HELOC vs Cash-Out Refinance: Which is Better?

Table of Contents

Homeowners often face a crucial decision when tapping into their home equity: choosing between a home equity line of credit (HELOC) vs. cash-out refinance. Both options offer unique advantages and potential drawbacks.

At HELOC360, we understand the importance of making an informed choice. This guide will break down the key differences between these two popular financing methods, helping you determine which option best suits your financial needs and goals.

What Is a HELOC?

Definition and Basic Features

A Home Equity Line of Credit (HELOC) is a financial tool that allows homeowners to access their home's equity. It functions as a revolving line of credit, similar to a credit card, but uses your home as collateral. This unique structure provides flexibility for borrowers who need access to funds over time.

How HELOCs Work

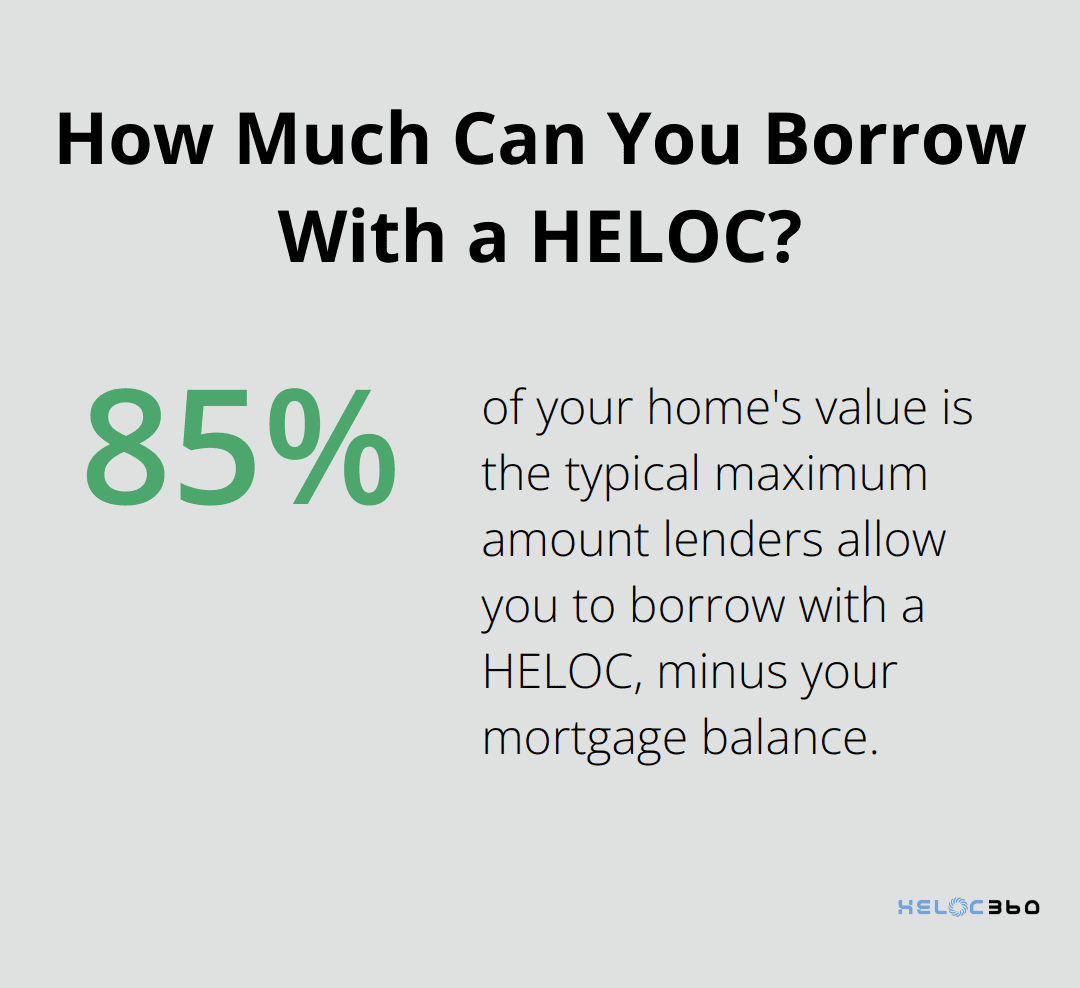

When you apply for a HELOC, lenders determine your credit limit based on your home's value and your outstanding mortgage balance. Most lenders allow you to borrow up to 85% of your home's value, minus your mortgage balance. For instance, if your home is worth $300,000 and you owe $200,000 on your mortgage, you might qualify for a HELOC of up to $55,000 (85% of $300,000 = $255,000, minus $200,000).

HELOCs operate in two distinct phases:

- Draw Period: This phase typically lasts 5 to 10 years. During this time, you can borrow from your credit line as needed, often making only interest payments.

- Repayment Period: Once the draw period ends, you enter the repayment phase. You can no longer borrow funds and must repay both principal and interest.

Interest Rates and Terms

HELOC interest rates are usually variable, tied to the prime rate plus a margin. As of January 2025, the average HELOC rate stands at approximately 8.62% for standard HELOCs and 9.12% for interest-only HELOCs, according to Bankrate. However, rates can vary significantly based on factors such as your credit score and loan-to-value ratio.

The variable nature of HELOC rates means your payments can fluctuate over time. This aspect can make budgeting more challenging compared to fixed-rate loans. Some lenders offer rate caps to limit potential increases, which can provide additional security for borrowers.

HELOC terms vary, but a common structure includes a 10-year draw period followed by a 20-year repayment period. Some lenders offer different term lengths, so it's beneficial to compare options to find the best fit for your financial situation.

Common Uses for HELOCs

Homeowners often use HELOCs for:

- Home improvements (e.g., kitchen remodels, bathroom upgrades)

- Debt consolidation

- Education expenses

- Emergency funds

- Business investments

The flexibility of a HELOC makes it particularly useful for ongoing expenses or projects with uncertain costs. However, it's important to have a solid repayment plan in place, as your home serves as collateral for the loan.

As we move forward, let's explore another popular option for accessing home equity: cash-out refinancing. This alternative approach offers its own set of advantages and considerations, which we'll discuss in detail in the next section.

Cash-Out Refinance Explained

What is Cash-Out Refinancing?

Cash-out refinancing allows homeowners to take out a larger mortgage loan, use the proceeds to pay off their existing mortgage and receive the remaining funds as a lump sum. This strategy can potentially secure better loan terms while accessing your home's equity.

The Process of Cash-Out Refinancing

When you choose a cash-out refinance, you take out a new mortgage for more than you currently owe. For instance, if your home is worth $300,000 and you owe $200,000 on your current mortgage, you might refinance for $250,000. This would provide you with $50,000 in cash (minus closing costs).

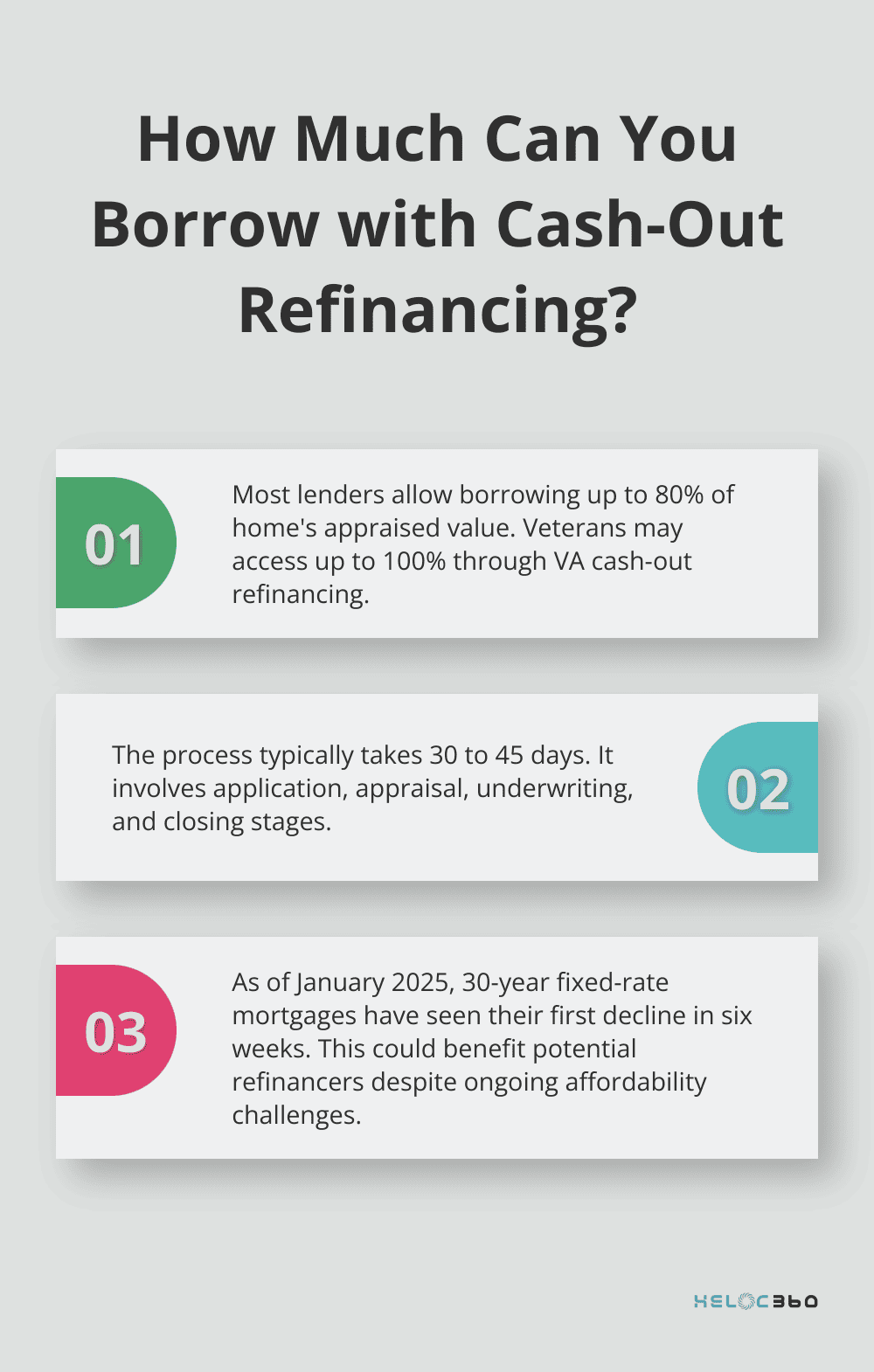

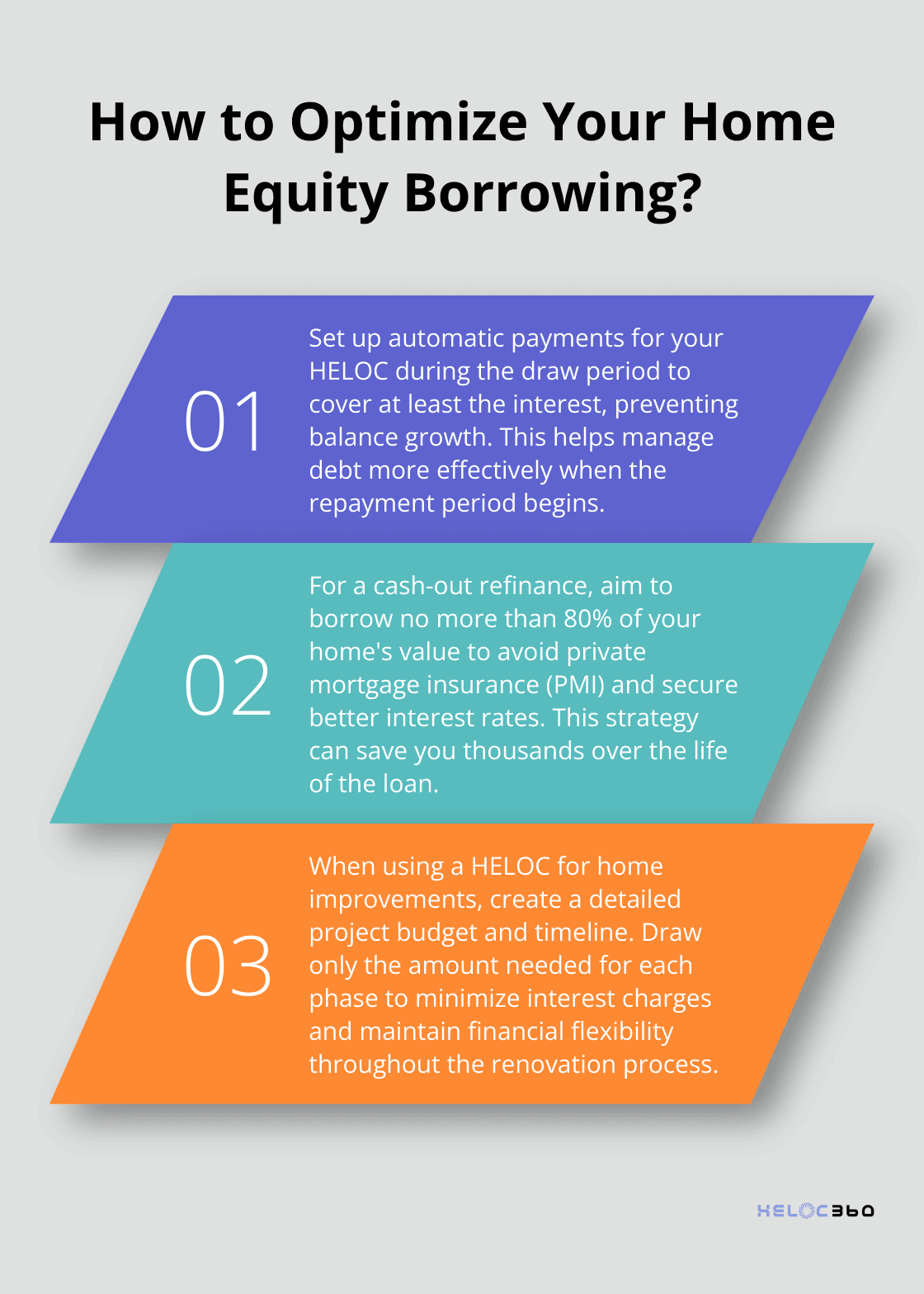

Most lenders permit borrowing up to 80% of your home's appraised value, minus any existing mortgage balance. However, the exact amount depends on factors such as your credit score, debt-to-income ratio, and the type of loan you select. Veterans may access up to 100% of their home's value through VA cash-out refinancing.

The process typically takes 30 to 45 days and involves several steps:

- Application: You provide financial information and documentation.

- Appraisal: An expert determines your home's current market value.

- Underwriting: The lender reviews your application and decides whether to approve the loan.

- Closing: You sign the new loan documents and receive your funds.

As of January 2025, the 30-year fixed-rate mortgage has seen its first decline in six weeks, according to Freddie Mac's Primary Mortgage Market Survey. While affordability challenges remain, this is welcome news for potential refinancers.

Strategic Uses for Cash-Out Refinancing

While you can use the cash from refinancing for any purpose, some applications are more financially prudent than others. Here are some strategic uses:

- Home Improvements: Investing in your property can increase its value. Kitchen remodels, for example, can recoup up to 75% of their cost (according to Remodeling Magazine's 2024 Cost vs. Value Report).

- Debt Consolidation: Using cash-out refinancing to pay off high-interest debt can save you money. For example, consolidating credit card debt into a lower-interest mortgage could save you thousands in interest over time.

- Education Funding: With rising college tuition costs, cash-out refinancing can offer a lower-cost alternative to student loans.

- Investment Opportunities: Some homeowners use their equity to invest in rental properties or start businesses. However, this strategy carries risks and requires careful consideration.

- Emergency Fund: Building a robust emergency fund can provide financial security. Financial experts often recommend saving 3-6 months of living expenses.

It's important to weigh the long-term implications of cash-out refinancing. While you might benefit from lower interest rates or debt consolidation, you're also extending your loan term and potentially increasing your overall debt. Always consider your financial goals and consult with a financial advisor before making a decision.

Now that we've explored cash-out refinancing, let's compare it to HELOCs to help you determine which option might better suit your financial needs.

Which Option Fits Your Financial Needs

Interest Rates and Repayment Terms

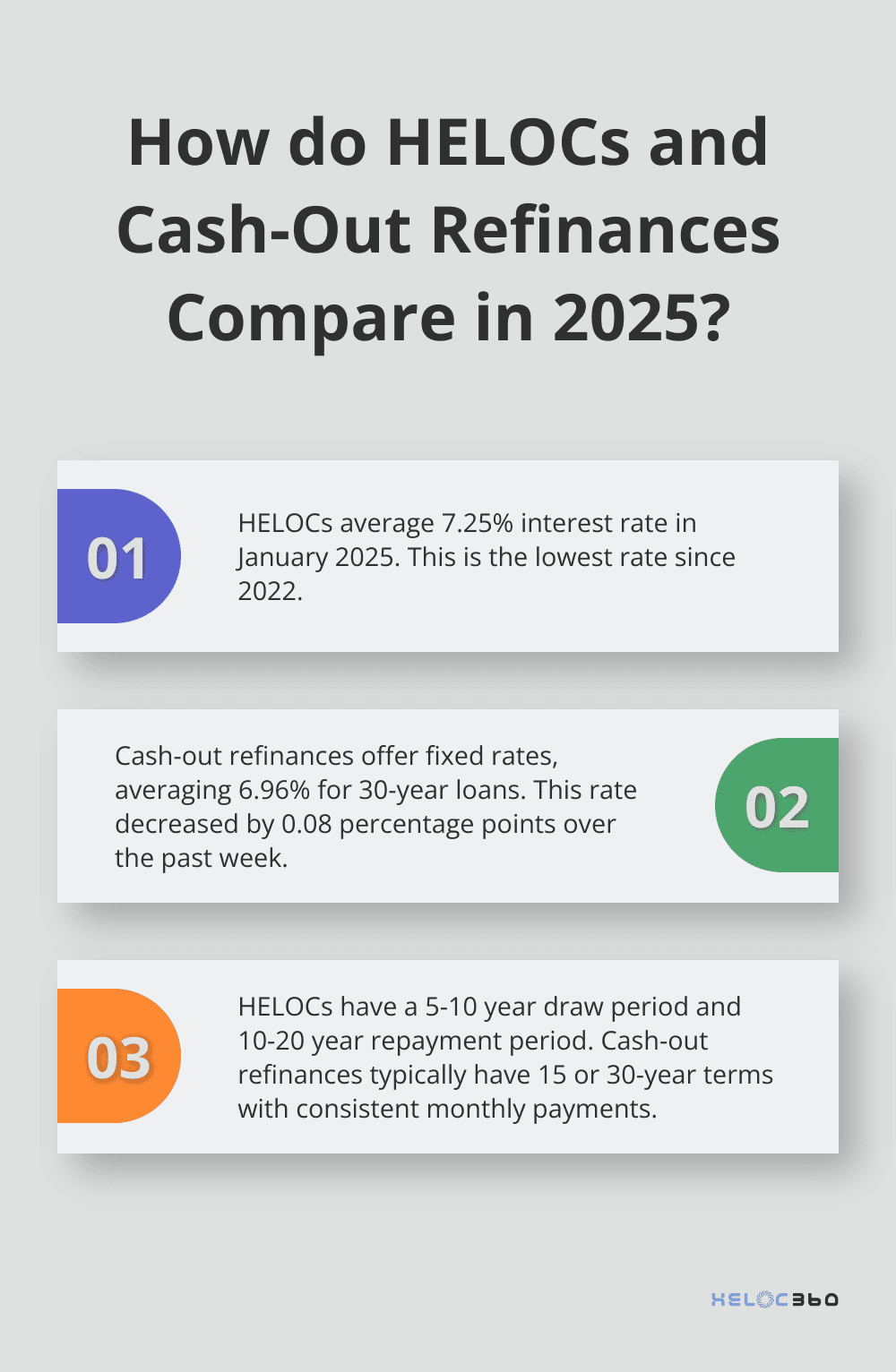

HELOCs typically come with variable interest rates. As of January 2025, McBride forecasts HELOCs to average 7.25 percent - a low not seen since 2022. These rates usually tie to the prime rate, which means your payments can change as market conditions shift.

Cash-out refinances often offer fixed interest rates. Freddie Mac's benchmark rate for a 30-year fixed-rate loan averaged 6.96%, a decrease of 0.08 percentage points over the past week. This stability can make budgeting easier over the long term.

Repayment terms also differ significantly. HELOCs usually have a draw period of 5-10 years, followed by a repayment period of 10-20 years. During the draw period, you might only pay interest on the amount borrowed. Cash-out refinances typically have a set term (often 15 or 30 years) with consistent monthly payments covering both principal and interest.

Impact on Your Existing Mortgage

A cash-out refinance replaces your current mortgage entirely. This means you'll have a new loan amount, potentially a new interest rate, and a reset loan term. If you've already paid off a significant portion of your original mortgage, starting over with a 30-year term could mean paying more interest over time.

HELOCs act as a second lien on your property, leaving your original mortgage untouched. This can benefit you if you already have a low interest rate on your primary mortgage and don't want to disturb it.

Flexibility in Borrowing and Repayment

HELOCs offer more flexibility in terms of borrowing. You can draw funds as needed up to your credit limit during the draw period. This makes HELOCs ideal for ongoing expenses or projects with uncertain costs. For example, if you're renovating your home and encounter unexpected expenses, you can easily access additional funds.

Cash-out refinances provide a lump sum upfront. While this can benefit large, one-time expenses, it may not suit you if you're unsure of exactly how much money you'll need. Additionally, you'll start paying interest on the full amount immediately, even if you don't use all the funds right away.

Tax Implications

Both HELOCs and cash-out refinances may offer tax benefits, but it's important to consult with a tax professional for advice tailored to your situation. Generally, interest paid on home equity debt is tax-deductible if the funds are used to buy, build, or substantially improve the home that secures the loan.

Closing Costs and Fees

Closing costs can significantly impact the overall cost of borrowing. Cash-out refinances typically have higher closing costs, often ranging from 2% to 5% of the loan amount. These costs can include appraisal fees, title insurance, and origination fees.

HELOCs usually have lower closing costs. Some lenders even offer HELOCs with no closing costs, though this may come with a higher interest rate or annual fees. It's important to factor in these costs when comparing your options.

Lower upfront costs might seem attractive, but they could lead to higher overall expenses if paired with a higher interest rate. You should always calculate the total cost of borrowing over the life of the loan before making a decision.

Final Thoughts

Choosing between a home equity line of credit vs cash-out refinance impacts your financial future. HELOCs offer flexibility with revolving credit and lower closing costs, ideal for ongoing expenses. Cash-out refinances provide stability with fixed rates and consistent payments, suitable for large, one-time expenses.

Your decision should factor in your current mortgage rate, desired equity access, and long-term financial goals. Consider the total borrowing cost, including closing fees, and evaluate your comfort with variable vs. fixed interest rates. These factors will help you determine the best option for your situation.

We at HELOC360 simplify this complex process and provide tools to make informed decisions. Our platform connects you with lenders that match your financial needs and goals. HELOC360 helps you unlock your home's equity potential, transforming your property's value into new opportunities.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.