Understanding HELOC Interest Fluctuations

Table of Contents

HELOC interest rates can be a rollercoaster ride for homeowners. These fluctuations can significantly impact your monthly payments and overall borrowing costs.

At HELOC360, we understand the importance of staying informed about the factors that influence these rates. This post will explore the key drivers behind HELOC interest changes and provide practical strategies to manage them effectively.

What Drives HELOC Interest Rates?

The Federal Reserve's Influence

The Federal Reserve's monetary policy significantly shapes HELOC rates. When the Fed adjusts its benchmark interest rate, it affects the entire financial system, including the prime rate. Most HELOCs link directly to the prime rate, so changes in the Fed's policy lead to shifts in your HELOC rate.

Existing HELOC borrowers can expect their rates to decrease in response to a Fed rate cut, but it may take 1-2 statement cycles for these changes to take effect.

Your Financial Profile's Impact

Your personal financial history plays a critical role in determining your HELOC rate. Lenders use your credit score to assess risk. A higher score often results in lower interest rates. If your score has improved since you initially obtained your HELOC, you might negotiate a better rate.

Applying for, opening and using a HELOC can help or hurt your credit scores depending on your overall credit profile and how you manage the account.

Property Value and Loan-to-Value Ratio

The value of your home and your loan-to-value ratio (LTV) also affect your HELOC rate. A lower LTV ratio often yields better rates because it represents less risk for the lender.

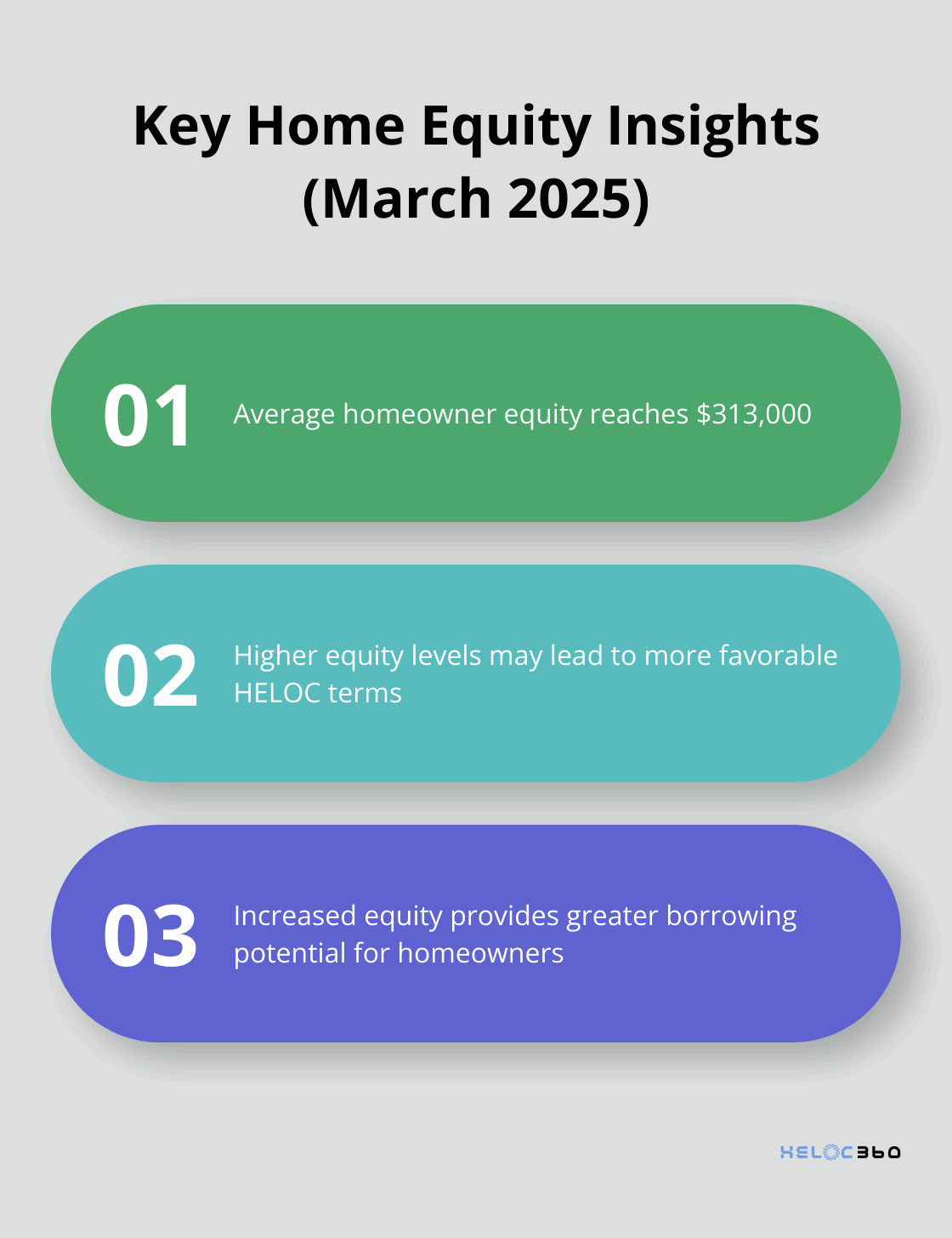

Recent data indicates that home equity levels have increased, with the average homeowner currently having $313,000 of equity in their home, according to the March 2025 Intercontinental Exchange (ICE) Mortgage report. This trend could result in more favorable HELOC terms for many homeowners.

Market Conditions and Economic Indicators

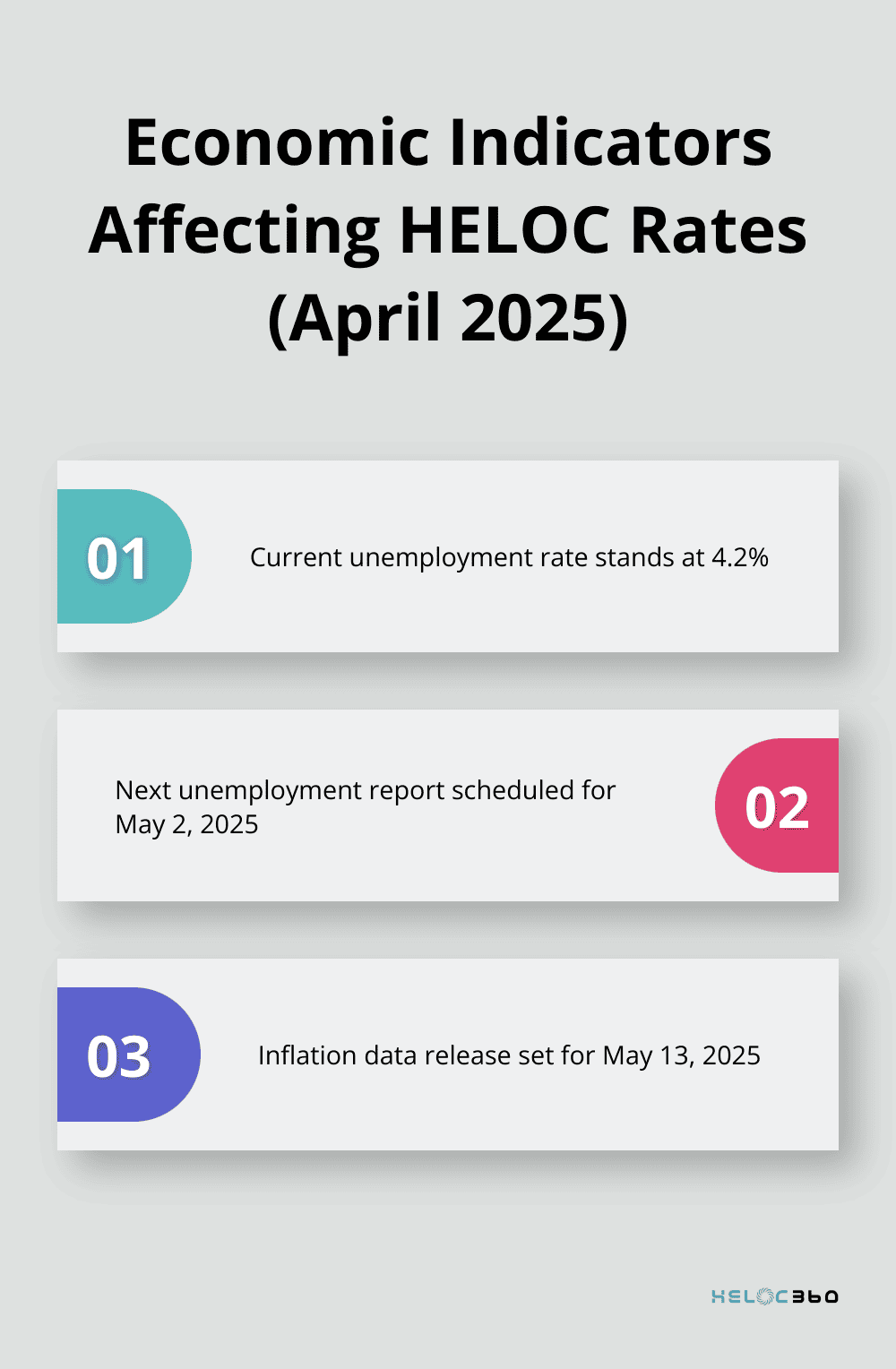

Broader economic factors, such as inflation and unemployment rates, influence HELOC rates. The current unemployment rate of 4.2% and declining inflation trends contribute to the favorable HELOC rate environment in early 2025.

Upcoming economic reports could signal potential shifts in HELOC rates. The next unemployment report (scheduled for May 2, 2025) and the inflation data release (set for May 13, 2025) will provide valuable insights into future rate trends.

Global Economic Events

International economic events can also impact HELOC rates. Trade disputes, geopolitical tensions, or global financial crises can cause ripple effects that reach the U.S. housing market and influence interest rates.

For example, a major economic slowdown in a large economy like China could lead to lower global interest rates, potentially benefiting HELOC borrowers in the U.S.

Understanding these factors helps you anticipate rate changes and make strategic decisions about your HELOC. The next section will explore how HELOC interest rates differ from fixed-rate loans, providing you with a comprehensive view of your borrowing options.

How HELOC Interest Rates Differ from Fixed-Rate Loans

Variable vs. Fixed Rates: Understanding the Basics

HELOC interest rates change with market conditions, particularly the prime rate. When the prime rate fluctuates, your HELOC rate follows. Fixed-rate loans, on the other hand, maintain a constant interest rate throughout the loan term.

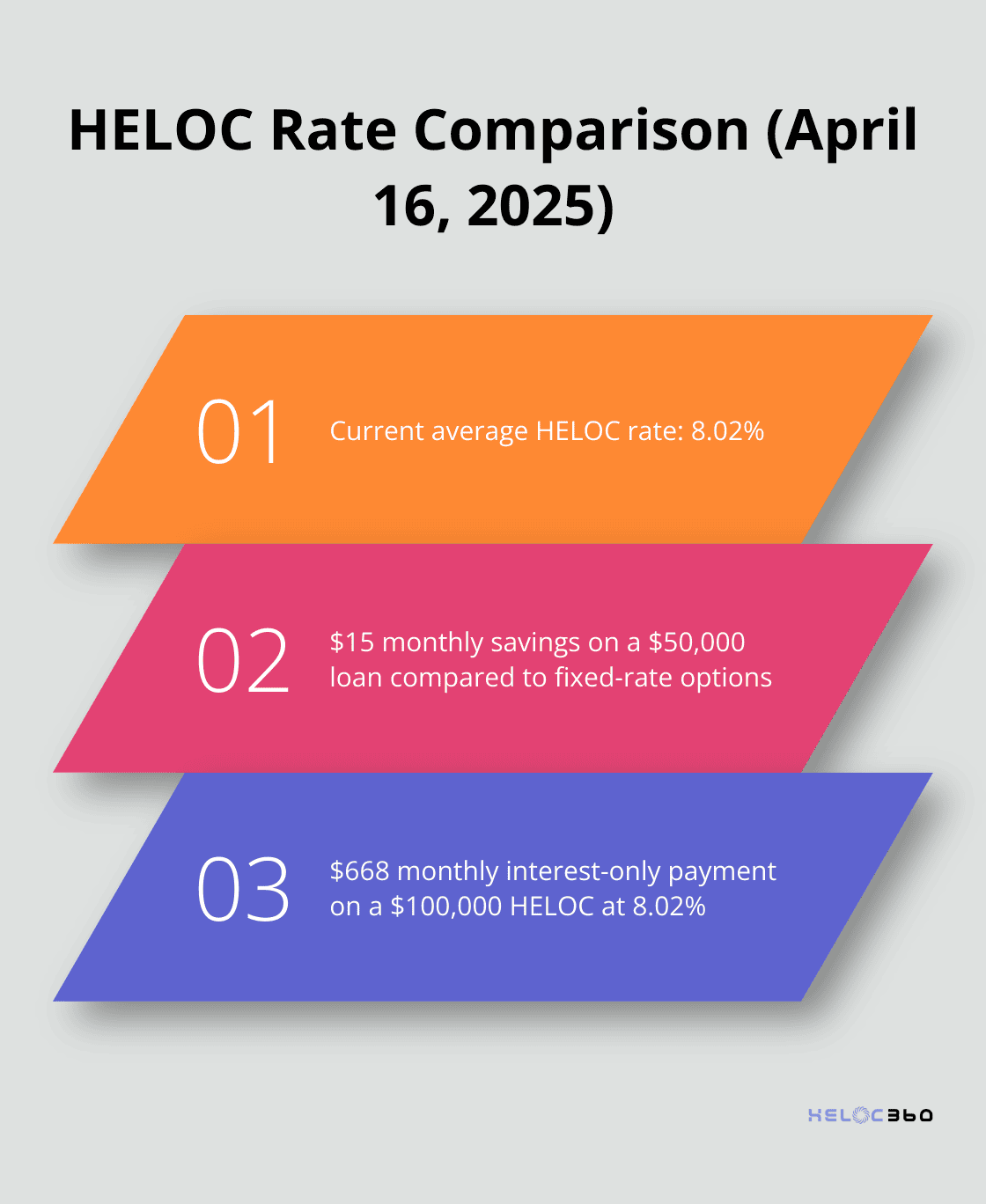

As of April 16, 2025, HELOC rates average 8.02%, according to Bankrate's latest survey of the nation's largest home equity lenders. This difference might appear small, but it impacts your finances over time. For a $50,000 loan, you save approximately $15 monthly with the current HELOC rate compared to a fixed-rate option.

The Two-Phase Structure of HELOCs

HELOCs typically consist of two distinct periods: the draw period and the repayment period. The draw period (usually 5-10 years) allows you to borrow against your credit line as needed, often with interest-only payments.

After the draw period ends, the repayment period begins. You can no longer borrow from the credit line and must start repaying both principal and interest. This transition often leads to a significant increase in monthly payments.

For instance, if you borrow $100,000 during a 10-year draw period at 8.02%, your monthly interest-only payment amounts to about $668. However, when the 20-year repayment period starts, your monthly payment could increase to around $836 (covering both principal and interest).

Protection Through Rate Caps

Some HELOCs let you convert some of your balance to a fixed interest rate. The fixed interest rate is typically higher than the variable rate, but it means your payments for that portion of the balance will remain stable.

While these options provide some security, fixed-rate loans don't require such protections due to their constant rates.

Choosing Between HELOC and Fixed-Rate Loans

Your choice between a HELOC and a fixed-rate loan depends on your financial goals and risk tolerance. If you value flexibility and accept potential rate changes, a HELOC might suit you better. However, if you prefer predictable payments and don't mind potentially paying more in interest, a fixed-rate loan could be the right choice.

The next section will explore strategies to manage HELOC interest rate fluctuations effectively, helping you make the most of your home equity borrowing experience.

How to Manage HELOC Rate Changes

Lock in a Fixed Rate

Many HELOC lenders offer the option to convert all or part of your variable-rate balance to a fixed rate. This strategy (often called a fixed-rate advance or lock option) can protect you from future rate increases.

You could lock in $30,000 at a fixed rate while keeping the remaining $20,000 variable on a $50,000 HELOC balance if you worry about rising rates. This approach provides a balance between stability and flexibility.

However, rates may continue dropping in 2025. HELOCs tend to have variable interest rates that automatically change based on the prime rate.

Take Advantage of Low-Rate Periods

When HELOC rates drop, it's an excellent opportunity to make extra payments. Extra payments during low-rate periods can reduce your principal faster and save on interest over time.

If rates drop from 8% to 7% on a $100,000 HELOC balance, your monthly interest-only payment would decrease from $667 to $583. Instead of pocketing the difference, you could maintain your $667 payment. The extra $84 per month would go directly toward reducing your principal.

If you decide to make extra payments, be sure to alert your lender that the funds should be applied to the principal.

Explore Refinancing Options

Refinancing your HELOC can be a smart move if market conditions have significantly changed since you opened your line of credit. This could involve refinancing into a new HELOC with better terms or converting your HELOC to a fixed-rate home equity loan.

If you opened a HELOC in 2023 when rates were around 10%, refinancing at today's average rate of 8.02% could lead to substantial savings. On a $100,000 balance, this rate reduction would save you about $165 per month in interest payments.

However, refinancing isn't free. You'll need to factor in closing costs (which typically range from 2% to 5% of the loan amount). Make sure the long-term savings outweigh these upfront costs.

Monitor Market Conditions

Stay informed about economic indicators that influence HELOC rates. Keep an eye on Federal Reserve announcements, inflation reports, and unemployment data. This knowledge will help you anticipate potential rate changes and make informed decisions about your HELOC strategy.

If unemployment worsened in April, it could encourage the Federal Reserve to cut interest rates again, perhaps as soon as their May meeting.

Consult with Financial Professionals

Financial advisors or mortgage professionals can provide personalized advice based on your specific situation. They can help you understand the implications of different strategies and choose the best approach for your financial goals.

Final Thoughts

HELOC interest rate fluctuations impact homeowners who leverage their home equity. The Federal Reserve, financial profiles, property values, and economic conditions shape these rates. Homeowners who stay informed about these factors can make strategic decisions about borrowing and managing their HELOCs effectively.

HELOC interest changes rapidly in response to various economic factors. This volatility emphasizes the need for vigilance and proactive management. Monitoring and managing your HELOC interest helps you maximize the benefits of your home equity while minimizing risks.

HELOC360 provides tools and expertise to help you navigate HELOC interest changes. We offer guidance, connect you with lenders, and help you understand how rate changes affect your financial goals. Our platform supports you in making informed decisions about your home equity, turning it into opportunities for growth and financial success.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.