Home equity lines of credit (HELOCs) are powerful financial tools that offer unparalleled flexibility. They allow homeowners to tap into their property’s value for various purposes, from home improvements to debt consolidation.

At HELOC360, we’ve seen firsthand how HELOC flexibility can transform our clients’ financial lives. This blog post will explore why HELOCs are the go-to choice for those seeking adaptable financing options.

How a HELOC Works: Unlocking Your Home’s Financial Potential

The Basics of Home Equity Lines of Credit

A Home Equity Line of Credit (HELOC) empowers homeowners to borrow against their property’s equity. This financial tool functions like a credit card, using your home as collateral. Lenders typically approve a maximum credit limit based on your home’s value and outstanding mortgage balance. Many lenders set the credit limit on a home equity line by taking a percentage (say, 75 percent) of the home’s appraised value and subtracting from that the balance owed on the existing mortgage.

Draw and Repayment: The Two Phases of a HELOC

HELOCs operate in two distinct phases:

- Draw Period: This phase lasts 5-10 years. During this time, you can borrow funds as needed and pay interest only on the amount used.

- Repayment Period: After the draw period ends, you enter this phase where you repay both principal and interest.

HELOC vs. Traditional Loans: A Comparison

HELOCs offer revolving credit, unlike traditional loans that provide a lump sum. This feature allows you to borrow, repay, and borrow again within your credit limit during the draw period. While traditional loans often have fixed interest rates, HELOCs typically feature variable rates tied to the prime rate.

Qualifying for a HELOC: Key Factors

Lenders consider three main factors when evaluating HELOC applications:

- Credit Score: A minimum score of 620 is typically required, with the best rates reserved for scores of 740 or higher.

- Debt-to-Income Ratio (DTI): Your DTI should not exceed 43%. This means your monthly debts should remain below 43% of your gross monthly income.

- Home Equity: You need sufficient equity in your home (typically at least 15-20% of your home’s value).

The HELOC Application Process

The HELOC application process involves several steps:

- Gather necessary documents (proof of income, tax returns, etc.)

- Submit your application

- Wait for the lender to review your application and order a home appraisal

- Receive the lender’s decision

- If approved, review and sign the HELOC agreement

Many platforms (such as HELOC360) have streamlined this process, making it easier for homeowners to access their equity. These platforms connect you with lenders that match your specific financial situation, potentially increasing your approval chances.

As you consider the benefits of a HELOC, it’s important to understand how this financial tool can be applied to various aspects of your life. Let’s explore the versatility of HELOCs in financial planning and how they can help you achieve your goals.

How Can You Use a HELOC?

HELOCs offer unparalleled versatility in financial planning, making them a powerful tool for homeowners. Let’s explore some practical applications of HELOCs that can transform your financial landscape.

Funding Home Improvements

One of the most common uses for a HELOC is financing home improvements. In 2023, the average HELOC balance grew 2.7% to $42,139, and more than $20 billion was added to the total HELOC debt across all U.S. consumers. This makes sense, as improvements can increase your home’s value, potentially offsetting the cost of borrowing.

A kitchen remodel costing $30,000 could yield a return on investment of up to 75% (according to Remodeling Magazine’s Cost vs. Value Report). Using a HELOC for such projects allows you to access funds as needed, paying interest only on what you use during the renovation process.

Strategic Debt Consolidation

HELOCs can effectively consolidate high-interest debt. With average credit card interest rates around 20% APR, using a HELOC with a lower interest rate to pay off these balances can lead to significant savings.

For instance, if you have $20,000 in credit card debt at 20% APR, you pay about $4,000 in interest annually. Transferring this debt to a HELOC with an 8% APR could reduce your yearly interest to $1,600, saving $2,400 per year.

Investing in Education or Business

HELOCs provide a flexible funding option for education expenses or starting a business. The U.S. Small Business Administration reports that 10% of small business owners use home equity to fund their ventures.

When using a HELOC for education, consider the potential return on investment. The Bureau of Labor Statistics provides information on earnings and educational requirements for various occupations.

Creating a Financial Safety Net

Establishing an emergency fund is important for financial stability. A HELOC can serve as a backup to your savings, providing quick access to funds in case of unexpected expenses or income loss.

Financial experts often recommend having 3-6 months of living expenses saved. If your monthly expenses are $5,000, try to secure a HELOC limit of at least $15,000-$30,000 to serve as an emergency buffer.

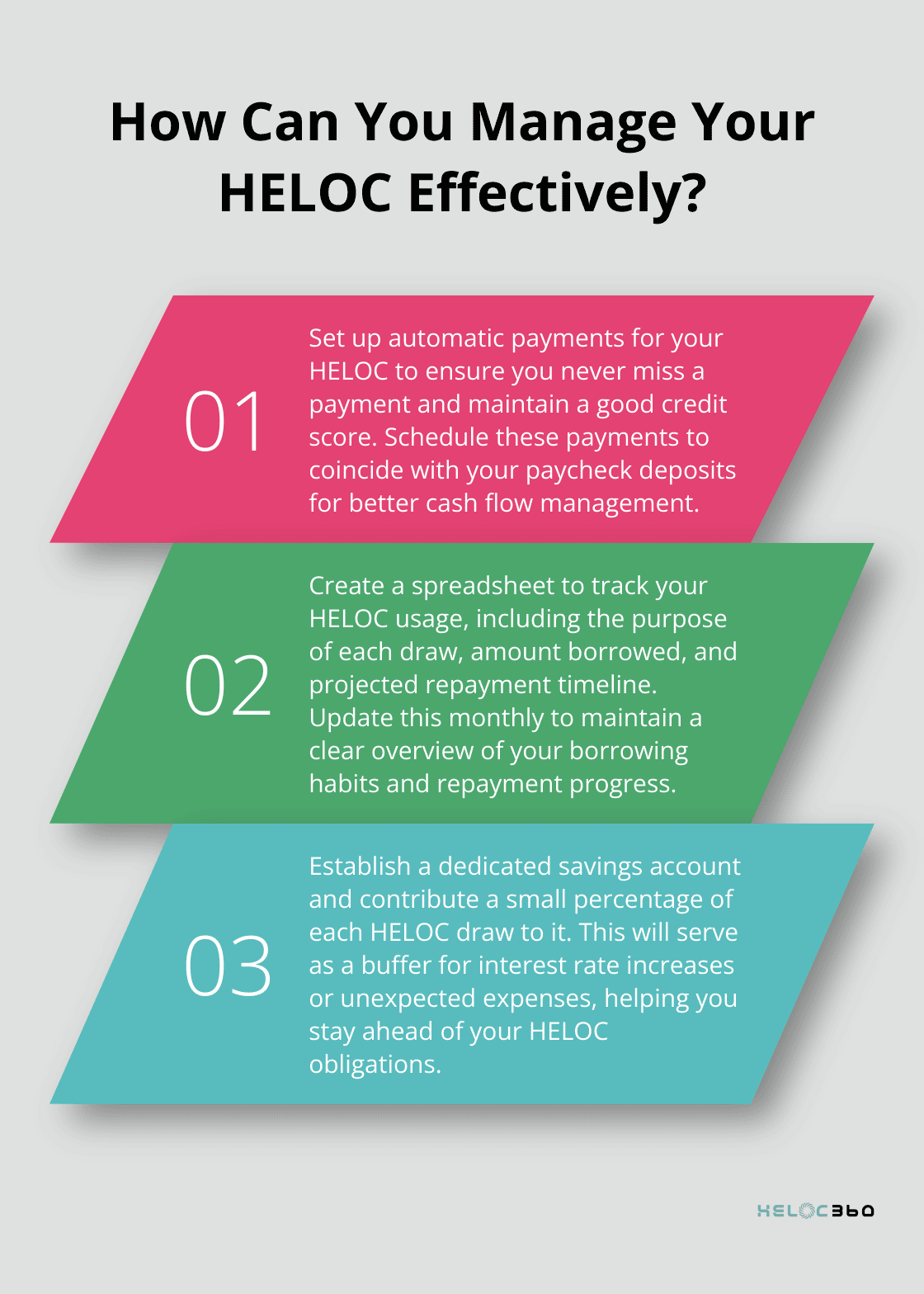

While HELOCs offer great flexibility, they also come with responsibilities. It’s important to have a solid repayment plan and use the funds wisely. The next section will explore the specific advantages of choosing a HELOC over other financing options, helping you make an informed decision about leveraging your home equity.

Why Choose a HELOC Over Other Financing Options?

Lower Interest Rates

HELOCs offer more competitive interest rates compared to other forms of consumer debt. This difference can lead to substantial savings over time.

Tax Advantages for Home Improvements

For tax years before 2018 and after 2025, for home equity loans or lines of credit secured by your main home or second home, interest you pay on the borrowed funds may be deductible, subject to certain dollar limitations, regardless of how you use the loan proceeds. (Always consult with a tax professional to understand how these deductions apply to your specific situation.)

Pay Interest Only on Borrowed Funds

Unlike traditional loans where you receive a lump sum and start paying interest immediately, HELOCs allow you to draw funds as needed. This means you only pay interest on the amount you’ve actually borrowed. If you have a $50,000 HELOC but only use $10,000, you’ll only pay interest on that $10,000. This feature makes HELOCs particularly useful for ongoing projects or as an emergency fund.

Flexible Repayment Options

The repayment structure of a HELOC differs significantly from a personal loan, affecting both short-term affordability and long-term financial planning. A HELOC typically has two phases: the draw period and the repayment period.

Revolving Credit Line

HELOCs provide a revolving credit line, similar to a credit card. This means you can borrow, repay, and borrow again within your credit limit during the draw period. This flexibility allows you to manage your finances more effectively, especially for ongoing expenses or projects with varying costs. (For instance, you could use your HELOC for a home renovation project, paying contractors as work progresses rather than taking out a large lump sum upfront.)

Final Thoughts

HELOCs offer unmatched financial flexibility for homeowners. They provide access to funds for various purposes, from home improvements to debt consolidation, with the ability to borrow as needed and pay interest only on the amount used. HELOC flexibility empowers homeowners to achieve their financial goals while potentially benefiting from tax advantages (consult a tax professional for specifics).

Responsible HELOC borrowing requires a solid repayment plan and wise use of funds. Your home serves as collateral, so it’s important to maximize benefits while minimizing risks. HELOC360 simplifies the process of obtaining a HELOC, connecting you with lenders that match your financial situation.

We at HELOC360 aim to help you navigate home equity borrowing with confidence. Our platform provides expert guidance to ensure you make the most of your property’s value. HELOC flexibility can help you secure a more stable and prosperous financial future, whether you want to renovate your living space, consolidate high-interest debt, or create a financial safety net.

Our advise is based on experience in the mortgage industry and we are dedicated to helping you achieve your goal of owning a home. We may receive compensation from partner banks when you view mortgage rates listed on our website.