HELOC for Rental Property A Smart Investment?

Table of Contents

Are you considering using a HELOC for rental property investments? This financing option can be a powerful tool for real estate investors looking to expand their portfolio or improve existing properties.

At HELOC360, we've seen firsthand how HELOCs can fuel smart investment strategies in the rental market. In this post, we'll explore the benefits, risks, and practical applications of using a HELOC for rental properties.

How HELOCs Function for Rental Properties

A Home Equity Line of Credit (HELOC) for rental properties serves as a potent financial instrument that enables real estate investors to access the equity in their investment properties. At its essence, a HELOC operates similarly to a credit card, offering a revolving line of credit that you can use as needed.

The Inner Workings of a Rental Property HELOC

When you submit an application for a HELOC on your rental property, lenders usually permit borrowing up to 75–80% of the property's value, subtracted from any existing mortgage balance. For instance, if your rental property is valued at $300,000 and you have a remaining mortgage of $150,000, you could potentially access up to $75,000 through a HELOC (assuming a 75% loan-to-value ratio).

HELOCs consist of two distinct phases: the draw period and the repayment period. During the draw period, which typically lasts around 10 to 15 years, you can access funds from your credit line as needed. This flexibility proves particularly advantageous for real estate investors who might need to access funds for various projects or purchases over time.

Benefits for Real Estate Investors

Using a HELOC for rental property investments offers several key advantages:

- Quick Capital Access: HELOCs provide rapid access to funds, allowing you to capitalize on investment opportunities as they arise. This speed can prove critical in competitive real estate markets where timing is paramount.

- Lower Interest Rates: HELOCs often feature lower interest rates compared to alternative financing options (such as personal loans or credit cards). This can result in substantial savings over time, especially for larger investments or renovations.

- Potential Tax Benefits: For tax years 2018 through 2025, interest paid on a loan secured by your main home or second home may be deductible, subject to certain limitations. (Always consult with a tax professional for the most current information.)

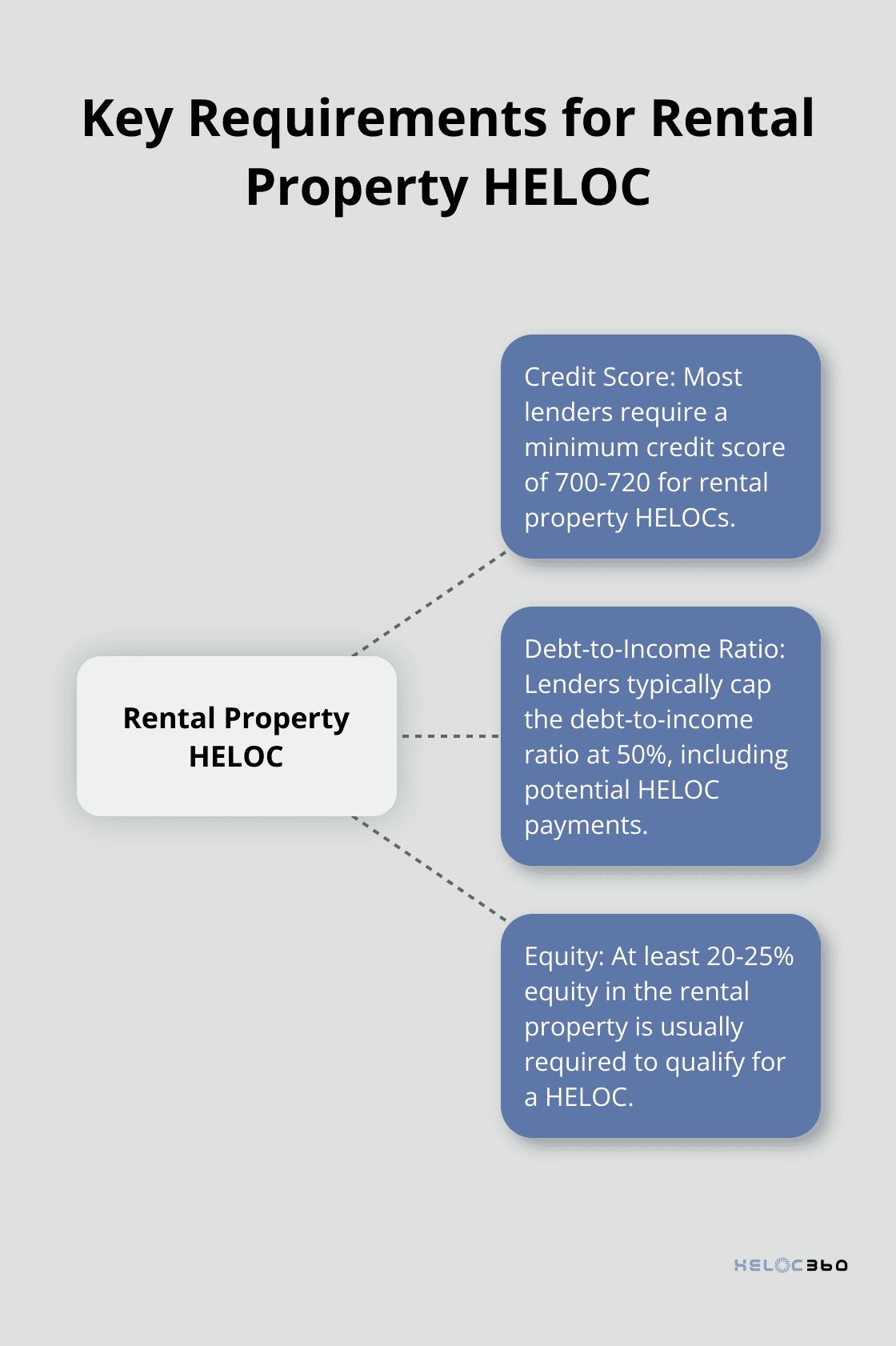

Qualifying for a Rental Property HELOC

Obtaining a HELOC for a rental property typically involves more stringent requirements compared to HELOCs for primary residences. Lenders perceive rental properties as higher risk, thus implementing more rigorous criteria to safeguard their investment.

Most lenders require:

- A minimum credit score of 700–720

- A debt-to-income ratio capped at 50% (including potential HELOC payments)

- At least 20–25% equity in the rental property

Lenders will scrutinize your rental income, so prepare to provide detailed records of your property's financial performance. Successful applicants often demonstrate a strong track record as landlords, with consistent rental income and well-maintained properties.

As we move forward, let's explore the strategic applications of HELOCs in rental property investments, including property acquisitions, renovations, and debt consolidation. Using a HELOC to purchase rental properties in high-demand markets could potentially generate returns that outpace inflation, making it a smart investment strategy.

Maximizing Rental Property Investments with HELOCs

Expanding Your Rental Portfolio

HELOCs offer real estate investors powerful strategies to grow their portfolios and increase returns. One of the most popular uses of a HELOC is purchasing additional rental properties. This strategy allows you to leverage the equity in your existing properties to acquire new ones without depleting your cash reserves.

For example, you could use a $100,000 HELOC as a down payment on a $400,000 property (assuming a 25% down payment requirement). This approach can significantly accelerate your portfolio growth compared to saving for each down payment individually.

It's important to carefully analyze potential properties. Look for areas with strong rental demand and favorable price-to-rent ratios. This financial metric evaluates the relative affordability of buying versus renting a property.

Boosting Property Value Through Renovations

Another effective strategy involves using HELOC funds to renovate and improve your existing rental properties. Strategic upgrades can increase both rental income and property value.

For instance, updating a kitchen in a rental property might cost $20,000 but could potentially increase monthly rent by $200–$300. Over time, this renovation could pay for itself and continue to generate additional income.

Try to focus on improvements that tenants value most. A recent report provides a comprehensive look at the home features and community amenities that renters can't live without and how much they are willing to pay for them.

Streamlining Finances with Debt Consolidation

Many real estate investors use HELOCs to consolidate high-interest debt related to their rental investments. This strategy can lower overall interest costs and simplify financial management.

For example, if you have $50,000 in credit card debt at 18% APR and a $30,000 personal loan at 12% APR, consolidating these with a HELOC at 7% APR could save you thousands in interest annually.

While this strategy can be effective, it's important to address the root causes of high-interest debt to avoid falling back into the same pattern.

Mitigating Risks and Maximizing Benefits

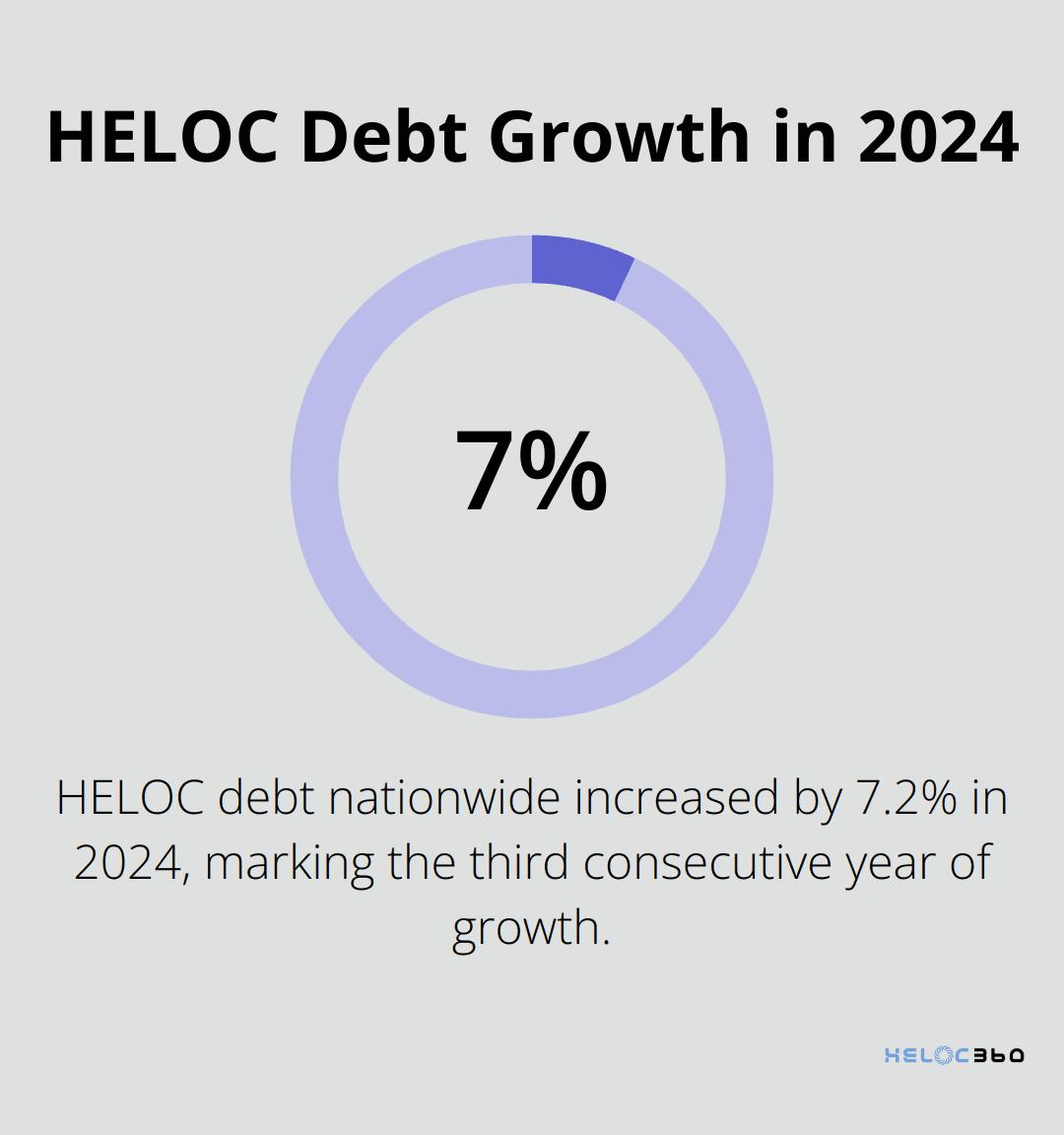

As you explore these strategies, it's essential to consider potential risks and plan accordingly. Variable interest rates on HELOCs can fluctuate, potentially affecting your cash flow. HELOC debt nationwide increased by 7.2% in 2024, marking the third consecutive year that HELOC balances have grown after a decade of decline.

To mitigate these risks, create a comprehensive financial plan that accounts for potential interest rate increases and changes in the rental market. Consider setting aside a portion of your rental income as a reserve fund to cover unexpected expenses or periods of vacancy.

In the next section, we'll explore the specific risks and considerations associated with using HELOCs for rental property investments, helping you make informed decisions as you grow your real estate portfolio.

Navigating HELOC Risks for Rental Properties

The Challenge of Variable Rates

HELOCs for rental properties come with variable interest rates, which can fluctuate based on market conditions. As of August 2025, rates can be as low as 7.750% APR for standard HELOCs and 8.750% for Interest-Only Home Equity Lines of Credit, assuming a 750 credit score.

To protect yourself from potential rate hikes:

- Negotiate a rate cap with your lender

- Include potential rate increases in your financial projections

- Explore options to convert a portion of your HELOC to a fixed-rate loan (if available)

Cash Flow and Debt Ratio Management

The use of a HELOC can significantly affect your cash flow and debt-to-income (DTI) ratio. While the initial draw period might only require interest payments, the repayment period can strain your finances without proper planning.

To maintain healthy cash flow:

- Create a detailed repayment plan before you draw funds

- Try to keep your front-end DTI ratio below 28% and your back-end DTI ratio below 36%

- Build a cash reserve equal to at least six months of HELOC payments

Navigating Tax Implications

The tax landscape for HELOCs on rental properties can be complex. Recent changes have altered the rules for interest deductibility.

Key tax considerations include:

- Interest deductibility (from 2018 through 2025, interest paid on HELOCs or home equity loans secured by your primary or secondary homes is potentially deductible, subject to certain conditions)

- Deduction limits ($750,000 for married couples filing jointly on total home loans, including HELOCs)

- Record-keeping requirements (meticulous documentation of HELOC fund usage is essential for tax purposes)

We at HELOC360 always recommend consultation with a tax professional to fully understand the tax implications of your HELOC strategy. The right approach can help you maximize deductions while maintaining compliance with IRS regulations.

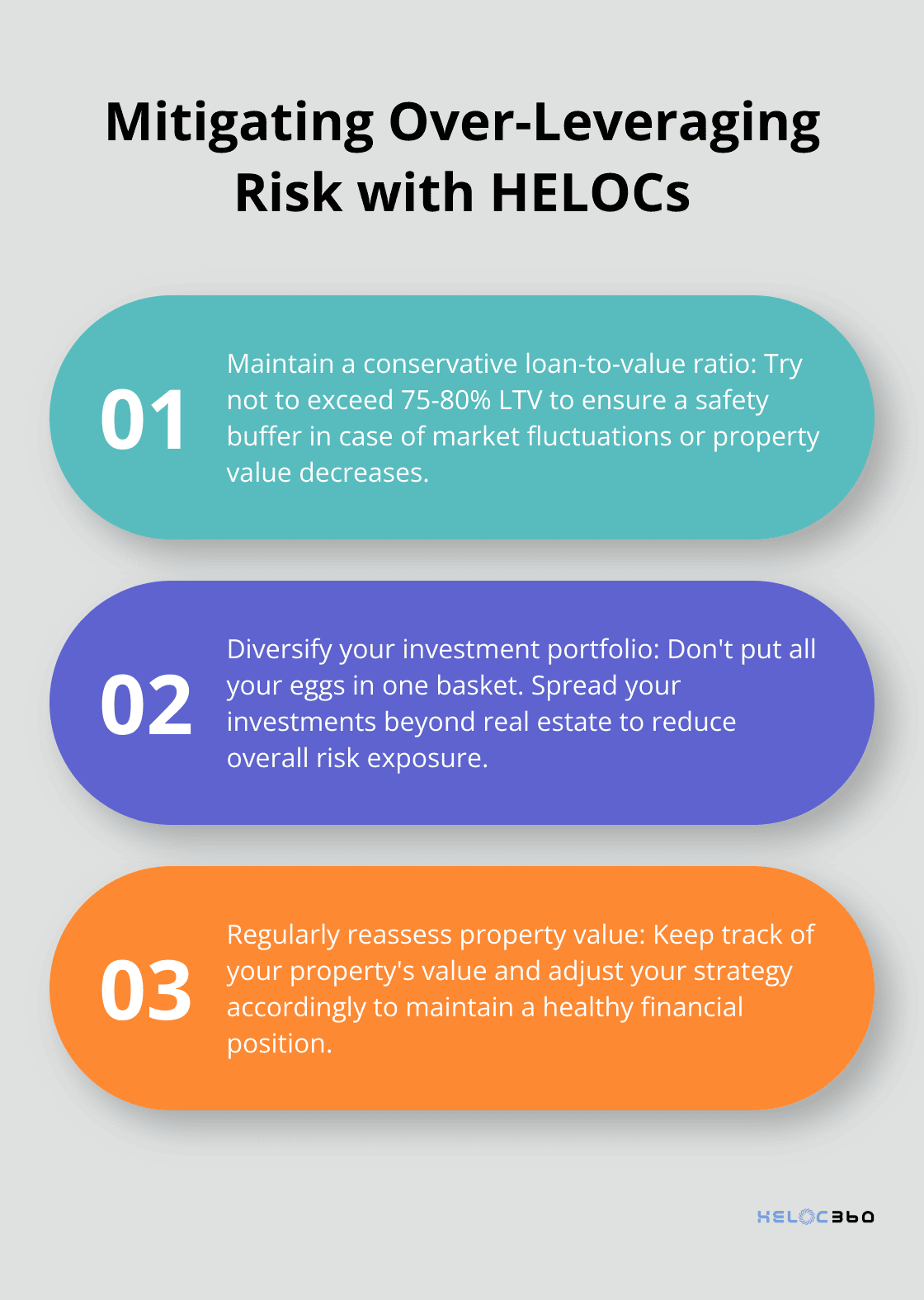

Risk of Over-Leveraging

Using a HELOC on your rental property can lead to over-leveraging if not managed carefully. This risk increases when property values decline or rental income decreases.

To mitigate this risk:

Market Volatility Considerations

Real estate markets can be unpredictable, and this volatility can impact your HELOC strategy. A downturn in the market could lead to decreased property values and potentially underwater mortgages.

To prepare for market fluctuations:

- Research local market trends thoroughly before investing

- Create a contingency plan for potential market downturns

- Consider long-term hold strategies rather than short-term flips when using HELOC funds

Final Thoughts

HELOCs for rental properties offer real estate investors a powerful tool to grow their portfolios and optimize finances. This flexibility allows investors to seize opportunities and potentially increase rental income and property values. However, using a HELOC for rental property investments requires careful consideration and planning due to variable interest rates, cash flow impacts, and tax implications.

Successful use of a HELOC for rental properties depends on informed decision-making and staying updated on market trends. Every investment decision should align with long-term goals and risk tolerance. A conservative approach, keeping loan-to-value ratios in check and preparing for market fluctuations, can help investors harness the benefits of a HELOC while minimizing risks.

We at HELOC360 can help you simplify the HELOC process and connect you with lenders that match your needs. Our platform provides tools and expertise to help you make informed decisions about leveraging your home equity. Exploring HELOC options could unlock new opportunities in your real estate journey, whether you're an experienced investor or just starting out.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.