What is a Home Equity Line of Credit Loan?

Table of Contents

Wondering what is a home equity line of credit loan? You're not alone. Many homeowners are curious about this flexible financing option.

At HELOC360, we're here to demystify HELOCs and help you understand how they work. In this post, we'll break down the key features, benefits, and potential risks of these unique loans.

What Is a HELOC?

Definition and Basics

A Home Equity Line of Credit (HELOC) is a financial product that allows homeowners to borrow against the equity they've built in their property. Unlike traditional loans, HELOCs offer a revolving line of credit, similar to a credit card, but with your home as collateral.

How HELOCs Work

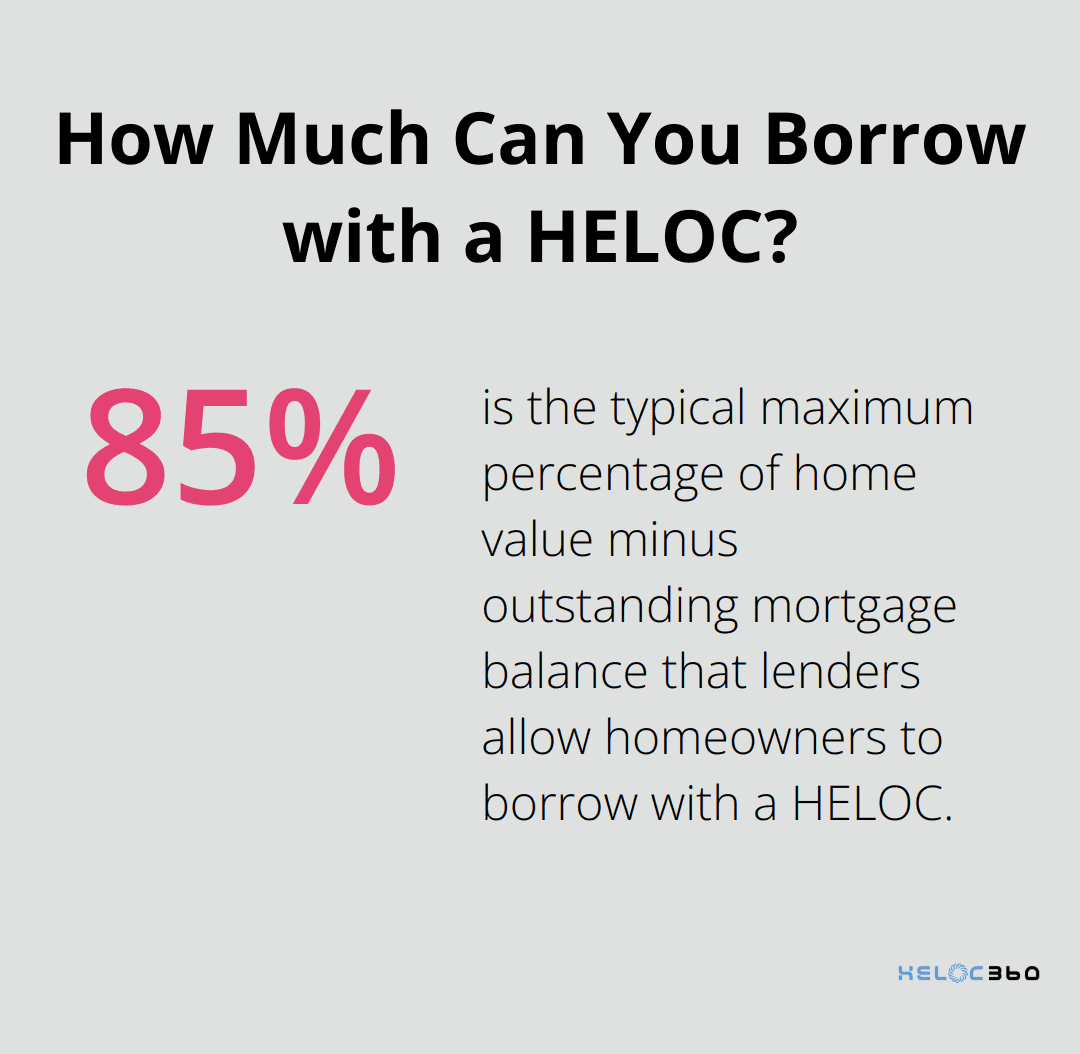

When you take out a HELOC, you receive a credit limit based on your home's value and your outstanding mortgage balance. For example, if your home is worth $300,000 and you owe $200,000 on your mortgage, you have $100,000 in equity. Lenders typically allow you to borrow up to 85% of your home's value minus your outstanding mortgage balance.

Phases of a HELOC

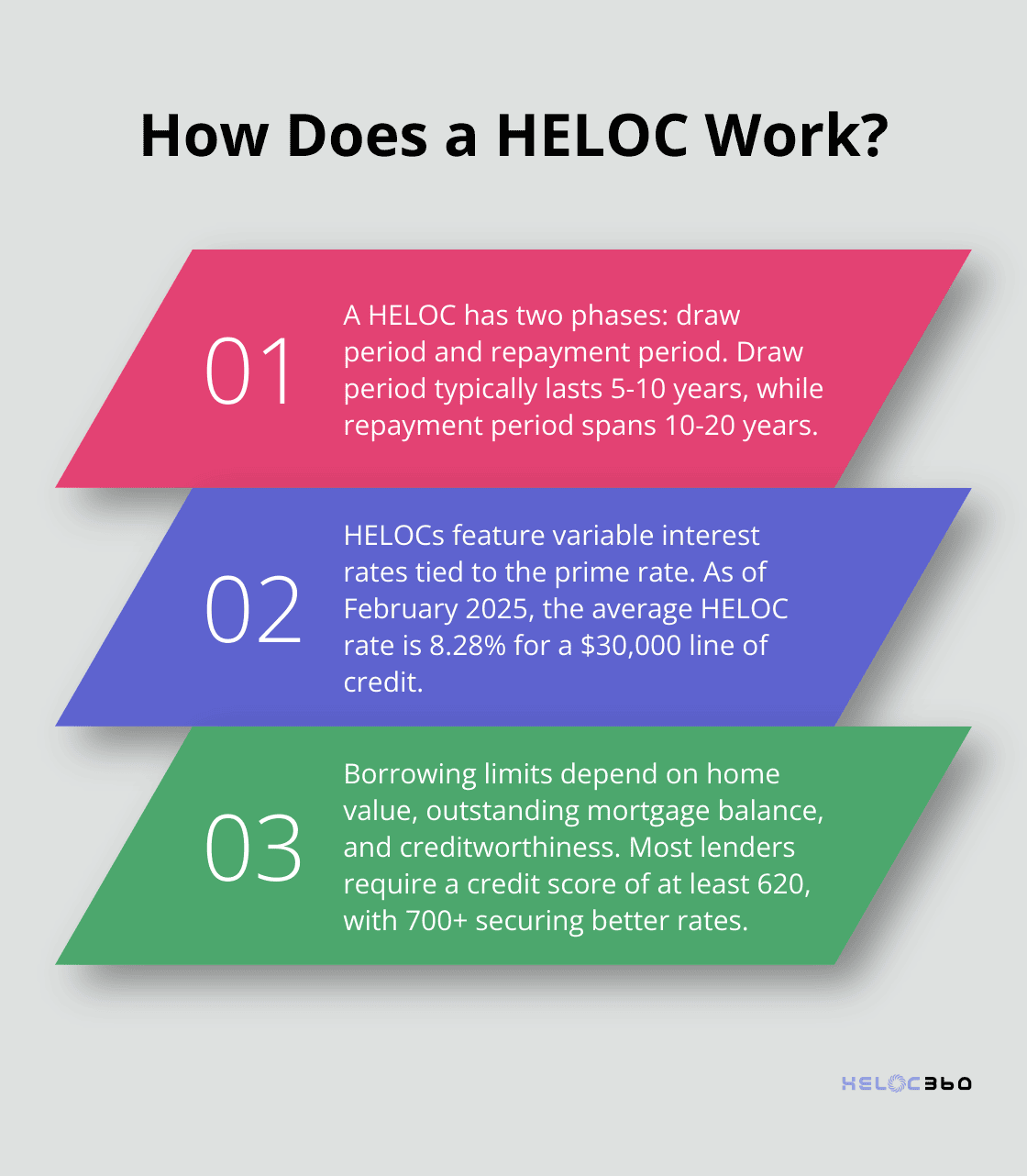

HELOCs have two distinct phases:

- Draw Period: This phase usually lasts 5-10 years. During this time, you can borrow funds as needed up to your credit limit. You'll only pay interest on the amount you've borrowed.

- Repayment Period: Once the draw period ends, you enter the repayment period. You can no longer borrow funds and must repay the principal plus interest.

Variable Interest Rates

One key feature of HELOCs is their variable interest rates. These rates typically tie to the prime rate, which means your monthly payments can fluctuate. As of February 2025, the average HELOC rate is 8.28% for a $30,000 line of credit. However, this rate can change based on market conditions and your creditworthiness.

Flexibility and Risks

HELOCs offer flexibility and potentially lower interest rates compared to other forms of borrowing. However, they also come with risks, including the possibility of losing your home if you can't make payments. It's important to carefully consider your financial situation and long-term goals before applying for a HELOC.

Now that we've covered the basics of HELOCs, let's explore how these loans differ from traditional loans and examine their unique features in more detail.

How a HELOC Really Works

The Two-Phase Structure

A Home Equity Line of Credit (HELOC) operates differently from traditional loans. Home equity loans and HELOCs are both secured by the borrower's home, and they usually have much more attractive interest rates. It has two distinct phases: the draw period and the repayment period. The draw period typically lasts 5-10 years. During this time, you can borrow funds up to your credit limit as needed. You'll only pay interest on the amount you've borrowed, which provides flexibility in managing your finances.

The repayment phase begins after the draw period ends. This period often spans 10-20 years. You can no longer borrow funds and must repay both principal and interest. Your monthly payments may increase significantly during this phase, as you now pay down the principal in addition to interest.

Variable Interest Rates and Their Impact

HELOCs feature variable interest rates, typically tied to the prime rate. This means your monthly payments can fluctuate based on market conditions. As of February 2025, the average HELOC rate is 8.28% for a $30,000 line of credit (according to Bankrate).

This variability can benefit you when rates are low, but it also means your payments could increase if rates rise. Some lenders offer the option to convert a portion of your balance to a fixed rate, providing more stability in your payments. However, these fixed rates are usually higher than the initial variable rate.

Borrowing Limits and Credit Requirements

Your HELOC borrowing limit is typically determined by three factors: your home's value, your outstanding mortgage balance, and your creditworthiness. Most lenders allow you to borrow up to a certain percentage of your home's value minus your outstanding mortgage balance.

For example, if your home is worth $400,000 and you owe $250,000 on your mortgage, your maximum HELOC amount would be calculated based on these factors.

Credit requirements for HELOCs are generally stricter than for credit cards. Lenders typically look for a credit score of at least 620, though a score of 700 or higher will likely secure you better rates. Your debt-to-income ratio is also a key factor, with most lenders preferring a ratio of 43% or lower.

Risks and Considerations

While HELOCs offer flexibility, they also come with risks. The most significant risk is the possibility of losing your home if you can't make payments. It's essential to carefully consider your financial situation before applying for a HELOC.

Additionally, a significant decrease in your home's value could restrict your access to additional credit under the HELOC. In harsher financial circumstances, lenders might even freeze your access to funds.

Now that we've explored how HELOCs work, let's examine their advantages and disadvantages to help you determine if this financial tool aligns with your needs and goals.

Are HELOCs Right for You?

Flexibility: A Double-Edged Sword

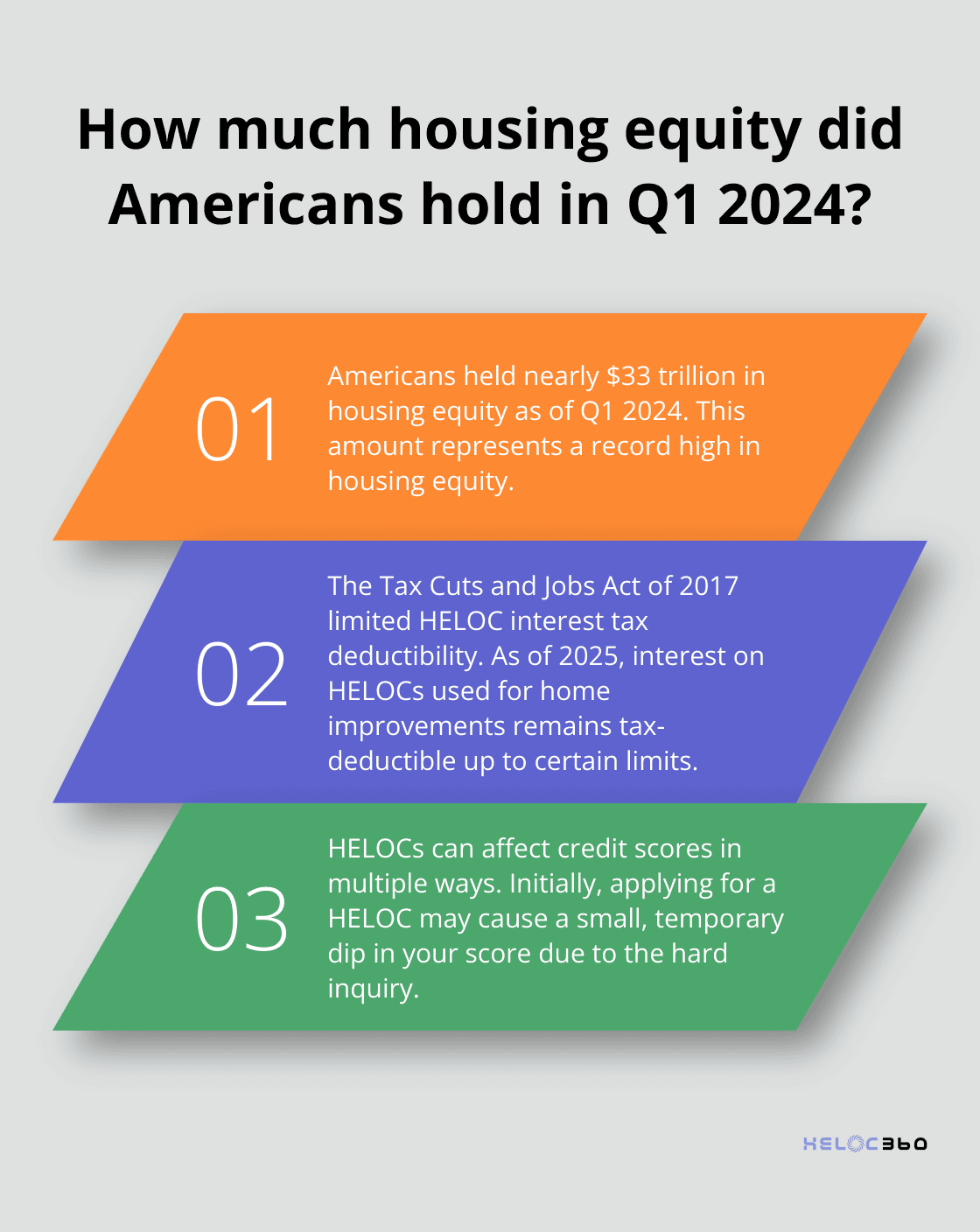

HELOCs offer unparalleled flexibility in borrowing and repayment. The flexibility of a HELOC can make it a great resource for managing cash flow, with quick access to funds that can be repaid. This feature benefits ongoing expenses like home renovations or education costs. However, this flexibility can lead to overspending if not managed carefully. According to Federal Reserve data, Americans held nearly $33 trillion in housing equity as of the first quarter of 2024 – a record amount.

Tax Implications: Potential Savings

The Tax Cuts and Jobs Act of 2017 limited the tax deductibility of HELOC interest, but some borrowers may still benefit. As of 2025, interest on HELOCs used for home improvements remains tax-deductible up to certain limits. Consult with a tax professional to understand how this might apply to your situation.

Risk Assessment: Your Home on the Line

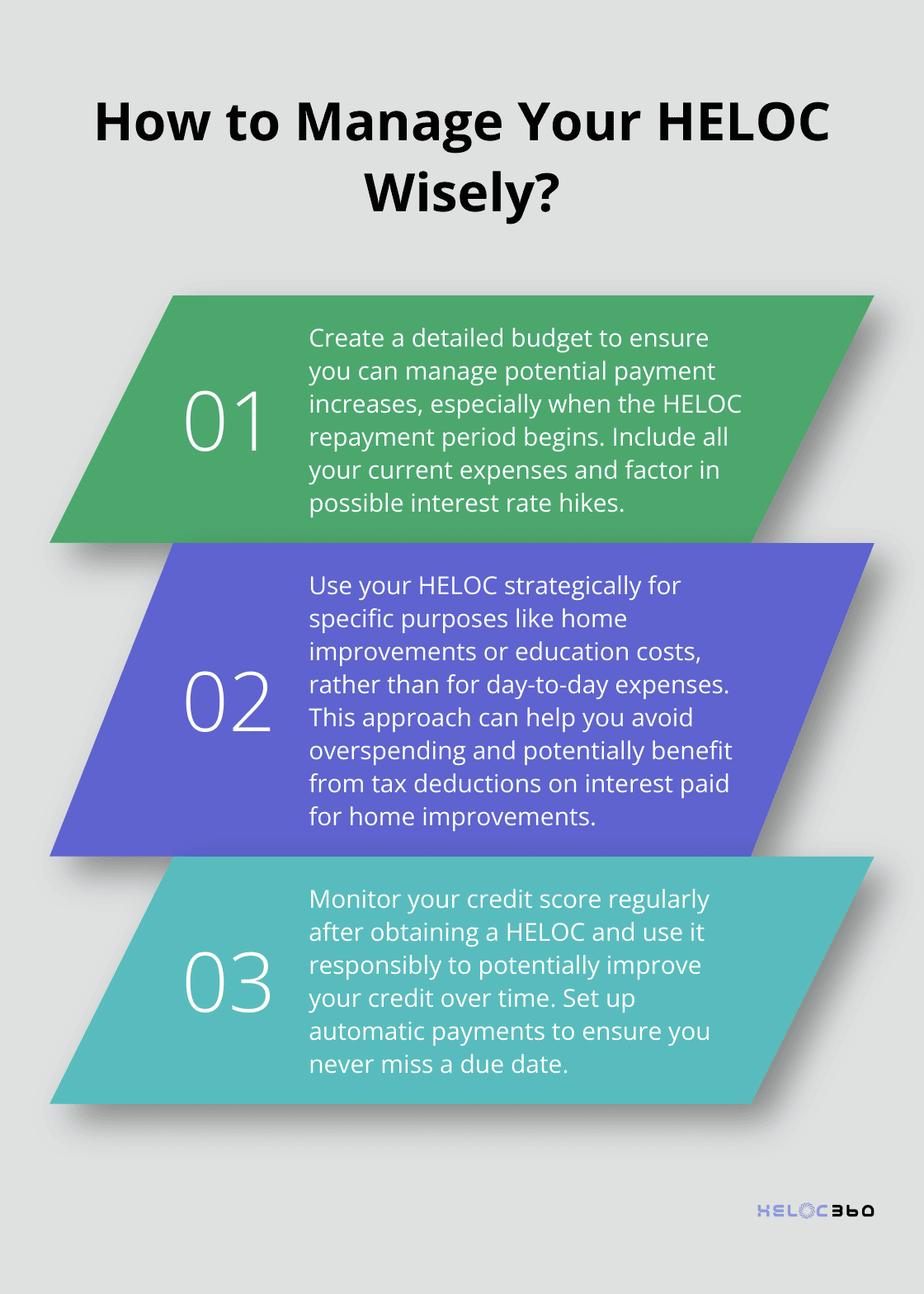

Using your home as collateral presents a significant risk. If you default on payments, you could lose your home. The CFPB will continue to monitor and review the home equity contract market to ensure compliance with federal consumer financial laws. Before applying for a HELOC, assess your financial stability and future income prospects. Create a detailed budget to ensure you can manage potential payment increases, especially when the repayment period begins.

Credit Score Impact: A Balancing Act

HELOCs affect your credit score in multiple ways. Initially, applying for a HELOC may cause a small, temporary dip in your score due to the hard inquiry. However, responsible use of your HELOC can positively impact your credit over time. Monitor your credit regularly and use your HELOC strategically to maximize its benefits while minimizing risks.

Expert Guidance: Making Informed Decisions

Choosing a HELOC involves complex considerations. Platforms like HELOC360 provide personalized guidance to help you navigate these factors and find the right solution for your unique financial situation. With expert advice, you can make an informed decision about whether a HELOC will help you achieve your financial goals.

Final Thoughts

Home Equity Lines of Credit (HELOCs) provide homeowners with a unique way to access their property's value. These financial tools offer funds based on your home's equity, with variable interest rates and two phases: the draw period and the repayment period. Understanding what a home equity line of credit loan is will help you make informed financial decisions.

HELOCs offer flexibility and potentially lower interest rates compared to other borrowing forms, but they also carry risks. You must assess your ability to manage potential payment increases, especially when transitioning from the draw period to the repayment period. Your credit score, debt-to-income ratio, and current home value all influence your eligibility and borrowing limits for a HELOC.

Navigating the complexities of HELOCs can challenge many homeowners. HELOC360 is a platform that helps homeowners unlock their home equity potential. We provide expert guidance and connect you with lenders that fit your needs, making it easier to achieve your financial goals. Take the time to research, consult with professionals, and use resources like HELOC360 to ensure you make choices that align with your financial objectives and risk tolerance.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

Best Home Equity Line of Credit Lenders: A Comparison

Compare home equity line of credit best lenders. Find top options for rates, terms, and customer service to make informed financial decisions.