Understanding Your HELOC Minimum Payments

Table of Contents

Understanding your HELOC minimum payment is essential for effective financial planning. Many homeowners struggle to grasp how these payments work and how they can impact their overall financial health.

At HELOC360, we've created this guide to demystify HELOC minimum payments and provide you with practical strategies for managing them. We'll walk you through the calculation process, offer tips for budgeting, and show you how to align your payments with your financial goals.

How HELOC Minimum Payments Work

The Two Phases of a HELOC

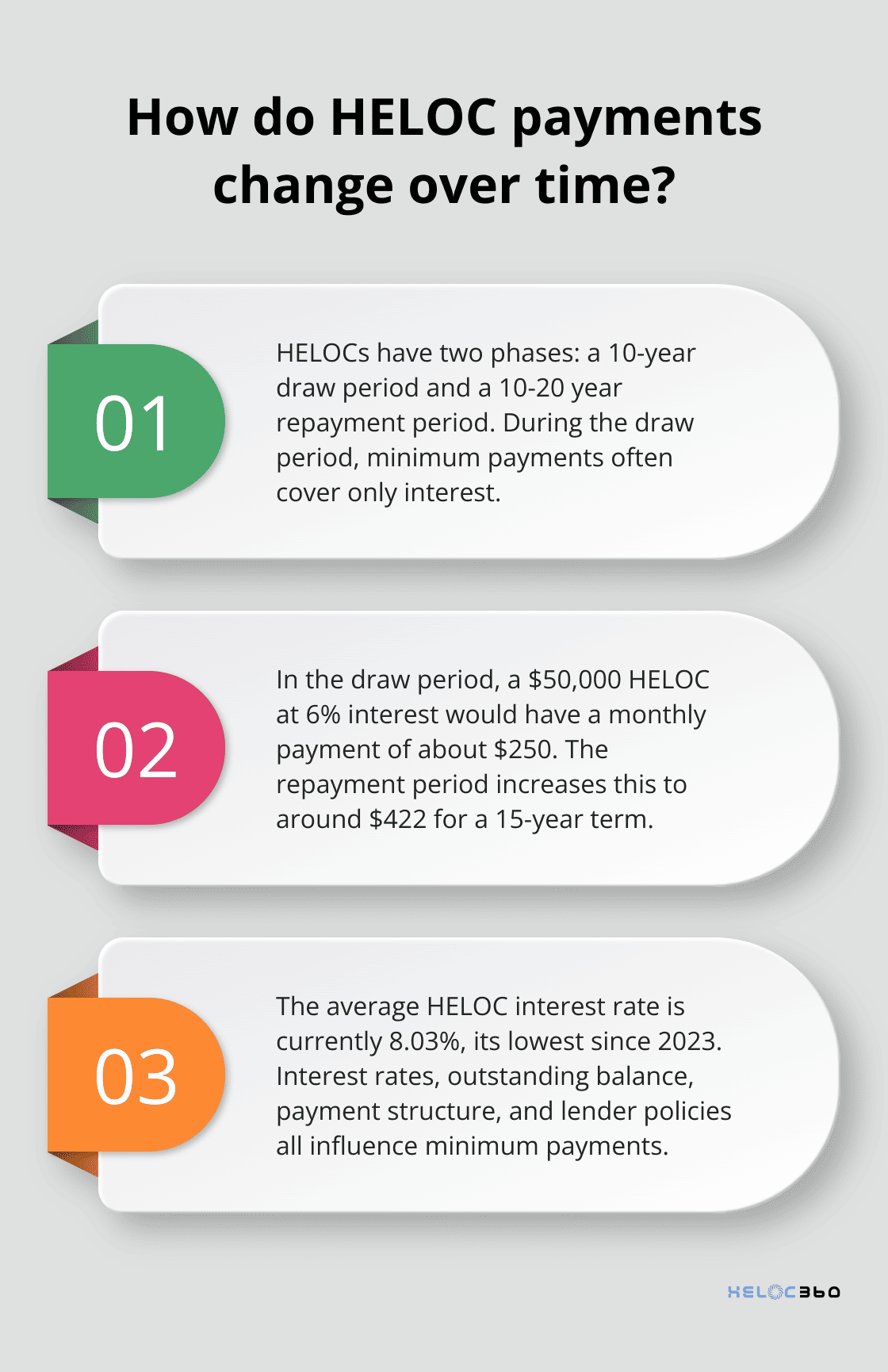

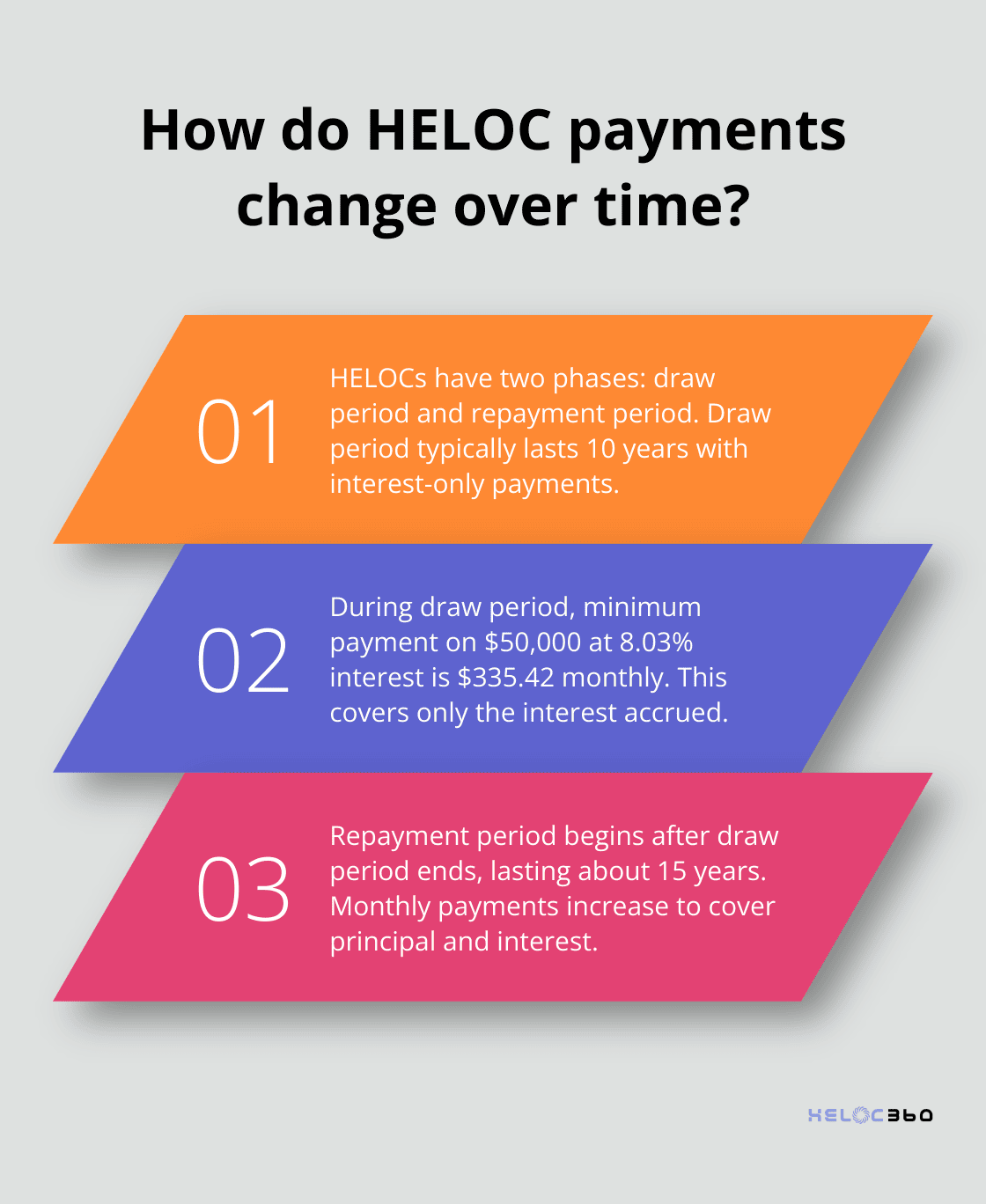

HELOCs operate in two distinct phases: the draw period and the repayment period. The draw period typically lasts 10 years, during which you can borrow from your credit line as needed. Your minimum payments during this time often cover only the interest on the amount you've borrowed.

Draw Period: Interest-Only Payments

In the draw period, your minimum payment calculation depends on the current balance and interest rate. For example, if you borrow $50,000 at a 6% annual interest rate, your monthly interest-only payment will be about $250. This lower payment can attract many borrowers, but it's important to note that it doesn't reduce your principal balance.

Repayment Period: Principal Plus Interest

The repayment period begins after the draw period ends and usually lasts 10 to 20 years. During this phase, your minimum payments include both principal and interest. Using the same example, if you have a 15-year repayment term, your monthly payment will increase to around $422. This significant jump can surprise many homeowners (who aren't prepared for the change).

Factors Influencing Your Minimum Payment

Several elements affect your HELOC minimum payment:

- Interest Rate: Most HELOCs have variable rates tied to the prime rate. When the prime rate changes, your interest rate and minimum payment follow suit.

- Outstanding Balance: Your payment depends on how much you've borrowed, not your total credit line.

- Payment Structure: Some lenders offer options like fixed-rate conversions or interest-only payments throughout the loan term.

- Lender Policies: Different lenders may use varying methods to calculate minimum payments.

The average HELOC interest rate is 8.03%, its lowest level since 2023.

Interest-Only vs. Principal-Plus-Interest: The Impact

Interest-only payments during the draw period can provide short-term financial flexibility, but they come with risks. You won't build equity, and you could face a significant payment increase when the repayment period begins.

On the other hand, making principal-plus-interest payments from the start can help you avoid payment shock and reduce your overall interest costs. For instance, if you borrow $100,000 at 8.03% and make principal-plus-interest payments over a 20-year term, your monthly payment will be about $836. While higher initially, this approach saves you money in the long run and builds equity faster.

Understanding these mechanics plays a key role in effective HELOC management. The next section will guide you through the process of calculating your HELOC minimum payment, providing you with practical tools and examples to make informed decisions about your borrowing and repayment strategies.

How to Calculate HELOC Minimum Payments

Understanding HELOC Payment Structures

HELOC minimum payments vary based on the loan phase. Most HELOCs have two distinct periods: the draw period and the repayment period. Each phase has its own payment structure, which affects how you calculate your minimum payments.

Calculating Interest-Only Payments During the Draw Period

During the draw period (typically 10 years), many HELOCs only require interest payments. To calculate this:

- Determine your current balance

- Find your current interest rate

- Multiply your balance by the annual interest rate

- Divide the result by 12 (months in a year)

For example, if you've borrowed $50,000 at 8.03% (the current average HELOC rate), your monthly interest-only payment would be:

($50,000 x 0.0803) / 12 = $335.42

Calculating Principal and Interest Payments During Repayment

When the repayment period begins, your payments will include both principal and interest. The calculation becomes more complex, involving the loan term and amortization. A simplified formula is:

Monthly Payment = P * (r * (1 + r)^n) / ((1 + r)^n - 1)

Where: P = Principal balance r = Monthly interest rate (annual rate divided by 12) n = Total number of monthly payments

Using our previous example with a 15-year repayment term:

P = $50,000 r = 0.0803 / 12 = 0.00669 n = 15 * 12 = 180

Plugging these numbers into the formula gives us a monthly payment of $477.40.

Tools for Accurate Calculations

Manual calculations can be time-consuming and prone to errors. Online tools offer a more efficient and accurate alternative. Many financial institutions provide HELOC calculators on their websites. The Federal Reserve also offers a reliable HELOC calculator.

Some platforms (like HELOC360) include built-in calculators that allow you to input your specific loan details and see projected payments over the life of your HELOC. These tools can help you compare different scenarios and make informed decisions about your borrowing strategy.

Accounting for Variable Rates

It's important to note that these calculations assume a fixed interest rate, which isn't typical for HELOCs. Variable rates can cause your payments to fluctuate. You should budget for potential increases to avoid financial strain.

Understanding how to calculate your HELOC minimum payments empowers you to make informed financial decisions. The next section will explore strategies for managing these payments effectively and aligning them with your overall financial goals.

How to Optimize Your HELOC Payments

Create a Dedicated HELOC Budget

To manage your HELOC payments effectively, you should create a separate budget for this expense. While rates may be low when you first open your HELOC, it's important to anticipate possible fluctuations, especially over a longer draw period. Analyze your monthly income and expenses to determine how much you can comfortably allocate to your HELOC payment.

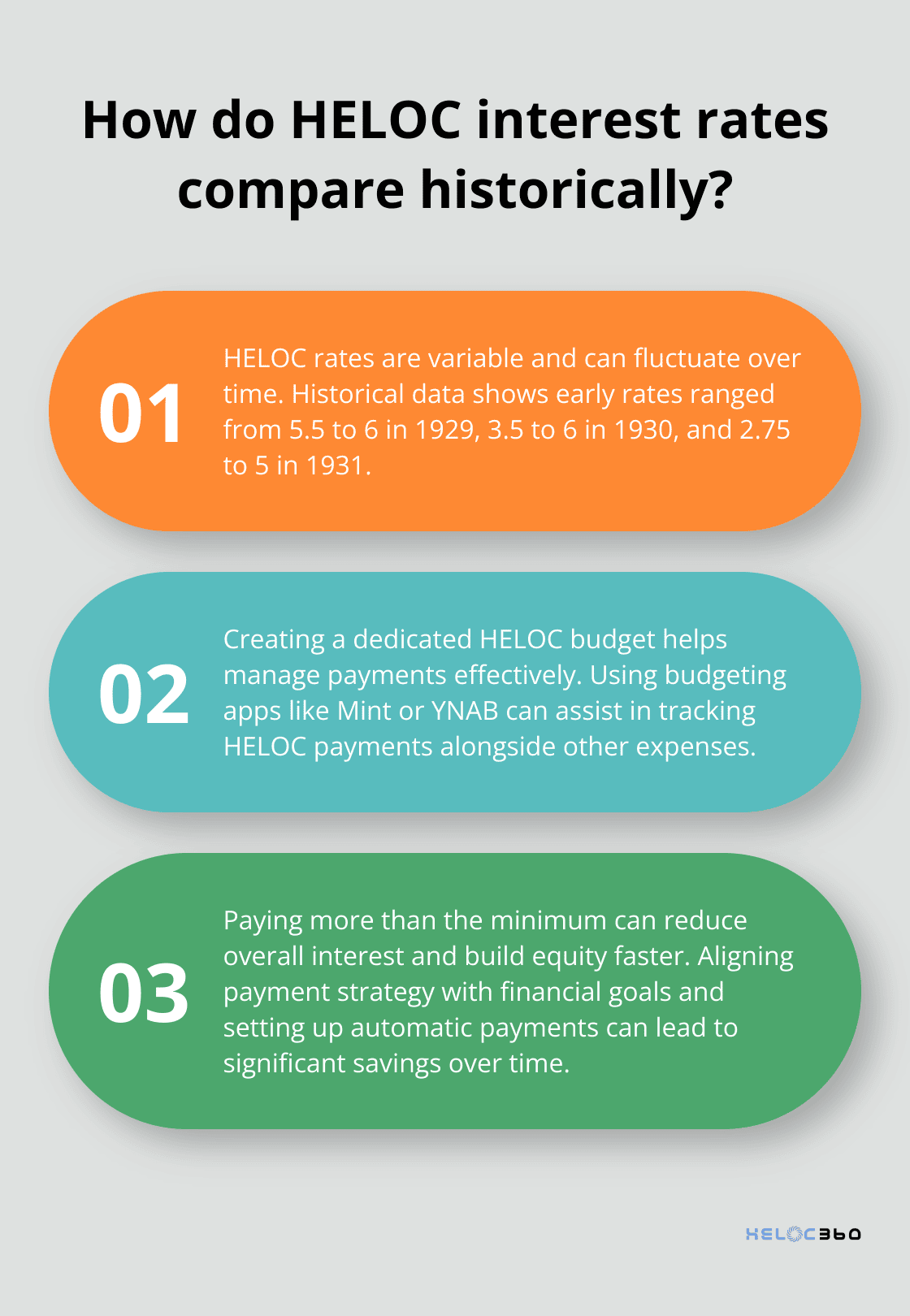

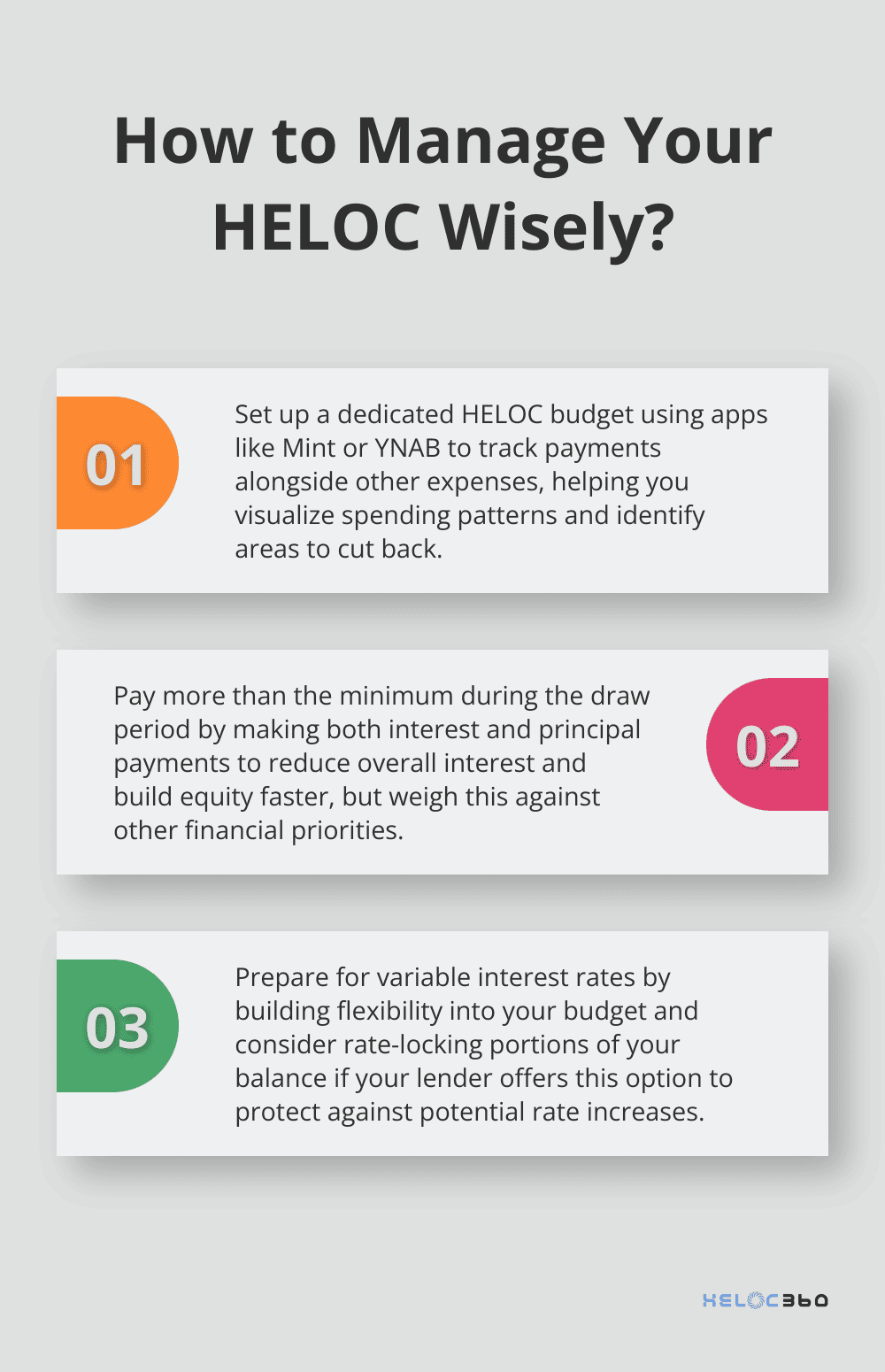

You can use budgeting apps like Mint or YNAB (You Need A Budget) to track your HELOC payments alongside your other expenses. These tools will help you visualize your spending patterns and identify areas where you can cut back to accommodate your HELOC payments more easily.

Pay More Than the Minimum

While making only the minimum payment on your HELOC might seem tempting (especially during the draw period), you will find significant advantages to paying more. Extra contributions towards your principal will reduce the overall interest you'll pay over the life of the loan and build equity faster.

While most HELOCs have an interest-only draw period, you can make both interest and principal payments to pay off the line of credit faster. When the line of credit enters the repayment period, you'll be required to make both principal and interest payments.

However, you should weigh this against other financial priorities. If you have high-interest debt or haven't maxed out your retirement contributions, those areas might be better places to allocate extra funds.

Align Your Payment Strategy with Financial Goals

Your approach to HELOC payments should align with your broader financial objectives. If you use your HELOC for home improvements that will increase your property value, you might choose to make larger payments to build equity faster. On the other hand, if you use the HELOC for debt consolidation, you might focus on paying off the highest-interest debts first while making minimum HELOC payments.

You should set up automatic payments to ensure you never miss a due date. Many lenders offer a small interest rate discount for enrolling in auto-pay, which can add up to significant savings over time.

Prepare for Variable Interest Rates

HELOCs typically have variable interest rates. Historical data shows that early rates ranged from 5.5 to 6 in 1929, 3.5 to 6 in 1930, and 2.75 to 5 in 1931. You should build some flexibility into your budget to accommodate potential rate increases, and consider strategies like rate-locking portions of your balance if your lender offers this option.

Regularly Review Your HELOC Management Approach

You should implement these strategies and regularly review your HELOC management approach to make the most of your home equity while maintaining financial stability. With careful planning and informed decision-making, your HELOC can become a powerful tool for achieving your financial goals.

Final Thoughts

Understanding HELOC minimum payments helps maintain financial stability and maximize home equity benefits. These payments differ between draw and repayment periods, with potential for significant increases when principal repayment begins. Accurate calculation of your HELOC minimum payment enables better budgeting and informed borrowing decisions.

Proactive HELOC management involves creating a dedicated budget and aligning payment strategies with broader financial goals. Paying more than the minimum (when possible) can reduce long-term costs and build equity faster. Variable interest rates require flexibility in your budget to accommodate potential increases.

HELOC360 offers solutions to optimize your HELOC experience and simplify management. Our platform provides expert guidance and connects you with suitable lenders. With strategic planning, your HELOC can become a key component in achieving your long-term financial objectives.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.