Smart Strategies for Maximizing Your HELOC

Table of Contents

Home equity lines of credit (HELOCs) offer homeowners a flexible way to tap into their property's value. However, using this financial tool effectively requires careful planning and smart strategies.

At HELOC360, we've seen firsthand how the right HELOC strategies can transform a homeowner's financial situation. This post will guide you through maximizing your HELOC's potential while avoiding common pitfalls.

What Is a HELOC?

Definition and Basics

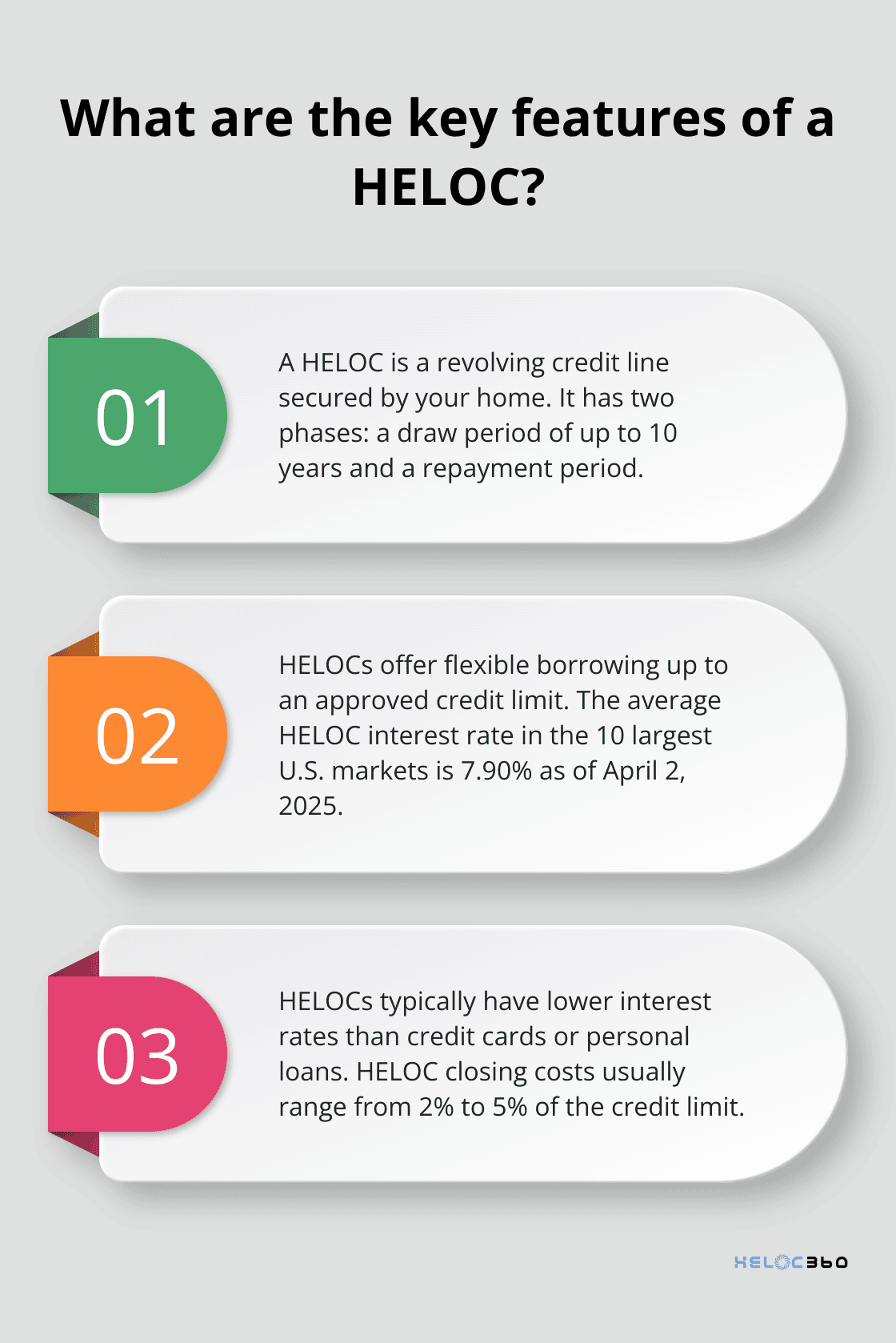

A Home Equity Line of Credit (HELOC) is a revolving form of credit secured by your property. You can borrow as little or as much as you need, up to your approved credit limit. This financial tool provides flexible access to funds for various purposes.

How HELOCs Work

HELOCs operate similarly to credit cards, with your home as collateral. Lenders approve you for a credit limit based on your home's value and outstanding mortgage balance. The HELOC lifecycle consists of two main phases:

- Draw Period (typically up to 10 years): During this time, you're usually only required to pay interest on what you borrow.

- Repayment Period: You pay back both principal and interest.

Key HELOC Features

HELOCs offer remarkable flexibility. You can borrow multiple times up to your credit limit without reapplying. Interest rates usually vary, tied to the prime rate. This means your payments can fluctuate based on market conditions.

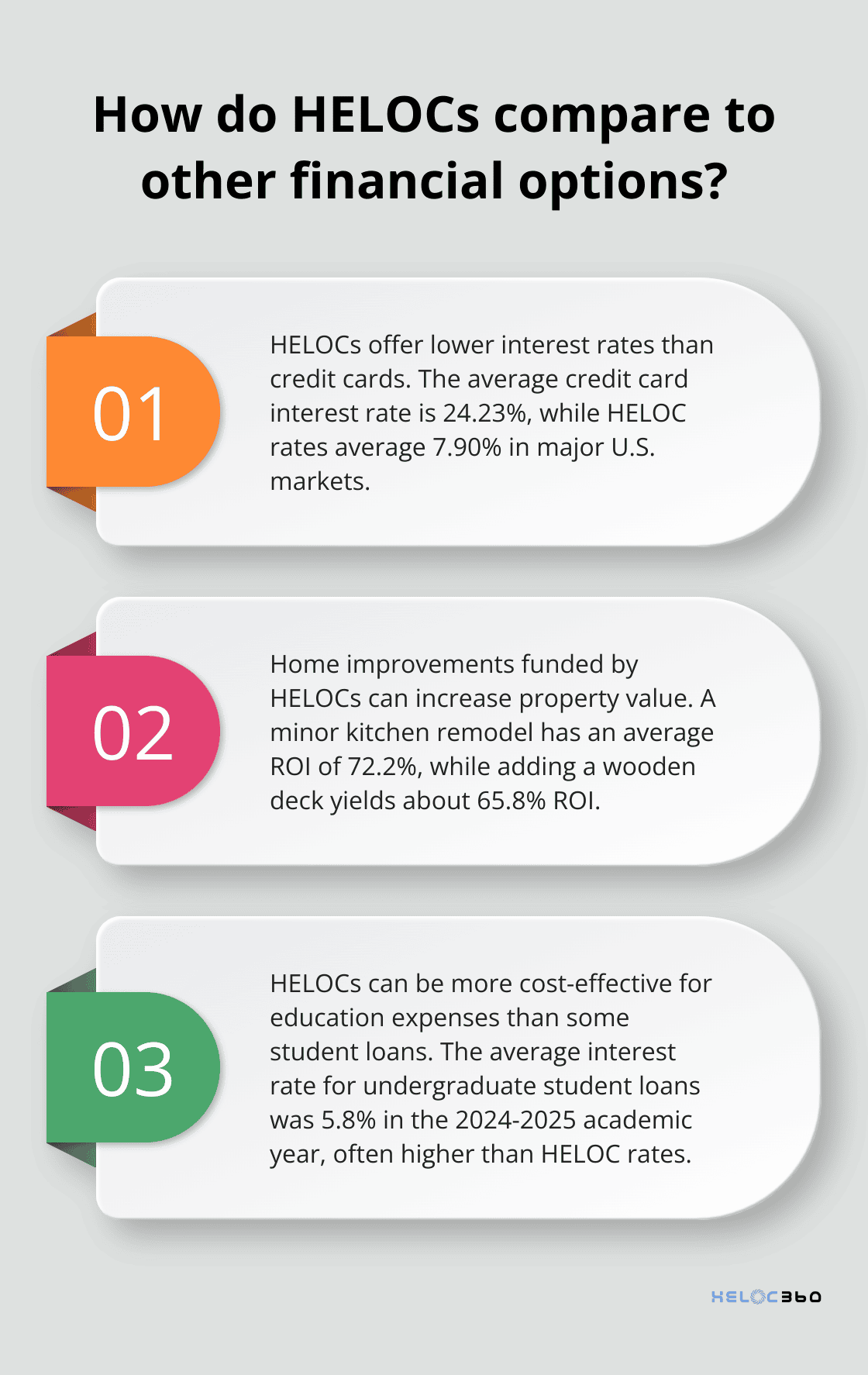

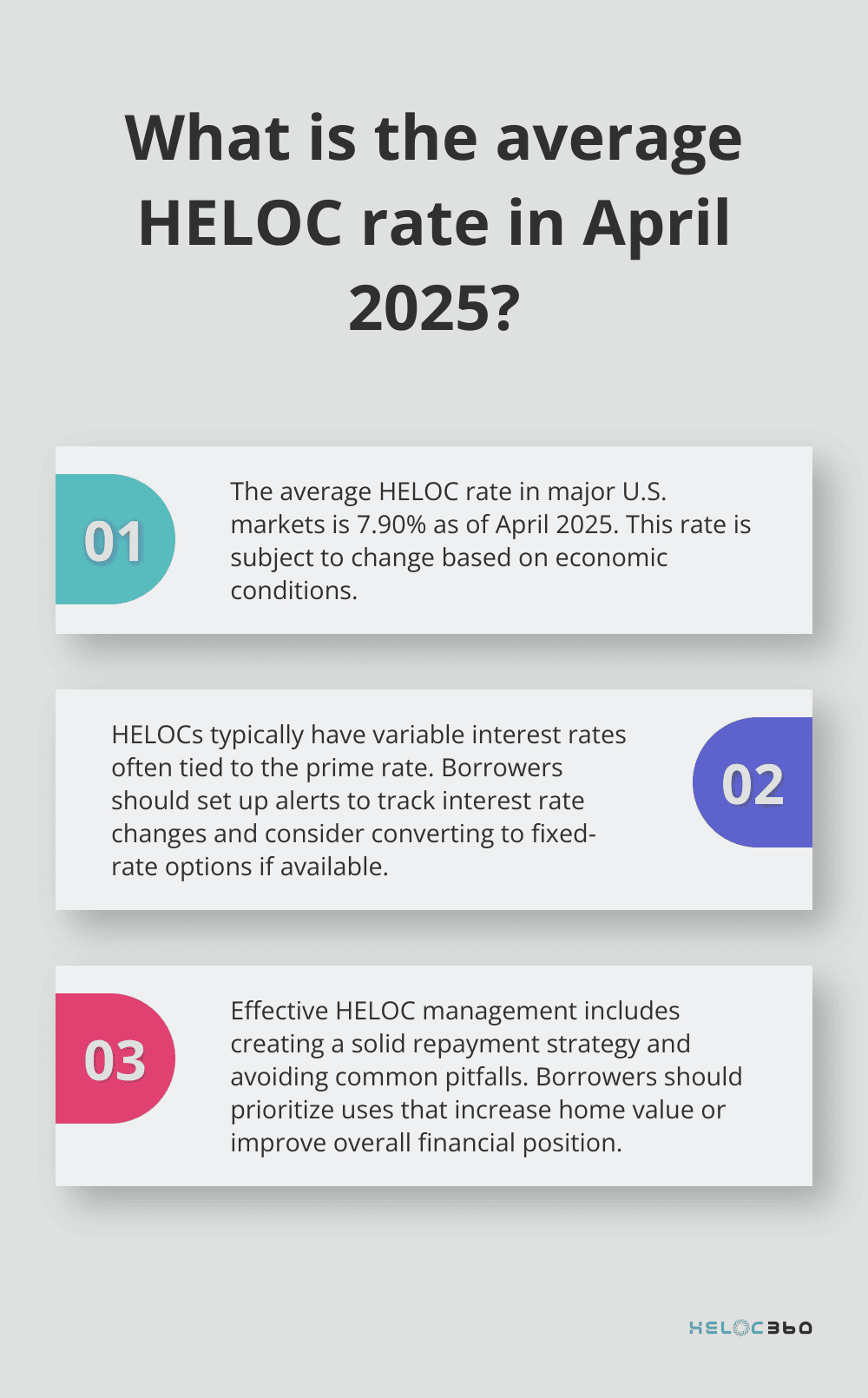

HELOCs often boast lower interest rates compared to credit cards or personal loans. As of April 2, 2025, the current average HELOC interest rate in the 10 largest U.S. markets is 7.90 percent.

HELOCs vs Other Loan Types

Unlike unsecured loans (e.g., personal loans or credit cards), HELOCs use your home as security. This security enables lower interest rates but puts your home at risk if you default on payments.

HELOCs differ from home equity loans, which provide a lump sum. The revolving credit nature of HELOCs makes them ideal for ongoing expenses or projects with uncertain costs.

Compared to cash-out refinancing, HELOCs don't require changes to your existing mortgage terms. This proves particularly beneficial if you already have a low interest rate on your primary mortgage.

HELOCs typically involve lower closing costs than refinancing. While refinancing costs can range from 3% to 6% of the loan amount, HELOC closing costs usually fall between 2% to 5% of the credit limit.

Choosing the Right Option

Understanding these distinctions proves essential when deciding which financial product best suits your needs. Consider factors such as your financial goals, current mortgage terms, and risk tolerance. Consulting with financial experts (like those at HELOC360) can help you navigate these options and make informed decisions that align with your unique situation.

As we move forward, let's explore smart ways to utilize your HELOC effectively and responsibly.

How to Maximize Your Home Equity Line of Credit (HELOC)

Boost Your Home's Value with Strategic Improvements

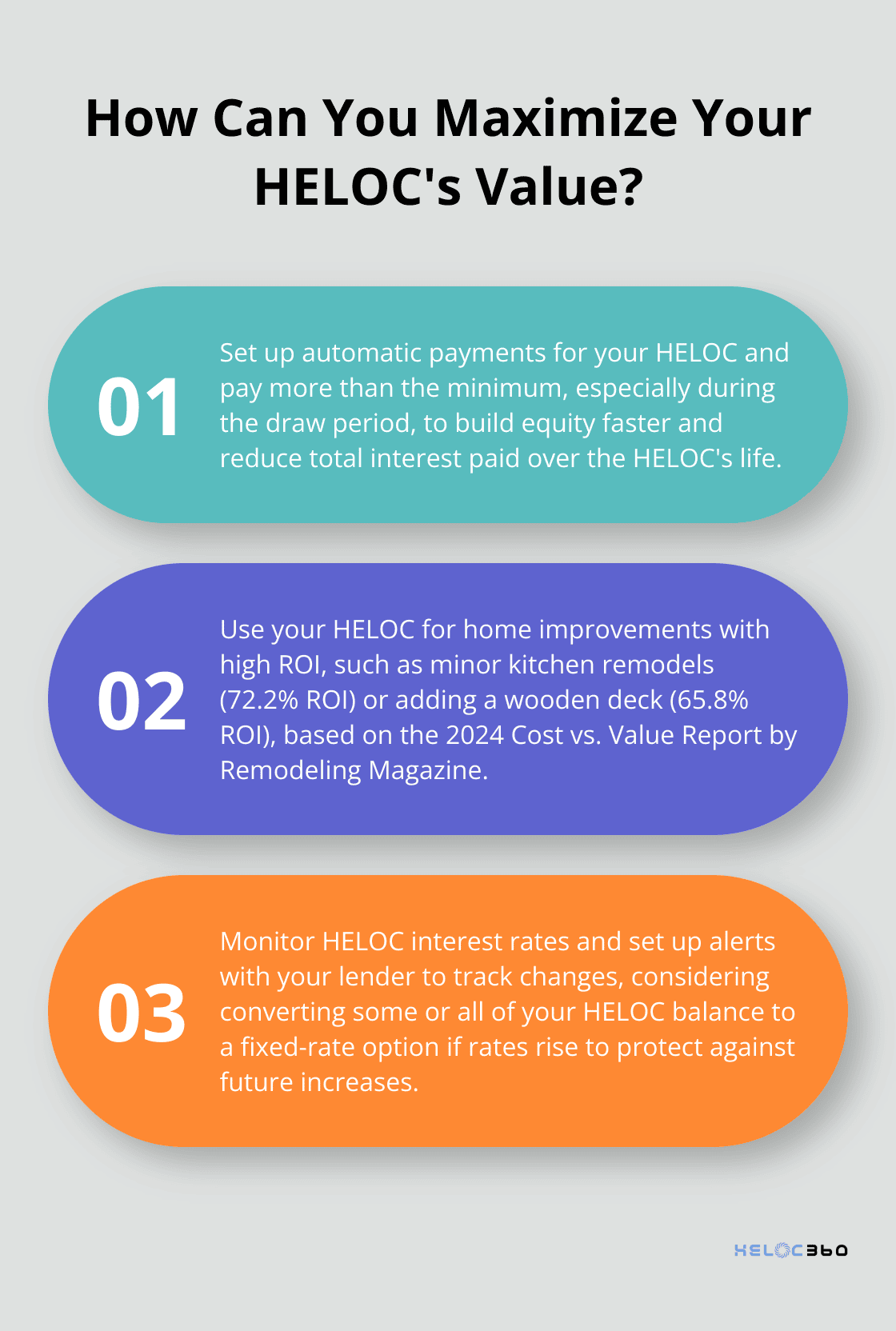

A Home Equity Line of Credit (HELOC) becomes a powerful financial tool when used strategically. One of the most effective ways to use your HELOC involves home improvements that increase your property's value. The 2024 Cost vs. Value Report by Remodeling Magazine highlights certain renovations that offer higher returns on investment (ROI). A minor kitchen remodel, for example, has an average ROI of 72.2%, while adding a wooden deck yields about 65.8% ROI.

You should focus on projects that enhance your home's functionality and appeal. Updating your kitchen with modern appliances, refreshing your bathroom, or improving your home's energy efficiency can significantly boost its value. The goal is to increase your home's worth beyond the cost of the improvements.

Tackle High-Interest Debt

Using your HELOC for debt consolidation can prove a smart financial move, especially if you deal with high-interest credit card debt. As of April 2025, the average credit card interest rate stands at 24.23%, while HELOC rates typically remain much lower (averaging 7.90% in major U.S. markets).

Transferring high-interest debts to your HELOC could potentially save you thousands in interest payments. This strategy, however, requires discipline. You must avoid accumulating new credit card debt after consolidation. Create a solid repayment plan and adhere to it to truly benefit from this approach.

Fund Education Expenses Wisely

HELOCs can offer a cost-effective way to finance education expenses. Unlike student loans (which had an average interest rate of 5.8% for undergraduates in the 2024-2025 academic year), HELOCs often offer lower rates. Plus, you have the flexibility to borrow only what you need, when you need it.

You should weigh this option carefully against federal student loans, which offer benefits like income-driven repayment plans and potential loan forgiveness. A financial advisor can help you compare these options based on your specific situation.

Create a Flexible Emergency Fund

While traditional financial advice suggests keeping 3-6 months of expenses in a savings account, a HELOC can serve as a backup emergency fund. It provides quick access to funds without the opportunity cost of keeping large sums in low-yield savings accounts.

If you face unexpected medical bills or sudden home repairs, your HELOC can provide immediate financial relief. You must repay any withdrawals promptly to maintain your financial health and keep your home equity intact.

These strategies can help you make the most of your HELOC. Responsible use remains key to leveraging this financial tool effectively. The next section will explore how to manage your HELOC responsibly to ensure long-term financial success.

How to Manage Your HELOC Responsibly

Create a Solid Repayment Strategy

Effective HELOC management starts with a robust repayment plan. Understand your HELOC's terms, including draw and repayment periods. While you might only need to make interest payments during the draw period, planning for principal payments can reduce your overall debt significantly.

Set up automatic payments to avoid missing due dates. Pay more than the minimum, especially during the draw period. This approach builds equity faster and reduces total interest paid over the HELOC's life.

If you've used your HELOC for debt consolidation, redirect the money saved from paying off high-interest debts towards your HELOC repayment. This strategy accelerates HELOC payoff without straining your budget.

Monitor Interest Rates and Market Trends

HELOC interest rates typically vary, often tied to the prime rate. As of April 2025, the average HELOC rate is 7.90% in major U.S. markets (subject to change based on economic conditions).

Set up alerts with your lender or use financial apps to track interest rate changes. If rates rise, consider converting some or all of your HELOC balance to a fixed-rate option (if your lender offers this feature). This protects you from future rate increases.

Keep an eye on housing market trends in your area. Rising home values might give you access to more equity. However, if values decline, exercise caution with further borrowing to avoid becoming underwater on your mortgage.

Avoid Common HELOC Pitfalls

A major pitfall involves using your HELOC for non-essential expenses. Resist the temptation to fund luxury vacations or buy new cars. Prioritize uses that increase your home's value or improve your overall financial position.

Another mistake is failing to read and understand all terms of your HELOC agreement. Pay attention to details like prepayment penalties, annual fees, or inactivity fees. These can impact the cost-effectiveness of your HELOC over time.

Avoid continually drawing from your HELOC without a clear repayment plan. This can lead to a debt cycle that becomes difficult to break, potentially putting your home at risk.

Stay Within Your Borrowing Limits

While HELOCs offer flexibility, maintain discipline in your borrowing habits. Set a personal borrowing limit below your approved credit limit. This buffer helps you avoid maxing out your HELOC and provides a safety net for unexpected expenses.

Use budgeting tools to track your HELOC usage. Many banks offer online portals or mobile apps that allow you to monitor your balance and payments easily. Review your HELOC statements regularly to ensure you're staying on track with your financial goals.

Consider setting up alerts with your lender. These can notify you when you're approaching certain thresholds of your credit limit, helping you stay mindful of your borrowing.

If you consistently near your credit limit, reassess your financial situation. Speak with a financial advisor or explore other options to address your financial needs.

Final Thoughts

HELOCs offer homeowners a powerful financial tool when used wisely. Smart HELOC strategies involve careful planning, disciplined borrowing, and proactive management. You can fund value-adding improvements, manage high-interest debt, cover education expenses, or create a flexible emergency fund.

Effective HELOC management requires a solid repayment plan, market trend monitoring, and avoidance of common pitfalls. You must maximize the benefits of your HELOC while minimizing risks (your home serves as collateral, so responsible borrowing is paramount). HELOC360 understands the complexities of home equity management and provides expert guidance to help you navigate the HELOC landscape with confidence.

Our platform connects you with suitable lenders and offers tools to make informed decisions about your home equity. HELOC360 supports your financial journey, whether you're considering a HELOC for the first time or looking to optimize your existing line of credit. We simplify the process, helping you unlock the full potential of your home's value.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.