Using a HELOC as a Bridge Loan Smart Move?

Table of Contents

Are you considering using a HELOC as a bridge loan? This financial strategy has gained popularity among homeowners looking for flexible financing options.

At HELOC360, we've seen an increasing number of clients exploring HELOC bridge loans as alternatives to traditional bridge financing. In this post, we'll examine the pros and cons of this approach and help you determine if it's the right choice for your situation.

What Are Bridge Loans and HELOCs?

Bridge Loans Explained

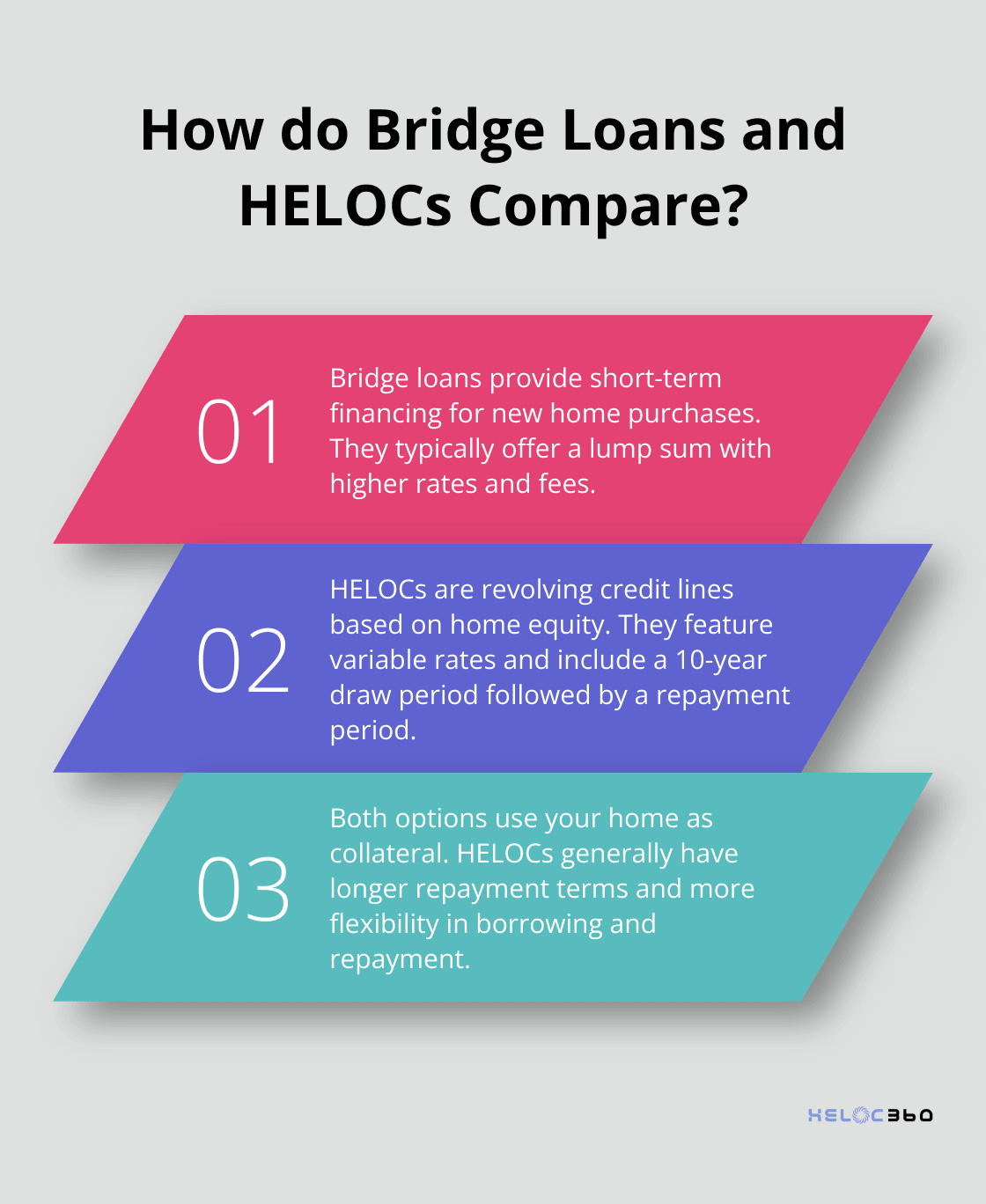

Bridge loans provide short-term financing for homeowners who want to purchase a new property before selling their current one. These loans typically serve as a source of funding until you get permanent financing or pay off debt.

How HELOCs Work

Home Equity Lines of Credit (HELOCs) offer revolving credit based on your home's equity. HELOCs typically feature variable rates, so interest usually increases if market conditions result in higher rates. HELOCs include a draw period (usually 10 years) for borrowing and repaying funds as needed, followed by a repayment period.

Key Differences Between Bridge Loans and HELOCs

The main distinctions between bridge loans and HELOCs lie in their flexibility and cost:

- Bridge loans provide a lump sum but come with higher rates and fees.

- HELOCs offer more flexibility in borrowing and repayment, often with lower rates.

- Both options use your home as collateral, risking foreclosure if you default.

- HELOCs generally have longer repayment terms, which can ease the financial burden.

Choosing Between Bridge Loans and HELOCs

When deciding between these options, you should assess your financial situation, real estate market conditions, and long-term goals. Bridge loans can be useful in competitive markets where quick closings are necessary. HELOCs might suit those seeking ongoing financial flexibility.

Many homeowners appreciate the versatility of HELOCs, which allow them to use funds for purposes beyond just bridging a home purchase (such as home improvements or debt consolidation).

Now that we understand the basics of bridge loans and HELOCs, let's explore the advantages of using a HELOC as a bridge loan alternative.

Why HELOCs Outshine Traditional Bridge Loans

Lower Interest Rates

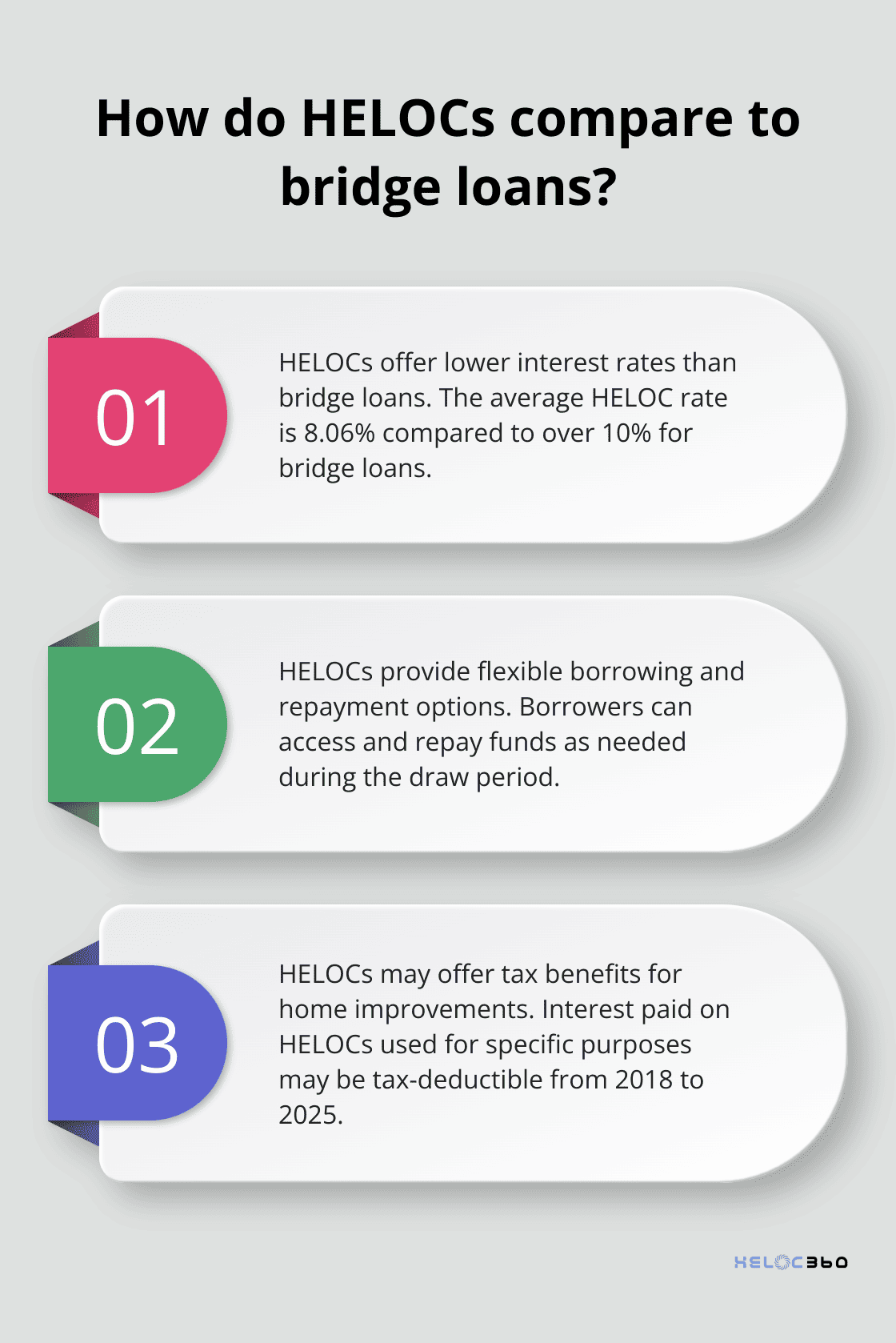

HELOCs offer a cost-effective financing option compared to traditional bridge loans. As of March 5, 2025, the average HELOC interest rate is 8.06 percent, while bridge loans often exceed 10%. This difference results in substantial savings for borrowers.

Consider a $200,000 loan over a one-year period:

- HELOC at 8.06%: Approximately $16,120 in interest

- Bridge loan at 10%: Around $20,000 in interest

The $3,880 difference remains in your pocket, highlighting the financial advantage of HELOCs.

Unmatched Borrowing Flexibility

HELOCs provide a revolving line of credit, allowing borrowers to access and repay funds as needed during the draw period. This flexibility proves invaluable when facing uncertain timelines in real estate transactions.

For example, when selling your current home and buying a new one, you can:

- Draw funds for the down payment on your new home

- Repay the balance when your current home sells

If the sale takes longer than expected, you won't face the rigid repayment schedule typical of bridge loans.

Potential Tax Benefits

The interest paid on a HELOC used for home improvements or to buy, build, or substantially improve your home may be tax-deductible for tax years 2018 through 2025. This potential benefit typically doesn't apply to bridge loans.

(It's important to consult with a tax professional to understand how this applies to your specific situation, as the rules can be complex and benefits depend on factors like loan amount and fund usage.)

Extended Repayment Terms

HELOCs often feature longer repayment terms compared to bridge loans. This extended timeline can ease the financial burden on borrowers, providing more breathing room in their budget.

While bridge loans typically require repayment within less than a year, HELOCs may offer repayment periods of 20 – 30 years. This extended timeframe allows for more manageable monthly payments and reduces the pressure to sell your existing home quickly.

Versatility Beyond Bridge Financing

Unlike bridge loans, which serve a single purpose, HELOCs offer versatility in fund usage. Homeowners can tap into their HELOC for various purposes beyond bridging a home purchase, such as:

- Home improvements

- Debt consolidation

- Education expenses

- Emergency funds

This multi-purpose nature makes HELOCs a valuable financial tool long after the bridge financing need has passed.

As we explore the advantages of using HELOCs as bridge loan alternatives, it's essential to consider potential risks and important factors to weigh before making a decision. Let's examine these considerations in the next section.

Navigating HELOC Risks

Market Volatility and Property Values

Real estate markets can be unpredictable. If property values decline, you might owe more than your home is worth. This scenario (known as being underwater on your mortgage) can complicate your financial situation.

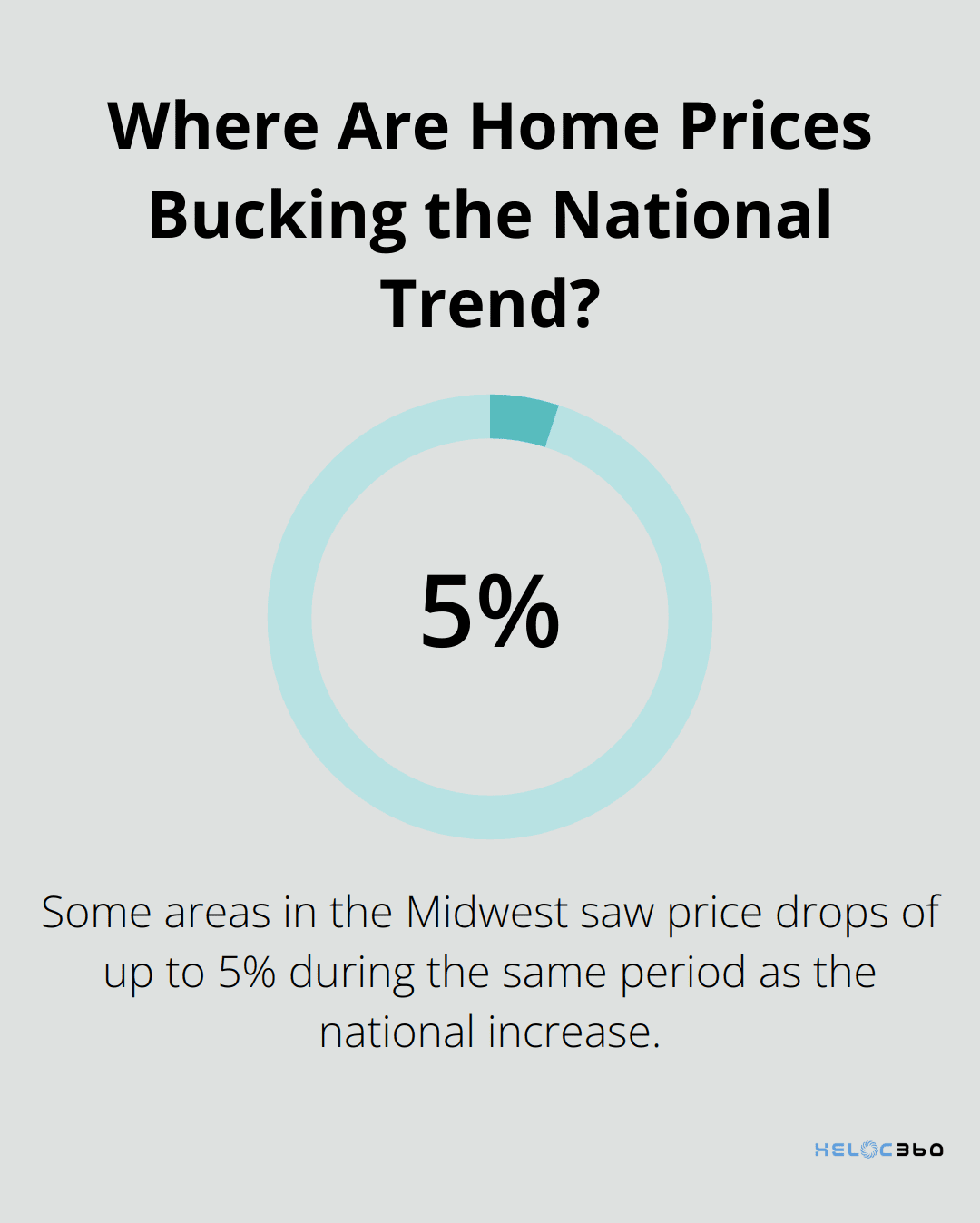

The National Association of Realtors reports home prices increased by 3.8% in February 2024. However, local markets can vary significantly. Some areas in the Midwest saw price drops of up to 5% during the same period.

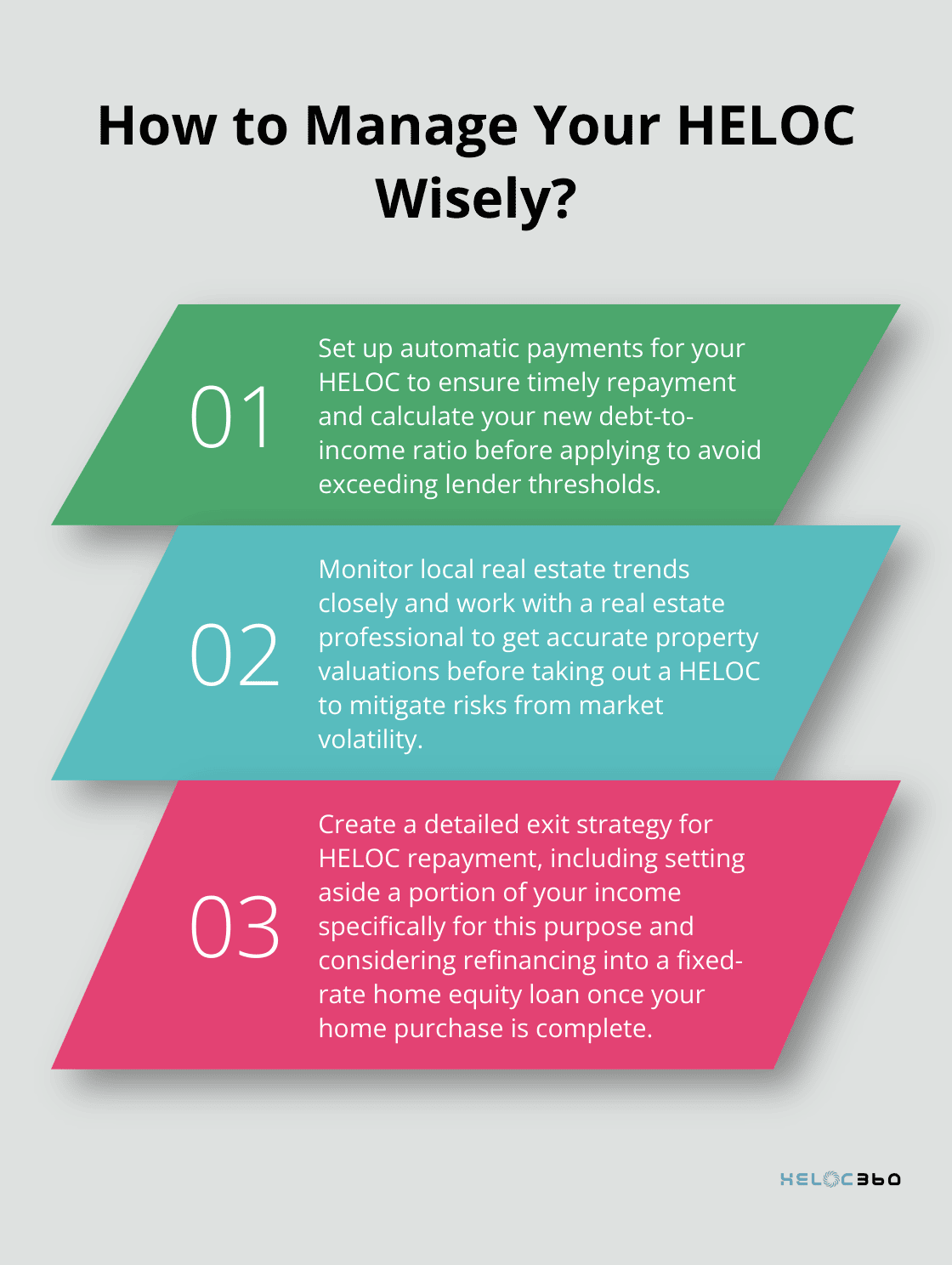

To reduce this risk, monitor your local real estate trends closely. Work with a real estate professional to get accurate property valuations before you take out a HELOC.

Debt-to-Income Ratio Implications

Additional debt through a HELOC can impact your debt-to-income (DTI) ratio. This ratio is a key factor lenders consider when they evaluate loan applications.

Most mortgage programs require a certain DTI ratio. If your HELOC pushes you above this threshold, you might face challenges when you qualify for other loans or refinancing options in the future.

Before you proceed with a HELOC, calculate your current DTI ratio and estimate how it would change with the additional debt. If it exceeds the lender's requirements, consider paying down existing debts or explore alternative financing options.

Developing a Solid Exit Strategy

A clear plan to repay your HELOC is essential. Without one, you risk carrying high-interest debt for an extended period, which potentially jeopardizes your financial stability.

Your exit strategy should account for various scenarios, including:

- Your current home doesn't sell as quickly as expected

- Unexpected changes occur in your income or expenses

- Interest rates fluctuate

One effective approach sets aside a portion of your income specifically for HELOC repayment. Another strategy refinances your HELOC into a fixed-rate home equity loan once you complete your home purchase.

Interest Rate Fluctuations

HELOCs typically come with variable interest rates. This means your payments can increase if market rates rise. The Federal Reserve's actions can significantly impact HELOC rates.

According to Bankrate's national survey, the average HELOC interest rate closed out the previous year almost a full percentage point lower.

To protect yourself from rate increases, consider setting a cap on your HELOC's interest rate or converting a portion of your balance to a fixed-rate option (if your lender offers this feature).

Overextending Your Finances

The easy access to funds that a HELOC provides can tempt you to overspend. This risk increases if you use your HELOC for non-essential expenses beyond its intended purpose as a bridge loan.

Try to stick to your original plan for the HELOC funds. Create a budget that accounts for both your current mortgage and potential HELOC payments to ensure you can comfortably manage both obligations.

Final Thoughts

Using a HELOC as a bridge loan can offer homeowners significant advantages. Lower interest rates, flexible borrowing options, and potential tax benefits make HELOCs an attractive alternative to traditional bridge loans. However, borrowers must consider market fluctuations, property value changes, and the impact on their debt-to-income ratio before making a decision.

We at HELOC360 help homeowners make informed decisions about their home equity. Our platform provides comprehensive solutions tailored to your unique financial goals, whether you consider a HELOC bridge loan or explore other ways to leverage your home's value. We simplify the process, offer expert guidance, and connect you with lenders that match your specific needs.

HELOCs can offer significant advantages, but they're not the right choice for everyone. You must understand the terms, risks, and responsibilities associated with any financial product before you commit. Careful consideration of your options and expert advice will help you make a decision that aligns with your financial objectives and sets you up for long-term success.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.