Is Now the Perfect Time to Get a HELOC?

Table of Contents

Is now the perfect moment for a HELOC? At HELOC360, we've been closely monitoring the market conditions and economic factors that influence HELOC timing.

In this post, we'll explore the current landscape for home equity lines of credit, discuss the potential advantages of securing a HELOC now, and highlight important considerations for homeowners.

Whether you're a seasoned real estate investor or a first-time homeowner, understanding the timing of HELOCs can help you make informed financial decisions.

Are HELOC Rates Dropping?

The current market conditions for Home Equity Lines of Credit (HELOCs) create a favorable environment for homeowners. Several key trends make now an attractive time to consider a HELOC.

Interest Rates Show a Downward Trend

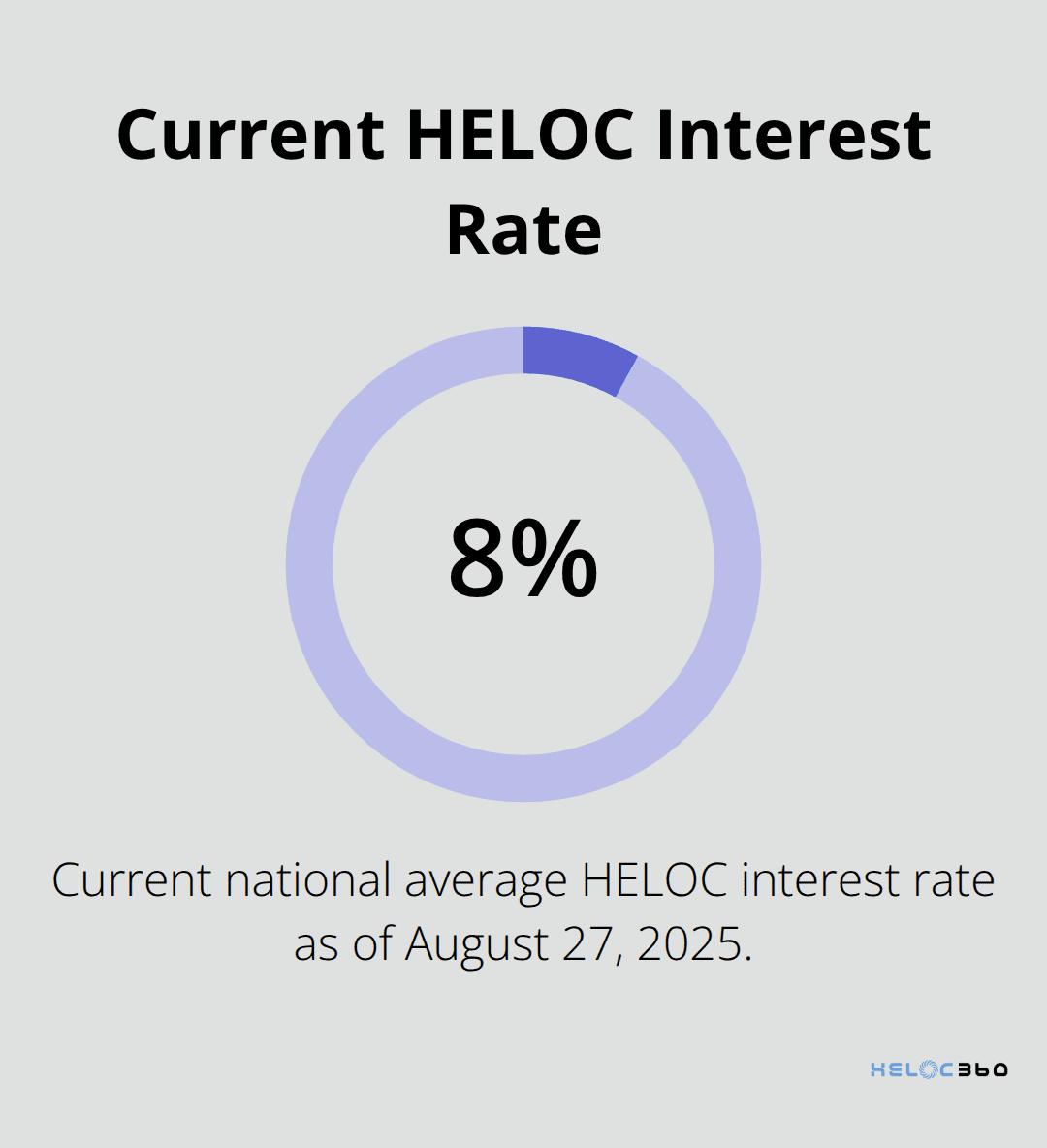

HELOC interest rates have decreased, reaching their lowest point since May 2025. As of August 27, 2025, the national average HELOC interest rate stands at 8.10% (according to Bankrate's latest survey of the nation's largest home equity lenders). This decline presents a window of opportunity for homeowners who want to tap into their home equity.

The Federal Reserve's decisions directly influence HELOC rates. With the Fed expected to reduce rates by 25 basis points in September, HELOC rates could drop even further in the coming months. This potential decrease makes it an ideal time to lock in a HELOC before rates potentially rise again.

Home Equity Levels Reach Record Highs

Across the United States, homeowners have accumulated significant equity in their properties. This surge in home equity provides a larger pool of funds that homeowners can potentially access through a HELOC. The average homeowner now holds approximately $185,000 in home equity (as reported by recent market analyses).

This increased equity not only allows for potentially larger HELOC amounts but also improves the chances of approval for many homeowners. Lenders typically require at least 15–20% equity remaining after the HELOC, so higher overall equity levels work in borrowers' favor.

Economic Factors Boost HELOC Availability

Several economic factors contribute to increased HELOC availability. Banks and lenders actively seek to expand their HELOC offerings due to the current economic climate. This competition among lenders can lead to more favorable terms and rates for borrowers.

Additionally, the housing market's stability has increased lenders' confidence in offering HELOCs. With home values holding steady or appreciating in many areas, lenders view HELOCs as a relatively low-risk product.

What This Means for Homeowners

For homeowners considering a HELOC, now presents an opportune time to explore options. The combination of falling interest rates, high home equity levels, and favorable economic conditions creates an ideal scenario for HELOC seekers. However, it's important to carefully assess your financial situation and goals before proceeding.

As we move forward, let's explore the specific advantages of getting a HELOC in the current market climate, and how these benefits can align with your financial objectives.

Why a HELOC Makes Sense Right Now

Unmatched Borrowing Flexibility

HELOCs offer unmatched flexibility. You can borrow any amount up to your approved limit and only pay interest on what you use. This feature proves particularly valuable in today's uncertain economic climate, where access to funds without the obligation to use them provides peace of mind.

Consider a home renovation project: a HELOC allows you to draw funds as needed, potentially saving you money on interest compared to a lump sum loan. This pay-as-you-go approach can revolutionize cash flow management during large projects or unexpected expenses.

Potential Tax Advantages

The interest paid on a HELOC may be tax-deductible if you use the funds for qualifying home improvements (subject to current tax laws). This potential tax benefit can significantly reduce your overall borrowing cost, making a HELOC an attractive option for homeowners who plan to reinvest in their properties.

For tax years 2018 through 2025, the deductibility of HELOC interest depends on how the funds are used. Many homeowners still benefit, especially when using the funds for substantial home renovations or additions that increase the property's value.

Competitive Rates Compared to Alternatives

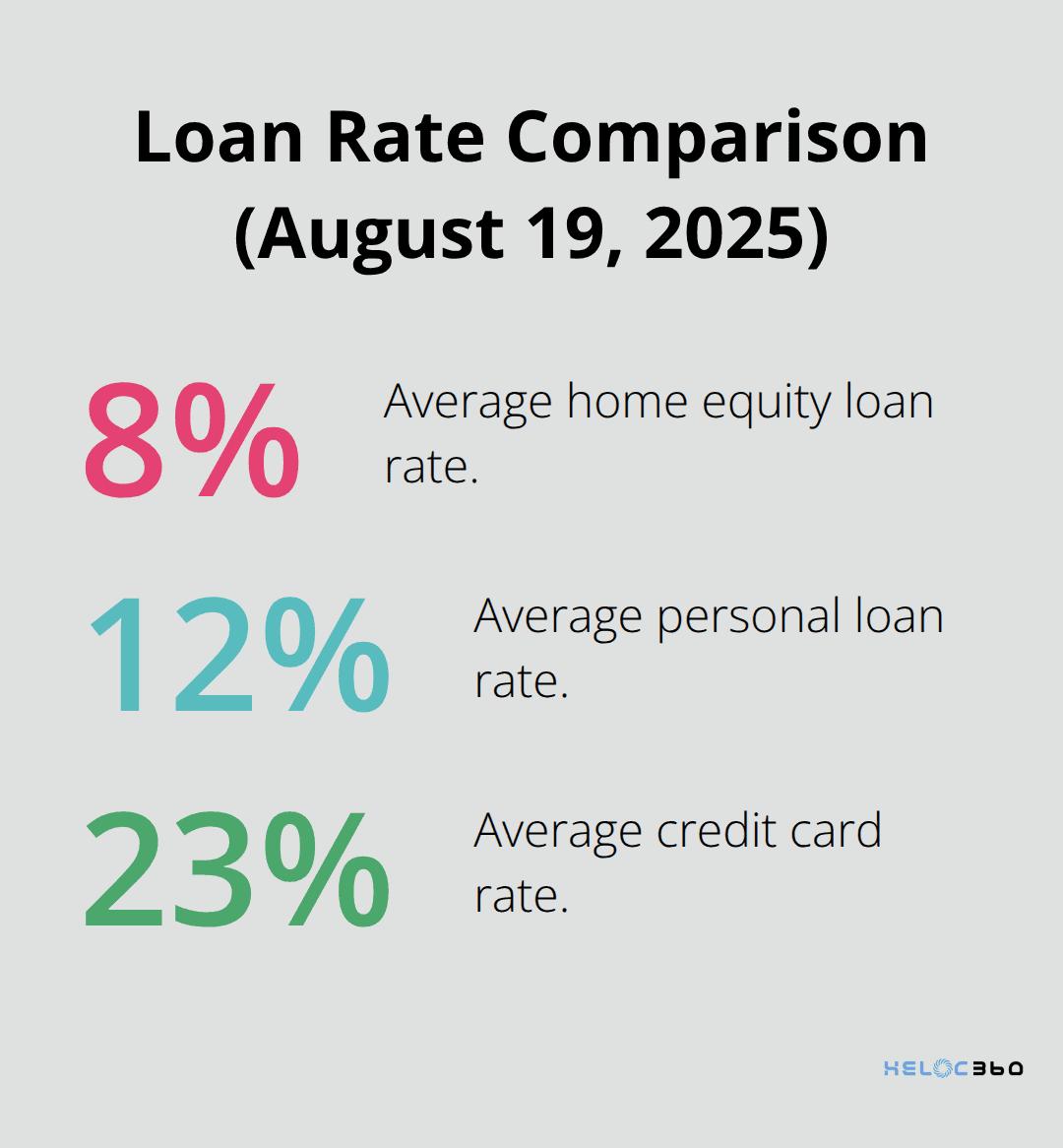

As of August 19, 2025, the average home equity loan rate is 8.23%, which sits significantly lower than the average personal loan rate of 12% or credit card rates approaching 23%.

This rate difference translates to substantial savings over time. On a $50,000 loan over five years, choosing a HELOC over a personal loan could save you thousands in interest payments. Many homeowners leverage these lower rates to consolidate high-interest debt, effectively reducing their monthly payments and accelerating their path to financial freedom.

With the Federal Reserve's recent statements on inflation and interest rates, HELOC rates could become even more attractive. This potential for changes in the economic landscape makes now an opportune time to consider a HELOC, as you could benefit from potential rate adjustments in the coming months without the need to refinance.

Leveraging Home Equity Wisely

The current market conditions, combined with the inherent flexibility of HELOCs and their competitive rates, create a compelling case for homeowners to consider this financing option. Whether you want to fund home improvements, consolidate debt, or create a financial safety net, a HELOC could serve as a smart choice in today's economic landscape.

As we move forward, it's important to understand that while HELOCs offer numerous advantages, they also come with certain considerations. Let's explore the factors you should weigh before deciding to get a HELOC.

Is a HELOC Right for You?

Evaluate Your Financial Health

Before you apply for a Home Equity Line of Credit, you must assess your current financial situation. A HELOC represents a significant financial commitment, so you need to ensure you can handle the payments.

Start by checking your credit score. Many lenders allow you to tap your equity with a credit score in the 600s, with some accepting scores as low as 620, especially for HELOCs. If your score falls below this threshold, focus on improving it before you apply. You can obtain your credit report for free from AnnualCreditReport.com.

Next, calculate your debt-to-income ratio (DTI). Lenders typically prefer a lower DTI. To determine your DTI, add up all your monthly debt payments and divide them by your gross monthly income. If your DTI is too high, consider paying down some existing debts before you pursue a HELOC.

Understand the Risks

Using your home as collateral involves significant risks. If you fail to make your HELOC payments, you could lose your home to foreclosure. This risk is real and demands careful consideration.

HELOCs often come with variable interest rates. While rates currently favor borrowers, they could increase in the future, potentially making your payments unaffordable. Before you commit to a HELOC, ensure you can handle potential rate increases.

Meet Qualification Requirements

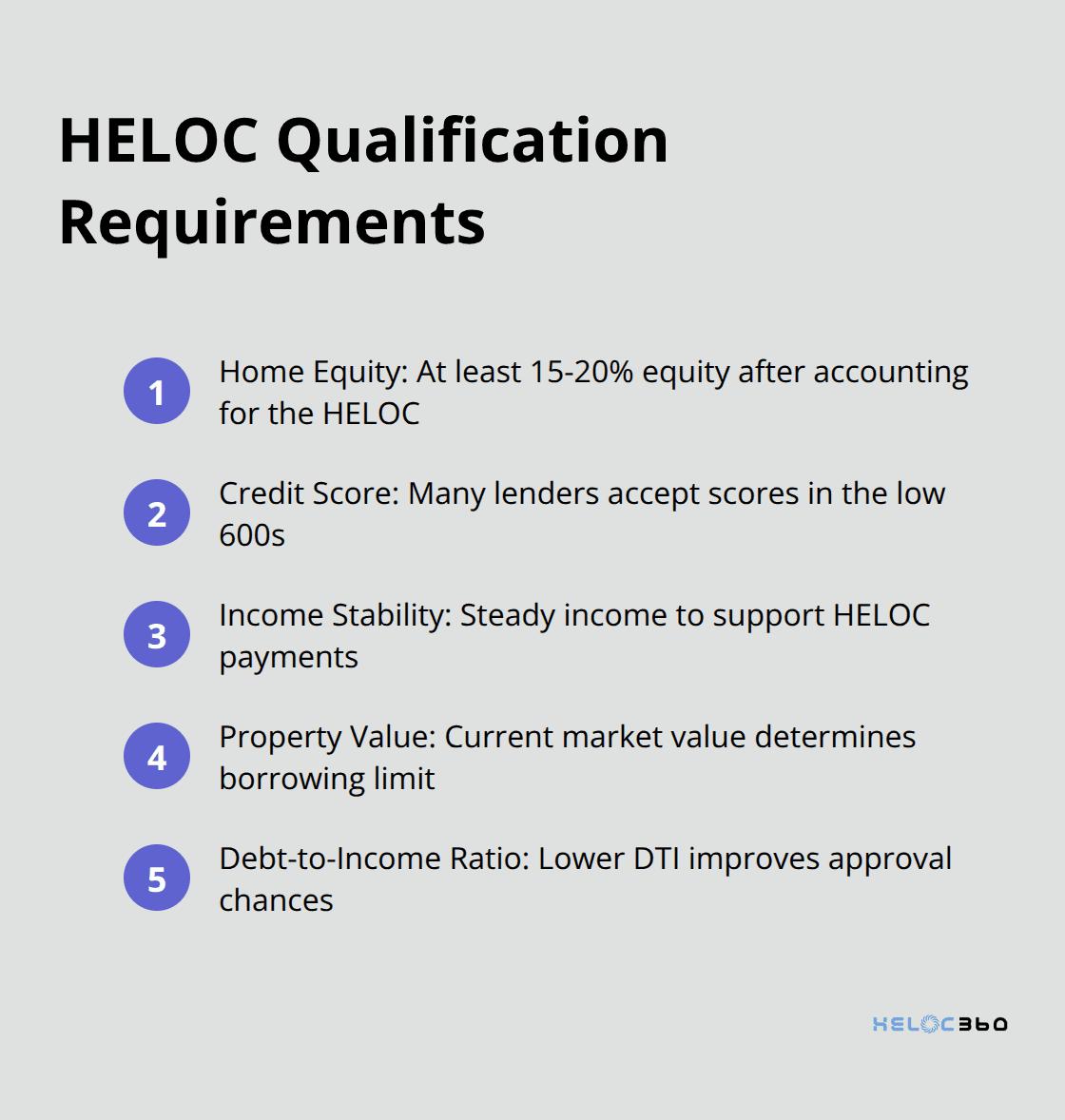

To qualify for a HELOC, lenders will examine several factors:

- Home Equity: You typically need at least 15–20% equity in your home after accounting for the HELOC.

- Credit Score: As mentioned earlier, many lenders now accept scores in the low 600s for HELOCs.

- Income Stability: Lenders want to see a steady income that can support HELOC payments.

- Property Value: An appraisal will determine your home's current market value, which affects how much you can borrow.

- Debt-to-Income Ratio: Keep your DTI as low as possible for the best chances of approval.

If you're self-employed, prepare to provide additional documentation. This might include tax returns, profit and loss statements, and bank statements from the past two years.

Consider Your Long-Term Goals

A HELOC can serve various purposes (home improvements, debt consolidation, or creating a financial safety net). However, you must align this financial tool with your long-term objectives. Consider how a HELOC fits into your overall financial strategy and whether it supports your future plans.

Explore Alternative Options

While a HELOC offers many benefits, it's not the only option available. Compare it with other financing methods like home equity loans, cash-out refinancing, or personal loans. Each option has its pros and cons, and the best choice depends on your specific financial situation and goals.

Final Thoughts

The current HELOC landscape offers a unique opportunity for homeowners. Interest rates have dropped to their lowest since May 2025, and home equity levels have reached record highs. These factors, combined with potential Federal Reserve rate cuts and increased lender competition, make HELOC timing particularly favorable right now.

A HELOC provides flexible borrowing, potential tax advantages, and competitive rates compared to other financing options. However, it's important to consider the risks, such as using your home as collateral and the variable nature of HELOC rates. Your decision should align with your long-term financial goals and current financial health.

We at HELOC360 aim to simplify the process of navigating home equity options. Our platform provides the knowledge and tools you need to make informed decisions about leveraging your home's equity. We connect you with lenders that match your unique needs, whether you're ready to apply for a HELOC or still exploring your options.

Related Articles

HELOC interest isn't always tax-deductible. Learn the IRS rules banks won't explain and avoid the $47,000 mistake most homeowners make with HELOC taxes.

Banks push cash-out refinances for higher profits, but HELOC vs cash-out refinance math often favors HELOCs - especially if you have a low 2021 rate.

HELOC tax deduction rules change in 2026. Learn the three scenarios, documentation requirements, and strategies banks won't explain.