Avoid These Costly HELOC Mistakes at All Costs

Table of Contents

Home Equity Lines of Credit (HELOCs) can be powerful financial tools, but they come with risks.

At HELOC360, we've seen countless homeowners fall into common HELOC traps that can lead to financial stress.

This post will highlight critical HELOC mistakes to avoid, helping you make smarter decisions about your home's equity.

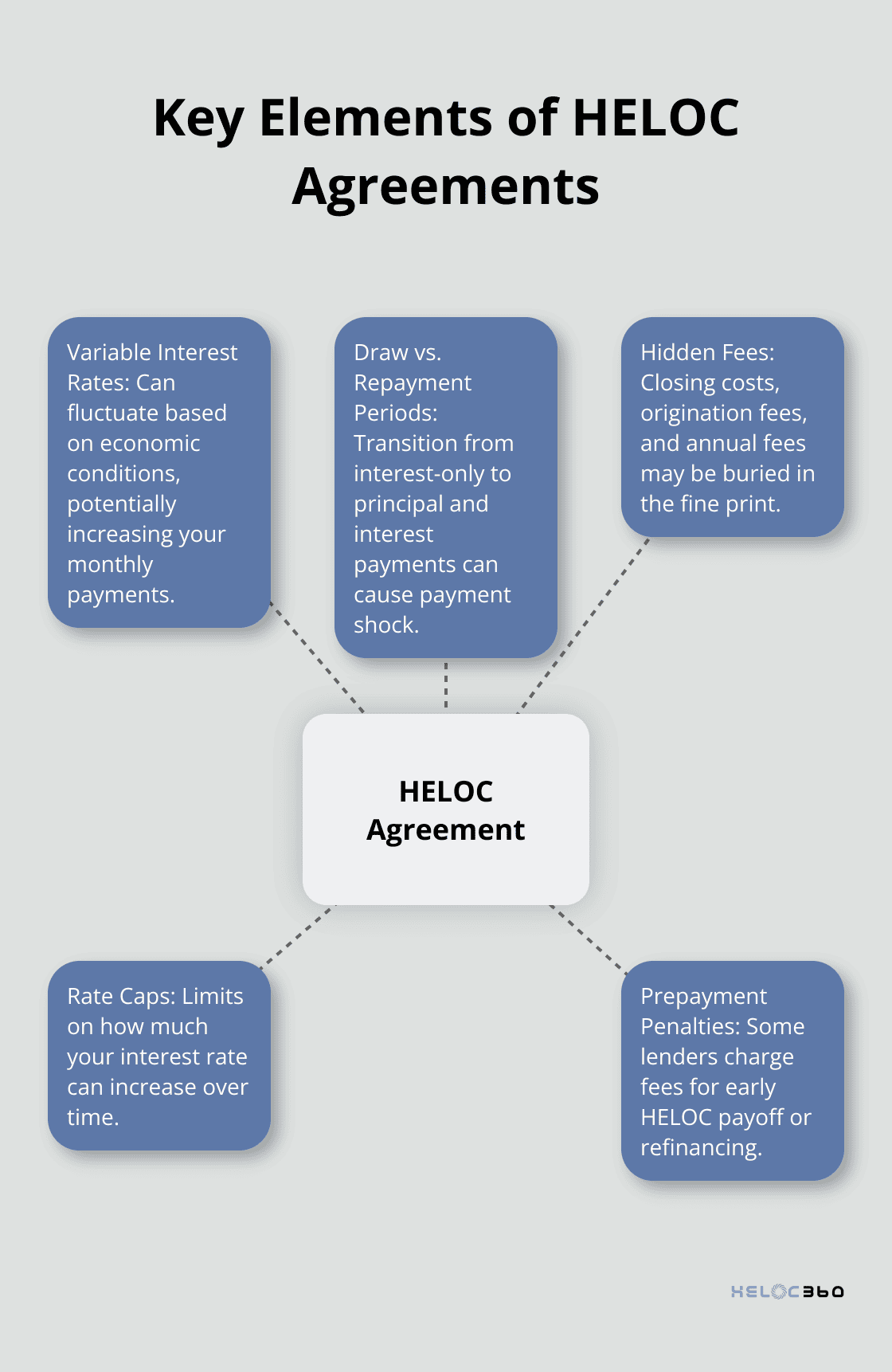

What's Hidden in Your HELOC Agreement?

Home Equity Lines of Credit (HELOCs) often conceal important details in their agreements. Many homeowners sign these contracts without a full understanding, which can lead to expensive surprises later. This chapter breaks down the key elements you must understand before you commit to a HELOC.

The Rollercoaster of Variable Interest Rates

HELOCs typically feature variable interest rates, which can dramatically affect your monthly payments. These rates often link to the prime rate and fed funds rate, which change based on economic conditions. The cost of borrowing can rise or fall, making it important to understand how these changes might impact your payments.

A mere 1% increase in your HELOC rate could result in hundreds of additional dollars in interest payments annually. Always ask your lender about rate caps and frequency of rate changes. Some lenders offer rate conversion options, which allow you to lock in a fixed rate on all or part of your balance.

The Two-Act Play: Draw Period vs. Repayment Period

HELOCs operate in two distinct phases: the draw period and repayment period. The draw period (typically 10 years) allows you to withdraw funds up to your limit. During the repayment period, you can no longer borrow from your HELOC and must repay the borrowed amount.

The real shock arrives when the repayment period begins. You must then pay back both principal and interest, often over a 10-20 year term. This transition can cause payment shock. For instance, a $50,000 HELOC at 7% interest could see monthly payments jump from $292 (interest-only) to $580 (principal and interest) when the repayment period starts.

The Fine Print: Fees and Penalties

Lenders often hide additional costs in the fine print. Many HELOCs come with closing costs, such as origination, recording, and credit report fees. Some lenders charge substantial prepayment penalties if you pay off your HELOC early or refinance.

Always request a complete fee schedule and factor these costs into your decision-making process.

The Importance of Transparency

Transparency should be a top priority when you consider a HELOC. Some platforms prioritize clear communication and help homeowners navigate these complex agreements. They ensure you understand every aspect of your HELOC before you commit.

Knowledge empowers you when it comes to leveraging your home's equity. As you explore HELOC options, don't hesitate to ask questions and seek clarification on any terms or conditions you don't fully understand. Your financial future may depend on it.

Now that you understand the hidden aspects of HELOC agreements, let's explore another common pitfall: the temptation to use your HELOC for non-essential expenses.

Why Your HELOC Isn't a Piggy Bank

The Allure of Easy Money

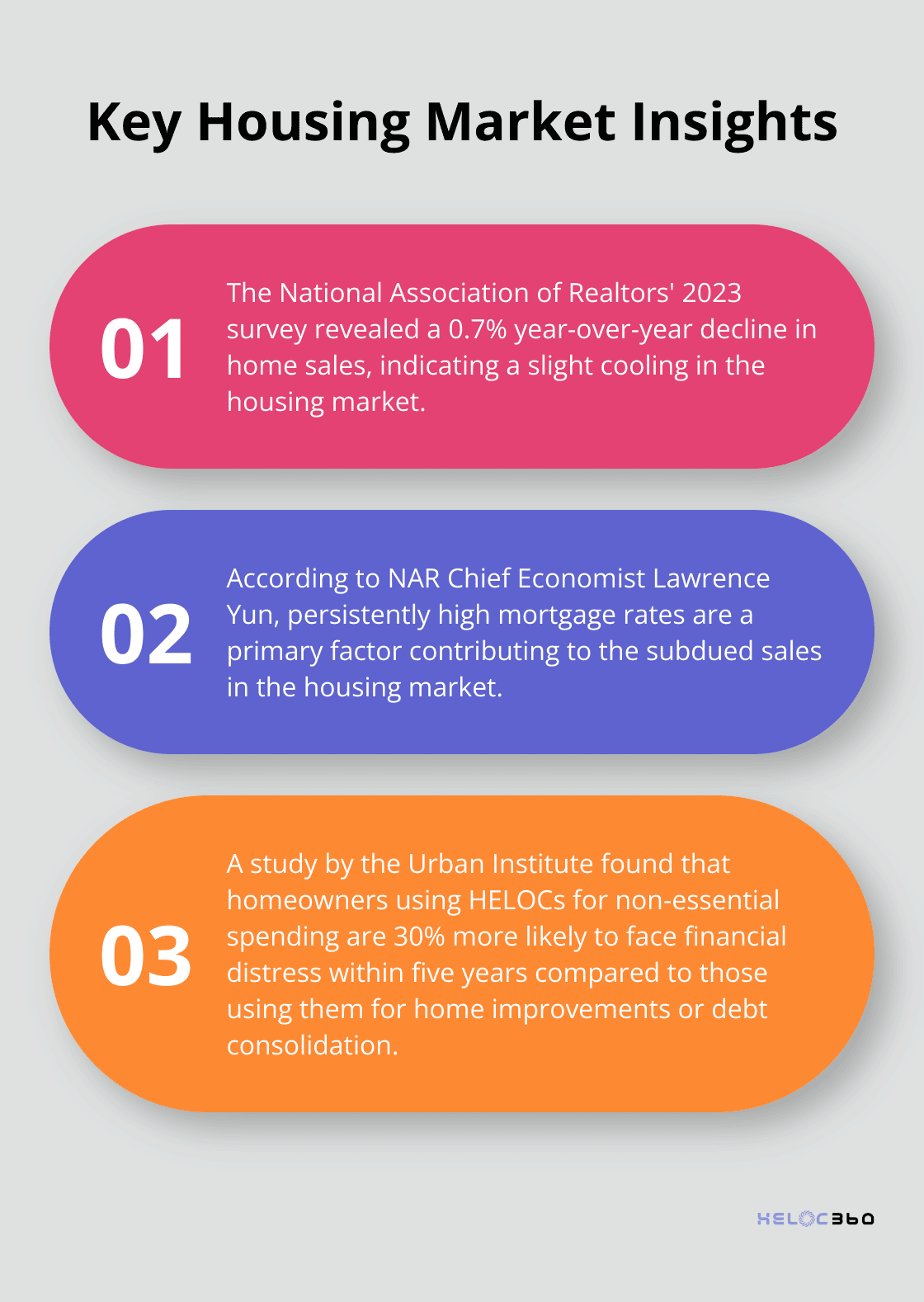

A Home Equity Line of Credit (HELOC) can seem like a financial windfall, but it's not free money. With a HELOC, you're borrowing against the available equity in your home and the house is used as collateral for the line of credit. A 2023 survey by the National Association of Realtors revealed that year-over-year, sales declined 0.7%. According to NAR Chief Economist Lawrence Yun, "The relatively subdued sales are largely due to persistently high mortgage rates."

The True Cost of Short-Term Pleasures

Using your HELOC for a dream vacation or a new sports car might appeal to you, but the long-term costs outweigh the short-term benefits. Let's examine the real impact:

- Interest Accumulation: HELOC interest rates fluctuate. A $20,000 vacation funded by a HELOC at 7% interest could cost you over $30,000 if you pay it back over 10 years.

- Reduced Home Equity: Every dollar you borrow shrinks your home equity. This limits your future financial options and puts you at risk if property values decline.

- Tax Implications: The Tax Cuts and Jobs Act of 2017 eliminated the tax deduction for HELOC interest used for non-home-related expenses. Deducting home equity loan interest can save you money on your tax bill, but you have to understand the rules under the Tax Cuts and Jobs Act (TCJA) of 2017.

Long-Lasting Financial Repercussions

Misusing your HELOC can severely impact your financial health:

- Increased Debt-to-Income Ratio: This makes it harder to qualify for future loans or credit.

- Risk of Foreclosure: If you can't repay your HELOC, you could lose your home.

- Reduced Retirement Savings: Money spent on HELOC payments for non-essentials is money not invested in your future.

A study by the Urban Institute found that homeowners who use HELOCs for non-essential spending are 30% more likely to face financial distress within five years compared to those who use them for home improvements or debt consolidation.

Smart Alternatives to HELOC Misuse

Instead of using your HELOC for non-essentials, consider these options:

- Create a savings plan for big purchases.

- Use rewards credit cards for vacations (but pay them off immediately).

- Look for ways to increase your income rather than borrowing against your home.

Your home equity is a valuable asset. Treat it with respect and use it wisely. (HELOC360 can guide you in making informed decisions about leveraging your home equity responsibly, ensuring you avoid the pitfalls of non-essential spending with your HELOC.)

As we move forward, it's important to understand another significant risk associated with HELOCs: the potential for foreclosure. Let's explore this critical aspect in the next section.

Could Your HELOC Lead to Foreclosure?

The Real Risk of Using Your Home as Collateral

When you take out a Home Equity Line of Credit (HELOC), you put your house on the line-literally. Many homeowners overlook this fact, focusing instead on the immediate benefits of accessing their home's equity. The reality is stark: a HELOC is a type of secured loan, meaning the borrower's home is the collateral.

The Consequences of Missed Payments

Missing HELOC payments isn't just a minor hiccup-it's a direct threat to your homeownership. Failure to make payments could result in the loss of your home through foreclosure. If you default on a HELOC, your home could be foreclosed on, your credit score will drop, and you may forget about future loans.

If you miss payments, your lender can start foreclosure proceedings. This process can begin after just a few missed payments, depending on your lender and state laws. The consequences extend beyond losing your home-foreclosure can ruin your credit score, making it hard to secure future loans or even rent an apartment.

Market Volatility and Negative Equity Risks

The housing market's unpredictability adds another layer of risk to HELOCs. If property values decline, you could end up owing more than your home is worth-a situation known as negative equity or being "underwater" on your mortgage.

A serious dip in home values can cause lenders to lower your credit line or freeze it - preventing you from withdrawing more funds - or even take other actions. This situation can trap homeowners, forcing them to continue paying on a depreciated asset or risk foreclosure.

Strategies to Protect Yourself from HELOC Risks

To safeguard against these risks, consider these strategies:

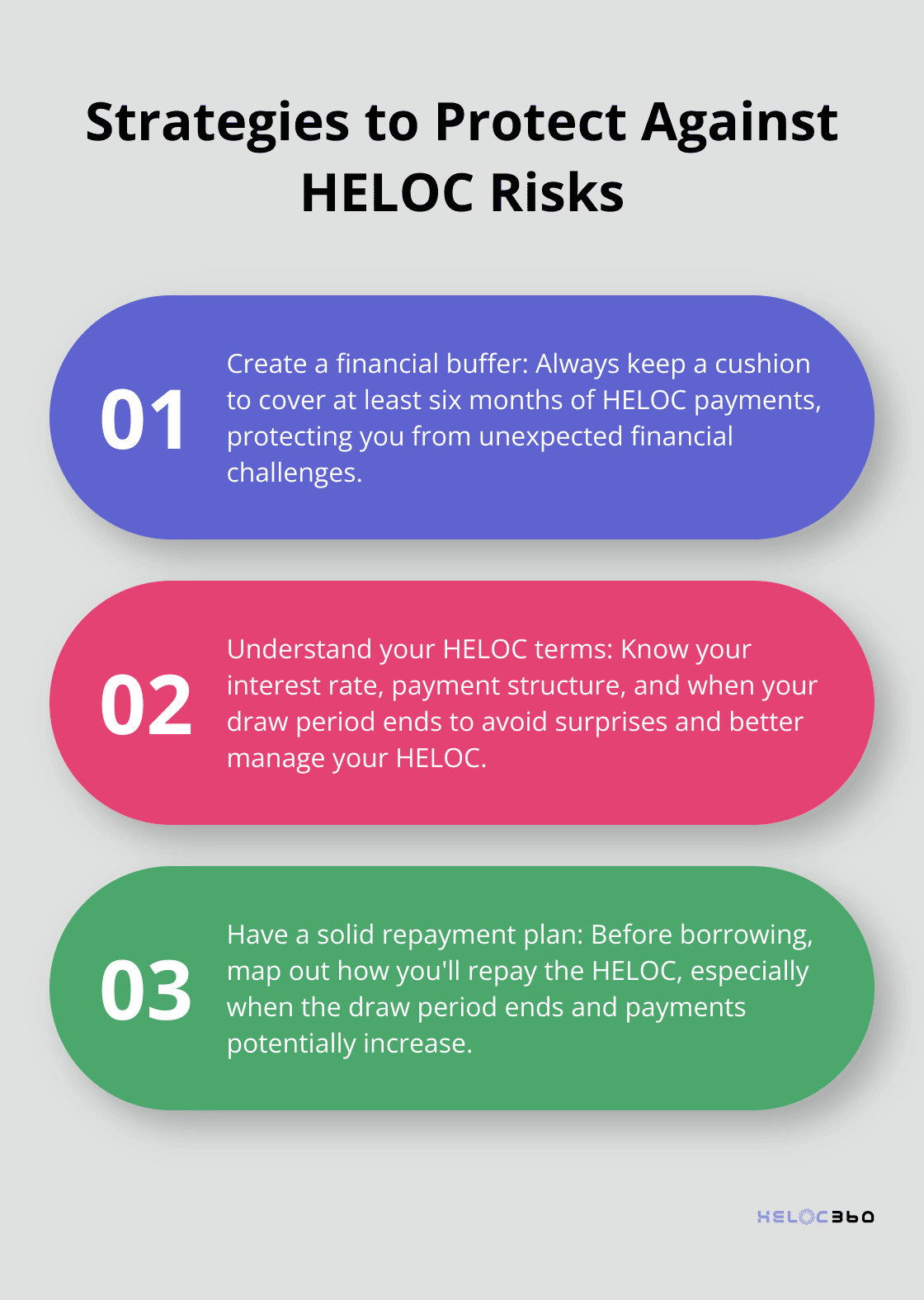

- Create a buffer: Always keep a financial cushion to cover at least six months of HELOC payments.

- Understand your terms: Know your interest rate, payment structure, and when your draw period ends.

- Monitor your home's value: Stay informed about local real estate trends and how they affect your equity.

- Have a repayment plan: Before borrowing, map out how you'll repay the HELOC, especially when the draw period ends and payments potentially increase.

- Consider fixed-rate options: Some lenders offer the ability to convert part or all of your HELOC balance to a fixed-rate loan, providing more payment stability.

While HELOCs can be valuable financial tools, they require careful management to avoid putting your home at risk. (Understanding these risks before taking out a HELOC is essential for protecting your most valuable asset-your home.)

Final Thoughts

Home Equity Lines of Credit (HELOCs) offer homeowners a powerful financial tool, but they come with significant risks that demand careful consideration. We explored several major HELOC mistakes that can lead to financial distress. These include not fully understanding the terms and conditions, using HELOCs for non-essential expenses, and mismanaging payments which can put your home at risk of foreclosure.

Avoiding these pitfalls requires thorough research and meticulous planning. Before taking out a HELOC, you must understand every aspect of the agreement, from interest rates to fees and penalties. You should have a clear purpose for the funds and a solid repayment strategy. It's also vital to stay informed about your home's value and local real estate trends to protect your equity.

Navigating the complexities of HELOCs can challenge even experienced homeowners. HELOC360 helps homeowners make informed decisions about leveraging their home equity. Our platform provides expert guidance and connects you with suitable lenders, potentially helping you avoid common HELOC mistakes and maximize the benefits of your home's equity.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.