Why Prepaying Your HELOC Might Be a Smart Move

Table of Contents

Are you considering HELOC prepayment but unsure if it's the right move? Many homeowners overlook this strategy, missing out on potential financial benefits.

At HELOC360, we've seen how prepaying a Home Equity Line of Credit can lead to significant savings and improved financial health. This post will explore why prepaying your HELOC might be a smart financial decision for you.

What Is HELOC Prepayment?

Understanding the Basics

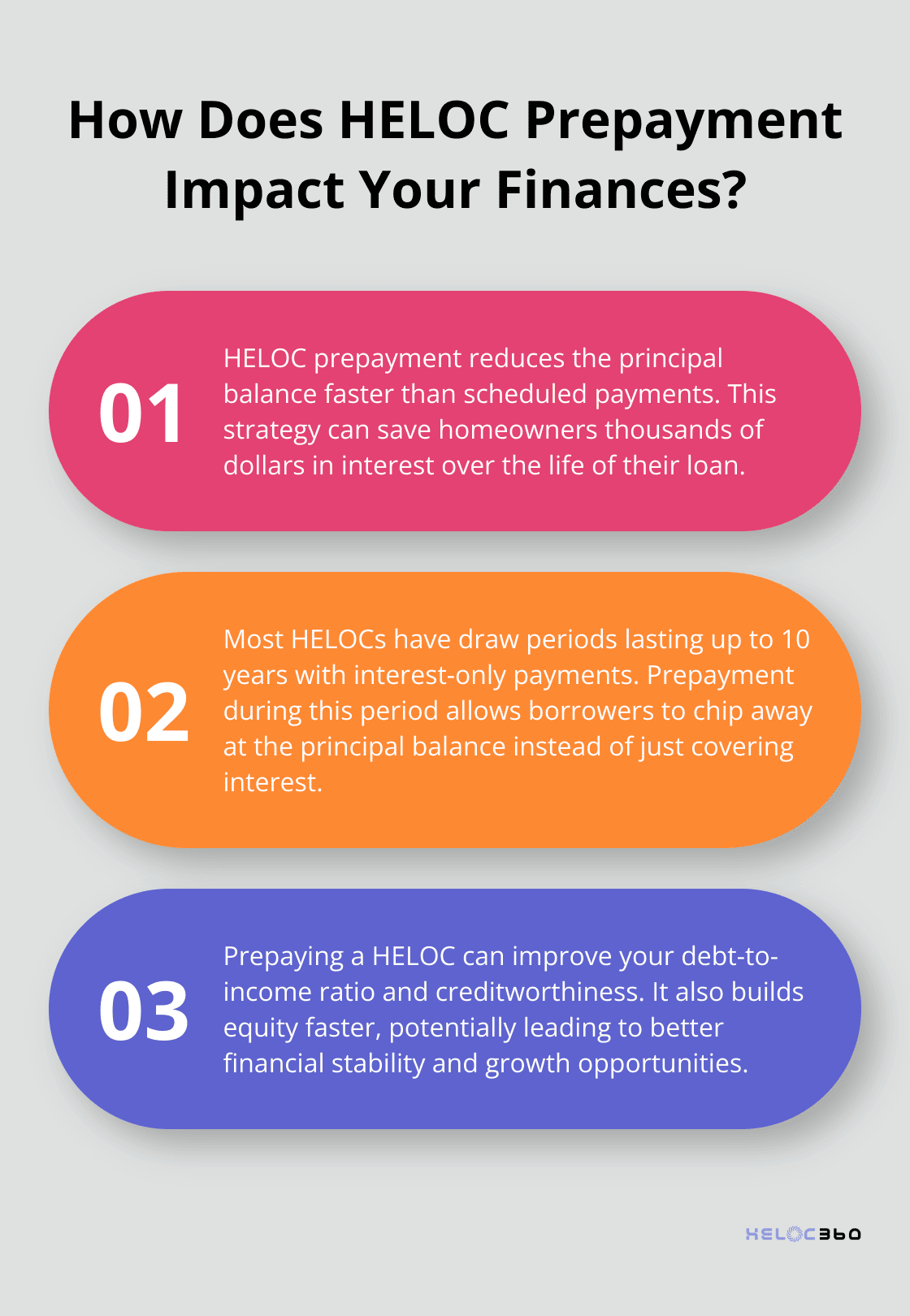

HELOC prepayment is a financial strategy that can save homeowners thousands of dollars in interest over the life of their loan. It involves paying more than the minimum required amount on a Home Equity Line of Credit, which reduces the principal balance faster than scheduled.

The Mechanics of HELOC Prepayment

When you prepay your HELOC, you don't just cover the interest due for that period. You actually chip away at the principal balance. This differs from regular payments, which often only cover the interest during the draw period. Most HELOCs have draw periods lasting up to 10 years, during which borrowers typically make interest-only payments.

Debunking Prepayment Myths

Many homeowners avoid prepaying their HELOC due to common misconceptions. One prevalent myth states that prepayment always incurs penalties. While some lenders charge fees for early payoff, many don't. For example, Alliant Credit Union offers HELOCs without prepayment penalties, allowing borrowers to pay off their balance at any time without extra costs.

The Impact on Your Financial Health

Prepaying your HELOC can significantly improve your financial standing. Loans with higher mortgage rates may default at a higher rate due to either an inability of those borrowers to make the associated payments. This strategy not only saves money but also builds equity faster, potentially improving your debt-to-income ratio and overall creditworthiness.

Leveraging Prepayment for Financial Growth

Homeowners who understand and utilize prepayment strategies often achieve their financial goals more quickly. You can leverage your HELOC as a powerful tool for financial growth and stability by making informed decisions about prepayment.

As we move forward, let's explore the specific financial benefits that HELOC prepayment can offer, including reduced interest costs and accelerated equity building.

How Prepaying Your HELOC Can Boost Your Finances

Slash Interest Costs

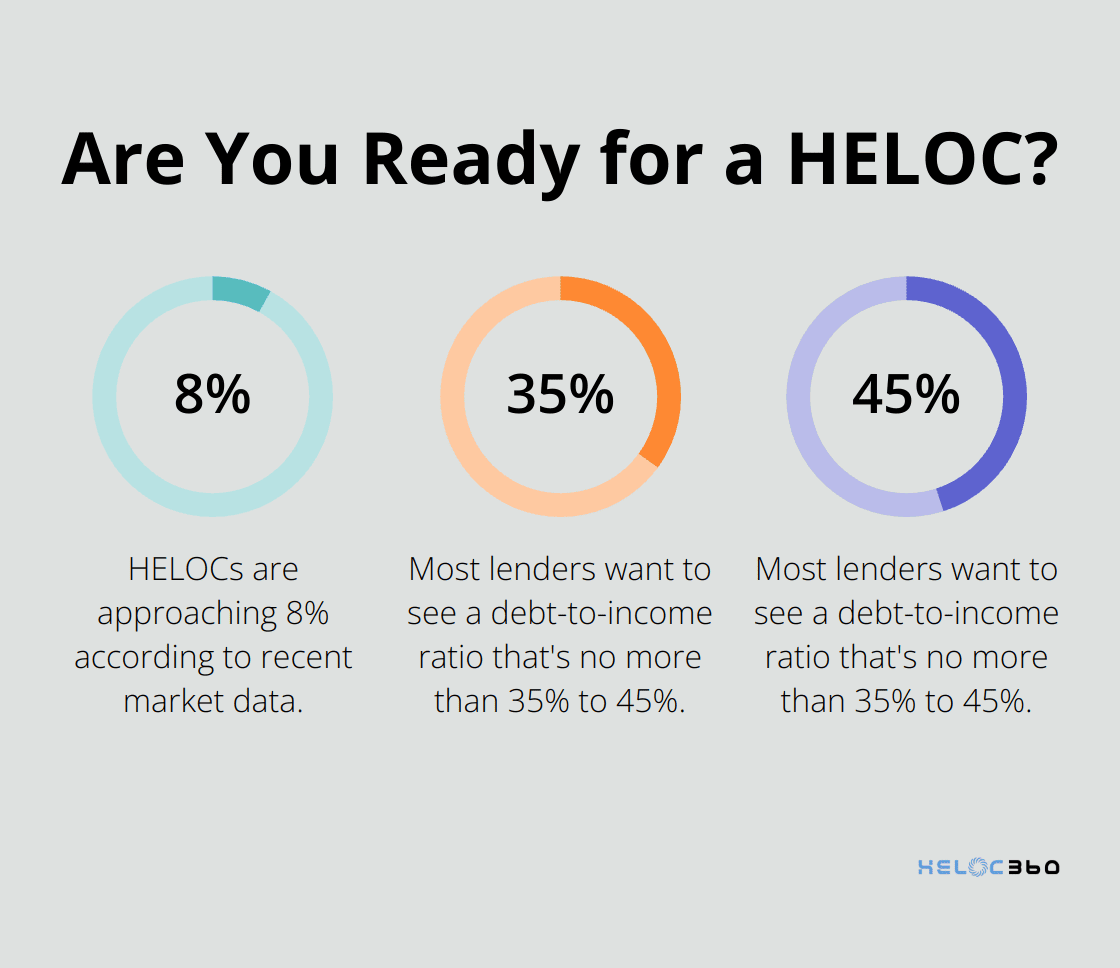

Prepaying your HELOC offers a powerful way to reduce interest expenses. When you make additional payments towards your principal balance, you decrease the amount of interest that accumulates over time. For example, on a $100,000 HELOC with an 8% interest rate, an extra $200 monthly payment could save you over $30,000 in interest over a 20-year term. This strategy proves particularly effective given HELOCs approaching 8% (according to recent market data).

Accelerate Your Debt-Free Timeline

Prepayment doesn't just save you money; it also shortens your loan term. Consistent overpayments can eliminate years from your repayment period. This acceleration means you'll achieve debt freedom sooner, opening up opportunities for other financial goals. For instance, if you have a 10-year repayment term on your HELOC, an additional payment equal to your regular monthly amount each year could potentially reduce your repayment time by two to three years.

Supercharge Your Home Equity

Every extra dollar you pay towards your HELOC principal directly increases your home equity. This rapid equity build-up can transform your financial situation, especially in today's real estate market where homeowners have an average of over $300,000 in home equity. Prepayment doesn't just reduce debt; it actively grows your most valuable asset.

Enhance Your Financial Profile

Prepaying your HELOC can significantly improve your debt-to-income (DTI) ratio, a key metric lenders use to assess creditworthiness. A lower DTI ratio can lead to better terms on future loans and increased financial flexibility. Most lenders want to see a debt-to-income ratio that's no more than 35% to 45%. Reducing your HELOC balance faster takes concrete steps towards achieving this goal.

Maximize Financial Flexibility

Prepayment creates a virtuous cycle of financial improvement. As you reduce your balance, you free up more of your credit line. This increased available credit provides a safety net for unexpected expenses or opportunities. You maintain access to funds while simultaneously improving your financial position (a win-win situation).

The benefits of prepaying your HELOC extend far beyond simple interest savings. This strategy reshapes your entire financial landscape, from accelerated debt repayment to improved creditworthiness. As you consider your options, it's important to evaluate how prepayment aligns with your specific financial goals and circumstances. Let's now explore the scenarios where prepaying your HELOC makes the most sense.

When Prepaying Your HELOC Makes Sense

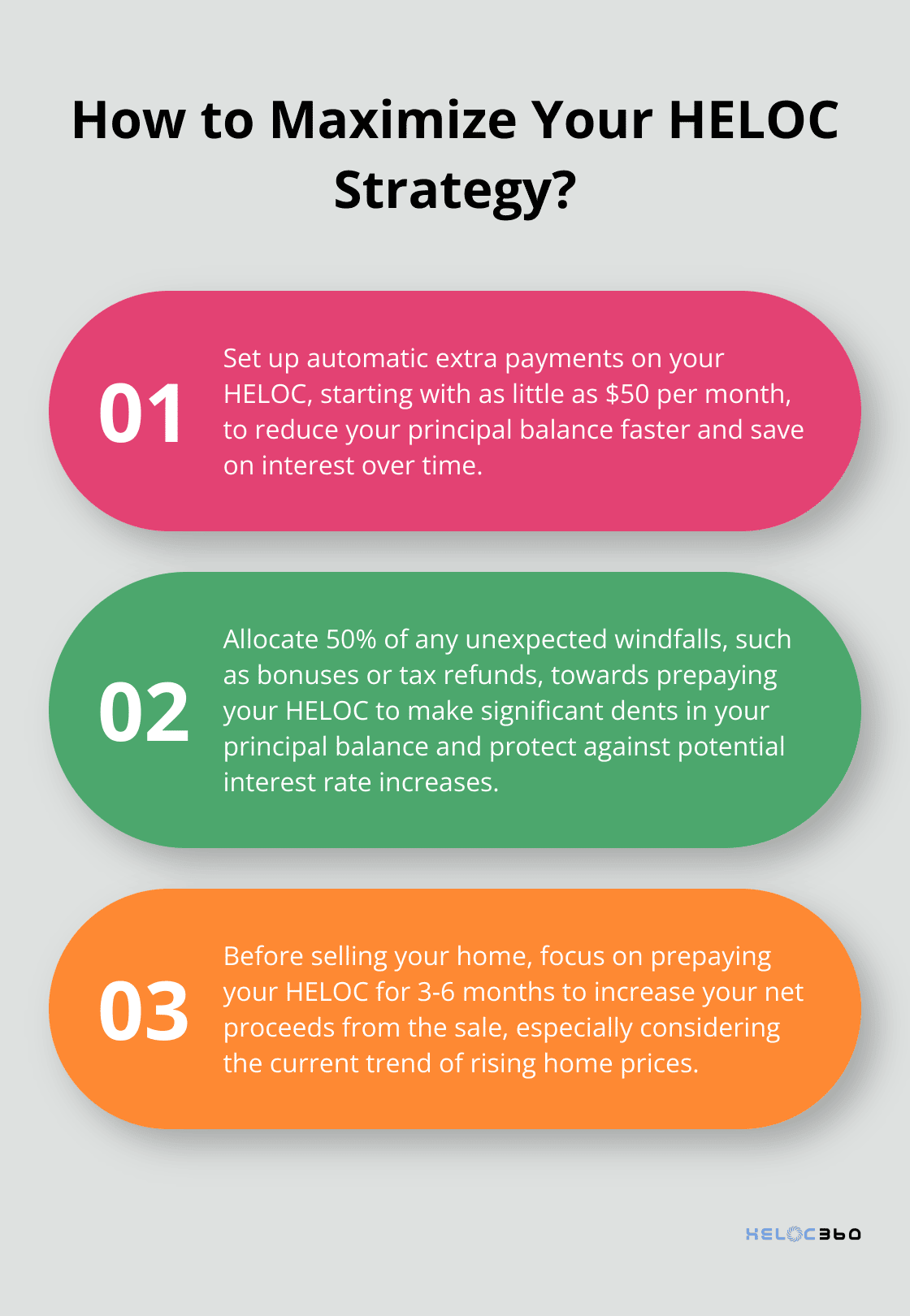

Unexpected Windfalls: A Golden Opportunity

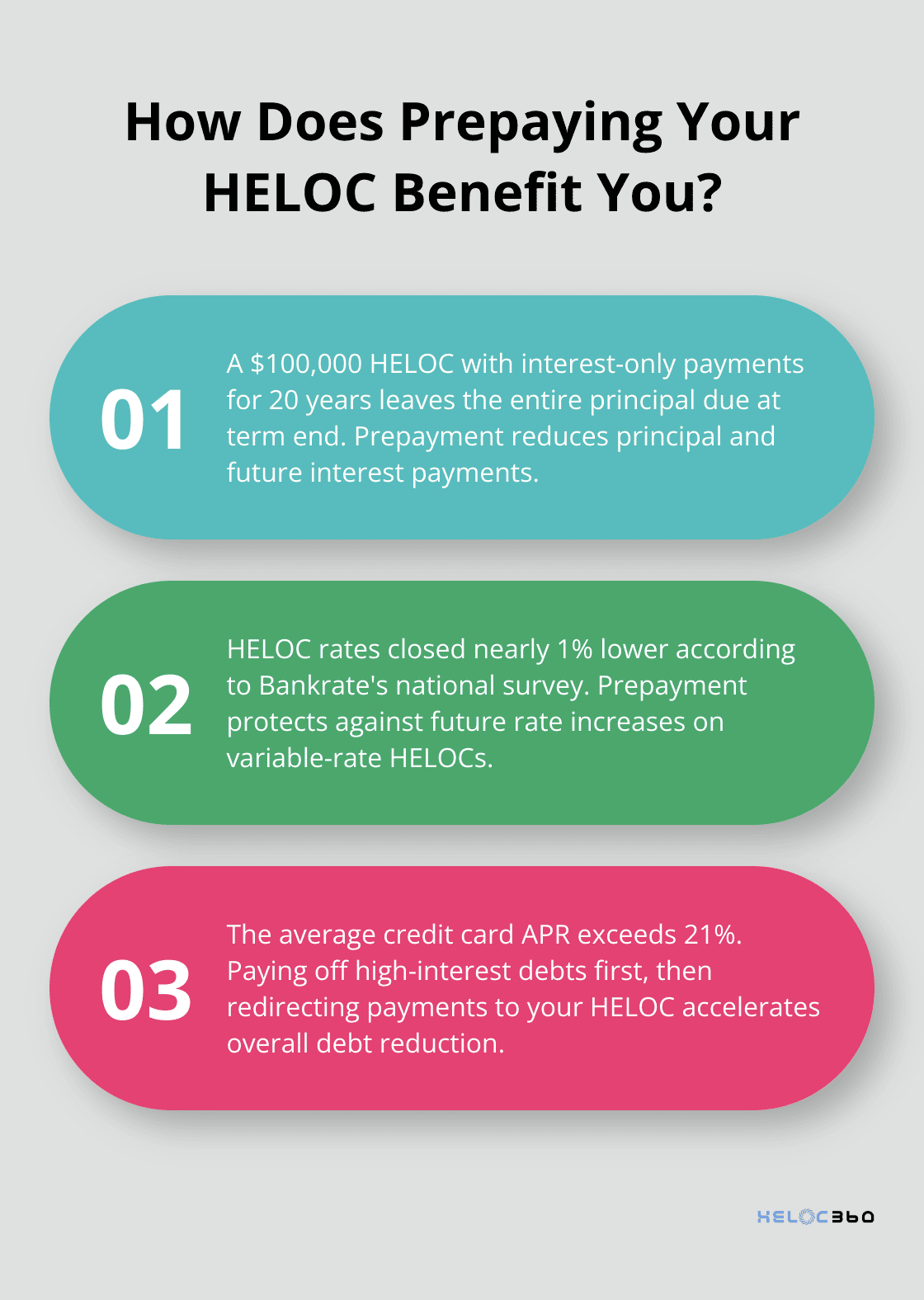

Extra money from bonuses, inheritances, or successful investments presents a perfect chance to prepay your HELOC. This approach can slash your principal balance and future interest payments. A $100,000 HELOC with an interest-only payment for 20 years would still leave you owing the entire $100,000 at the end of the term.

Outpacing Interest Rate Hikes

The Federal Reserve's recent actions have pushed interest rates upward. If you have a variable-rate HELOC, prepayment now can protect you from future rate increases. The average HELOC interest rate closed out the year almost a full percentage point lower, according to Bankrate's national survey of lenders. Reducing your principal balance before rates climb further minimizes the impact on your finances.

Accelerating Your Debt Payoff Strategy

HELOC prepayment can supercharge your broader debt reduction plan. After you pay off high-interest debts like credit cards (which average over 21% APR), redirect those payments to your HELOC. This strategy maintains momentum in your debt payoff journey while cutting interest costs.

Maximizing Proceeds from Home Sales

Prepaying your HELOC becomes a strategic move if you plan to sell your home soon. A reduced HELOC balance increases your net proceeds from the sale. This strategy proves particularly effective in today's market, where home prices have appreciated significantly. The median existing-home sales price rose 3.8% from February 2024 to $398,400, marking the 20th consecutive month of year-over-year price increases.

Balancing Prepayment with Other Financial Goals

While prepayment offers substantial benefits, consider your overall financial picture. Maintain an emergency fund and don't neglect other important financial objectives. If you're unsure about prepayment for your situation, a financial advisor can provide personalized guidance tailored to your unique circumstances.

Final Thoughts

HELOC prepayment offers homeowners a powerful strategy to optimize their home equity. This approach reduces interest costs, shortens loan terms, and accelerates equity building. It improves debt-to-income ratios and provides greater financial flexibility and security.

Your decision to prepay your HELOC should stem from a thorough assessment of your unique financial situation. Consider your current interest rate, future financial goals, and overall debt management strategy. Balance HELOC prepayment with other financial priorities, such as maintaining an emergency fund or investing for retirement.

We at HELOC360 have developed a platform to help homeowners make informed decisions about their HELOCs. Our comprehensive solutions simplify the process, provide expert guidance, and connect you with suitable lenders. HELOC360 empowers you to transform your home's value into a gateway for new financial opportunities.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.