Why a HELOC Might Not Be Right for You

Table of Contents

At HELOC360, we believe in providing comprehensive information about home equity lines of credit (HELOCs). While HELOCs can be beneficial for many homeowners, they're not always the best choice for everyone.

In this post, we'll explore some of the potential HELOC cons that you should consider before making a decision. Understanding these drawbacks can help you make a more informed choice about whether a HELOC aligns with your financial goals and circumstances.

Are HELOCs More Expensive Than Fixed-Rate Loans?

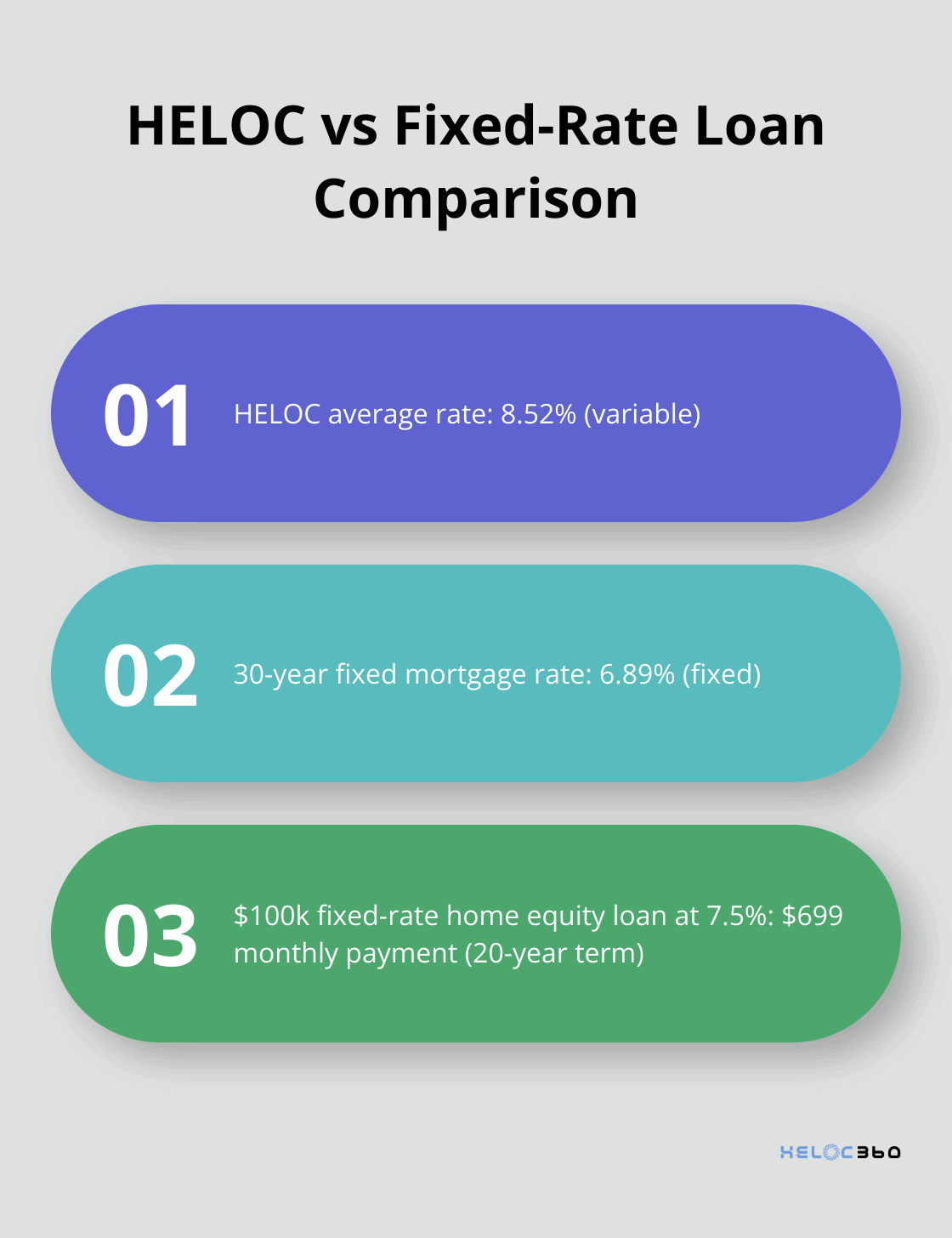

HELOCs typically come with variable interest rates, which can make them more expensive than fixed-rate loans over time. The Federal Reserve Bank of St. Louis reports that as of April 2025, the average HELOC rate stands at 8.52%, while the average 30-year fixed mortgage rate is 6.89%.

The Impact of Rising Rates

Interest rate increases can lead to significant payment hikes for HELOC borrowers. For instance, a $100,000 HELOC balance facing a 2 percentage point rate increase could see monthly interest-only payments jump from $710 to $877 (a $167 increase).

HELOC vs. Fixed-Rate Options

Fixed-rate home equity loans offer more predictable payments. While their initial rates might exceed those of HELOCs, they shield borrowers from future rate increases. A $100,000 fixed-rate home equity loan at 7.5% would maintain a consistent monthly payment of $699 over a 20-year term.

Strategies to Mitigate HELOC Rate Risks

Some lenders provide rate caps or fixed-rate conversion options for HELOCs. These features can help manage interest rate risk but often involve fees or higher initial rates. It's important to compare offers from multiple lenders to secure the best terms.

Considering Long-Term Costs

When evaluating a HELOC, factor in potential rate increases and their impact on your budget. If you value payment stability, a fixed-rate loan might better suit your needs. The lowest initial rate doesn't always translate to the best long-term choice.

As we move forward, let's examine another critical aspect of HELOCs: the potential risk to your most valuable asset - your home.

Can a HELOC Put Your Home at Risk?

The Reality of Home-Secured Loans

A HELOC puts your home at risk if you fail to make payments. This type of loan uses your property as collateral, which means the lender can claim your home if you default.

Understanding the Foreclosure Process

When you default on HELOC payments, the lender may start foreclosure proceedings. The foreclosure process duration varies by state, with Fannie Mae providing specific guidelines for servicers to determine foreclosure time frames.

Financial Fallout of Defaulting

Defaulting on a HELOC doesn't just threaten your home; it wreaks havoc on your finances. Your credit score could plummet, making future borrowing difficult (if not impossible). The lender might also pursue legal action to recover any remaining balance after a foreclosure sale.

Risk Mitigation Strategies

To protect your home, create a solid financial plan before taking out a HELOC. Build a budget that accounts for potential interest rate increases and income changes. The Consumer Financial Protection Bureau suggests maintaining an emergency fund as one of the first steps you can take to start saving and protect yourself financially.

Exploring Safer Alternatives

If the risks associated with a HELOC concern you, consider alternatives like a home equity loan with fixed payments or a cash-out refinance. A cash-out refinance typically incurs closing costs similar to your original mortgage, while a HELOC usually has no or relatively small closing costs.

The decision to use a HELOC requires careful consideration of your financial situation and future plans. While HELOCs offer flexibility, they also come with significant risks. In the next section, we'll explore another potential drawback: the temptation to overspend when you have easy access to a large line of credit.

Is Easy Credit Access a Financial Trap?

The Temptation of Available Funds

HELOCs offer homeowners a tempting financial resource: a large pool of credit tied to their home's equity. While this can benefit planned expenses or emergencies, it also presents a significant risk of overspending and debt accumulation.

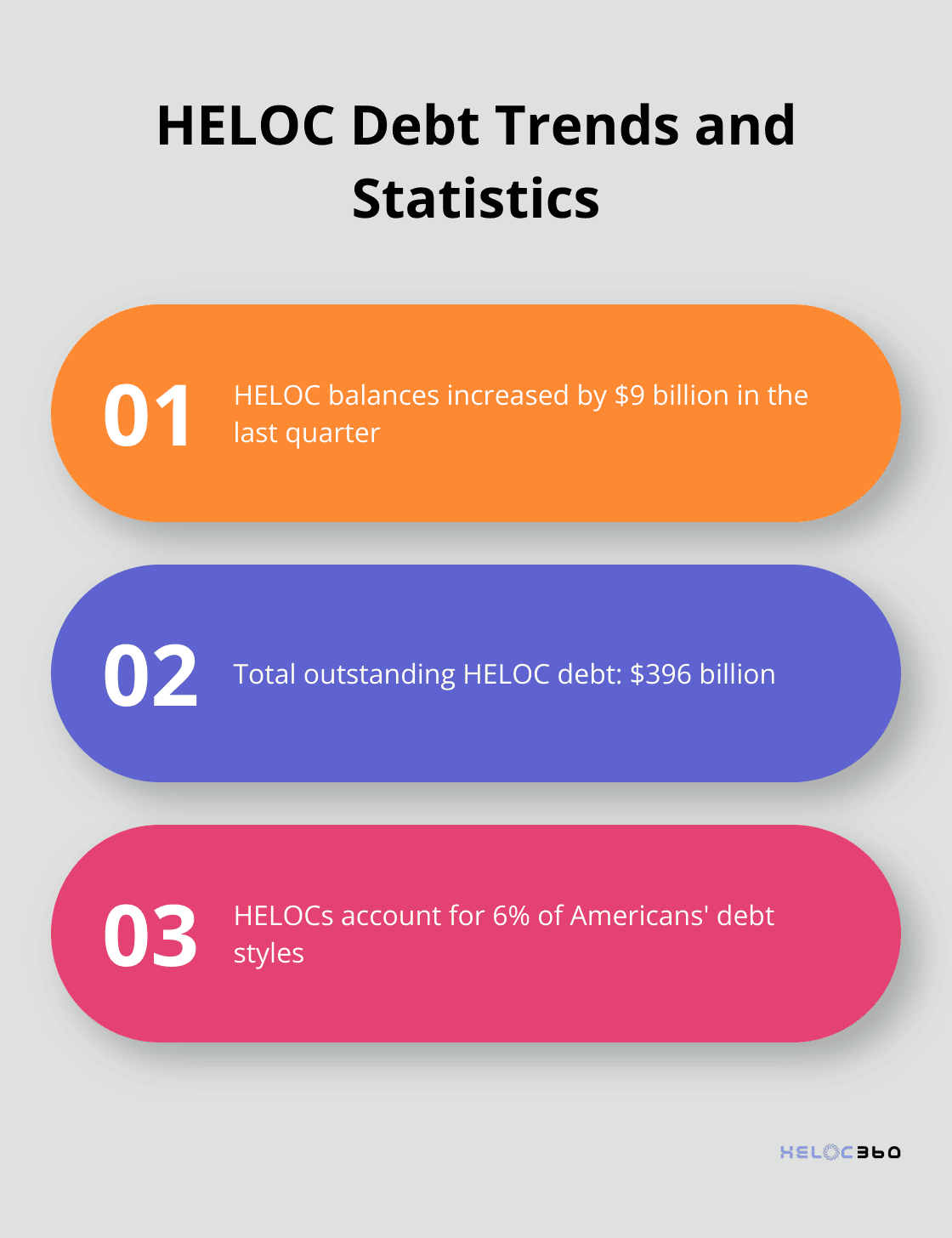

Balances on home equity lines of credit (HELOC) rose by $9 billion, the eleventh consecutive quarterly increase after 2022Q1, and there is now $396 billion in outstanding HELOC debt. This substantial amount can lead homeowners to view their HELOC as an extension of their income, rather than a loan they must repay.

The Risk of Debt Accumulation

A study by the Urban Institute found that HELOCs account for 6 percent of Americans' debt styles. This statistic suggests that many homeowners use HELOCs as part of their financial strategy.

Creating a HELOC Budget

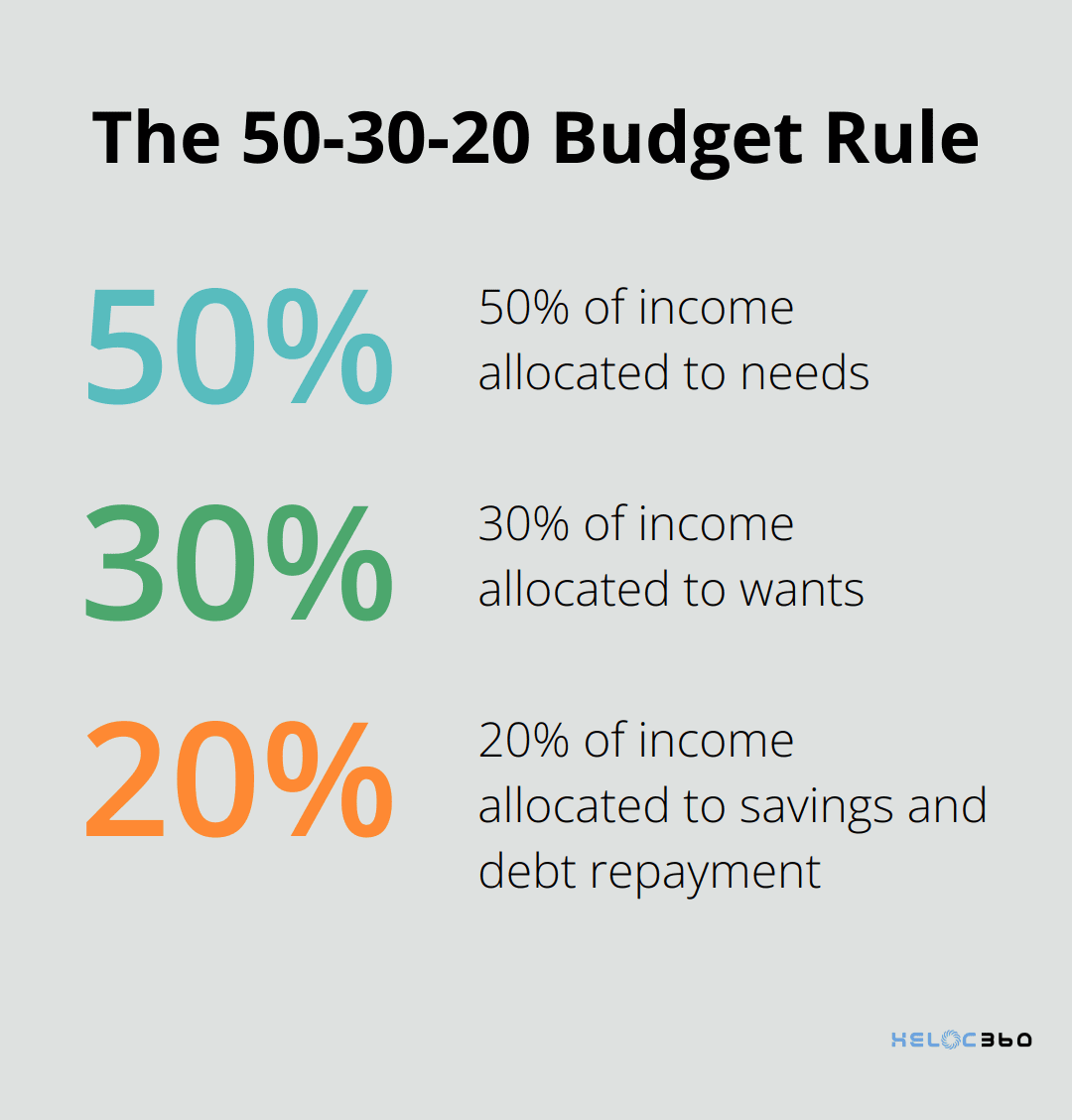

To avoid falling into a debt trap, homeowners must create a strict budget for HELOC funds. The 50-30-20 rule can serve as a useful starting point. This approach allocates 50% of income to needs, 30% to wants, and 20% to savings and debt repayment.

Establishing Clear Spending Guidelines

Financial experts recommend that homeowners establish clear guidelines for HELOC usage before accessing the funds. For example, a homeowner might decide to only use their HELOC for home improvements that increase property value or for consolidating high-interest debt.

Tracking HELOC Activity

Regular review of HELOC statements is essential. Homeowners should set up automatic alerts with their lender to notify them of large withdrawals or when their balance reaches a certain threshold. This proactive approach can help borrowers stay on top of their borrowing and prevent overspending.

Final Thoughts

HELOCs offer homeowners a flexible way to access their home equity, but they come with significant drawbacks. The variable interest rates can lead to higher costs over time, especially in a rising rate environment. This unpredictability can strain budgets and potentially lead to financial stress.

Using your home as collateral puts your most valuable asset at risk if you default on payments. The ease of access to large sums of money can also tempt overspending, potentially leading to a cycle of debt that's difficult to break. These HELOC cons warrant careful consideration before making a decision.

For those still interested in exploring HELOC options, HELOC360 offers a platform to help you navigate the complexities of home equity borrowing. Our expert guidance can help you make an informed decision about whether a HELOC aligns with your financial objectives. You should assess your individual financial situation, long-term goals, and risk tolerance before deciding on a HELOC.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.