve as excellent sources for this information. Anticipate rate changes and adjust your borrowing strategy accordingly.

Explore Fixed-Rate Conversion Options

If you worry about rising rates, explore the option to convert part or all of your HELOC balance to a fixed rate. Many lenders offer this feature (often called a fixed-rate advance or option). It allows you to freeze a portion or all of your balance at a fixed interest rate, protecting you against market fluctuations that impact rates.

Before you decide, compare the offered fixed rate with your current variable rate and future rate projections. Also, check for any fees associated with the conversion. This evaluation will help you determine if a fixed-rate conversion aligns with your financial goals.

Maximize Low-Rate Periods

When HELOC rates drop, seize the opportunity to make extra payments towards your principal. This strategy can reduce your overall interest costs and help you pay down your balance faster. Even small additional payments can make a significant difference over time.

For example, if you have a $50,000 HELOC balance at 8% interest, paying an extra $100 per month could save you thousands in interest over the life of the loan and shorten your repayment period by several years.

Improve Your Credit Score

Your credit score plays a key role in determining your HELOC rate. Lenders typically offer the best rates to borrowers with scores above 740. If your score falls below this threshold, focus on improving it. Pay your bills on time, reduce your credit utilization ratio, and address any errors on your credit report.

Borrowers with substantial home equity, high credit scores and low DTIs may qualify for better interest rates and a larger draw.

Shop Around for Better Rates

Don't hesitate to compare offers from multiple lenders. Different financial institutions may offer varying rates and terms. Try to obtain quotes from at least three lenders to ensure you get the best deal possible. HELOC360 can help you connect with lenders that fit your unique needs and financial situation.

Final Thoughts

HELOC rates fluctuate due to economic trends and individual financial factors. The Federal Reserve's policies, inflation rates, and employment data shape these rates. Your credit score and home equity also affect the HELOC rates you receive. These changes impact your monthly payments, long-term costs, and borrowing power.

We at HELOC360 recommend a proactive approach to manage your HELOC. Review your rates regularly, consider fixed-rate conversions during low-interest periods, and make extra payments when possible. Maintain a strong credit profile and compare offers from multiple lenders to secure the best rates.

Your home's equity serves as a valuable financial tool. Understanding HELOC rates and their effects helps you maximize this resource for your financial goals. Visit HELOC360 for personalized guidance and to connect with lenders that match your unique needs.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.