Should You Consider HELOC Payment Deferment?

At HELOC360, we understand that financial challenges can arise unexpectedly, leaving homeowners searching for solutions.

HELOC deferment is an option that allows borrowers to temporarily pause or reduce their payments. However, it's crucial to weigh the pros and cons before making a decision.

In this post, we'll explore whether HELOC payment deferment is the right choice for you and what factors you should consider.

What Is HELOC Payment Deferment?

Definition and Purpose

HELOC payment deferment allows homeowners to temporarily pause or reduce their Home Equity Line of Credit (HELOC) payments. This financial tool provides relief during challenging times, such as unexpected job loss or medical expenses.

How HELOC Payment Deferment Works

When you opt for payment deferment, you modify your regular payment schedule. Depending on your lender's policies, you might skip payments entirely or make reduced payments for a specific period (typically ranging from a few months to a year).

It's essential to understand that interest usually continues to accumulate during the deferment period. This means your balance will likely increase when you resume regular payments. Your payments will need to cover both your outstanding loan balance and any interest that has accumulated.

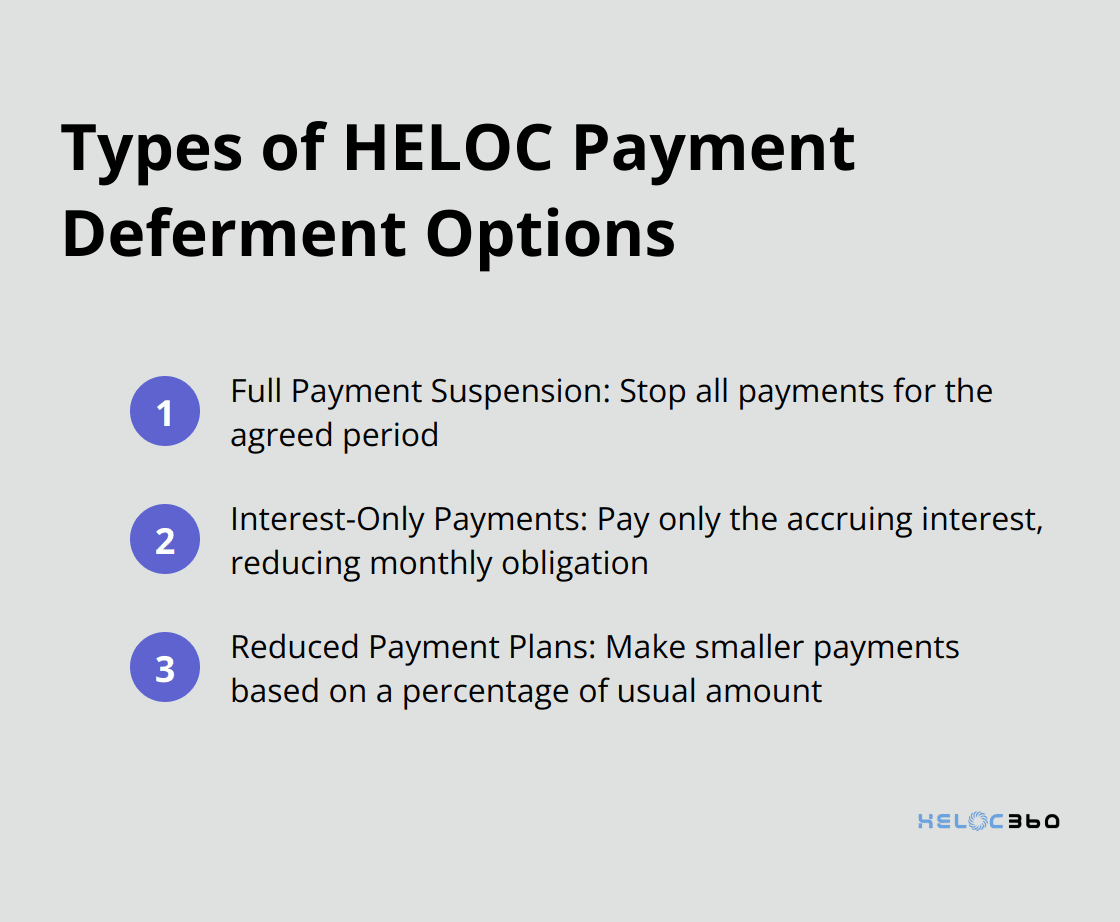

Types of HELOC Payment Deferment Options

Lenders offer various deferment options to accommodate different financial situations:

- Full Payment Suspension: You stop all payments for the agreed period.

- Interest-Only Payments: You pay only the accruing interest, significantly reducing your monthly obligation.

- Reduced Payment Plans: You make smaller payments than your regular amount (often based on a percentage of your usual payment).

Each option impacts your long-term financial health differently. For example, interest-only payments prevent your balance from growing as quickly as full suspension but don't reduce your principal.

Terms and Conditions

Before deciding on HELOC payment deferment, you must understand the specific terms and conditions. Some lenders may charge fees for deferment or adjust your credit line. Always inquire about the impact on your loan term, interest rate, and total repayment amount.

While deferment can offer short-term relief, it's not a permanent solution to financial problems. It serves best as a bridge to help you through temporary setbacks.

Next Steps

To explore HELOC payment deferral options, contact your lender directly. They can provide detailed information about their deferment programs and help you make an informed decision based on your unique financial goals and circumstances. As you weigh your options, consider the potential benefits and drawbacks of payment deferment (which we'll discuss in the next section).

Benefits of HELOC Payment Deferment

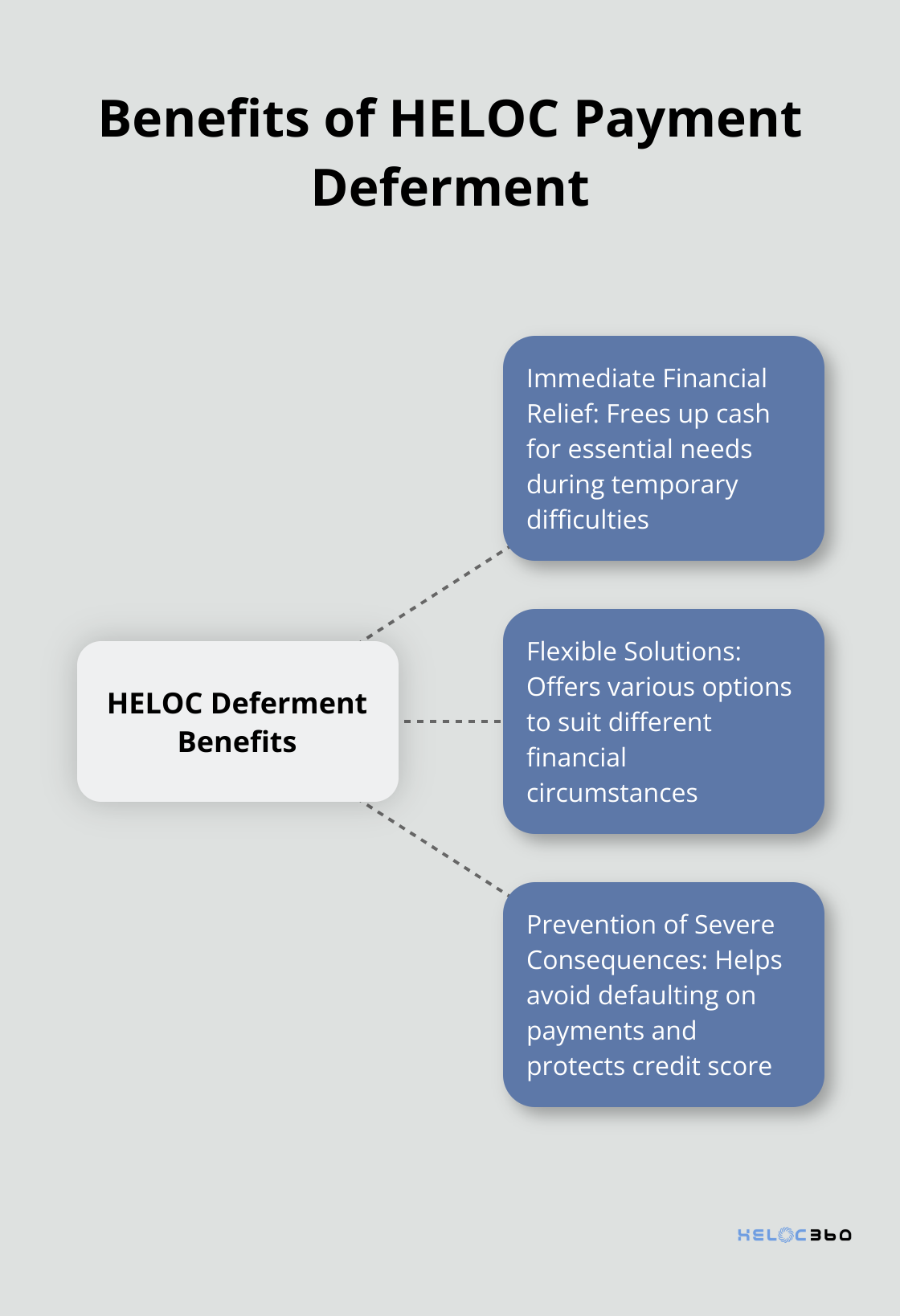

Immediate Financial Relief

HELOC deferment offers homeowners a valuable lifeline during temporary financial difficulties. This option provides several advantages that can help you navigate challenging times without compromising your financial stability.

One of the primary benefits of HELOC payment deferment is the immediate financial relief it offers. If you face unexpected expenses or a temporary loss of income, deferring your HELOC payments can free up cash for essential needs. This financial breathing space can prove invaluable when you need to regain your financial footing.

For instance, if you lose your job and need time to find new employment, deferring your HELOC payments for a few months can allow you to focus on your job search without the added stress of meeting this financial obligation. The Bureau of Labor Statistics reports on the duration of unemployment, which can vary widely. A HELOC deferment could cover this period, allowing you to maintain your financial stability while seeking new employment.

Flexible Solutions for Various Situations

HELOC payment deferment isn't a one-size-fits-all solution. Lenders often offer various options to suit different financial circumstances. You might defer all payments, make interest-only payments, or reduce your payment amount for a specified period.

This flexibility allows you to choose an option that best aligns with your current financial situation and future goals. For example, if you're a seasonal worker with fluctuating income, you could potentially arrange for lower payments during your off-season and resume full payments when your income increases.

Prevention of Severe Financial Consequences

Perhaps the most significant advantage of HELOC payment deferment is its potential to help you avoid defaulting on your payments. Default can have serious consequences, including damage to your credit score, potential foreclosure, and long-term financial repercussions.

Opting for payment deferment is a proactive step to manage your finances responsibly. This approach demonstrates to lenders that you're committed to meeting your obligations, even if you need some temporary adjustments to do so. It's a strategic move that can protect your financial health in the long run.

While HELOC payment deferment offers several benefits, it's important to consider potential drawbacks as well. Let's explore some of the disadvantages in the next section to provide a balanced perspective on this financial tool.

The Hidden Costs of HELOC Payment Deferment

HELOC payment deferment can appear as an attractive option during financial hardship, but it's important to understand the potential drawbacks. While it offers short-term relief, deferment can lead to long-term financial implications that might outweigh the immediate benefits.

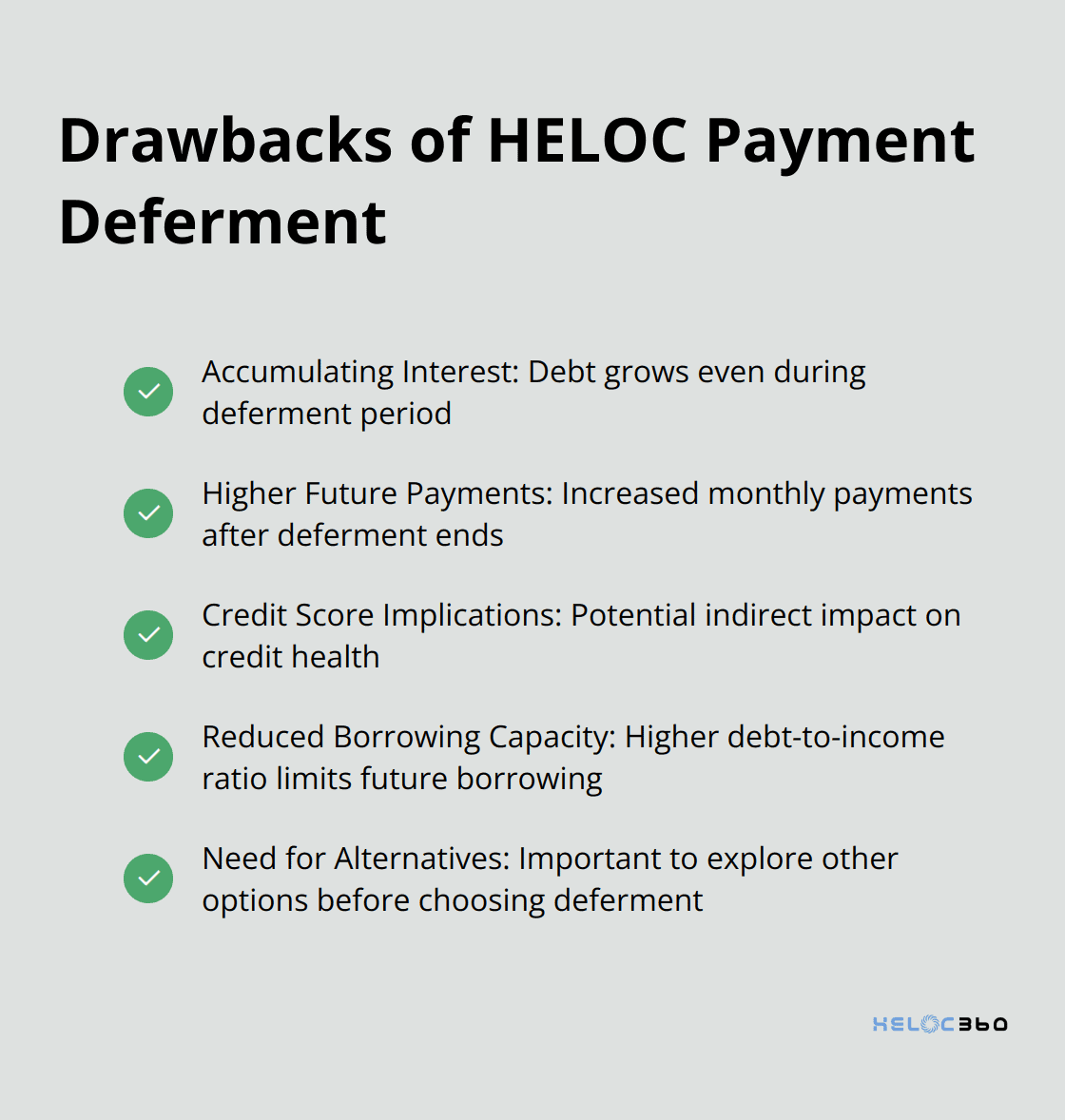

Accumulating Interest: A Growing Burden

When you defer HELOC payments, interest continues to accrue on your outstanding balance. This means your debt grows even while you're not making payments. Interest-only HELOCs calculate monthly payments differently than traditional HELOCs, with homeowners paying only the interest during the draw period.

The Shock of Higher Future Payments

Once the deferment period ends, you'll likely face higher monthly payments. These increased payments account for the accumulated interest and the need to repay the loan within the original term. Mortgage balances shown on consumer credit reports grew by $199 billion during the first quarter of 2025 and totaled $12.80 trillion at the end of March.

Credit Score Implications

A properly arranged deferment shouldn't directly impact your credit score, but it can indirectly affect your financial health. The increased debt load from accrued interest can raise your credit utilization ratio (a key factor in credit scoring). Additionally, if you struggle with higher payments post-deferment, any late or missed payments will negatively impact your credit score.

Reduced Borrowing Capacity

The increased balance on your HELOC can limit your future borrowing options. Lenders consider your debt-to-income ratio when evaluating loan applications. A higher HELOC balance means a higher ratio, potentially making it more difficult to secure additional credit when needed.

Alternative Options to Consider

Before opting for payment deferment, it's wise to explore alternative options. These might include refinancing your HELOC, negotiating a modified payment plan with your lender, or seeking financial counseling to improve your overall financial situation. Each option has its own pros and cons, so it's important to evaluate them carefully based on your specific circumstances. If you can't make payments on your HELOC, the original lender has the right to sell the loan off to another party such as a credit collection agency.

Final Thoughts

HELOC deferment offers homeowners temporary financial relief during challenging times. It provides flexibility and helps avoid defaulting on payments, which can be crucial for those experiencing setbacks like job loss or unexpected expenses. However, this option comes with potential long-term consequences that require careful consideration.

The drawbacks of HELOC deferment include continued interest accumulation and potentially higher future payments. These factors may strain your budget when regular payments resume and impact your credit score and borrowing capacity. It's important to assess your current financial situation and future income prospects realistically before opting for deferment.

We at HELOC360 recommend consulting with financial advisors or lenders before making a decision about HELOC deferment. Our platform helps homeowners navigate complex financial decisions, providing expert guidance and connecting you with suitable lenders. For more information on maximizing your home equity, visit HELOC360.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.