Best Home Equity Line of Credit Lenders: A Comparison

Table of Contents

Choosing the right home equity line of credit (HELOC) lender can be overwhelming. With numerous options available, it's crucial to compare and evaluate the best HELOC lenders to find the perfect fit for your financial needs.

At HELOC360, we've done the legwork to bring you a comprehensive comparison of the top HELOC lenders in the market. This guide will help you navigate through the offerings of major financial institutions and understand the key factors to consider when selecting a HELOC provider.

Understanding Home Equity Lines of Credit (HELOCs)

What Is a HELOC?

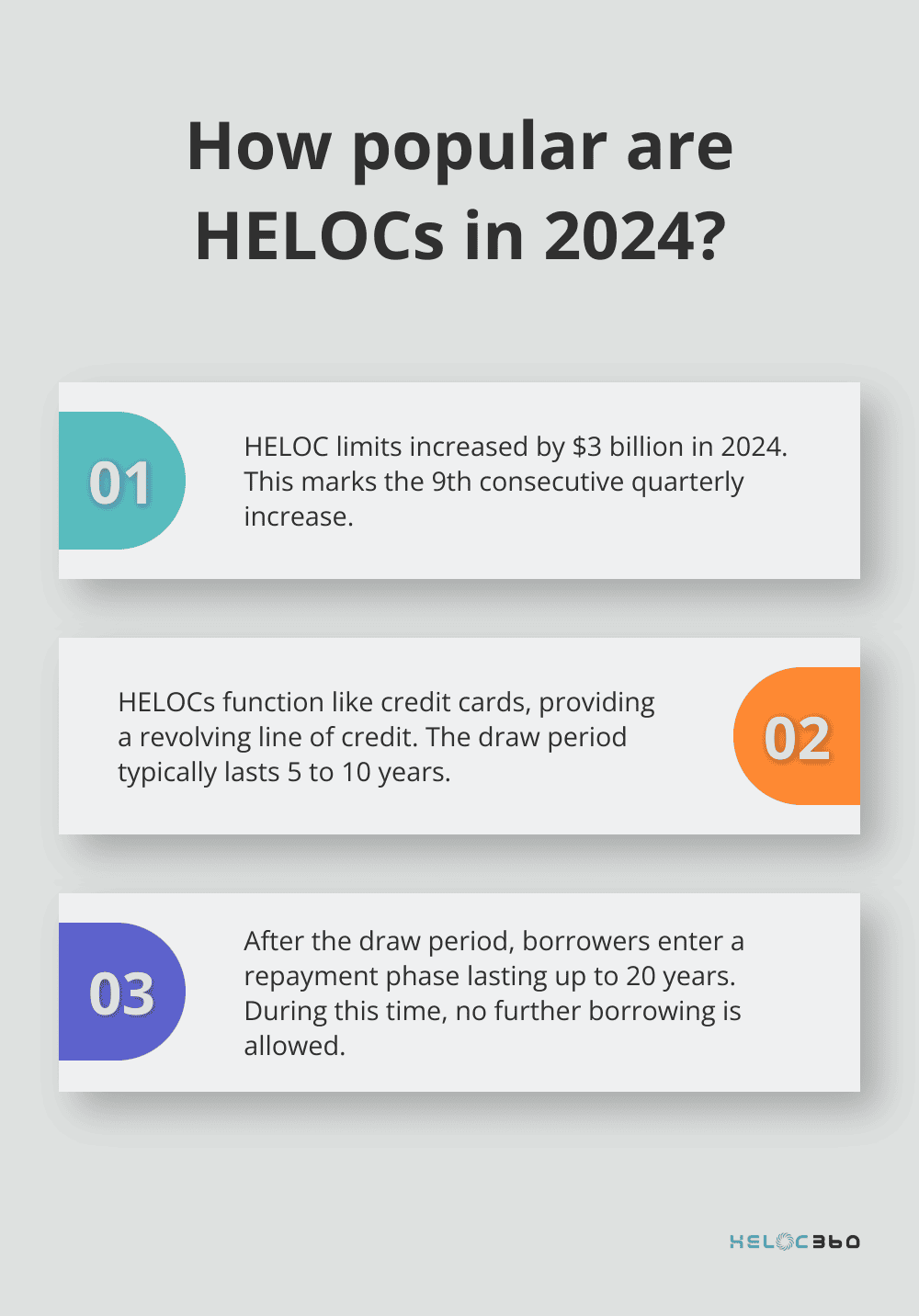

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity they've built in their property. Unlike traditional loans, HELOCs function more like credit cards, providing a revolving line of credit that borrowers can access as needed during a set period (typically 5 to 10 years).

How HELOCs Work

When you open a HELOC, the lender establishes a credit limit based on factors such as your home's value, credit score, and income. You can borrow up to this limit, repay it, and borrow again during the draw period. Interest applies only to the amount you borrow, not the entire credit line.

After the draw period ends, you enter the repayment phase (which can last up to 20 years). During this time, you can no longer borrow from the line of credit and must repay the outstanding balance.

HELOCs vs. Other Home Equity Products

HELOCs differ significantly from home equity loans and cash-out refinances:

- Home equity loans provide a lump sum with fixed payments.

- Cash-out refinances replace your existing mortgage with a new, larger one.

- HELOCs offer more flexibility in borrowing and repayment.

The Federal Reserve reports that as of 2024, limits on home equity lines of credit (HELOC) increased by $3 billion, the 9th consecutive quarterly increase.

Smart Uses for Your HELOC

HELOCs can serve as powerful financial tools when used wisely. Common uses include:

- Home improvements: Renovations can increase your home's value, potentially making the HELOC a smart investment.

- Debt consolidation: With typically lower interest rates than credit cards, HELOCs can effectively consolidate high-interest debt.

- Education expenses: Paying for college or other educational pursuits can strategically use home equity.

- Emergency fund: A HELOC can serve as a backup for unexpected expenses (offering peace of mind).

- Business funding: Entrepreneurs often use HELOCs to finance startups or expand existing businesses.

The Importance of Responsible HELOC Use

It's important to use HELOCs responsibly. Your home is on the line, so defaulting on payments could put your property at risk. Always consider your long-term financial goals and ability to repay before tapping into your home equity.

As we move forward to explore the top HELOC lenders and their offerings, keep these fundamentals in mind. Understanding the basics of HELOCs will help you make informed decisions when comparing different lenders and their products.

Top HELOC Lenders and Their Offerings in 2025

Bank of America: Competitive Rates and Flexible Terms

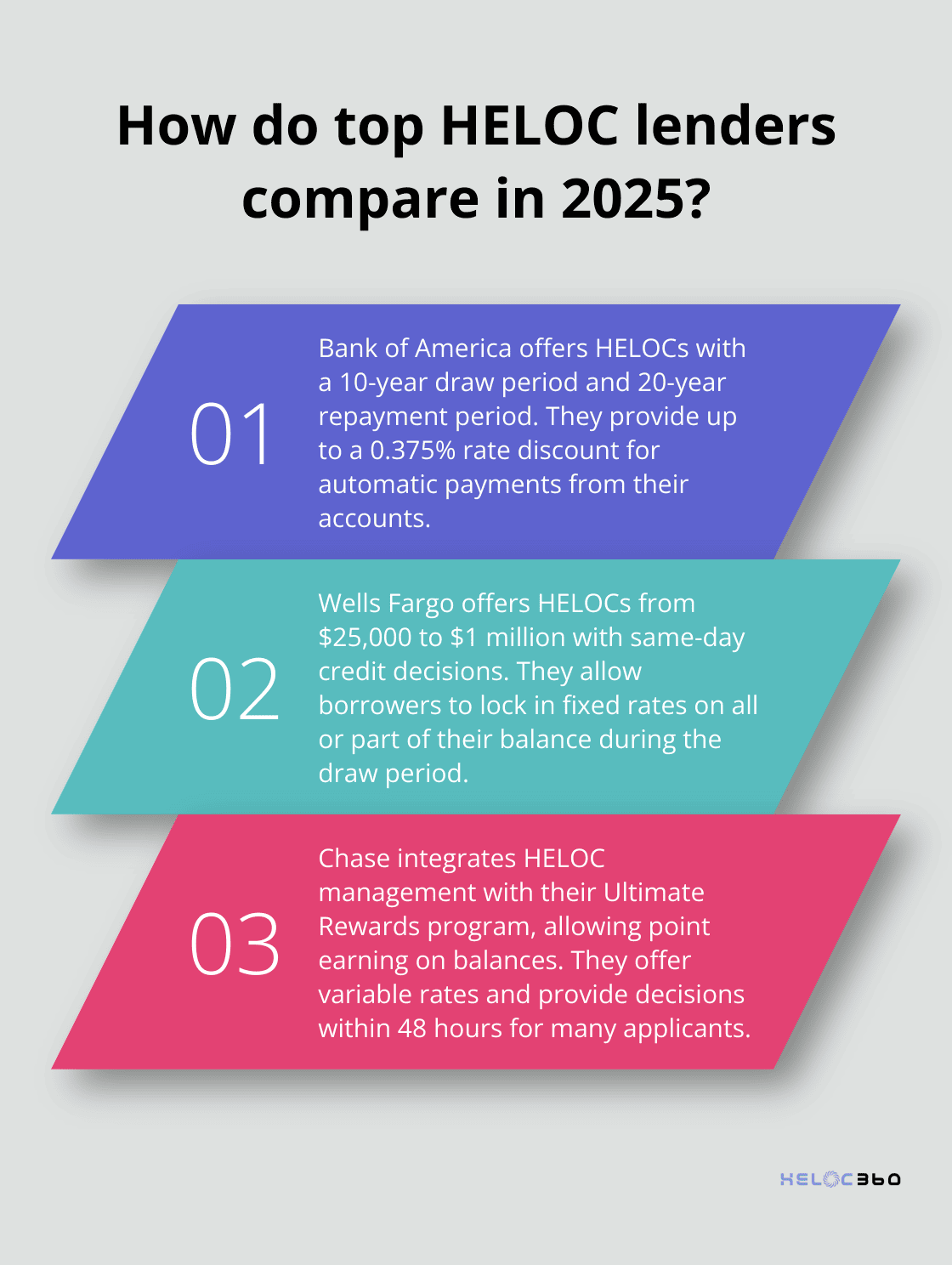

Bank of America offers a home equity line of credit (HELOC) that provides the flexibility to use your funds over time. Their HELOCs include a 10-year draw period and a 20-year repayment period, which allows ample time for fund access and balance repayment.

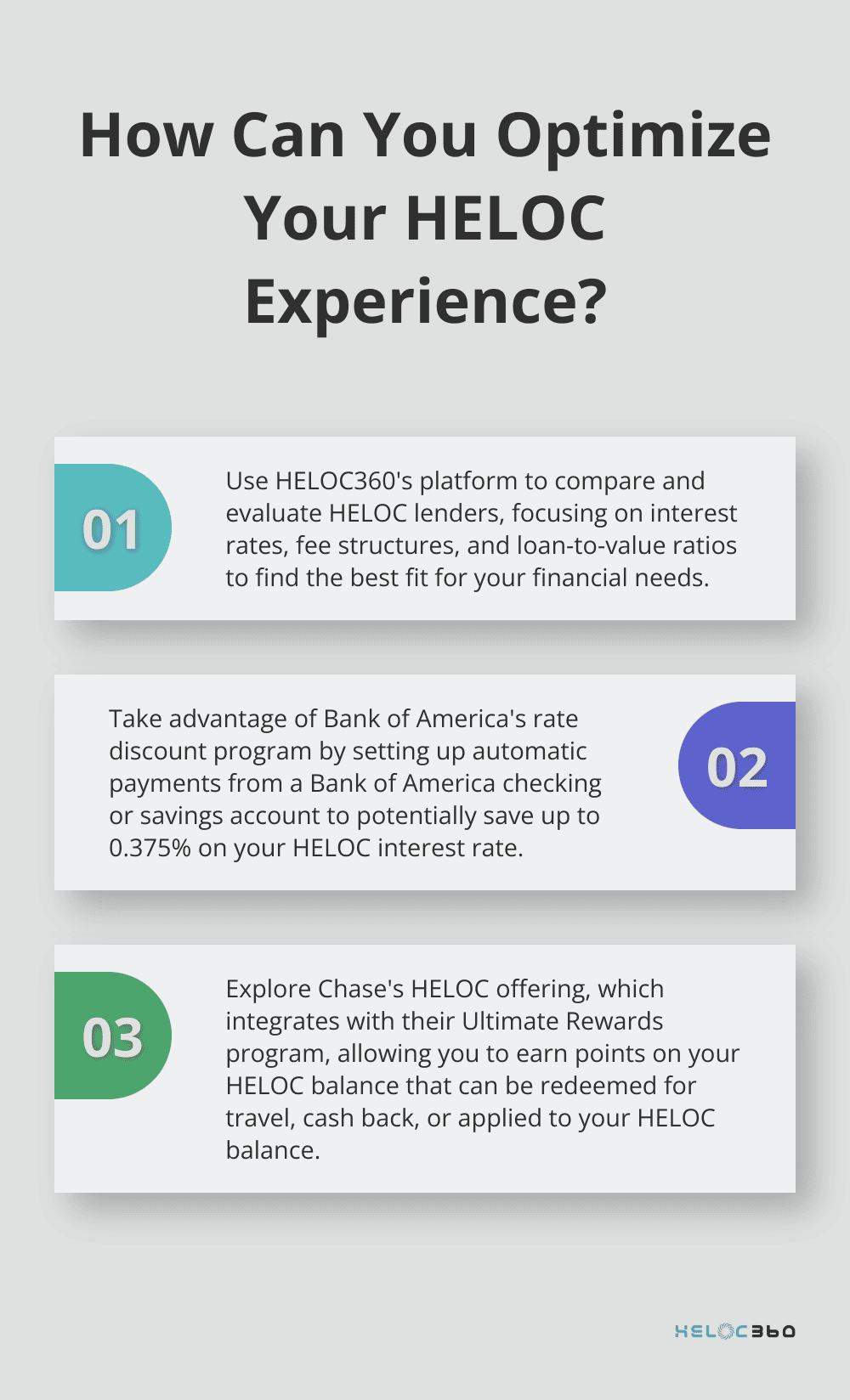

A standout feature is their rate discount program. Customers receive up to a 0.375% rate discount for setting up automatic payments from a Bank of America checking or savings account. This can lead to significant savings over the HELOC's lifetime.

Bank of America also impresses with its online tools, including a home equity calculator and a transparent fee structure. They charge no application fees and offer to pay closing costs for lines up to $1 million.

Wells Fargo: Streamlined Application and Customer Support

Wells Fargo has streamlined its HELOC application process. The whole process can be completed easily, with most customers getting a same-day credit decision.

Their customer service excels, with dedicated home equity specialists available via phone, chat, or in-branch appointments. This support proves particularly valuable for first-time HELOC borrowers navigating the process.

Wells Fargo offers lines of credit from $25,000 to $1 million. They've also introduced a feature allowing borrowers to lock in a fixed rate on all or part of their balance during the draw period, providing flexibility and protection against rising rates.

Chase: Innovative Features and Rewards Integration

Chase positions itself as an innovator in the HELOC space. Their standout feature integrates HELOC management with their popular Chase Ultimate Rewards program. Borrowers earn points on their HELOC balance, which they can redeem for travel, cash back, or apply to their HELOC balance.

Chase offers variable rates for their HELOCs. The exact APR you might qualify for depends on your credit score and other factors, such as whether you're an existing customer or enroll in auto-payments.

Chase's application process is notably quick, with many applicants receiving decisions within 48 hours. They also offer a rate discount for existing Chase customers, depending on their relationship with the bank.

Discover: No-Fee HELOCs and Transparent Pricing

Discover has carved out a niche in the HELOC market with their no-fee policy. As of 2025, they charge no application fees, no origination fees, and no annual fees. This results in significant savings compared to other lenders who may charge upwards of $500 in various fees.

Discover also offers a unique feature called "Rate Lock Plus." This allows borrowers to lock in a fixed rate on all or part of their balance at any time during the draw period, with the added flexibility to unlock and relock rates up to three times.

However, Discover's maximum HELOC amount is $300,000, which may limit homeowners in high-value markets or those seeking to borrow larger amounts.

HELOC360: Tailored Solutions and Expert Guidance

While traditional lenders offer compelling features, HELOC360 stands out as a top choice for homeowners seeking personalized HELOC solutions. The platform simplifies the process and provides expert guidance, connecting you with lenders that fit your unique needs. With HELOC360, you can unlock the full potential of your home equity and achieve your financial goals more efficiently.

As we move forward, it's important to consider various factors when choosing a HELOC lender. The next section will explore key elements to evaluate, ensuring you make an informed decision that aligns with your financial objectives.

How to Choose the Right HELOC Lender

Interest Rates and Fee Structures

Interest rates play a primary role when you evaluate HELOC lenders. As of February 2025, the average HELOC rate stands at 8.28%, according to Bankrate. However, rates can vary widely between lenders and depend on your credit score, loan-to-value ratio, and other factors.

You should look for lenders offering competitive rates, but don't stop there. Examine the fee structure carefully. Some lenders charge application fees, annual fees, or early closure fees that can add up quickly. For example, U.S. Bank charges no closing costs on their HELOCs (potentially saving you thousands of dollars).

Loan-to-Value Ratios and Borrowing Limits

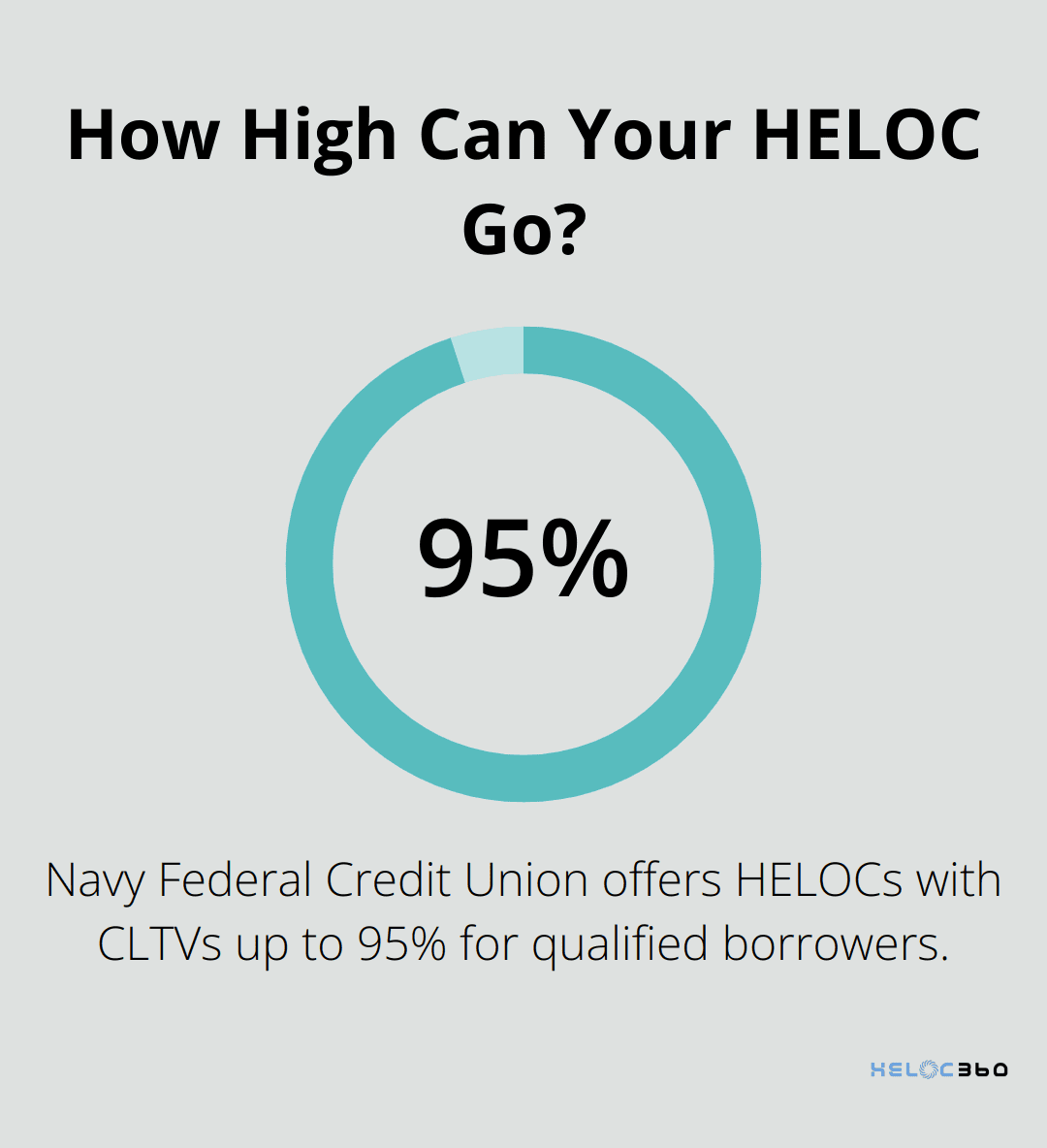

The loan-to-value (LTV) ratio determines how much you can borrow. Most lenders cap the combined loan-to-value ratio (CLTV) at 80-85%. However, some institutions like Navy Federal Credit Union offer HELOCs with CLTVs up to 95% for qualified borrowers.

Consider your home's value and your existing mortgage balance when you evaluate lenders. If you need to borrow a larger amount, look for lenders with higher CLTV limits or larger maximum credit lines. Flagstar Bank, for instance, offers HELOCs up to $1 million (which could benefit homeowners in high-value markets).

Flexibility in Repayment Terms

Repayment flexibility can make a significant difference in how you manage your HELOC effectively. Most HELOCs have a draw period of 5-10 years, followed by a repayment period of up to 20 years. However, some lenders offer more flexible options.

For example, Regions Bank allows borrowers to convert portions of their HELOC balance to fixed-rate loans during the draw period. This feature can provide stability in a rising rate environment. Similarly, some lenders offer interest-only payment options during the draw period, which can lower your monthly payments but may result in higher costs over time.

You should understand these terms fully before you commit to a lender. Try to find lenders offering terms that align with your financial goals and repayment capabilities.

When you evaluate repayment terms, also consider prepayment penalties. Some lenders charge fees if you pay off your HELOC early, which could limit your financial flexibility.

Customer Service and Digital Tools

The quality of a lender's online tools and customer support can greatly enhance your borrowing experience. You should look for lenders that offer robust online account management, mobile apps, and easy-to-use calculators.

For instance, PNC Bank provides a Home Insight Planner tool, helping borrowers navigate their options and understand the impact of a HELOC on their finances. Similarly, Citizens Bank offers a user-friendly online application process and provides personalized rate quotes without affecting your credit score.

Don't underestimate the value of good customer service. Check customer reviews and ratings from sources like J.D. Power's U.S. Home Equity Line of Credit Satisfaction Study. In their 2024 study, Citizens Bank ranked highest in customer satisfaction for home equity products.

While traditional lenders offer compelling features, HELOC360 stands out as a top choice for homeowners seeking personalized HELOC solutions. The platform simplifies the process and provides expert guidance, connecting you with lenders that fit your unique needs.

Final Thoughts

Top HELOC lenders offer unique features tailored to different borrower needs. Bank of America, Wells Fargo, Chase, and Discover stand out with competitive rates, streamlined processes, innovative rewards, and cost-effective policies. The best home equity line of credit lender for you depends on your specific financial situation and goals.

We at HELOC360 simplify the complex process of finding and comparing HELOC options. Our platform connects you with lenders that match your unique requirements (visit HELOC360 for more information). You will make an informed decision and unlock the full potential of your home equity with our comprehensive approach.

A HELOC is a strategic financial instrument that can open doors to new opportunities. You should research, compare, and consult with financial professionals to ensure you make the best choice for your circumstances. You will confidently move forward on your path to financial success with the right HELOC and a clear plan for using your home equity.

Related Articles

Funding College with a HELOC Is It the Right Choice?

Explore if using a HELOC for college tuition is wise. Learn the benefits, risks, and real-world examples in this insightful guide.

When's the Perfect Time to Apply for a HELOC?

Find the ideal HELOC timing. Explore key factors affecting when to apply for a HELOC and secure the best rates for your financial goals now.

What is a Home Equity Line of Credit Loan?

Discover what a home equity line of credit loan is and how it can improve your finances. Get tips for effective HELOC management.