Home Equity Lines of Credit (HELOCs) often seem like an attractive financial option, but they come with significant drawbacks that many homeowners overlook.

At HELOC360, we’ve seen countless cases where HELOCs have led to financial strain rather than relief. This post will explore the hidden risks and common pitfalls of HELOCs, as well as better alternatives for accessing your home’s equity.

By understanding these HELOC drawbacks, you’ll be better equipped to make informed decisions about your financial future.

Are HELOCs Too Good to Be True?

The Interest Rate Rollercoaster

HELOCs typically come with variable interest rates. This feature can cause your payments to skyrocket unexpectedly. In 2024, HELOC rates fluctuated between 6.5% and 8.5%. These rates can change rapidly, leaving borrowers in a precarious financial position. The Federal Reserve Bank of New York reported that HELOC balances hit $387 billion in Q3 2024. This surge in popularity could push rates even higher in the future.

The Overspending Trap

A HELOC makes it easy to borrow more than you can afford. The HELOC utilization rate increased from 37.74% to 39.81% over three years. This statistic indicates that more homeowners max out their credit lines. Using your HELOC for non-essential purchases (like vacations or luxury items) can quickly lead to financial trouble.

Your Home at Risk

Many homeowners overlook a critical risk: missing HELOC payments can result in foreclosure. A Bankrate Home Equity Insights Survey revealed that 16% of homeowners believe there’s no acceptable reason to tap into their home equity. These cautious homeowners have a point. When you use your home as collateral for everyday expenses or risky investments, you put your most valuable asset in jeopardy.

The Hidden Costs

HELOCs often come with hidden fees that can add up quickly. These may include annual fees, transaction fees, and inactivity fees. Some lenders also charge hefty penalties for early repayment. These additional costs can significantly increase the total amount you owe, making it harder to pay off your HELOC in the long run.

The Unpredictable Future

Economic conditions can change rapidly, affecting your ability to repay your HELOC. Job loss, medical emergencies, or a sudden drop in home values can all impact your financial stability. In such situations, a HELOC can transform from a helpful financial tool into a burdensome debt that threatens your homeownership.

While HELOCs aren’t inherently bad and can be useful for home improvements or emergencies, it’s essential to understand these risks fully. Before you consider a HELOC, explore all your options. Personal loans, cash-out refinancing, or building up your savings might offer more stability and less risk to your home. In the next section, we’ll explore common HELOC pitfalls that every homeowner should avoid.

HELOC Traps That Can Sink Your Finances

The Luxury Spending Trap

HELOCs can lead to financial quicksand if you don’t exercise caution. Many homeowners fall into the trap of using HELOC funds for non-essential purchases. This behavior erodes your home’s value and puts you at risk of owing more than your home is worth if property values decline.

In 2024, a concerning trend emerged: homeowners tapped into their equity for vacations, designer goods, and other luxuries. The Federal Reserve Bank of New York reported HELOC balances reached $402 billion in Q3 2024. This surge suggests many homeowners use their home equity as a piggy bank, rather than a tool for strategic financial moves.

The Draw Period Danger Zone

HELOC borrowers often ignore their draw period end date. HELOCs typically have a 10-year draw period where you can borrow funds and make interest-only payments. When this period ends, you must start repaying both principal and interest, which can lead to payment shock.

Consider this example: If you borrow $100,000 at 7% interest during a 10-year draw period, your monthly payment might jump from about $583 (interest-only) to $1,161 when you enter the repayment period. This sudden increase has caught many homeowners off guard, leading to financial distress (and in some cases, foreclosure).

The True Cost Conundrum

Many homeowners underestimate the total cost of borrowing with a HELOC. HELOCs often have variable interest rates, which means your payments can increase significantly over time. In 2025, the national average HELOC rate was 8.22% according to Bankrate. This volatility can make budgeting difficult and increase your overall borrowing costs.

Moreover, homeowners often overlook additional fees associated with HELOCs. These can include annual fees, inactivity fees, and early closure fees. Some lenders charge up to $75 annually just to maintain the line of credit, even if you’re not using it.

The Hidden Fee Surprise

When you sign up for a HELOC, you might not realize the extent of hidden fees that can accumulate. These fees can significantly increase the total cost of your loan. Common hidden fees include:

- Appraisal fees

- Title search fees

- Application fees

- Annual maintenance fees

- Inactivity fees

Some lenders even charge cancellation or early termination fees if you decide to close your HELOC before a specified time. These hidden costs can add up quickly, turning your seemingly affordable HELOC into an expensive financial burden.

The Foreclosure Risk

One of the most serious risks of a HELOC is the potential for foreclosure. Because your home serves as collateral for the loan, failing to make payments can result in losing your house. This risk becomes even more pronounced if you’ve used your HELOC for non-essential expenses or investments that don’t pan out.

The foreclosure risk intensifies during economic downturns when job losses increase and home values may decrease. In such scenarios, homeowners who have maxed out their HELOCs might find themselves underwater on their mortgages, making it difficult to refinance or sell the property to avoid foreclosure.

To avoid these pitfalls, you must have a clear purpose for your HELOC funds and a solid repayment plan. Try alternatives like personal loans or home equity loans with fixed rates for more predictable payments. Always read the fine print to understand all associated costs.

In the next section, we’ll explore better alternatives to HELOCs that can help you access your home equity without exposing yourself to these risks.

What Are Better Options Than HELOCs?

Cash-Out Refinancing: A Fixed-Rate Solution

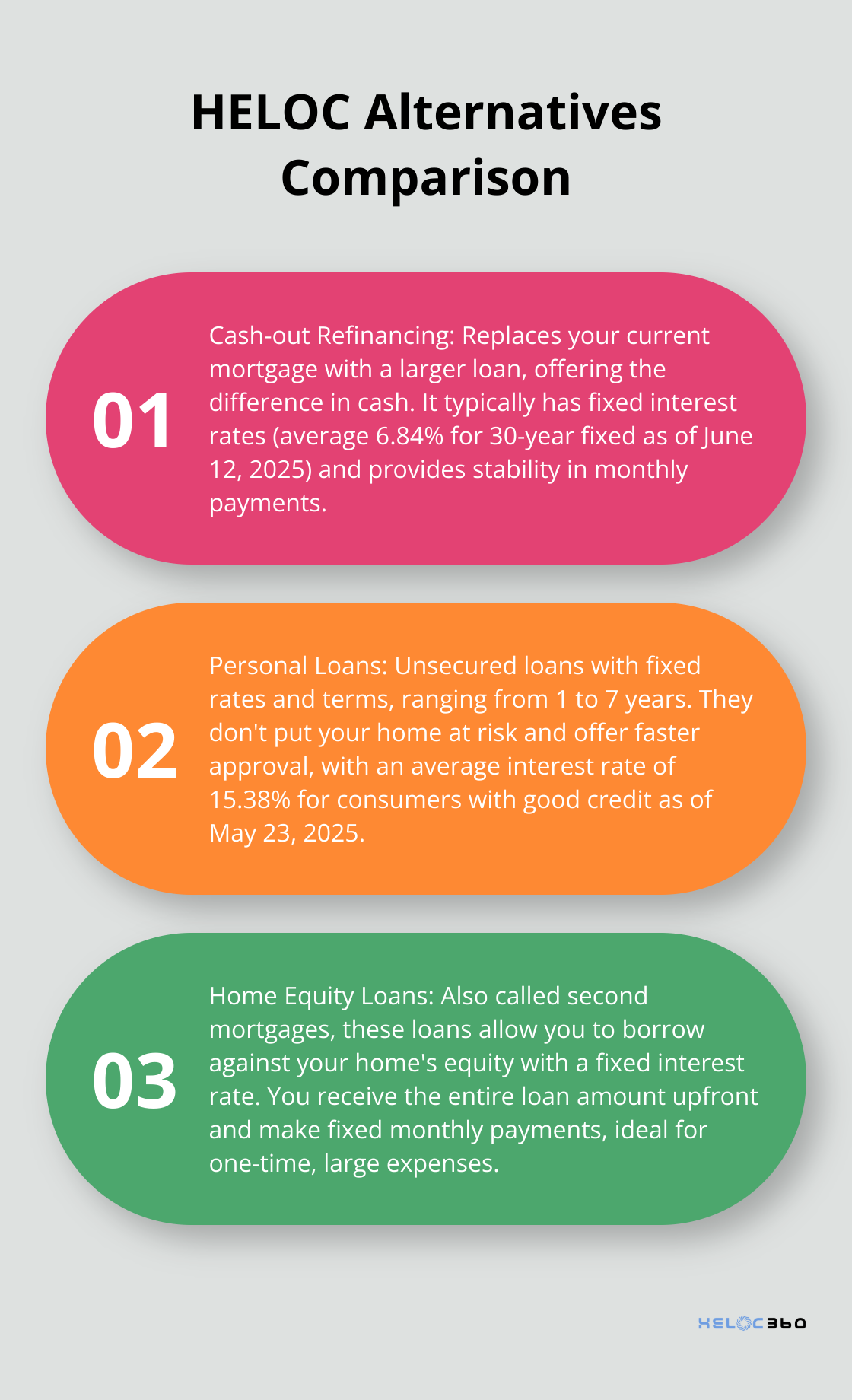

Cash-out refinancing replaces your current mortgage with a new, larger loan. The difference is paid out in cash. Unlike HELOCs, cash-out refinancing typically offers fixed interest rates. As of June 12, 2025, the average 30-year fixed refinance rate was 6.84% (according to Freddie Mac). This option provides stability in your monthly payments, which makes budgeting easier.

However, refinancing costs can be substantial. You’ll also reset your mortgage term, which potentially means paying more interest over time. But if you need a large sum and want predictable payments, cash-out refinancing could be your best bet.

Personal Loans: Quick and Unsecured

Personal loans offer a way to borrow without using your home as collateral. They typically have fixed rates and terms, ranging from 1 to 7 years. As of May 23, 2025, the average personal loan interest rate for consumers with good credit (690 to 719 credit score) was 15.38%.

While rates are higher than HELOCs, personal loans don’t put your home at risk. They’re also faster to obtain – many lenders offer same-day approval and funding within a week. If you need a smaller amount and want to avoid using your home equity, a personal loan could be ideal.

Home Equity Loans: The Fixed-Rate HELOC Alternative

Home equity loans, often called second mortgages, allow you to borrow against your home’s equity with a fixed interest rate. Unlike HELOCs, you receive the entire loan amount upfront and make fixed monthly payments.

Home equity loans are best for one-time, large expenses where you know exactly how much you need to borrow.

Savings and Budgeting: The Safest Path

The safest alternative to a HELOC is often not borrowing at all. Creating a robust savings plan and budget can help you achieve your financial goals without risking your home or taking on debt.

Start by tracking your expenses for a month. Redirect this money into a high-yield savings account.

For larger goals, consider automating your savings. Set up automatic transfers to a dedicated savings account each payday. Even small amounts add up over time.

These alternatives might not provide immediate access to large sums like a HELOC, but they offer more financial stability and less risk to your home. Always consider your long-term financial health when choosing between borrowing options.

Final Thoughts

HELOCs can seem attractive, but they come with significant drawbacks. Variable interest rates, potential overextension of finances, and foreclosure risks are just a few HELOC drawbacks homeowners must consider. Alternatives like cash-out refinancing, personal loans, and home equity loans might better suit your financial situation.

Careful financial planning is essential when considering any form of borrowing, especially one that puts your home on the line. You should assess your financial goals, evaluate your ability to repay, and consider the long-term implications of your decision. We at HELOC360 want to help you explore your home equity options further.

Our platform guides homeowners through home equity borrowing complexities, providing tailored solutions and connecting you with suitable lenders. We believe in empowering homeowners with knowledge and options, ensuring you make the best decision for your financial future. Your home is likely your most valuable asset, so any decision involving your home equity should be made with careful consideration and expert guidance.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.